Netlist (NLST) is back in the kind of fight that can move a stock fast. The company just opened fresh legal fronts against Samsung, and the new ITC complaint also names Alphabet's (GOOG) (GOOGL) Google, Nvidia (NVDA), Supermicro (SMCI), and Broadcom (AVGO). That keeps Netlist squarely in the middle of the AI memory story, where patents, pricing, and server demand all matter at once. Traders liked the headline. NLST jumped 12.6% to a $2.85 close on Friday following the news.

The new lawsuit is a big deal because it widens the target list and sharpens the AI angle. Netlist says the case is based on infringement of two patents tied to Samsung HBM products and Samsung DDR5 RDIMMs and MRDIMMs. The new ITC complaint pulls in Google, Supermicro, Nvidia, and Broadcom as additional respondents. Netlist is also seeking exclusion and cease and desist orders.

The bigger picture is simple. This is still a tiny company that can snuggle into a huge case against Big companies, but it now has real operating momentum too. That makes the story more interesting than just another patent slugfest.

About NLST Stock

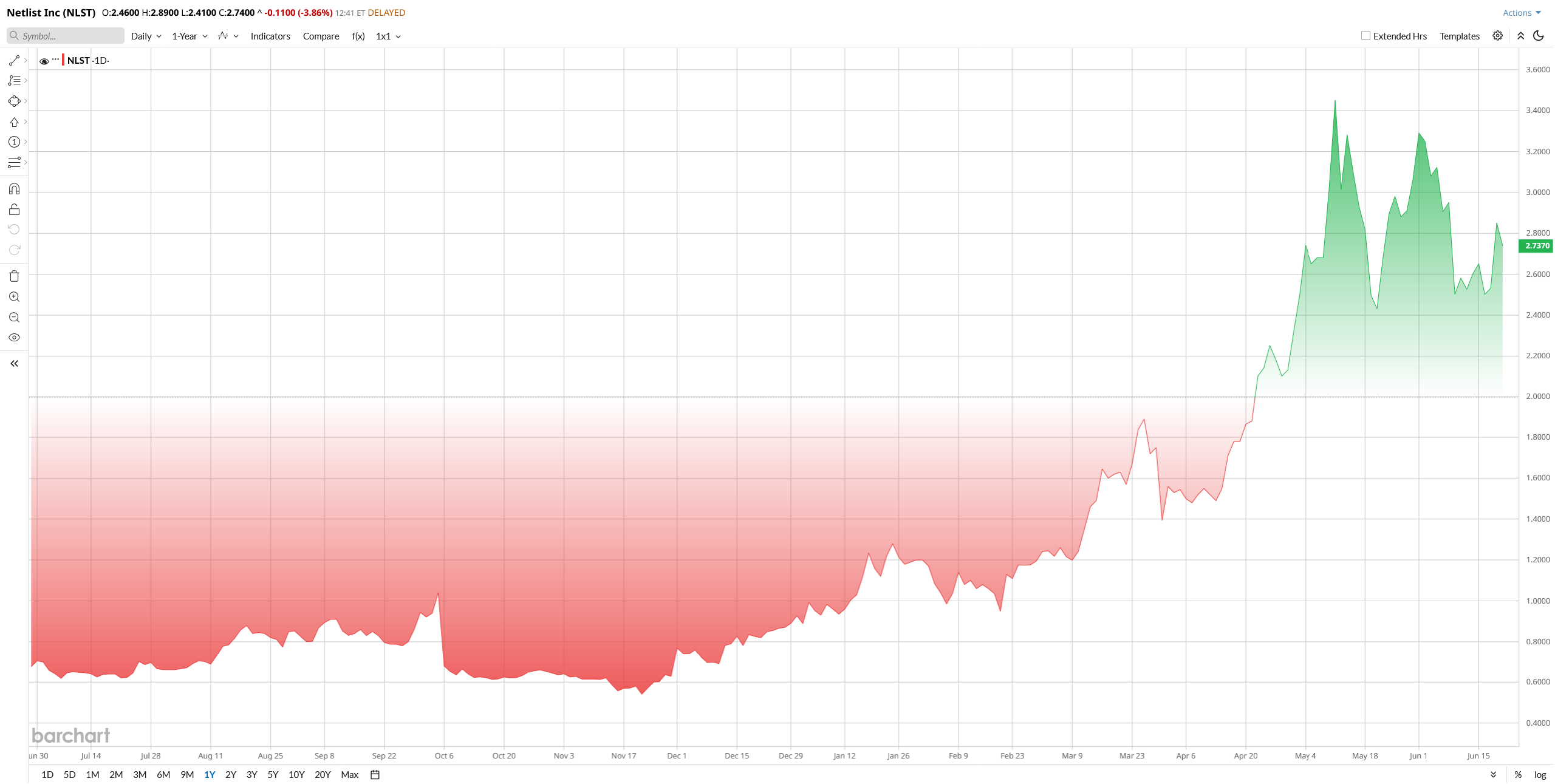

NLST stock has been outperforming the broader market in 2026. Shares have more than tripled year-to-date (YTD), due to the boom in AI-driven memory demand. The chart also says the stock is sitting above its 50-day moving average, but just below its 200-day moving average. That tells us the trend is still constructive, even after a big run. The technical setup is not broken. It is just choppy, which fits a stock tied to court dates and memory pricing as much as earnings.

Valuation is where things get tricky. Barchart puts Netlist at a price-to-sales ratio of 4.48 and a price-to-book ratio of 77.4. Those are not bargain numbers, especially for a stock with only $188.63 million in annual sales and a market cap near $951.6 million. So, NLST does not look cheap. It looks priced for more progress, more memory demand, and maybe a better outcome in the patent fight. If that story stalls, the multiple can shrink fast.

Netlist Beats Q1 Earnings Estimate

Netlist reported its Q1 earnings on May 12, which were quite impressive. First quarter revenue jumped to $104.9 million, up 262% year-over-year (YoY) from $29.0 million. Gross profit surged to $22.4 million from $1.3 million a year ago. Net income came in at $8.6 million, or $0.03 per share, versus a loss of $9.5 million, or $0.03 per share, in the prior year quarter. The company said the gains came from robust demand for memory products. It did not break out revenue by division in the release, so investors are left with the total picture rather than a segment map.

Read more: AI is “one of the largest industries ever” ...and it’s already disrupting this $1T market

CEO C.K. Hong summed it up well: “We remain well positioned to capitalize on AI memory technologies.” Netlist ended the quarter with $17 million in cash and cash equivalents and $10 million in restricted cash.

Recent News and Developments

Netlist is not just living in the courtroom. In 2026, the company has also pushed hard on policy and IP enforcement. It urged the United States Trade Representative (USTR) to take stronger action in the Section 301 probe into South Korea over semiconductor IP abuse. Hong said Netlist has spent hundreds of millions of dollars building foundational memory technology and argued that Samsung still ships infringing products without a license. Netlist wants revenue from products, but it also wants value from patents.

That is why every legal headline matters so much. One win, one settlement, or one licensing deal could change the financial picture quickly. One setback could do the opposite.

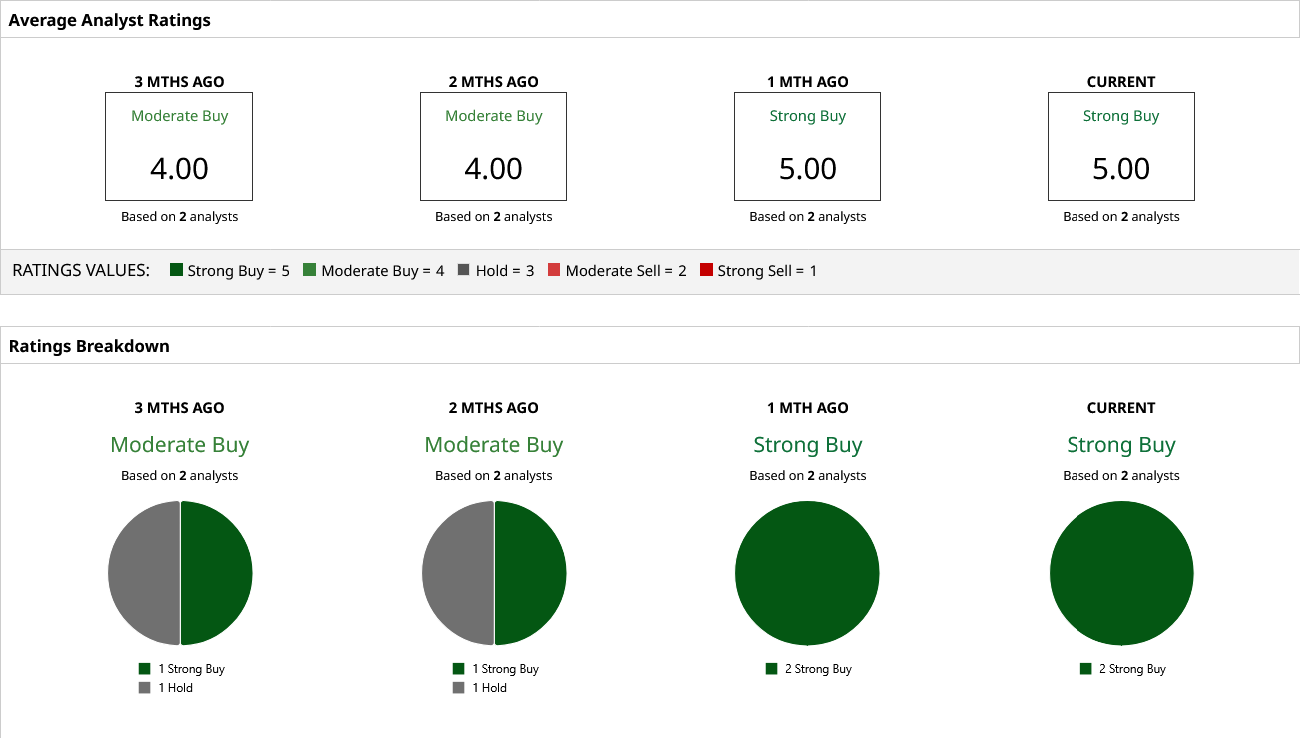

Analyst Opinions on NLST Stock

Wall Street coverage is still thin, but the tone is friendly. Barchart data shows a “Strong Buy” rating for NLST stock based on two analysts. It also shows an average 12-month target of $5.00. That implies about 79% upside from the current price.

Read more: This Pre-IPO stock is up 4,000% already

Roth MKM is the clearest public note here. It kept a “Buy” rating and raised its target to $5 from $3 after Q1, citing strong memory product sales and traction in AI server memory products. Earlier coverage from Roth had already lifted its target to $2 and then $3 as the patent case picture improved. That is the bull case in a nutshell.

The market is not just betting on memory demand. It is betting that Netlist can turn patents into cash.