CaliberCos (CWD) shares soared nearly 90% on Thursday after announcing plans of using part of its cash reserves to load up on Chainlink (LINKUSD) as part of a broader crypto treasury strategy.

According to Chris Loeffler, the company’s chief executive, this decision transforms CWD into a “diversified alternative asset manager” offering investors exposure to both “real and digital asset infrastructure.”

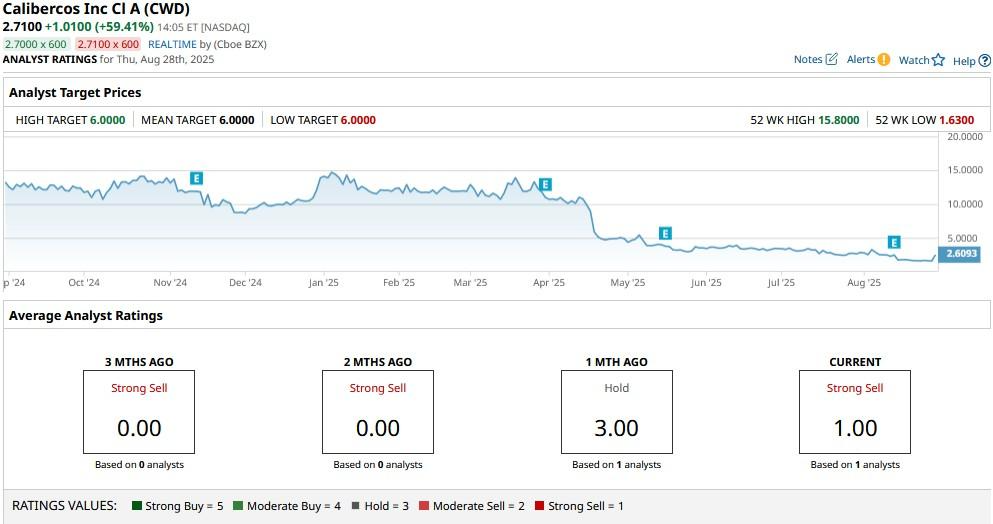

CaliberCos stock has been a disappointment for shareholders this year. Despite an explosive rally today, it’s down more than 80% versus its price at the start of 2025.

Why LINK Strategy Is Not a Reason to Buy CaliberCos Stock

Note that the massive surge in the CWD share price today following management’s decision to allocate treasury funds to Chainlink isn’t entirely justified.

Crypto treasury strategies are inherently speculative and expose companies to volatile assets with uncertain returns.

For serious investors, the announcement shouldn’t mean much since it doesn’t reflect operational strength or improved fundamentals. Simply put, it’s a financial bet, not a business breakthrough.

Without clear revenue growth, profitability, or strategic execution in its core business, CaliberCos shares remain prone to paring back today’s gains just as quickly as they were booked.

As famed investor Jim Cramer often warns, “speculation isn’t a strategy.” Investors should focus on sustainable value creation, not hype-driven price action tied to crypto headlines.

Momentum alone isn’t a reliable investment thesis.

CWD Shares Are Not Worth Touching With a 10-Ft Pole

CaliberCos stock remains unattractive despite the crypto treasury pivot since it’s flashing red flags that are too hard to ignore.

The real estate investment and asset management firm has received a delisting warning from Nasdaq due to negative $17.6 million in stockholders’ equity.

This minimum required to remain listed is $2.5 million.

Compounding the risk is the fact that CWD shares are barely covered by Wall Street analysts, leaving investors with little institutional insight or accountability.

In conclusion, with limited transparency, weak fundamentals, and a looming threat of delisting, CWD stock is operating in the shadows and should, therefore, be avoided despite the tempting short-term pop.