Healthcare stocks have lagged the broader market this year as investors chased higher-growth names in tech and AI. Dividend payers, in particular, have taken a hit amid shifting rate expectations and sector-specific hiccups. That backdrop sets up an interesting opportunity for income seekers who prize consistency over flash.

Take Abbott Laboratories (ABT). The stock sits 26% below its 52-week high of $139.06, trading near $102 per share. When will it bounce back? The short answer: the fundamentals already point higher, and the pullback looks more like a buying window than a warning sign.

The Quarter That Triggered the Slide

Abbott delivered full-year 2025 results in January that showed adjusted diluted EPS of $5.15, up 10% from the prior year. Revenue reached $44.3 billion, reflecting 5.7% reported growth and 6.7% organic growth when stripping out Covid-19 testing sales. Fourth-quarter adjusted EPS hit $1.50, a 12% increase, while sales came in at $11.5 billion.

The market focused on the top-line miss and nutrition softness. Shares dropped sharply afterward. Granted, that reaction stung for anyone watching the price ticker. Yet the company still expanded margins and generated roughly $2.6 billion in free cash flow for the quarter alone, according to MarketBeat data. Over the trailing 12 months, free cash flow totaled about $7.4 billion—more than enough to cover the $3.84 billion paid in dividends.

To put that in context, Abbott’s payout ratio sits at 45% of earnings and 36% of cash flow. That leaves plenty of room for continued growth without stretching the balance sheet.

Dividend King Status Remains Rock-Solid

Passive income investors value reliability above all. Abbott has now raised its dividend for 54 consecutive years, and the latest quarterly payout of $0.63 (annualized to $2.52 per share) yields 2.52% at current prices—more than double the S&P 500’s ($INX) 1.1% average.

Compare that track record to peers. Johnson & Johnson (JNJ) offers a slightly higher yield near 2.3% but slower organic growth. Medtronic (MDT) yields around 3.3% yet trades at a lower valuation because its growth lags Abbott’s recent pace. No matter how you slice it, Abbott stacks up as the growth-oriented Dividend King in the group.

Guidance Points to a Clear Rebound Path

Abbott laid out 2026 expectations alongside those results: organic sales growth of 6.5% to 7.5% and adjusted EPS of $5.55 to $5.80—10% growth at the midpoint. That guidance reflects confidence in medical devices (led by electrophysiology and diabetes care) plus established pharmaceuticals.

It also just completed the acquisition of Exact Sciences for $21 billion. The deal establishes Abbott as a leader in the fast-growing cancer screening and diagnostics segments and gives it access to millions of additional potential customers. Additionally, it gives Abbott a leading pipeline of next-generation cancer screening and diagnostics designed to detect cancer even earlier.

ABT stock now trades at a trailing P/E around 28, while the forward multiple sits closer to 19. That’s reasonable for a company projecting double-digit EPS gains and steady margin expansion of 50 to 70 basis points annually.

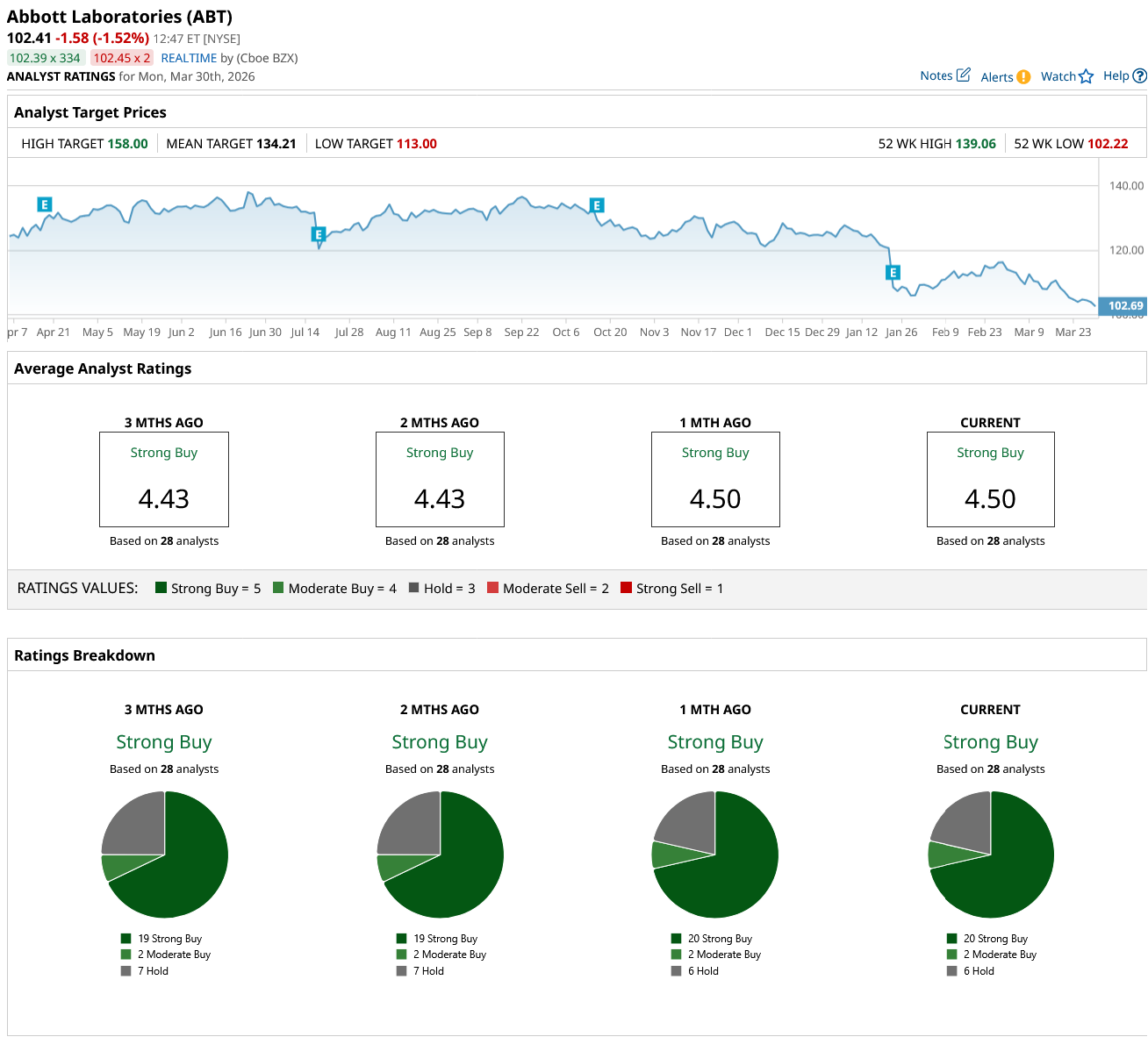

Analysts agree. Of 28 firms covering ABT stock, 20 rate it a "Strong Buy," giving it a similar consensus rating. Two analysts rate the stock a "Moderate Buy," and six say "Hold." There are no "Sell" ratings in the mix. The average 12-month price target of $134.21 implies roughly 32% upside potential from $102. High targets reach $158; the low sits at $113.

Key Takeaway

All in all, Abbott’s 26% pullback stems from one soft quarter and sector rotation—not cracks in the business model. With 54 years of dividend increases, robust free cash flow, and 2026 guidance calling for 10% EPS growth, the setup favors patient income seekers. Keep watch for ABT's earnings scheduled for April 16.

ABT stock may not snap back overnight, but the data show a company firing on the fundamentals that matter most for long-term safety and income. For yield hunters comfortable holding through temporary noise, this Dividend King looks like a compelling entry point today.