Peloton instructor Kendall Toole before one of her recent live rides. (Photo via author)

Not Just An Bike With An iPad Attached

With Peloton Interactive, Inc. (NASDAQ:PTON) in the news recently on speculation of a possible buyout, a point I made on my personal Twitter account recently bears repeating: Peloton skeptics underestimate the parasocial relationships Peloton users have with their instructors.

To some extent, Peloton instructors are already leveraging these relationships in their side hustles: for example, the one pictured at the top, former UCLA cheerleader Kendall Toole, is a pitchwoman for a plant-based protein bar company.

Perhaps under new management, Peloton will start to take advantage of these obvious sorts of brand extensions itself, while making them mutually profitable for their instructors. On Monday, our friends at the social data firm LikeFolio offered a few reasons why Peloton could find itself under new management soon. I've posted their email in full below; following that, a hedge in case Peloton's upcoming earnings disappoint, or there's a general market downturn.

Authored by Andy Swan at LikeFolio

Three reasons PTON could be acquired

Peloton (NASDAQ:PTON) stock is soaring today on reports of potential acquirers circling the company, including Amazon, Apple, Nike, Alphabet, and even Disney.

Here are three reasons we believe Peloton will make a very attractive buyout target and could spark a bidding war:

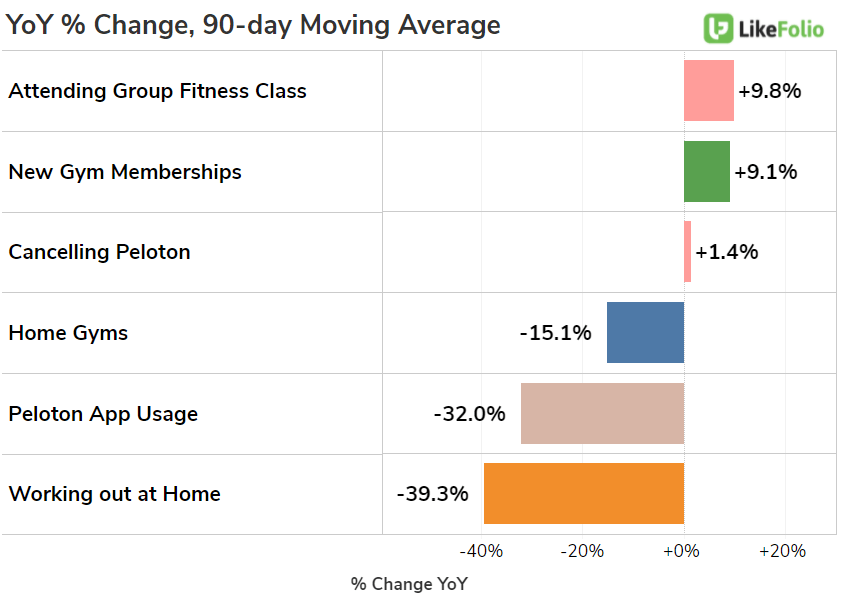

1. Macro trends have put the stock on sale

During the pandemic, we saw a massive shift in consumer behavior around exercise.Gyms were shut down or avoided, and “working out at home” became one of the fastest-growing trends in our universe.

Peloton (PTON) was at the perfect place at the perfect time and capitalized on this incredible demand surge in a big way.

But now – the tide has shifted.

Americans are “moving on” from COVID – and returning to some of their normal pre-pandemic activities.

Working out at home has taken a back seat to getting out there and joining a gym or attending a group fitness class in person.

In other words… things are normalizing.

A savvy acquirer likely knows that, like the pandemic-fueled move TO Peloton, this move AWAY from Peloton-beneficial macro trends is likely overdone as well.Wall Street has panicked and put PTON stock on sale.

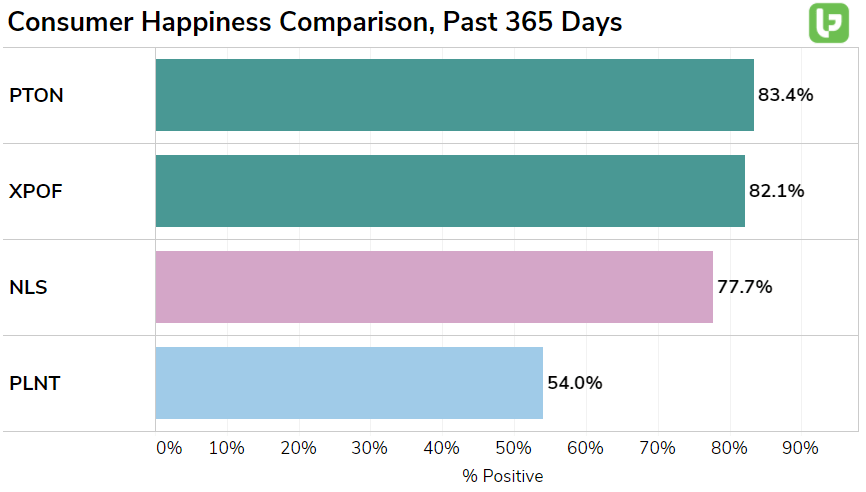

2. Consumers LOVE Peloton

Peloton has one of the highest consumer happiness levels of any company in our coverage universe.

This holds up nicely against competitors – both in the home workout space as well as chain gyms:

Despite the jokes about Peloton’s being a “stationary bike with a mounted iPad”, Peloton users love their equipment and the content.

This engaged audience means Peloton’s subscribers are unlikely to cancel their monthly service, as evidenced by the company’s historical monthly churn rate of under 1%.

Acquirers love subscription revenue models with low churn – and Peloton’s consumer happiness levels make it an attractive target.

3. The COMPANY is performing well

Wall Street got it wrong during the pandemic and priced PTON as if the company would grow at that pace forever.

Forget the stock for a moment…. It’s suffering from unrealistic investor expectations.An acquirer will care about how the company itself is doing.

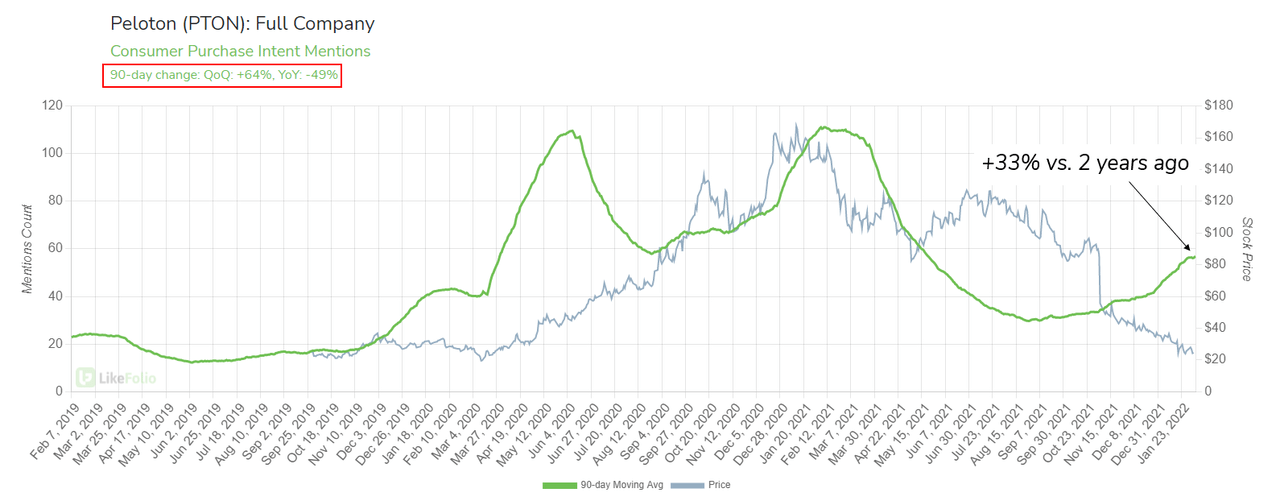

LikeFolio consumer insights data suggests that consumer demand is strong.

If you remove the insanity of the pandemic, you can see that Peloton is showing consumer demand levels that have increased by 33% vs the same time period 2 years ago.

That’s right – despite an enormous level of pull-forward demand in 2020 and 2021, Peloton still has more overall demand for its products than it did before the pandemic began.

On top of that, the company showed an impressive ability to scale to meet booming demand – and added a huge base of monthly subscribers to its subscription-based revenue model.

Not bad, not bad at all.

Bottom Line?

While the macro winds have shifted against Peloton for the moment, Wall Street’s panic is just as overdone as its euphoria a month ago.

Peloton’s ability to create and maintain a large base of very happy subscribers will continue to make Peloton an attractive acquisition target for many suitors in the near future.

Authored by David Pinsen at Portfolio Armor

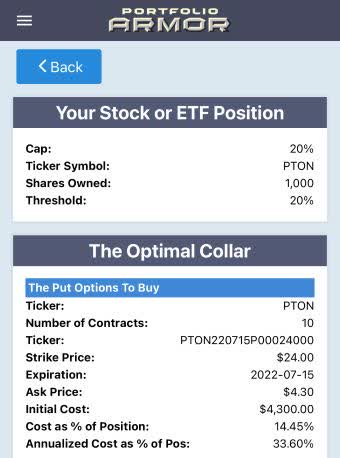

A Hedge For Peloton Longs

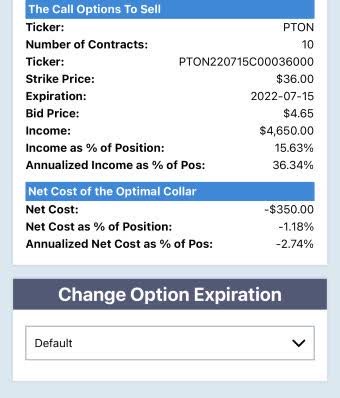

As of Monday's close, this was the optimal collar to hedge a thousand shares of Peloton against a greater-than-20% drop over the next several months, while not capping your upside potential at less than 20%.

Screen captures via the Portfolio Armor iPhone app.

Here, the cost was negative, meaning you would have collected a net credit of $350 when opening this hedge, assuming, to be conservative, that you placed both trades at the worst ends of their respective spreads (buying the puts at the ask and selling the calls at the bid). In practice, since you can often buy and sell options at some price within the spread, you would likely have collected a larger net credit.