A little-known provision of the Internal Revenue Code — Section 721 — lets investors with concentrated stock positions contribute shares into a partnership structure without triggering capital gains. Here's how it works, who it's designed for, and what separates modern income-generating structures from traditional exchange funds.

Engineers at Google, Meta, and Nvidia regularly accumulate seven-figure stock positions through RSUs and options. Over time, a single position can come to represent the majority of their investable net worth. The math is clear: diversification reduces portfolio risk. But any financial advisor will also confirm the practical complication — selling highly appreciated stock creates an immediate and often substantial tax bill.

This is not a niche problem. It's a structural feature of equity-heavy compensation that affects hundreds of thousands of technology professionals. Section 721 of the Internal Revenue Code offers one path through it.

What Section 721 Actually Says

The statutory language is concise. Section 721(a) states: "No gain or loss shall be recognized to a partnership or to any of its partners in the case of a contribution of property to the partnership in exchange for an interest in the partnership."

In plain terms: when you contribute appreciated stock to a qualifying partnership structure in exchange for a partnership interest, no taxable event occurs at the time of contribution. The gain is deferred — not eliminated. It remains embedded in your partnership interest and will eventually be recognized when the asset is sold or distributed.

Congress designed Section 721 to allow asset pooling without creating a tax barrier at formation. The policy logic: the investor has not received cash, has not cashed out, and has not realized an economic gain in the conventional sense. They have simply changed the form of ownership.

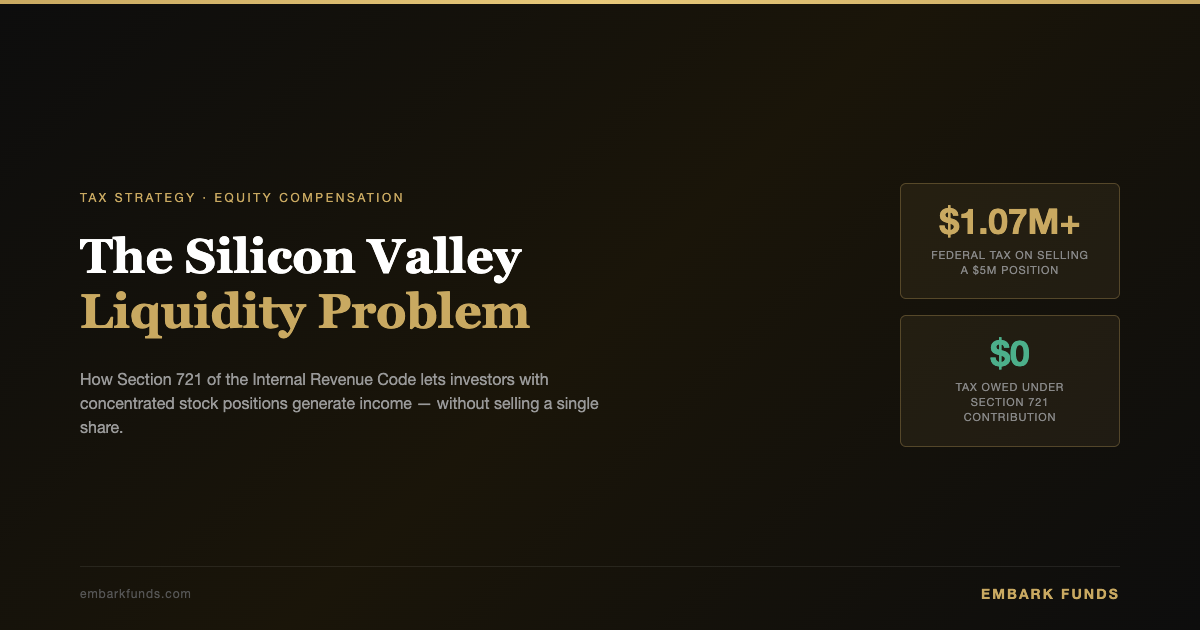

The Tax Math on a $5M Position

To understand why this matters, consider a straightforward example. An engineer holds $5 million in a single stock with a $500,000 cost basis — a common scenario for someone who joined a major tech company a decade ago.

Federal tax on sale

(20% LTCG + 3.8% NIIT on $4.5M gain)

Tax owed at contribution

under Section 721

For California residents, the combined federal and state rate approaches 37.1% — adding California's 13.3% on top of federal long-term capital gains tax. On a $4.5 million gain, that translates to a tax bill of approximately $1.67 million due in the year of sale.

Important clarification: Section 721 provides tax deferral, not elimination. The cost basis carries over to the partnership interest (Section 722) and to the contributed property inside the partnership (Section 723). When the asset is eventually sold — by the partnership or after distribution — the deferred gain is recognized and taxed at that time.

How the Contribution Process Works

The mechanics are more straightforward than the statutory language might suggest. When structured correctly, a Section 721 contribution follows a defined sequence:

- Identify the concentrated position The investor holds appreciated publicly traded stock with a low cost basis relative to current market value.

- Identify a qualifying partnership structure The fund must be structured to avoid the Section 721(b) "investment company" exception — typically by holding at least 20% of its assets in illiquid investments such as commercial real estate.

- Execute an in-kind transfer Shares are transferred via ACAT or DTC directly from the investor's brokerage account into the partnership's custodial account. No sale occurs. The investor receives a partnership interest proportional to the fair market value of the contributed shares.

- Basis mechanics activate The investor's basis in their partnership interest equals their original cost basis (Section 722). The partnership takes the same carryover basis in the contributed property (Section 723). The built-in gain is preserved in both.

- Partnership manages and generates returns Depending on the fund structure, the partnership may hold the shares, execute income-generating overlay strategies, or pool contributions with other investors for eventual diversification.

For a detailed walkthrough of the transfer mechanics, see The Complete Guide to In-Kind Transfers.

Exchange Funds vs. Income-Generating Structures

Most public discussion of Section 721 centers on exchange funds — limited partnerships where multiple investors pool concentrated stock positions. After a mandatory 7-year holding period (required under Section 731(c) to avoid gain recognition on marketable securities), each investor receives back a diversified basket of all contributed stocks rather than their original shares.

Goldman Sachs and Morgan Stanley (through its acquisition of Eaton Vance) have historically operated major exchange fund programs, typically requiring qualified purchaser status and $5M+ minimum contributions.

The tradeoffs are meaningful: investors give up their specific position, accept a 7-year lockup, pay annual management fees of roughly 0.75%–1.25%, and receive no income during the holding period.

"Exchange funds solve the diversification problem. They don't solve the income problem."

A different category of Section 721 structure focuses on income generation rather than diversification. Rather than pooling shares with other investors and waiting 7 years, these vehicles accept in-kind contributions and deploy overlay strategies — covered calls, securities-backed lending, and yield generation — targeting consistent annualized income while the investor maintains exposure to their original position. The concentrated stock is not sold, and no diversification is forced.

Embark's SPV model is built on this approach — embarkfunds.com — targeting annualized income without requiring investors to exit their position or accept a multi-year lockup.

Key Statutory Guardrails

Three provisions of the tax code govern how Section 721 contributions are structured and where they can fail:

| Rule | What It Does | Practical Impact |

|---|---|---|

| §721(b) | Investment company exception | Gain is recognized if contribution creates diversification in a primarily securities-holding fund. Solved by 20%+ illiquid assets. |

| §704(c) | Built-in gain allocation | Pre-contribution gains are allocated back to the contributing partner — they cannot be shifted to other partners. |

| §707(a)(2)(B) | Disguised sale rule | Distributions to the contributing partner within 2 years of contribution may be recharacterized as a taxable sale. |

Who This Strategy Is Designed For

Section 721 itself has no investor qualification requirement — the statute applies broadly. However, the funds and private partnership structures that use it are private placements under Regulation D, restricted to accredited investors ($1M+ net worth excluding primary residence, or $200K+ annual income) or qualified purchasers ($5M+ in investments).

The profile of an investor for whom this strategy is relevant typically includes: a single publicly traded position of $1M or more, significant unrealized appreciation relative to cost basis, and a desire for income or liquidity without triggering a taxable event. Technology professionals holding concentrated RSU positions represent the clearest use case — for a full overview of applicable strategies, see RSU Strategy for Tech Employees.

A Note on Tax Advice

Section 721 strategies involve complex tax and securities law. The mechanics described here are educational and reflect general statutory provisions. Individual outcomes depend on specific facts — cost basis, holding period, state of residence, fund structure, and other variables. Investors should work with qualified tax counsel before executing any contribution strategy.

For a full technical breakdown of the contribution mechanics and IRS basis rules, see What Is a Section 721 Contribution Strategy?

See What Your Concentrated Position Could Generate

Model income potential, downside protection, and retained upside — without selling a single share.

Learn More at embarkfunds.com