In reporting on the housing crisis, I often hear some version of a simple story purporting to explain why so many Americans struggle to afford a place to live. The story goes like this: Housing costs are unaffordable because [INSERT BAD COMPANY HERE] is greedy and jacking up prices. The villain can be Airbnb or developers; it can be deep-pocketed foreigners or iBuyers. The story is compelling because it does not directly implicate regular people, sympathetic institutions, or elected officials.

To state the obvious, stories can be compelling without being true. Especially suspect are stories that scapegoat a group or an entity that is impossible or at least very difficult to defend: banks or oil companies or criminals, say. The scapegoat takes the blame for a complex problem. The trick is to cast a villain such that the surrounding facts become irrelevant. Who cares whether criminals have actually destroyed American cities? Attempting to stress-test theories like this just makes you look pro-crime and puts you on the same side as people who have committed terrible acts. But false narratives are dangerous because they distract attention from real problems, and plausible solutions.

The latest version of the housing-villain story targets private-equity firms and hedge funds, broadly “institutional investors” that have supposedly been outcompeting regular homebuyers and are therefore responsible for the skyrocketing rents and home prices of 2020 and 2021. “One of the largest hedge funds, the largest Wall Street firms in the world, is going around and buying up every single-family home in this country,” J. D. Vance argued at the start of his senatorial campaign in 2021, noting that first-time homebuyers, disproportionately Black Americans, were unable to become homeowners as a result.

I don’t want to be hyperbolic, but the idea that these firms are ultimately responsible for our housing-affordability crisis is absolutely ridiculous, and no one who knows anything about housing markets believes it. Yet this story has gained so much traction that it has spawned hearings and bills on Capitol Hill. One recent effort by Senator Jeff Merkley of Oregon seeks to levy high taxes on any company owning more than 100 single-family homes, in order to push it to sell those homes to owner-occupants or smaller investors. I asked Merkley what drew his attention to hedge-fund activity in the housing market, and he told me that he had “started to hear from people in the neighborhood saying, ‘Here’s the problem: We’re competing when we’re looking for a home; we’re competing against all-cash offers from businesses’ … It brought me back to thinking about whether we should have American families having to compete against billionaires to have a place to rent or to buy.”

In order to have the type of pricing power that would allow any entity to push up rents and home prices, it would need to own significant shares if not an outright majority of homes in a particular market. At the national level, this is obviously not happening. According to one report, institutional investors purchased just 3 percent of homes sold in 2021. At the state level, the story seems unlikely as well. Georgia, a state with a relatively high amount of investor activity, saw some 8.5 percent of 2021 home sales go to the largest investors, according to CoreLogic data. In Merkley’s home state, just 2 percent of sales went to “mega-investors,” who own 1,001 or more properties. But 8 or 2 percent of home sales doesn’t mean 8 or 2 percent of the total housing stock—far from it. After all, most homes aren’t up for sale; from year to year, a great majority of homes remain in the same hands. Further, a purchase does not mean a permanent holding. Investors in both states quite likely went on to sell some of these homes.

At any rate: Home prices and rents increased quickly across the country, in communities large and small. When trying to determine what is responsible for this phenomenon, you have to find an explanation that is common to all of these places, not one that is particular to this market or that one. From August 2020 to August 2021, Nevada, Arizona, Utah, Montana, and Idaho, saw the most significant home-price increases, but of those states, just the first two saw relatively high rates of mega-investors, again according to CoreLogic data. (2021 data shows that Arizona saw the highest at roughly 8.9 percent of homes on the market going to mega-investors.)

Additionally, some proponents of the scapegoat story argue that even if institutional investors are not dominant at the state level, they could still be distorting local real estate. Someone looking for a three-bedroom single-family home in the suburbs of Atlanta is not equally satisfied with one in the Savannah suburbs, so what matters to that person is the local context. But just because something is theoretically possible doesn’t mean it’s actually happening. And these theories imbue investors with a mastermind quality that they frankly haven’t earned. For instance, fearmongering about Zillow buying up real estate fell flat when the company exited the market after off-loading many homes at a loss.

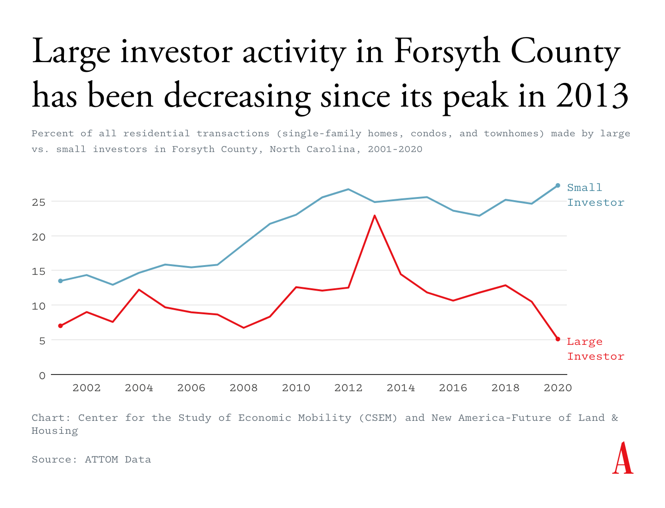

If there are no solid data supporting the institutional-investor-scapegoat story, there are certainly plenty of misleading statistics. Here’s one egregious example: A report from the House Financial Services Committee reads that “in the third quarter of 2021 alone, institutional investors bought 42.8% of homes for sale in the Atlanta metro area and 38.8% of homes in the Phoenix-Glendale-Scottsdale area.” These are unbelievably big numbers, and they are—literally unbelievable, that is. The citation provided in the document was not correct, but I was able to find the relevant report and, wouldn’t you know it, that’s not what it says. The report shows only the share of purchases made by investors, not institutional investors. Why does this matter? Because investors include people or entities who own fewer than 10 properties, midsize investors who own 10 to 99 homes, iBuyers—which buy properties and then immediately resell them—and even people who purchase vacation homes through an LLC. Relatedly, a New America report last year of investor activity in North Carolina suggests that investor growth in that market is actually being driven by smaller players.

I’ve seen this type of bait and switch more times than I can count. Instead of being clear that institutional investors make up just a small fraction of total investor purchases, politicians conflate statistics, tangling up true facts with a predetermined story. At an event on the rise of institutional investors, Marcia Fudge, the secretary of the U.S. Department of Housing and Urban Development, noted that in Cleveland’s eastern inner-ring suburbs, “investors have purchased nearly ⅓ of homes every year since 2015.” This is not as blatant as the House committee report, because Fudge was careful to say merely “investors.” But in the context of her remarks, given at an event titled “Institutional Investors in Housing,” the implication was that private-equity firms or hedge funds were taking over Cleveland.

This bait and switch matters. First, because it reveals a lack of rigor when people find data to fit a preordained narrative instead of looking to determine what is actually happening. Second, because if these homes are being bought by a wide range of investors, this reduces even further the likelihood that any single investor has significant enough market share to mess with prices.

The other deceptive part of the latest scapegoat story is that these institutional investors are regularly outbidding homebuyers with all-cash offers. Although all-cash offers are certainly on the rise, many of these bids are from wealthy people, house flippers, or smaller landlords. And one survey of realtors found an average “0% difference in offer price of institutional buyers compared to other buyers.” In 2021, according to a recent report, the “median purchase price of institutional buyers [was] typically 26% lower than the states’ median purchase prices,” suggesting that they are not typically competing with ordinary individual buyers, anyway. Institutional investors tend to specialize in distressed communities. In these markets, they can take advantage of economies of scale in making repairs.

There are real problems with corporate landlords. For instance, large corporate investors are significantly more likely to file eviction notices “even after controlling for past foreclosure status, property characteristics, tenant characteristics, and neighborhood,” according to a study of Fulton County, Georgia. As the sociologist Esther Sullivan has argued, corporate investors may also take advantage of mobile-home owners, who tend not to own the land beneath their unit, by escalating fees for the maintenance of park properties.

These problems are worth solving by, say, increasing resources for code enforcement so that landlords of all stripes are held accountable for not keeping their properties habitable. Local governments should also create rental registries that can track important information about properties and landlords to allow for both careful study and accountability of bad actors. The urban-policy expert Bruce Katz and his co-authors have also recommended that states require LLCs to disclose beneficial owners—anyone who owns more than 25 percent of the entity.

But if some institutional investors make bad landlords, that doesn’t mean they’re behind the housing-affordability crisis. They are not why rents are so high or why homeownership is out of reach for so many. Investors are not driving the unaffordability; they are responding to it. Many different investors are all flocking into the housing market; what is most relevant is the fundamental reason they are all being drawn there.

Housing is primarily unaffordable in this country because of persistent undersupply. In fact, institutional investors are entering the single-family-home market precisely because supply constraints have led to skyrocketing prices. One institutional investor’s SEC filing admitted just that, celebrating a “decline” in supply that has “driven strong rental rate growth and home price appreciation.” The filing also lamented the possibility that “continuing development … will increase the supply of housing and exacerbate competition for residents.”

A lack of supply is caused by a complex web of rules and regulations that prevent developers—profit and nonprofit alike—from building enough housing to meet demand. A recent report from Freddie Mac estimates a shortage of 3.8 million housing units. For decades the United States has been underbuilding in employment hubs (such as San Francisco, New York, and Boston) and the surrounding suburbs, pushing prices up. Elected officials have allowed the home-building process to become hijacked by unrepresentative opposition and gummed up in legal challenges, many under the guise of bogus environmental concerns.

If elected officials want to fix the problem, they should eliminate those constraints, such as bans on duplexes, triplexes, and multifamily buildings. And they should curtail the various legal pathways that are used to obstruct new housing. As the Brookings Institution expert Jenny Schuetz explained to the House Financial Services Committee last summer: “Targeting a small subset of landlords without addressing underlying market conditions and policy gaps will not meaningfully improve the well-being of renters and prospective homebuyers.”

As I’ve followed the scapegoat story, I’ve also been struck by the implicit suggestion that renters are less worthy of single-family homes than owner-occupants are. After all, corporate landlords rent to real people. In his announcement speech, Vance made the implicit explicit, arguing, “If you can’t own a home in your community, you’re not a real citizen.” And Merkley’s bill, which hopes to transfer single-family-rental homes to owner-occupants, skates past what its success would mean for renters. One report indicates that 85 percent of single-family-rental residents would not qualify for a mortgage.

I asked Merkley’s office what would happen to the families renting these properties if his bill were to pass and large investors were forced to sell them off. His office pointed me to a provision that would create down-payment assistance for potential homebuyers, and argued that pushing investors out of the market would reduce rents. But down-payment assistance doesn’t change the fact that most of these renters don’t have the credit score to qualify for a mortgage, nor would the assistance necessarily go to the families settled in these homes now. And I hope by this point it’s clear that even if institutional investors exited these markets, that would not make a dent in home prices or rents. Notably, a similar policy in Hong Kong led to a reduction in short-term speculation but did “not effectively cool down housing prices.”

Private equity isn’t the first villain, and it likely won’t be the last, to be cast in the role of the housing scapegoat. Airbnb, foreign buyers, greedy developers—all of these groups have taken center stage and probably will again. Nobody needs to defend these entities, but playing whack-a-mole with the villain of the moment won’t increase the amount of affordable housing we build, it won’t untangle the uncomfortable matrix of interests that opposes change and growth and opportunities for first-time homebuyers, and it won’t satisfy the growing anger of the tens of millions of Americans spending more than 30 percent of their income on housing.

The political project of building enough affordable housing and enacting necessary tenant protections is a hard one. Don’t let make-believe villains distract you from the real solutions to the housing crisis. We have to build.