European markets edge higher

Despite a wobble when Wall Street moved into negative territory during the afternoon, European markets have, for the most part, managed to keep their heads above water after recent declines. Mining companies supported the FTSE 100, following upbeat Chinese trade data, while in Europe airlines benefited from the continuing falls in the oil price. The final scores showed:

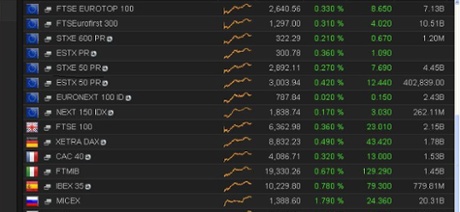

- The FTSE 100 finished 26.27 points or 0.41% higher at 6366.24

- Germany’s Dax added 0.27% to 8812.43

- France’s Cac closed 0.12% higher at 4078.70

- Italy’s FTSE MIB dipped 0.32% to 19,139.08 as the Bank of Italy said it saw downside risks to the government’s 2015 GDP forecasts

- Spain’s Ibex ended 0.36% better at 10,187.3

In the US, the Dow Jones Industrial Average is currently down 22 points or 0.14%.

And with that, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Bundesbank president Jens Weidmann continues to be at odds with ECB president Mario Draghi over how much stimulus the bank should provide to prop up the ailing eurozone economy, judging by his latest comments today.

ECB's Weidmann: Some ECB Policies Have Reached Edge Of Mandate

— Live Squawk (@livesquawk) October 13, 2014

#ECB's Weidman sticks to the hawkish script in that 'rates shouldn't stay low for longer than needed', BUT no mention of Draghi fallout

— RANsquawk (@RANsquawk) October 13, 2014

*WEIDMANN: CREDIBILITY OF FISCAL RULES AT RISK IF STRETCHED MORE

— Michael Hewson (@mhewson_CMC) October 13, 2014

Weidmann is also unhappy at the idea of France postponing its adherence to EU budget deficit targets until 2017. According to Reuters he said:

In the event of further violation of the deficit limit by France, the credibility of the EU budget rules would be damaged if the commission were not to intensify action.

WEIDMANN SAYS FRANCE, ITALY INCREASING REASON FOR CONCERN

— MineForNothing (@minefornothing) October 13, 2014

Jens Weidmann making clear that he's not happy. With just about anything.

— Duncan Weldon (@DuncanWeldon) October 13, 2014

Updated

Here’s the Reuters take on Standard & Poor’s comments:

The economic risks in the euro zone are tipped to the downside and the ratings outlook may not reflect this, Standard and Poor’s chief sovereign ratings officer Moritz Kraemer said on Monday.

”The risks are probably to the downside in the euro zone. The ratings outlook does not reflect it in such a clear way,” said Kraemer, during a webcast to discuss the agency’s downgrade of France’s rating outlook late on Friday.

”We have three positive outlooks and three negative outlooks but if you look beneath just the mere numbers you will see that the sovereigns with a positive outlook in combination are economies which account for less that 3% of eurozone GDP, whereas those with a negative outlook account for a combined 38% of GDP.”

S&P has a positive outlook for Ireland, Cyprus and Slovakia and a negative outlook for France, Italy and Slovenia.

More rating agency downgrades may be on the way, judging by this:

S&P'S KRAEMER SAYS ECONOMIC RISKS TO DOWNSIDE IN EURO ZONE AND RATINGS OUTLOOK DOES NOT CLEARLY REFLECT THIS ratings downgrades coming

— FxMacro (@fxmacro) October 13, 2014

Incidentally, S&P’s next scheduled reports are Portugal on 7 November and Spain a week later.

Updated

The current worries about the health of the global economy are overdone, for the most part, according to Capital Economics.

The economic research group’s Julian Jessop said there were four main areas of concern, the most worrying being the signs of a renewed downturn in the eurozone, Germany in particular. He said:

There are a number of ways in which the deep-rooted problems in the euro-zone could play out. The single currency could muddle through, as it has for many years. But our feeling is that more extreme outcomes are still on the cards, including an eventual break-up. In any event, it is hard to see any solution that does not involve additional easing by the ECB and further euro weakness in the coming months.

We are less worried about the second concern, namely the collapse in the oil price. This slump is partly a reflection of weak demand from Europe and China, but it is mainly due to booming supply and has been compounded by dollar strength and panic selling. As such, the collapse in oil prices overstates the weakness of world economy. And whatever the reasons for the fall, lower energy costs should actually help to kick-start global growth. Overall, we expect the price of Brent to recover a little by year-end, perhaps to $93 per barrel from the current $88, before heading lower once more (our end-2015 and end-2016 forecasts are $85 and $80, respectively).

The third global concern is the slowdown in the major emerging economies. But this is essentially old news. The bulk of this slowdown took place between 2010 and 2012, since when growth has actually been relatively stable. Admittedly, China’s growth may have weakened a little further in the third quarter– perhaps to sub-7%. But this would still be a decent and probably healthier pace.

Overall, our view is that a lot of the bad news for commodity prices – especially metals – is now surely priced in.

The final source of concern is a host of worries under the general umbrella of “geo-political risks”, to which we must now add fears over the Ebola outbreak. We think the bulk of these worries are overdone, but again it could be Europe that provides the biggest shocks. Political developments in the UK and France are worth watching especially closely. In particular, the rise of UKIP could force an early referendum on the UK’s membership of the EU, with any talk of British exit sending shockwaves across the region.

What’s more, even if we are right that global growth fears soon start to fade – helped if necessary by additional stimulus in the euro-zone and China – the focus could simply return to the prospects of an earlier tightening of monetary policy in the US. This should see Treasury yields resume their upward trend and keep market volatility generally high.

Following the latest surveillance visit to Spain by European Commission staff, the EC and ECB concluded the situation was improving but further reforms were needed:

The recent economic and financial developments confirm the positive trends of stabilisation that have been unfolding over the last two years. However, it will be important to remain vigilant, as the large imbalances from the pre-crisis period and the related policy challenges in the labour market and beyond are still substantial. Full and effective implementation of the reform agenda and, where needed, its further strengthening, is paramount and often requires joint delivery by various tiers of government, as well as close monitoring of outcomes from the reforms.

Updated

With markets in positive territory for a change, Wall Street is joining in the mini-rally.

In early trading the Dow Jones Industrial Average is up 44 points or 0.27%, helping to support the earlier rises on European markets.

As the Eurogroup meets in Luxembourg ahead of tomorrow’s Ecofin get-together, one of the items on the agenda is the French budget.

The country was granted an extra two years until 2015 to bring its budget shortfall below the EU ceiling of 3% of GDP. But in September France said it would not meet the 2015 deadline but would aim instead for 2017. Jeroen Dijssellbloem, chair of the eurozone finance ministers, said on Friday it should not be given extra time, and ahead of the Eurogroup meeting he continues to express his doubts:

EU DIJSSELBLOEM: FIGURES IN FRANCE BUDGET NOT HOPEFUL - MNI

— Fabrizio Goria (@FGoria) October 13, 2014

https://twitter.com/FGoria/status/521642552077086720

EU DIJSSELBLOEM: THERE ARE CONCERNS SURROUNDING FRENCH BUDGET, SHOULD BE NO DEALS OUTSIDE OF GROWTH PACT - MNI

— Fabrizio Goria (@FGoria) October 13, 2014

Meanwhile Italy seems more optimistic about its own prospects:

Italy fin min Padoan: Confident Italy is making its way back to sustained growth

— Live Squawk (@livesquawk) October 13, 2014

Updated

Lunchtime summary

Here’s a summary of what’s happened so far:

- UK income tax revenues are likely to come in lower than expected, public finances watchdog the Office for Budget Responsibility has warned

- Stock markets continue to be volatile but have edged higher after earlier falls

- France’s Jean Tirole has won the Nobel prize for economics (technically The 2014 Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel). Follow our separate live blog

- Bank of England governor Mark Carney says eurozone weakness will not dictate UK monetary policy

- Most European banks are likely to pass the ECB’s assessments, says Fitch

And here’s the latest market update:

In a note entitled Deutschlanding, Credit Suisse analysts say the recent poor data from Germany shows how imbalanced its economy is, with its bias towards exports:

Recent euro area data suggest that a slowdown in cyclical momentum has lurched into sharp recession: in August German industrial output fell as precipitously as it did during the Great Recession.

That collapse in production is more statistical artefact than reality, in our view. The euro area and German economies have slowed, but are not in recession. Industrial production data should reverse their falls in the autumn.

But, still, something has happened, even if recent data are an exaggeration. Reliable indicators do point to a slowdown in German manufacturing, in part driven by its hitherto successful capital goods sector. We’d attribute that to slower demand growth in Asia and a knock to exporters’ confidence from the imposition of sanctions on Russia.

We think this marks an important shift. Germany is perhaps the world’s most imbalanced economy: biased towards exports and with a current account surplus worth 7% of GDP. Those imbalances have until now driven significant economic (out)performance. But external demand has turned less supportive. That points to a gradual erosion of Germany’s trade and current account surplus and, in turn, a headwind against German GDP growth from net trade.

The key question is what that means for growth, in both Germany and the euro area. In the short term, slower German growth is likely to keep euro area GDP growth anaemic, given how insipid the recovery is in the rest of the euro area. So far, negative feedback from weaker external to domestic demand in Germany and the rest of the euro area looks limited. Although some further deterioration is likely, it may be offset other factors pushing for an improvement in euro area domestic demand dynamics.

Still, insipid GDP growth and diminishing external demand require stronger domestic stimulus. The political will for, let alone implementation of, looser fiscal policy is still absent. That leaves monetary policy: we continue to expect the ECB to broaden its asset purchases to sovereign debt, possibly early next year.

Another mechanism to offset this would be a weaker currency. The recent drop in the euro can help, but a larger decline would be necessary to deliver a meaningful change to the euro area’s growth dynamics. As it happens, such a fall would likely benefit the export sector in other euro area economies rather than Germany.

Meanwhile:

GERMAN GOVT SPOKESMAN SAYS GERMAN GOVERNMENT SAYS NO PLANS TO ABANDON BALANCED BUDGET GOAL, SAYS THIS TARGET HAS "HIGH VALUE"

— MineForNothing (@minefornothing) October 13, 2014

Updated

Most European banks likely to pass ECB assessments - Fitch

The majority of European banks are likely to pass the ECB’s stress tests, according to ratings agency Fitch. It said:

We expect the majority of banks to pass the assessment, and many of those that fail could be technical failures, in the sense that capital shortfalls have either already been addressed in 2014 or capital is easily sourced from within a banking group. Only a small minority of institutions are likely to have a headline capital shortfall that means they will need to establish plans to raise capital or reduce assets by the middle of 2015.

But the assessments, due to be published on 26 October, are not the end of it, and Fitch estimated it would cost another €235bn to raise reserves enough to cover impaired loans for all banks to around 80%. It said:

The ECB’s comprehensive assessment is only a first step in levelling the playing field for banks’ access to private sector funds and ability to extend lending. High levels of unreserved problem loans will leave some banks, particularly in weaker countries, still vulnerable, Fitch Ratings says.

There is a strong correlation between banks with the weakest balance sheets and weak eurozone sovereigns. Greece, Ireland, Italy and Spain made up more than two thirds of unreserved impaired loans at end of the first half of 2014. The banks with the highest unreserved impaired loans relative to capital tend to be from peripheral eurozone countries.

Capitalisation has strengthened notably for most of the 130 banks undergoing the assessment since the last EU-wide stress test in 2011. This has continued into 2014, with reported equity for the banks in the exercise rising by around €65bn in the first half of 2014, including common equity raising of around €31bn. The banks also issued €15bn of additional Tier 1 securities, with further progress in the third quarter of 2014.

We expect further capital increases and restructuring to follow the comprehensive assessment at the banks identified as the weakest. Despite this, balance sheet strength will remain dependent on collateral valuation. Further progress will be needed in the first few years of the single supervisory mechanism to strengthen the balance sheet of weaker banks.

We estimate it would cost around €70bn to raise reserve coverage of impaired loans for all banks undergoing the assessment to 60%. Upping coverage to a very solid (and arguably conservative) level of 80% would cost around €235bn. We certainly do not expect this much capital to be injected into the system during the next few years. The numbers do, however, give a strong indication of the importance of remaining vigilant about collateral valuation when assessing banks.

Here’s the Reuters take on Carney’s latest comments:

Euro zone weakness will be only one factor that helps to determine when the British central bank raises interest rates, Bank of England Governor Mark Carney said in interviews broadcast on Monday.

Carney told U.S. news channel CNN that weakness in the euro zone and elsewhere had been a major theme at the International Monetary Fund’s meetings in Washington, but that Britain’s recovery had been driven primarily by domestic factors.

“The only difficulty that is caused by Europe is that it provides an additional drag on growth. But that doesn’t dictate the monetary policy of the Bank of England,” he said.

Carney added that the BoE had already forecast that Britain’s rapid recovery would slow slightly towards the end of 2014, and would continue to keep a close eye on domestic inflation pressures that might come from the labour market.

Carney said in a separate interview with CNBC television that weaker global demand was producing a “very benign global inflationary environment and that is something that we do certainly take into account.”

Carney says eurozone weakness will not dictate UK rate policy

Bank of England governor Mark Carney has been on CNN, suggesting the recent weakness in the eurozone might have an effect on the timing of UK interest rates, but it will not dictate policy. Here are the snaps of his comments, courtesy Reuters:

13-Oct-2014 11:04 - BANK OF ENGLAND’S CARNEY SAYS WILL TAKE EURO ZONE WEAKNESS INTO ACCOUNT IN THINKING ON INTEREST RATES - CNN

13-Oct-2014 11:05 - BANK OF ENGLAND’S CARNEY SAYS DOMESTIC FACTORS HAVE BEEN DRIVING UK RECOVERY

13-Oct-2014 11:06 - BANK OF ENGLAND’S CARNEY SAYS NEED TO ASSESS WHETHER UK ECONOMY WILL SLOW SLIGHTLY AT END OF 2014 - CNN

13-Oct-2014 11:07 - BANK OF ENGLAND’S CARNEY SAYS EURO ZONE WEAKNESS DOES NOT DICTATE MONETARY POLICY OF BOE

13-Oct-2014 11:08 - BANK OF ENGLAND’S CARNEY SAYS BOE WILL IGNORE DATE OF UK ELECTION WHEN SETTING POLICY - CNN

The Bank is widely expected to be the first of the major central banks to begin to raise interest rates after months of record lows, but these comments sound a little more dovish than of late.

Carney (CNBC) - Reiterates BoE independent. Ignore UK election when setting policy. Sees modest sign of deceleration in UK economy

— Steve Collins (@TradeDesk_Steve) October 13, 2014

Updated

Mkt rout wiped out $1.5tn dollar from global stocks last week. Global equities have lost $4.5tn in value since record pic.twitter.com/QwXwPbmbm5

— Holger Zschaepitz (@Schuldensuehner) October 13, 2014

Back in the corporate world, and Smith & Nephew has disappointed investors with news that a novel spray on skin treatment to help heal leg ulcers has failed in a late stage clinical trial.

The product - designated HP802-247 - consists of living cells which are designed to work with the body’s own cells, but despite the failure of the trial in North America, a phase 3 study in Europe is due to report in 2016. But the outcome of this latest test is a particular disappointment given earlier successful trials. Analyst Nicholas Keher at Investec said:

Phase 2b results were published in June 2011 and showed positive results, meeting both primary and secondary end points with a significant improvement over the gold standard treatment.

The company therefore needs to determine why those results could not be repeated in the larger phase 3 trial in North America and whether they should attempt the trial again. A second phase 3 trial is currently underway in the EU, which is expected to report in May 2016 and Smith & Nephew will continue to review the HP802 program whilst this trial continues.

We had assumed HP802 would launch in 2017 with 6% peak penetration in 2021, leading to peak revenues of $230m, thus there are no changes within our forecast period. However our price target reduces to 1023p from 1100p as we increase the risk adjustment on HP802 to only a 25% chance of success (the product could still launch in the US if the US trial is repeated, but also in the EU if the Phase 3 trial there is successful) and we reduce our recommendation to hold from add.

The Nobel Prize for Economics - technically The 2014 Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel - is expected to be announced around noon (BST).

My colleague Graeme Wearden is now covering the event, and his live blog is now up and running.

Updated

With no major economic data due today, and US bond markets closed for Columbus Day, it is likely to be another uncertain day on the markets.

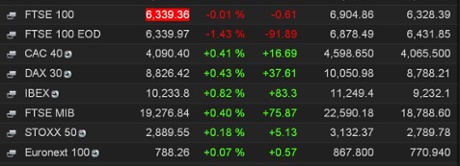

Indeed, European markets have now edged into positive territory after their early falls, with airlines lifted by the falling oil price. Mining shares are also giving some support after the better than expected data from China, a key consumer of commodities.

Updated

Falling markets do not appear to be stopping the flow of major deals, especially if they involve tax benefits.

US healthcare group Steris has agreed to buy the UK’s Synergy Health, a specialist in sterilisation services, for £19.50 a share or around $1.9bn. In the market Synergy’s shares have jumped 32% to £18.50.

The merged company will be incorporated in the UK, presumably so it can benefit from lower corporate taxes. The US is trying to clamp down on such moves, which have been cited as important reasons for a number of proposed deals, notable Pfizer’s attempt to buy AstraZeneca.

Over in Russia, and the ruble continued to weaken against the dollar and euro, despite central bank intervention.

The currency touched a new all-time low against the euro, as it continues to be pressurised by falling oil prices, the strength of the dollar and the impact of sanction on Russia due to the Ukraine situation.

Russia’s central bank governor Elvira Nabiullina said it had spent $6bn defending the ruble in the past 10 days but maintained the situation on the currency market was under control. Alastair Winter at Daniel Stewart said:

Russia’s central bank is rapidly using up its reserves in its fight to slow the rouble’s plunge. Mr Putin may have won the first easy battles but by putting politics before economics he is risking a deep recession. The slide in the price of oil is inflicting the worst damage.The news that he is removing troops from the Ukraine border may be posturing but could also be a sign that in the rumoured splits at Mr Putin’s ‘imperial court’ the realists are starting to prevail.

European stock markets are clawing back some of their early losses, but they’re all still in the red (the DAX is down 0.3% and the CAC is down 0.4%).

Alastair McCaig, market analyst at IG, says it could be a long week:

Just over a month ago expectations that the FTSE could break above the 7,000 level were the norm, with the index trading less than 100 points away. The subsequent economic data out of Germany and dismantling of confidence has not only slaughtered European markets but dragged the UK down too.

Only an hour or so into Monday’s trading and this already feels like it will be a long week: ratings agencies are downgrading their outlook on France, Tuesday’s German ZEW data is thought unlikely to inspire, the European Council is likely to reject the latest French budget, and Thursday’s eurozone inflation figures are a real cause for concern.

Here’s the biggest risers and fallers on the FTSE 100 this morning:

$FTSE - 0.3% Main movers: pic.twitter.com/cwNbLlV86s

— Brenda Kelly (@BrendaKelly_IG) October 13, 2014

Updated

Today’s stock market falls come as investors await a showdown between the European Central Bank, markets and politicians within Europe.

Jeremy Cook of World First sums up the rival camps:

The first, led by ECB President Mario Draghi, is those who are looking for a more accommodative monetary policy from the European Central Bank to further support business and lending within the Eurozone.

The second are those members of the European Central Bank who are against these unconventional measures, led by Bundesbank President Jens Weidmann.

Thirdly are the Eurozone politicians who may be eventually called upon to change the rules of the Eurozone in order to allow the European Central Bank more room to manoeuvre.

Updated

OBR warns that UK income tax revenue may disappoint

Another reason for gloom this morning; Britain’s public finances watchdog has warned that income tax revenues are likely to come in lower than expected.

And that’s because many of the jobs created since the recession ended are relatively poorly paid.

Press Association has the details:

Robert Chote, the head of the Office for Budget Responsibility, said the expected shortfall was due to the numbers going into relatively low paid work.

“From the perspective of the public finances, that’s not particularly good news,” he told the BBC Radio 4 Today programme.

“The Chancellor of the Exchequer gets more bang for his buck if wages and salaries rise as a result of people’s earnings going up than if employment goes up.

“If earnings go up you are taking more people into higher income tax brackets whereas if employment is going up you are perhaps bringing in more people at the bottom.

“This continued story of earnings growing less rapidly than expected and employment growing more rapidly than expected does perhaps suggest that we’re more likely to be disappointed than to over-achieve on income tax receipts this year.”

While shares fall, the gold price is rising - up $8 per ounce to $1,230 this morning.

Gold is benefitting from the market nervousness. It is also higher because the US dollar (in which it is priced) has fallen back after a recent rally.

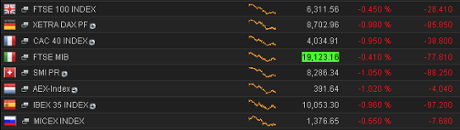

It’s another ‘sea of red’ across Europe’s stock markets this morning, as the German DAX hit a new one-year low:

FTSE 100 hits 15-month low as European markets drop again

The FTSE 100 has hit its lowest level since July 2013, at the start of trading in London.

The blue-chip index of top shares fell by as much as 43 points to 6294, a 15-month low.

The biggest faller is chipmaker ARM; the semiconductor industry is under pressure after a profit warning from US firm Microchip.

Other European stock markets also opened in the red, with the German DAX and French CAC both down 1%.

Fears that Germany may fall into recession, and the news that rating agency S&P cut France’s credit rating outlook on Friday night, are weighing on the markets.

The mood on the trading floors is rather bearish, as IG analyst Chris Weston puts it:

The [market] open is at least looking like a lonely and dark place for the bulls.

Today's European markets look set to be like the weather in London today - stormy and squally.

— Michael Hewson (@mhewson_CMC) October 13, 2014

It’s not a rout, though -- mining shares have picked up in early trading in London, saving the FTSE 100 from falling further.

Mining stocks have saved an opening sell-off- sector +2% - FTSE 100 -40 points at 8.04am - ASTRA -1.5%, Tesco -0.9% - OIL stocks - av 0.5%

— David Buik (@truemagic68) October 13, 2014

Updated

Middle East stock markets have already started the week badly, having opened on Sunday.

The Dubai market tumbled 6.5%, as falling oil prices and growth fears sparked a wave of selling among traders, who were also reacting to Friday’s big losses in Europe and the US.

Asian markets fell today despite better than expected Chinese trade data over the weekend.

Associated Press has more details:

Asian stock markets were lower Monday, shrugging off robust Chinese trade figures as investors exited riskier assets after concerns resurfaced about the global economic outlook.

Hong Kong’s Hang Seng fell 0.6 percent to 22,962.35 and China’s Shanghai Composite slid 1 percent to 2,351.39. South Korea’s Kospi dropped 0.8 percent to 1,926.18. Australia’s S&P/ASX 200 declined 0.6 percent to 5,159.00. Markets in Southeast Asia and New Zealand also dropped. Stock markets in Japan were closed for a holiday.

Last week, the International Monetary Fund trimmed its global growth forecasts for this year and next, citing weakness in Japan, Latin America and Europe. The global economy will expand 3.3 percent this year instead of 3.4 percent and expand 3.8 percent in 2015. The IMF said recovery is “weak and uneven” in the advanced economies.

Terry Torrison, managing director at Monaco-based McLaren Securities, tells Reuters that traders are rather nervous after last week’s selloff:

“We’re still looking quite poorly, on the markets. The nervousness is still there. I don’t think anyone will want to come running back into the market early doors,”

Updated

Opening post: Markets start the week with fresh falls

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, the eurozone and business.

Stock markets are beginning the new week where they ended the old one -- falling, in the face of economic worries.

The Asian markets have lost ground already today, sending leading shares across the region down to seven-month lows.

Asia at afternoon... Sensex down 0.5% ASX ends down 0.6% HK, Kospi down 0.7% each Shanghai down 0.9% Taiex down 2.6% (!) $HSI $XJO

— Michael Kitchen (@KitchenNews) October 13, 2014

Japan is closed for a public holiday.

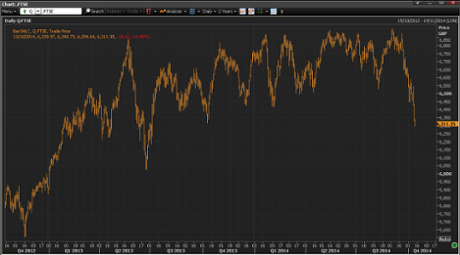

And European markets are expected to follow suit when trading begins at 8am BST. Both the FTSE 100 and German DAX hit their lowest levels of the year last week, and are expected to continue that trend.

William Nicholls of Capital Spreads in London writes:

“European equities look set to open sharply lower yet again following a terrible ending to U.S. equity trading on Friday and another lurch lower in Asia overnight,”

“As the global recovery seems to become increasingly less certain...the risk off trade has become worryingly prevalent.”

Last week ended badly for Europe, with the FTSE 100 and German DAX both hitting their lowest level in a year, after a flurry of bad economic data from Germany

Then, after the markets closed, there was a double-whammy of bad news from rating agency S&P. It cut its outlook on France, and stripped Finland of its AAA rating altogether.

Finns Told Golden Era Over After S&P Downgrade Shock

The market correction comes as several of the world’s top central bankers and finance ministers gather in New York to ‘war game’ the collapse of a major transatlantic bank.

Fed chair Janet Yellen, Bank of England governor Mark Carney, Treasury secretary Jack Lew and chancellor George Osborne will play out a financial crisis, to see if they cope better than in 2008.

Six years after Lehman’s crash, US and UK play out next financial crisis.

And the other big news of the day is the award of the Sveriges Riksbank Prize in Economic Sciences in Memory of Alfred Nobel, around lunchtime....

Updated