US stock markets close 2% down

US stock markets closed down almost 2% on Friday following sharp falls across the world due to investor’s renewed concern about the health of the global economy after the US Federal Reserve’s decided to leave American interest rates on hold.

The Dow Jones Industrial Average closed down 291.7 points ( or 1.75%) to 16,383 points. The S&P 500 lost 32.09 points (or 1.6%) to 1,958.11 and the Nasdaq fell 66.72 points (1.36%) to 4,827.23 points.

The Fed is fanning fears over global growth, causing a big selloff: http://t.co/N57fUQRJf4 pic.twitter.com/7cjswWI260

— MarketWatch (@MarketWatch) September 18, 2015

You can also read our updated news story here:

Updated

Over in Athens tonight, Syriza has held a pre-election rally where Padomes leader Pablo Iglesias has just addressed the crowd with the opening line: “I will speak in Spanish because in Berlin they have to learn what Spanish and Greek sounds like!”

He then went on to liken Tsipras to “a lion ... Noone has ever tried to defend your rights like Alexis.”

European shares close sharply lower after Fed comments

The US Federal Reserve may have left interest rates unchanged but the central bank’s cautious comments about the outlook for the global economy sent shudders through global markets.

Chris Beauchamp, senior market analyst at IG said: “Markets can be a fickle thing. Going into last night’s Fed meeting, talk revolved around how damaging a rate hike would be to equity markets. It turns out that no hike can also be rather problematic, especially when accompanied by a sober statement and downgrades to economic forecasts. As a result, stocks moved swiftly into the red this morning and have stayed there all day.”

European markets were harder hit than the UK, with the weaker dollar pushing the euro higher and causing concern for European exporters. So the closing scores showed:

- The FTSE 100 finished 82.88 points or 1.34% lower at 6104.11

- Germany’s Dax dropped 3.06% to 9916.16

- France’s Cac closed 2.56% lower at 4535.85

- Italy’s FTSE MIB fell 2.65% to 21,514.90

- Spain’s Ibex ended 2.57% lower at 9847.2

- In Greece, ahead of the weekend’s election, the Athens market added 0.76% to 697.57

On Wall Street the Dow Jones Industrial Average is currently down 235 points or 1.42%.

On that note we’ll close for the moment, but should be back to catch the Wall Street close. Meanwhile, thanks for all your comments.

Christopher Vecchio, Currency Analyst at DailyFX, confirms that a US rate hike this side of Christmas is now less likely than before:

The implied probability of a rate hike in October, per the Fed funds futures contract, dropped from near 45% yesterday to 18% today; for December, from above 60% yesterday to 26% today.

Updated

Some analysts are arguing today that the Fed has created a new ‘third mandate’, on top of its existing dual duties to deliver price stability and maximum employment.

Jeremy Zirin, chief equity strategist at UBS Wealth Management, says (via Reuters)

“Investors are wrestling with how concerned they should be regarding global growth.”

“The Fed has introduced a quasi third mandate about the global growth, apart from the labor market and inflation.”

That means added uncertainty, which usually equals falling stock markets....

Updated

Every major stock market is in the red, with the exception of the Australian and Hong Kong indices which closed many hours ago before the rout got underway.

Updated

Perhaps we can file today in the ‘inexplicable market reaction’ box.

Stocks are acting like they expected more QE yesterday,

— Lorcan Roche Kelly (@LorcanRK) September 18, 2015

Updated

Bill Gross backs the Fed

Bond trading veteran Bill Gross says the Fed made the right call last night, given financial market conditions.

Speaking on Bloomberg TV right now, Gross suggests that the current era of non-standard monetary policy could last for another five or ten years.

That would allow the problems created during the ‘fat’ decades of debt-driven growth pre-Lehman Brothers to be worked off, he argues.

Bill Gross says we need low interest rates in order to recapitalize. Watch live http://t.co/H89WEacu1C pic.twitter.com/um4ZAczB26

— Bloomberg TV (@BloombergTV) September 18, 2015

Gross concedes through that asset prices are simply too high, partly because they’re being priced against record low US interest rates and German bond yields.

Ultimately, there has to be a rebalance if capitalism itself is to rebalance, Gross added.

Wall Street opens sharply lower

US markets have followed the rest of the world lower after the Federal Reserve’s concerns about economic growth.

The Dow Jones Industrial Average has lost more than 200 points or 1.2% in early trading, while the FTSE 100 is now 1.6% lower and Germany’s Dax has dropped 3.49%, with investors worried about euro strength against a weaker dollar hitting European exporters.

Dow opens down more than 200 points http://t.co/Mnt63OLRu6 pic.twitter.com/Ds2IKg7tMG

— Business Insider (@businessinsider) September 18, 2015

Updated

The Wall Street opening bell has been rung, and the New York stock market is open for business.

The scale of today’s selloff is a little surprising, given that the markets didn’t really expect the Federal Reserve to raise interest rates rates yesterday.

But they also didn’t expect the Fed to be quite so gloomy about the global economy. That dovishness is making investors around the globe reassess the prospects of a rate hike.

Guy Dunham of Baring Asset Management in London explains:

Federal Reserve slightly surprised market participants by combining a decision to leave interest rates where they are with dovish language, and revised down their median short and long-term expectations by 0.25%.

Investors who hold risky assets are particularly uneasy, he adds, given the confusion over the timing of any rate hike.

Here’s a reminder of how rate expectations have been pushed back:

Implied probabilities of a Fed rate hike following yesterday’s meeting pic.twitter.com/dNsqvdk1dN

— Bond Vigilantes (@bondvigilantes) September 18, 2015

The Fed decision sparked a small rally in some emerging markets, but nothing sensational.

India’s Sensex index jumped 2% earlier today, on relief that US rates hadn’t been hiked. The optimism has faded, though, with the index up just 1% in late trading.

Viktor Shvets, head of Asian strategy at Macquarie Securities, predicts that the optimism won’t last. He told CNBC:

“I think in the short-term, emerging markets will be supported because the Federal Reserve didn’t tighten. Basically, there’s little bit less pressure for U.S. dollar to appreciate, a little bit more liquidity.

“There’ll be some relief particularly, in places like Indonesia, Malaysia, up to places like Brazil, South Africa, Russia. Will it last? The answer is no.”

Warning: This market bounce will be short-lived » http://t.co/1Y5CeNECdD pic.twitter.com/qexyUc7dzw

— CNBC (@CNBC) September 18, 2015

Updated

Traders heading to Wall Street this morning should take their best tin hat.

Futures: Dow -200; S&P -24; Nasdaq - 51

— Brenda Kelly (@Brenda_Kelly) September 18, 2015

Updated

Now this is curious. Someone in the City has sold shares in two blue chip heavyweights, BP and HSBC, way below the market value.

Shares in both companies briefly dropped by almost 5%, before swiftly rebounding.

C'mon, who did it?! #HSBC pic.twitter.com/Y2yeQTv3cU

— Jonathan Ferro (@FerroTV) September 18, 2015

Someone had a pop at BP stock as well pic.twitter.com/zXXflkce2L

— Jonathan Ferro (@FerroTV) September 18, 2015

It’s probably a ‘fat-fingered trade’, where someone presses the wrong button. But two at the same time suggests something went badly awry.

@FerroTV It's no fat finger. Someone SAT on a keyboard.

— Brenda Kelly (@Brenda_Kelly) September 18, 2015

Andy Haldane’s fascinating speech (online here) also outlines how Britain could introduce a tax on money.

That would encourage people to spend, pushing up inflation, and avoiding the problem that it’s hard to cut UK interest rates much lower.

Another option is to embrace an electronic currency like Bitcoin, which Haldane says has “real potential”.

If paper currency were then abolished altogether, it would be possible to impose negative interest rates on deposits.

As Haldane puts it:

What I think is now reasonably clear is that the distributed payment technology embodied in Bitcoin has real potential. On the face of it, it solves a deep problem in monetary economics: how to establish trust – the essence of money – in a distributed network. Bitcoin’s “blockchain” technology appears to offer an imaginative solution to that distributed trust problem.

Whether a variant of this technology could support central bank-issued digital currency is very much an open question. So too is whether the public would accept it as a substitute for paper currency. Central bank-issued digital currency raises big logistical and behavioural questions too. How practically would it work? What security and privacy risks would it raise? And how would public and privately-issued monies interact?

The Bank of England’s chief economist is trending on Twitter after warning that the UK recovery is weakening, and may need a rate cut not a hike.

The editor of the FT is leading the charge:

Must read: Andy Haldane on the future of money #BigBrain http://t.co/l69PKc7lVl

— Lionel Barber (@lionelbarber) September 18, 2015

#Interestrates could actually be cut next, not raised, says @bankofengland economist Andy Haldane. Some fear #ChinaMeltdown & 0% #inflation

— Rob Young (@robyounguk) September 18, 2015

Migration season for central bank doves? PostFed, BoE's Haldane says may need to cut rates, not raise them http://t.co/n0sBOM1gH6 @ReutersUK

— David Milliken (@david_milliken) September 18, 2015

Updated

European markets hit new lows

The European selloff is gathering pace, led by Germany’s DAX index.

The strengthening euro, and new confusion over when the Fed might hike rates, are proving to be a nasty cocktail for traders across Europe.

Conner Campbell of SpreadEx explains:

The longer investors had to ruminate on Thursday’s Fed statement the worse they seemed to take it, with the European indices widening their losses as the day went on.

An export-hurting rise in the euro-dollar was the main culprit, with the currency pairing jumping by around 0.4% as the morning continued.

And with US stocks heading for a bath too, all the main European indices have shed at least 1%. The DAX is down 2.9%, back below the 10,000 point mark at 9,933.

And here’s a reminder of how the euro jumped last night, when the Fed decision came.

Updated

The futures market is now suggesting chunky falls on Wall Street when trading begins, in two hours time.

Out of hours Dow now pointing to a -170 start, back into Tuesday's range.

— David Jones (@JonesTheMarkets) September 18, 2015

Updated

Andy Haldane: UK isn't ready for higher interest rates

The Bank of England’s chief economist is reiterating his opposition to an interest rate hike in the near future and says policy could just as easily be loosened as tightened if the UK is hurt by turmoil in emerging markets.

Andy Haldane is using a speech to business owners in Northern Ireland to discuss events in the Greek economy and in China, where an economic slowdown has coincided with a stock market rout and sent jitters through global markets.

Haldane, one of nine policymakers that vote on interest rates at the Bank, reiterated warnings he made earlier this year that the UK economy was not ready for higher borrowing costs.

Haldane’s comments put him at odds with other members of the monetary policy committee, who have been talking up the strength of the UK economy and its ability to withstand contagion from slowing emerging markets.

“In my view, the balance of risks to UK growth, and to UK inflation at the two-year horizon, is skewed squarely and significantly to the downside,” Haldane said in the speech to the Portadown Chamber of Commerce.

“Against that backdrop, the case for raising UK interest rates in the current environment is, for me, some way from being made.”

Haldane said it was unclear how much the UK would be affected by the slowdown in emerging nations, significant drivers of global growth in recent years. But he said there were significant risks of contagion given the growing clout of developing economies in recent years.

Added to that, Haldane highlighted challenges in the UK.

“While the UK’s recovery remains on track, there are straws in the wind to suggest slowing growth into the second half of the year. Employment is softening, with a fall in employment in the second quarter and surveys suggesting slowing growth rates. Surveys of output growth, in manufacturing, construction and possibly services, have also recently weakened. All of these data were taken prior to recent emerging market economy wobbles,” he said.

Given those risks, there was no case right now for hiking, he said, concluding:

“One reason not to do so is that, were the downside risks I have discussed to materialise, there could be a need to loosen rather than tighten the monetary reins as a next step to support UK growth and return inflation to target.”

How low can you go? - speech by Andrew Haldane http://t.co/w3rPTP8fJq

— Bank of England (@bankofengland) September 18, 2015

Anne Richards: Fed was right to hold fire

Janet Yellen doesn’t want to go down in history as the Fed chair who plunged the global economy into recession, and the US with it.

So explains Anne Richards, chief investment officer at Aberdeen Asset Management. She believes the Federal Reserve’s rate-setting committee was right to leave interest rates unchanged

Richards told Bloomberg TV that raw economic data simply doesn’t provide a compelling reason to hike rates. If the Fed moves too quickly, it “could make 2016 much uglier from an economic perspective”.

Richards added that the Fed has now looked “beyond its borders” to survey the global economy, and concluded that the outlook for next year isn’t as rosy as they thought.

Wall Street is expected to follow Europe’s lead lower, when the New York stock exchange opens in just over three hours.

US indices slipping lower in the overnight markets. Dow currently 80 points lower than yesterday's close.

— David Jones (@JonesTheMarkets) September 18, 2015

Updated

Fed hike in 2015 now less likely

After Janet Yellen’s dovish performance last night, investors have all-but discounted the chances that interest rates will be hiked at October’s meeting.

And there’s much less confidence that the Fed will raise rates before the end of the year. There’s now more chance that the first hike comes in 2016.

The Bond Vigilantes team at M&G have kindly tweeted the key charts:

The markets now think an Oct rate hike is off the cards, despite Yellen saying the meeting is “live” pic.twitter.com/al1QmDgSvF

— Bond Vigilantes (@bondvigilantes) September 18, 2015

Implied probabilities of a Fed rate hike following yesterday’s meeting pic.twitter.com/dNsqvdk1dN

— Bond Vigilantes (@bondvigilantes) September 18, 2015

Fed gives German stocks the shivers

Yikes. The German DAX is now down almost 2%.

The selloff is driven by fears that Germany’s exporters will be thumped by the renewed strength of the euro against the US dollar.

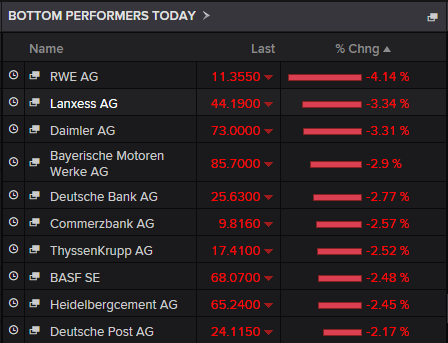

Top fallers include carmakers BMW and Daimler, chemical giant BASF, and industrial conglomerate ThyssenKrupp.

Traders need to fasten their seat belts for a period of high volatility, warns Ipek Ozkardeskaya of London Capital Group.

She explains that economic data will be scrutinised more tightly than ever, thanks to the Fed’s new concern about the global economy.

The inflation in China and the unemployment in the Eurozone will be as important as onion prices in India and dairy product sales volume in New Zealand. Given the dull economic fundamentals across the globe, it may be hard for the Fed to take the first step before the end of the year.

It will be even harder for the market to assess a consensus and to come up with expectations.

#Fed inaction adds nothing but turbulence to the market: $TRY $BIST #EM http://t.co/rQnoPTxO8f

— Ipek Ozkardeskaya (@IpekOzkardeskay) September 18, 2015

Gold miners are benefitting from the Fed’s reluctance to raise interest rates, reports my colleague Nick Fletcher:

Janet Yellen’s concerns about the Chinese economy has undermined leading shares, despite the Federal Reserve chair announcing on Thursday that US interest rates would remain on hold.

The worries about the outlook for the global economy have pushed mining shares lower, although precious metal miners are shining on hopes that the Fed decision will weaken the dollar - which is already happening - and lift gold prices.

So Randgold Resources has risen 118p to £38.47 and Fresnillo is 17p better at 607p.

HSBC’s chief economist reminds us that we’ve been expecting a US rate rise “soon” for a long time.

Remember the beginning of the year when everyone said US rates would definitely rise in June? And then September? Still waiting....

— Stephen King (@KingEconomist) September 18, 2015

The German stock market is continuing to weaken, now down around 1.3% today.

DAX looking ugly. A break below 10068 could have major bearish implications pic.twitter.com/ZQog7mg0Wy

— Joshua Mahony (@JMahony_IG) September 18, 2015

Updated

Britain’s interest rates could now remain lower for longer, thanks to the Fed, argues RBS’s economics team.

They point out that the two policy rates usually rack each other quite closely, due to a) the amount of trade between the two countries, and b) the US’s pre-eminent position.

The Bank of England is also likely to favour waiting for the Fed to hike first.

Why yesterday's #Fed decision not to raise rates matters for the UK. Read: http://t.co/E3IIQqLkPr pic.twitter.com/qN0fs5gkbz

— RBS Economics (@RBS_Economics) September 18, 2015

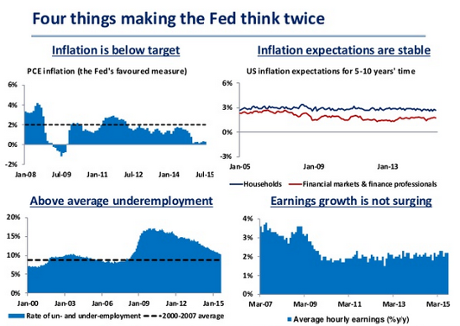

RBS also pulled together four charts to explain why the Fed didn’t hike (from this Powerpoint presentation):

When China sneezes, the US catches a cold and Europe gets the flu. #Fed #PBoC

— Joshua Raymond (@Josh_RaymondUK) September 18, 2015

The Federal Reserve has knocked confidence in the global economy by leaving interest rates unchanged and sounding so cautious, argues Jameel Ahmad, FXTM chief market analyst.

The indication from the Federal Reserve that global economic weakness played a major factor in delaying a US interest rate rise strongly weakens the possibility of an interest rate rise at all this year.

Global growth concerns are a reoccurring theme as current suggestions strongly point towards economic momentum in China continuing to slow even further next year. Both the Bank of Japan (BoJ) and European Central Bank (ECB) are going to find themselves under increasing pressure to reinvigorate economic momentum, and the emerging markets remain vulnerable to further weakness.

Marc Ostwald of ADM Investor Services is fuming about the Federal Reserve’s decision to leave rates unchanged, and sound rather dovish about inflation and China.

He points out that the Fed raised its growth forecasts, and lowered its unemployment projection, clearing the way for a rate hike. Instead, weaker global conditions were cited as a reason to ignore these forecasts.

Ostwald says:

If the FOMC’s objective was to convey confusion, it has succeeded, thereby ploughing a deep furrow of instability and destabilization, and shining a very bright light on the large debt and liquidity trap it and other G7 central banks have spent 7 years crafting.

Fed no longer a cen bank, just source of confusion, ploughing deep furrow of instability & destabilization, and nightmare of liquidity trap

— Marc Ostwald (@MOstwald1) September 18, 2015

Eurozone stock markets are suffering because the euro has rallied against the dollar overnight.

That’s bad for exporters in France and Germany.

It may also have spoiled Mario Draghi’s breakfast. The ECB president managed to weaken the euro earlier this month by hinting at further stimulus measures. Maybe he’ll have to deliver soon.

Question now, how long can the ECB afford to wait?

— Frederik Ducrozet (@fwred) September 18, 2015

The dollar has just hit a three-week low against major currencies, down 0.2%.

That reflects the chance that US interest rates may not rise until next year.

European markets hit by Fed fears

Germany and France’s main stock indices have both fallen over 1% in early trading, echoing the selloff in London.

Investors in Frankfurt and Paris aren’t impressed by Janet Yellen’s dovish performance last night, where the Fed chief warned that the slowing Chinese economy could “restrain US economic activity somewhat”.

That’s encouraging investors to sell shares, and pile into safe assets including German bunds (see 7.55am)

Here’s the damage across Europe’s stock markets this morning:

Updated

You might think that ultra-low interest rates would boost stock markets in Europe.

But traders are worried that Janet Yellen sounded quite concerned about low inflation and the global economy at last night’s press conference.

Mike van Dulken of Accendo Markets explains:

Markets had anticipated either a dovish hike (easy does it) or a hawkish hold (be prepared) [but got neither].

While markets had desired clarity, it appears that uncertainty (and volatility) may be here to stay (December hike, Jan, later?).

Updated

And we’re off! Europe’s stock markets are open, allowing traders to give their verdict on last night’s Federal Reserve decision.

As predicted, shares are dropping in London, with the FTSE 100 losing 33 points or 0.5% to 6153.

Other European indices are also dipping, as the relief rally that began in Asia peters out....

Updated

Wendell Perkins, senior portfolio manager for Manulife Asset Management, reckons US interest rates will probably remain at their record lows until next year.

Perkins also predicts more volatility as the markets react to last night’s Fed decision.

Investors need to consider a) When are they going to raise, b) what are they afraid of, and c) how worried are they about conditions in the global economy, he told Bloomberg TV.

Money is pouring into German government bonds this morning.

This is pushing down the yield (or interest rate) on debt issued by Europe’s largest member. That’s often a sign of anxiety in the markets.

Big moves in European #bond yields following US...German debt rallying, yield dropping 9bps on 10yer pic.twitter.com/St3WcgBPjJ

— Caroline Hyde (@CarolineHydeTV) September 18, 2015

Good morning all. There’s a subdued feel in the City today, after the Fed disappointed those hoping that the Federal Reserve would raise interest rates last night.

The decision wasn’t a shock (as we blogged yesterday, the markets suggested only a 32% chance of a hike).

But some investors are now fretting about why Janet Yellen and the rest of the FOMC held borrowing costs at record lows again.

It’s slightly ironic. Traders don’t want the flow of cheap money to end, but they’re also worried that central bankers feel the need to keep replenishing the punchbowl.

As London CapitalGroup dealer Jonathan Sudaria puts it:

“Yes, we’ve got a reprieve on an immediate interest rate hike, but thereason for the stay of execution is rather bearish itself.”

And that’s why the main European stock markets are expected to dip in early trading.

Seems Europe gonna follow US equities lower...US on hold highlight risks to global economy&just postpones inevitable? pic.twitter.com/2grwHY02m2

— Caroline Hyde (@CarolineHydeTV) September 18, 2015

Updated

I’m handing over now to my colleague Graeme Wearden who is poised at his work station in London. Thanks for joining me.

Back in Asia, the Nikkei is still in the doldrums while the other major bourses perform pretty well on the prospect of cheaper money.

But in Japan a delay in the US hike has served to strengthen the yen, which is bad for exports and for stock markets.

Only a weakening yen will bring relief to the Nikkei according to Capital Economics’ Julian Jessop, who said in a note:

The single most important driver of equity performance in the next year or so is likely to be renewed weakness in the yen.

He sees the prospect of more QE from the Bank of Japan and a rate hike by the Fed as the two main factors to that situation around.

Updated

IG seeing European markets opening down, but only slightly.

China selloff was a 'necessary correction' – French finance minister

The French finance minister, Michel Sapin, is in Beijing and he’s being polite about the state of the Chinese economy.

It’s a real concern for a lot of people, including America’s finest economic brains. But Sapin said he sees no particularly significant risk from recent stock market turbulence and the recent fall was a “necessary correction”, Reuters reports.

Updated

Opinion still mixed on whether the Fed move was the correct one.

Chris Weston from IG in Melbourne has delivered his verdict on the day’s events and his view is that the Fed was as dovish as it could possibly have been and would have gone for a rise if it had not been for the August turmoil in China.

It seems logical the central bank would have raised rates if it weren’t for recent international developments, but they tried desperately to buy themselves flexibility.

And as he says in conclusion, it could get interesting in Europe today despite the fairly muted response in Asia:

It promises to be a very interesting session in Europe and the US, as traders have time to really assess the Fed’s view and what it means for markets. As always, the first move might not be the right move and cooler heads should prevail.

Updated

Summary

Time for a quick recap on the day’s main news here in Asia Pacific:

- The region’s markets have reacted positively to the Fed’s inaction, except the Nikkei in Japan which is down 1.42%. The Shanghai Composite is just about to restart after a lunch break but is up 0.4%. The Hang Seng is up 0.42% and the ASX200 is 0.83%

-

European markets are expected to open higher

- The chief of Australia’s central bank says the Fed will hike rates “by Christmas”

- The US dollar slipped back against Asian currencies, slipping to a three-week low against the euro and a basket of currencies

- Chinese house prices edged up for the fourth month in a row

As dawn breaks over Europe this is a good time to see what’s happening with the futures markets.

And it looks like the main markets will be up with FTSE predicted to open up 0.32%, the DAX in Germany up 0.26% and the CAC in paris up 0.32%.

Looks like the jury is still well and truly out on whether China’s economy is going to have a hard or soft landing as it decends from the heights of double digit growth. One of the reasons the Fed gave for keeping on hold were “heightened concerns” about the global economy in the wake the sharp selloff on Chinese stock markets in August and whether that means China can keep driving global growth as it has helped to do since the GFC.

Developments we saw in financial markets in August partly reflected concerns of downside risk to Chinese economic performance and the deftness with which policymakers are addressing those concerns.

If you want to see her full press conference, here it is:

Chinese house prices rise

Today’s most interesting data comes from China where home prices inched upwards for a fourth consecutive month in August.

Average new home prices inched up 0.3% in August from the previous month, according to Reuters calculations based on data released by the national statistics bureau on Friday, the same pace as in July.

But Reuters reported that the Chinese property market – source of many concerns about the health of the economy – would not be booming again any time soon.

Analysts do not expect a full-blown turnaround any time soon, as a huge overhang of unsold homes discourages new construction and investment in all but the biggest cities.

Back to the markets then and the Japanese stock market has started up again after the lunch break. The Nikkei is still down though at 18,170, a fall of -1.4%.

Elsewhere it seems reasonably calm. In fact you could say the S&P/ASX200 here in Australia is having a good day. It is standing at 5,189 points, a rise of 0.8% on the day.

The Shanghai Composite in China is up 0.4% at lunch.

Stevens’ testimony before the House of Representatives economics committee was wide-ranging. he also spoke about how he thinks the Australian economy will weather the headwinds facing China which Janet Yellen is so concerned about.

Whether that financial volatility itself will serve further to dampen global growth prospects remains to be seen. Sometimes such events portend a wider set of economic events, but just as often, they don’t.

There is still a pretty good chance that we will come out of this episode fairly well, and much better than we came out of previous episodes of this type.

US Fed will raise rates before Christmas – RBA chief

Glenn Stevens, the governor of the Reserve Bank, has weighed into the debate today. Despite suggestions that the Fed might now not raise until 2016, he thinks it will raise rates before Christmas. That means either at its October meeting or in December.

Speaking at a parliamentary hearing in Canberra, he said:

I would still think an increase in the Fed funds rate is probably going to happen this year.

The majority of FOMC [Federal Open Market Committee] members still think that they’re likely to start raising this year, there’s two meetings left.

Australia can weather global turmoil – RBA

Glenn Stevens, the governor of the Reserve Bank of Australia, has been giving evidence today to a parliamentary committee. He has an optimistic view of the economy and thinks it can weather the headwinds threatening China and which are worrying Janet Yellen so much.

Stevens told the House of Representatives economics committee in Canberra:

There is still a pretty good chance that we will come out of this episode fairly well, and much better than we came out of previous episodes of this type.

In the period ahead if we can get the non-resources part of the economy to keep improving gradually, build some confidence ... then we’ll get the unemployment rate to come down.

We ought be looking to get back into the fives over time, and given enough time I think we will, unless we’re hit by a bad shock somewhere [NB it’s currently 6.2%].

Nine years is a long time in global economics. Check out that gold price.

As mentioned below, the Australian dollar has benefited from the expectation that US borrowing costs would stay on hold and rein in the long march of the greenback. As a result it has rallied around 2c in the past week or so since sinking to a new six-year low and this afternoon is buying US71.95c.

Early on Friday it spiked to US72.76c, its highest level since August 24.

Updated

Here’s some more reaction.

It is not in doubt that the Fed intends to raise rates, but the question that has obsessed economists and investors for the past couple of years has always been the timing.

For Larry Elliott, the Guardian’s economics editor, Thursday night’s decision shows that the Fed has become ultra-cautious and does not want to risk hiking rates if it has to reduce them again because the recovery is not strong enough. You can read his full article here but this is the main thrust:

This is the weakest recovery the world’s biggest economy has experienced in modern times and even now, more than six years after the trough of the recession, there are mixed signals. The Fed is not entirely convinced that it is party time for the US economy.

The Fed is also weighing up the implications of a US interest rate increase on emerging markets, and in particular whether the prospect of higher US yields will intensify capital flows out of countries such as China and Brazil.

So when will rates rise? When there is a further improvement in the jobs market and when the Fed is “reasonably confident” that inflation is on course to move back up to 2%. Not yet, in other words.

Markets-wise it has been a bit mixed. The expectation was for a hold so the semi-rally in stocks and currencies suchas the Australian dollar in recent days showed that the decision has been priced in.

However, there has still been a bit of action, notably in Japan where the Nikkei plunged on the opening before fighting back.

Here are the scores so far:

- Nikkei down 1.39%

- Shanghai Composite down 0.15%

- S&P/ASX200 up 0.41%

- Hang Seng up 0.39%

- Kospi up 0.52%

Good afternoon/morning and welcome to the markets live blog following the Fed’s decision to keep rates near zero.

You can read how the action unfolded here as relayed by my colleagues Graeme Wearden and Jane Kasperkevic. But the main takeaway seems to be that the very dovish comments from Fed chair Janet Yellen suggests that she and her fellow committee members might wait until next year to increase borrowing costs.

here’s the verdict of the world’s biggest bond trading company, Pimco.