A long day of down selling without much respite across the globe has ended with the US’s Dow Jones Industrial Average stock index closing down lower in a single day than it has since the country’s national debt was downgraded by Standard & Poor’s. The Nikkei lost a full 3.8% today and the FTSE lost 3.03%, with other European markets faring poorly as well.

The bad news that appears to have kicked off the crunch comes primarily from the Chinese manufacturing sector, which was lower last month than it has been in three years. Those specific economic woes aren’t solely Chinese: the French manufacturing sector contracted at a faster rate in August than it had the month prior, and growth in US manufacturing has slowed, as well.

Last week’s highs and lows in the American market were marked by frantic trading throughout the day; today the Dow collapsed at open and stayed low throughout the day.

This liveblog is closing down for the day but we’ll be continuing to cover the markets around the clock and will return to live coverage as stock exchanges open tomorrow.

Updated

All three major indices in the US stock markets closed down more than 2.8% today

The Dow, the Nasdaq and the S&P 500 all closed far below their opening prices today after a day of panicked selling of a kind not seen since Black Monday 2011.

- Dow Jones Industrial Average - 16,058.35, down 469.58 points, -2.84%

- S&P 500 - 1913.87, down 58.31 points, -2.96%

- Nasdaq - 4,636.10, down 140.40 points, -2.94%

S&P 500: 497 stocks down today. With data going back to 1996, hit 500 only once: August 8, 2011. $SPX pic.twitter.com/cg6ztLAO5Z

— Charlie Bilello, CMT (@MktOutperform) September 1, 2015

Sobering: 497 of the 500 stocks in the S&P 500 are down overall today (at the moment). August 8 is a bad day in US market history - it’s the day Standard & Poor’s (the S&P of S&P 500) downgraded US sovereign debt from AAA or “risk free” to AA+, better known as Black Monday 2011.

There are two other Black Mondays: October 19, 1987, when a stock market contagion spread from Hong Kong (people still argue about why - everyone blamed computers at the time), and October 28, 1929, in many ways the starter pistol for the Great Depression.

For perspective, the Dow lost 12.82% on Black Monday in 1929 (and then another 11.73% the next day), 22.61% on Black Monday in 1987, and 5.55% on Black Monday in 2011. It’s down by 2.80% at the moment, so this is more of a Grayish Monday at worst.

Updated

Here’s a quick chart of all the stocks on the Dow just before the top of the hour, ranked by largest chunk of share price lost thus far today. Data captured at 2:58pm.

Edited to add: the number on the far right is volume, or total shares traded, bought or sold.

Updated

Cartoonists try and stay one step ahead of the political circus. New Carousel @politico http://t.co/wkF1koEVEQ pic.twitter.com/vuADzhVUTc

— Matt Wuerker (@wuerker) August 28, 2015

A quality cartoon from the great Matt Wuerker last week has aged disappointingly well.

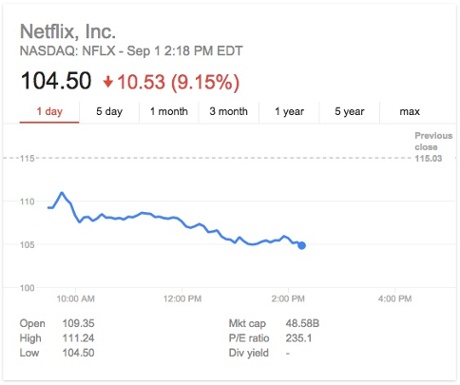

Netflix, a stock that has gone from strength to strength over the last several years, has had a rough day. It took a hit like the rest of the market throughout August but today it seems to have been singled out for shareholder ire (well, not singled. Energy stocks aren’t doing great!) and is down by more than 9%.

There are three parts to the stock’s troubles today:

1. It’s a lousy day to be publicly traded.

2. Variety reports that Apple may get into original streaming content, the market that Netflix has dominated for years despite legions of imitators who’ve tried (mostly in vain) to woo the company’s loyal customers. Betting against Netflix has been bad business, but betting against Apple is also rarely a winning proposition.

3. The company chose to forego the renewal of a lucrative deal with Epix. It’s a contract that was likely invisible to most consumers but it also put a lot of recent-run movies on the service. Now that Netflix is deeper and deeper in business with Disney (which also sells the streaming service its Marvel Comics live-action shows), Netflix is hoping its upcoming streaming of Disney films will make up the shortfall. The trouble is that there’s a gap between the end of the Epix contract and the start of the Disney, and Epix is signing up with competitor Hulu.

Updated

The Dow is off by more than 400 points

The Dow is now off more than 400 points http://t.co/Js3NGwHm3W pic.twitter.com/swTuKZZzy0

— Bloomberg Markets (@markets) September 1, 2015

This chart is an hour old but it’s still within five points of the Dow as I type this.

Updated

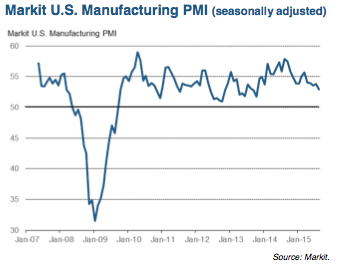

A little more color on the decline in the manufacturing sector: The Institute for Supply Management’s (ISM) monthly report reveals that manufacturing is losing momentum and businesses in that sector are skittish.

“Business is guarded but steady. Margins are tight. Markets are very competitive. China is lackluster,” said an unattributed statement from one of the index’s constituent companies in the wood products industry.

The ISM’s main metric, Purchasing Manager Index (PMI), is an important bellwether for the sector (although perhaps not for the economy overall, according to Rob Carnell in the linked block): PMI above 50 percent indicates that the manufacturing economy is expanding overall; below 50 percent indicates that it’s declining.

In August the index was at 51.1, down from 52.7 the previous month.

Updated

This is Sam Thielman in New York taking over from Nick.

Thus far, things have not gone well in the US markets today. The Dow is down more than 400 points and the S&P 500 is off by more than 50, both hovering around a 2.5% percent decline. The market still has three hours open but if trends continue it will be a rough start after the worst month global markets have seen in years. August’s 6.86% decline exceeded the 9.34% falloff in May 2012, according to S&P Dow Jones Indices.

Energy shares fell for the first time in five days, giving back much of the sector’s recent rally, and commentators are again discussing whether the declines will trip the New York Stock Exchange’s “circuit breakers” – automated trading curbs designed to prevent losses from accruing too quickly.

Updated

Despite the poor Chinese manufacturing data and the negative market reaction, things may not be as bad as they seem, reckons Capital Economics. Its global economist Michael Pearce said:

Markets inevitably focused on the weak surveys in China, where the official and Markit manufacturing PMIs fell to a four and six-year low respectively. However, we do not think that the immediate economic outlook there is quite as bad as many headlines suggest. Industrial activity has been depressed by a range of temporary factors which should fade in the coming months, while recent policy easing is still feeding through to the broader economy.

For the most part, any weakness appears to have been limited to China. Manufacturing PMIs in the rest of Emerging Asia remained weak, but the global manufacturing PMI excluding China has held up much better in recent months.

Admittedly, the latest manufacturing surveys for the US point to continued weakness in the sector. But this is primarily due to the stronger dollar and is not a major concern given that growth in the much larger services sector is motoring ahead.

Elsewhere, a breakdown of the euro-zone PMIs revealed declines in both Italy and Spain. The drop in the Spanish manufacturing PMI was the third in a row and suggests that the breakneck pace of expansion in the first half of the year is unlikely to be sustained. Spain’s growth rate is likely to slow further over the coming years as the boosts from a weaker euro and lower oil prices fade.

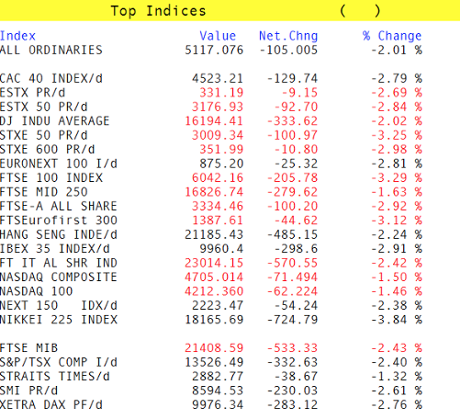

European markets close sharply lower

It started in China, again, and sent global markets tumbling once more. Disappointing Chinese manufacturing data set the tone for the day, with commodity companies hit particularly hard and oil prices on the slide. A slowdown in eurozone and UK factory growth did not help matters, nor did weaker than expected US data. So with renewed concerns about the Chinese economy, along with concerns that QE was not helping the eurozone much, and uncertainty over the timing of a US rate rise, investors had every reason to cash in. With a number of key economic indicators this week, not least the US non-farm payroll numbers on Friday, there is likely to be little let up for stock markets. The closing scores showed:

- The FTSE 100 fell 189.4 points or 3.03% to 6058.54, with mining companies the leading losers and only one riser in the form of engineering group Meggitt

- Germany’s Dax dropped 2.38% to 10,015.57

- France’s Cac closed 2.4% lower at 4541.16

- Italy’s FTSE MIB finished down 2.24% at 21,451.37

- Spain’s Ibex ended 2.59% off at 9992.8

- The Athens market fell 0.43% to 621.51

Meanwhile on Wall Street the Dow Jones Industrial Average is currently 348 points or 2.1% lower.

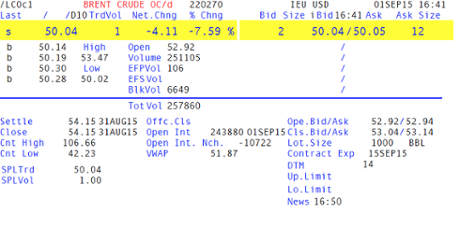

Oil is one of the fallers of the day, with Brent crude now down more than 7.5%:

Updated

Here’s our latest report on the day’s market falls, from Katie Allen:

Global stock markets staged a dramatic start to September as rising worries about China’s economic slowdown sparked fresh sell-offs in Asia, Europe and on Wall Street.

After suffering their worst month in three years in August, US shares tumbled after Tuesday’s opening bell. In early trading, the Dow Jones industrial average was down 2.2% and the S&P 500 had sold off 1.9%. News that US manufacturing activity slowed in August added to pressure on share prices.

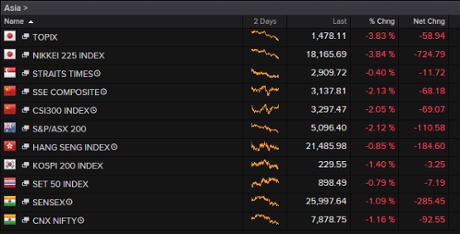

The sell-off on Wall Street mirrored losses in Asia overnight, and later on European bourses, in the wake of more weak data on China’s manufacturing sector, suggesting output slumped to a three-year low in August. Worries about waning demand from the world’s second biggest economy left Japan’s Nikkei down a hefty 3.8%, taking it close to a six-month low last week. China’s Shanghai composite index suffered a smaller 1.3% loss.

As the sell-off rippled out to Europe, the FTSE 100 index of bluechip London-listed shares was down more than 3% at 6,056 on Tuesday afternoon, extending last month’s sharp losses. A 6.7% drop during August marked the worst month for UK’s leading share index since May 2012. The pan-European FTSEurofirst 300 shed 9% over the same period, the worst monthly performance for four years. On Tuesday it was down 3%.

Investor confidence has been rattled by a combination of factors. Alongside signs China’s economy is slowing, the country’s stock market has tumbled from multi-year highs in June and interventions by policymakers have done little to stem the rout.

At the same time, markets are bracing for the prospect of the first US interest rate rise since before the global financial crisis.

Full story here:

Updated

Reports of further Chinese action to help stabilise its stock market, from the South China Morning Post:

BREAKING: 50 China brokerages will jointly contribute 100 bln RMB capital to gov margin finance agency to start "new round of market rescue"

— George Chen (@george_chen) September 1, 2015

New round of capital contributions by 50 firms came after CSRC meeting Saturday as regulator urge sec industry to be united to stabilize mkt

— George Chen (@george_chen) September 1, 2015

And the slide in global markets continues:

Over to Greece, and there are reports that the country’s creditors may delay the first bailout review by a month or so to November.

Citing EU sources, agency MNI said the creditors are worried that the forthcoming election may derail the economy, and they have yet to agree on milestones for the next tranche of funding for the country. This move could push talks of potential debt relief further into the distance.

Ahead of the US non-farm payroll numbers on Friday, ING Bank’s Rob Carnell has been reading the runes of today’s ISM data for clues to the jobs figure:

With Federal Reserve vice-chair, Stanley Fischer, hinting over the weekend at his Jackson Hole speech that a September rate hike remained possible (and downplaying what is likely to be a soft CPI release later this week), the market is turning its attention to data relevant to Friday’s all-important labour report.

The run-up to this report kicked off today with the August manufacturing ISM. The headline index fell from 52.7 in July, to 51.1 in August, but the focus currently has to be on the employment index of this survey. This fell 1.5 points to 51.2.

Unfortunately, of all the data we have to scrutinise this week, this is perhaps the least useful of all. Changes of the manufacturing ISM employment index have a correlation of only 0.3 with changes in the non-manufacturing ISM employment index since January 2013, which should arguably be a more reliable index for payrolls given its broader coverage of the labour market. But even that correlation is the wrong sign, and we should probably ignore it completely.

In comparison with the manufacturing ISM, its big-sister index, the non-manufacturing ISM has virtually no correlation at all with the directional change in the first release of payrolls changes. Over the same period, its correlation is 0.02 (though we take solace in it having at least the right sign). In short, today has told us nothing, and may even be misleading. Moreover, the non-manufacturing index release on Thursday will be only about as useful as tossing a coin.

All of which leaves the ADP index on Wednesday as the least worst of a very bad bunch of payrolls indicators (correlation Jan 2013 to present equals +0.55). Consensus is looking for 200,000, up from 185,000 in July. Anything either side of that could see big market swings.

Updated

The weak manufacturing data has pushed Wall Street even lower, with the Dow Jones Industrial Average now down 380 points or 2.3%.

US manufacturing growth slows in August

The slowdown in US manfacturing growth has been confirmed by the Institute of Supply Management.

Its index of factory activity fell to 51.1 in August from 52.7 the previous month, the lowest reading since May 2013. It was below analysts’ expectations of a 52.6 reading. With the global economy - especially China - showing signs of slowing down, it is no surprise that US export orders are under pressure.

ISM export orders lowest since 2009 record low. Prices Paid sink to 39 from 44.

— Ashraf Laidi (@alaidi) September 1, 2015

With both the ISM and the Markit reports showing a weaker than expected economy, a decision by the US Federal Reserve to raise rates in September is again thrown into question.

Dow back in correction territory, trades >10% below high. pic.twitter.com/izv9oK5Mg4

— Holger Zschaepitz (@Schuldensuehner) September 1, 2015

The US manufacturing sector grew at its slowest pace in almost two years in August, according to the first of the day’s two sector surveys.

The final US manufacturing purchasing managers’ index from Markit fell to 53 from 53.8 in August. This was the lowest level since October 2013, but was slightly higher that the preliminary reading of 52.9. Tim Moore, senior economist at Markit, said:

August’s survey highlights that the US manufacturing sector continues to struggle under the weight of the strong dollar and heightened global economic uncertainty, but resilient domestic spending and subdued cost pressures are keeping the recovery on track.

Reflecting this, new orders from abroad have now fallen in four of the past five months, which represents the weakest phase of manufacturing export performance since late-2012.

Updated

More details on the opening falls in US markets from my colleague Dominic Rushe:

The Dow was off around 2% the S&P 500 1.37% and the Nasdaq 1.9% as investors reacted to more bad news about China’s economy. The falls followed a small dip on Monday. When the markets closed, they had experienced their worst August in three years.

Dow opens down 300 points

As expected, Wall Street has opened sharply lower.

The Dow Jones Industrial Average is down more than 300 points or nearly 2% within minutes of the opening, in the wake of poor Chinese data and ahead of two surveys of US manufacturing.

The stock exchange has invoked Rule 48 - which suspends a requirement for stock prices be announced at the market open and is designed to help market makers in times of major volatility. This is the fourth time in two weeks the exchange has used this regulation.

Summary: Another bad day in the markets

Time for a recap, while we brace for the opening of Wall Street (and manufacturing PMIs from America).

On a trip to Indonesia, Christine Lagarde sounded the alarm, saying:

Other emerging economies, including Indonesia, need to be vigilant to handle potential spillovers from China’s slowdown and tightening of global financial conditions.

Lagarde also warned that global growth is weaker than the IMF had expected, further dampening optimism over the world economy.

Here’s the full story:

2) World stock markets have also been hit by fresh worries over China’s economy, after a new survey showed that its factories are shrinking at the fastest pace in five years.

There is also concern over Europe’s recovery, after factory growth in Spain and Italy slowed, and France suffered another contraction.

Europe’s stock markets are all deep in the red today, with mining stocks leading the rout. Here’s the damage:

-

FTSE 100: down 188 points or 3% at 6071

-

German DAX: down 292 points or 2.8% at 9966

-

French CAC: down 125 points or 2.7% at 4527

Investors remain gripped by worries over China’s economy, a week after Black Monday and three weeks after the surprise devaluation of the yuan.

As Jasper Lawler of CMC Markets puts it:

Another set of disappointing Chinese manufacturing data prompted a lower open for UK and European stocks on Tuesday with a slowdown in Europe’s own manufacturing sector exacerbating the declines.

Asian markets had already suffered a bad day. Japan’s Nikkei fell almost 4%, and the Shanghai Composite lost 1% despite a late recovery that suggested the authorities had intervened again.

These photos show the picture at stock markets worldwide.

3) Canada’s economy has fallen into recession, underlining weaknesses in the global economy.

4) But there are (much-needed) signs of recovery in the eurozone labour market.

The jobless rate dipped to 10.9% in July, despite rising unemployment in France, Finland and Austria.

Wall Street is not a happy place today, as fears over China’s economy sweep through New York again.

The Dow is now expected to shed 400 points, or 2.4%, when trading kicks off in 45 minutes.

BREAKING: Dow futures tumble 400 points amid China data jitters http://t.co/NoDteakQPF

— CNBC Now (@CNBCnow) September 1, 2015

Canada falls into recession.

The Canadian economy has been dragged into recession by the fall in the oil price, and the weaker global economy.

Canada’s GDP fell by 0.1% in the second quarter of the year, new data from Statistics Canada show.

That’s not as bad as economists expected. But, following a 0.2% contraction in January-March, it means Canada is officially suffering a ‘technical recession’.

Some photos from the world’s stock markets, on another worrying day for investors:

Today’s falling markets show that investors simply cannot shake off their fears over China, says Philip Marey, strategist at Dutch financial group Rabobank:

“The problem is that we have these brief spells of optimism like we had last week when U.S. GDP was revised up, but the overall theme is still the weakness in China and that is very hard to dispel from markets.”

(via Reuters)

Updated

Analysts at Barclays are concerned that China’s manufacturing PMI fell to a three-year low last month. Here’s their take:

“The summer weakness [in China] could be linked to the recent Tianjin port explosion and large-scale factory closures in Beijing ahead of the WWII victory day parade on 3 September,”.

“Even so, we believe the multiyear-low PMI confirms that the economy is still not on a solid footing, and we look for a flat growth profile during the rest of 2015, with continued downside risks,” they added.

One UK company is bucking today’s selloff, though - Aga Rangemaster, whose shares have jumped 10%.

The takeover battle for Aga intensified this morning when white goods maker Whirlpool made an approach to the cooker maker, potentially beating an earlier bid from Middleby.

My colleague Sean Farrell explains:

Whirlpool’s intervention pits two US companies against each other to take Aga into foreign ownership more than 80 years after its kitchen ranges were first manufactured in Britain...

The Aga cooker, made mainly from scrap metal, absorbs heat from a constantly burning source, which is then used for cooking. The cookers became an established feature of cultural life in 1990 when the Oxford Companion to English Literature first included the term “Aga saga” – intended to sum up the novels of Joanna Trollope and once memorably characterised as tales of illicit rumpy-pumpy in the countryside.

Cripes! More here:

Every share on the FTSE 100 index has lost ground today, as the City kicks off September with a broad-based selloff.

That has left the FTSE 100 languishing down 2.1%, or -133 points, at 6114.

Dawn just broke over New York, but there’s not much sunshine in the markets.

The US stock market is expected to fall by over 2%, when Wall Street opens at 9.30am local time (2.30pm BST).

Market Sell-off: US Futures Extend Losses; Dow & S&P Futures Fall More Than 2%: Dow Fut 16156.00 -2.13% #MarketSelloff

— CNBC-TV18 (@CNBCTV18Live) September 1, 2015

August was the worst month for the US stock market in three years, and there’s no sign (yet) that September will show a strong recovery.

Overnight, Australia’s central bank left interest rates unchanged at their current record low of 2%.

The RBA flagged up the “further softening in conditions in China and east Asia” recently, but also pointed stronger US growth. Economists believe Australia’s economy will slow, as China’s troubles ripple through the global economy.

Here’s the full story:

Good news: Eurozone unemployment at a 3 & half year low. Bad news: It's 10.9%.

— Duncan Weldon (@DuncanWeldon) September 1, 2015

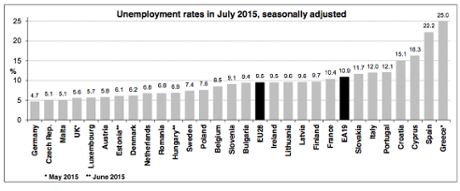

Eurozone unemployment falls below 11%

Finally, some good news. The eurozone’s jobless rate has fallen to its lowest level since 2012.

Unemployment across the single currency region dipped to 10.9% in July, down from 11.1% in June.

The recovery was broad-based, with unemployment falling in 23 EU member states and stable in two (Belgium and Romania). Only Finland, France and Austria suffered rising joblessness over the last 12 months.

Guess what: there's only 3 EU countries where the unemployment rate ↑ in July: Finland (to 9.7%), France (to 10.4%) & Austria (to 5.8%)

— María Tejero Martín (@Maria_Tejero) September 1, 2015

As usual, the lowest unemployment rate was recorded in Germany (4.7%), followed by the Czech Republic and Malta (both 5.1%).

The highest (of course) was Greece (25.0% in May 2015) and Spain (22.2%).

Youth unemployment remains far too high, with 21.9% of under-25s out of work across the eurozone.

And while the drop in unemployment is clearly welcome, Europe’s unemployment rate is roughly double that of America (5.3% in July).

Updated

Tens of thousands of protesters are marking Christine Lagarde’s visit to Jakarta with a demonstration.

They are calling for higher wages and an end to job cuts, and urging Indonesia’s leaders to launch new stimulus measures to kick-start its economy.

Lagarde: Prepare for bumpiness from Chinese slowdown

The head of the International Monetary Fund, Christine Lagarde, has warned emerging nations to brace themselves for the impact of China’s economic slowdown.

Speaking in Indonesia today, Lagarde said the global economy was weaker than the IMF had expected. And the recent spike in “global risk aversion and financial market volatility” could hurt growth in Asia.

China is a particular cause of concern. Lagarde said:

As the Chinese economy is adjusting to a new growth model, growth is slowing—but not sharply, and not unexpectedly. The transition to a more market-based economy and the unwinding of risks built up in recent years is complex and could well be somewhat bumpy. That said, the authorities have the policy tools and financial buffers to manage this transition.

Other emerging economies, including Indonesia, need to be vigilant to handle potential spillovers from China’s slowdown and tightening of global financial conditions.

IMF's Lagarde says other EM economies need to be vigilant for spillovers from China's slowdown & tighter global fincl conditions @Reuters

— Sri Jegarajah (@cnbcSri) September 1, 2015

The IMF chief also warned that the US Federal Reserve is close to raising America’s interest rates, potentially dragging capital out of developing economies:

There are signs that the recovery is firming up in the United States, advancing the prospects of interest rate lift off.

This could pose a risk for emerging economies, including Indonesia, in the form of weaker capital flows, higher interest rates, and financial volatility.

Lagarde also challenged Indonesian leaders to end the exclusion of young people and women from its economy. Here’s the full speech

Indonesia’s youth are vital for renewing growth momentum; they are the next change agents http://t.co/e5lu9f7PGn pic.twitter.com/UOT2ZRSMVZ

— Christine Lagarde (@Lagarde) September 1, 2015

Updated

Connor Campbell of SpreadEX confirms that the problems in China’s factories have pushed European shares down this morning:

After that awful August things haven’t gotten off to the greatest start this September, with further disappointing data from China immediately creating drag for the European indices.

Weak manufacturing and services PMIs from both the official figures and the Caixin surveys shows the Chinese slowdown is showing no signs of, well, slowing down.

Growth in Britain’s factory sector also slowed last month, Markit says.

The UK factory PMI dipped to 51.5, from 51.9, dashing City hopes of a small increase in growth.

UK Manufacturing PMI (August) = 51.5 vs 52.0 expected and 51.9 previous

— World First (@World_First) September 1, 2015

Firms also reported that employment levels fell in August, for the first time in two years.

Updated

European selloff deepens after PMI reports

Europe’s stock markets are now down by around 2.5%, following the double-whammy of weak manufacturing data from China (see here), and mixed reports from Europe (here)

The FTSE 100 has now shed 143 points to 6103, as September gets off to a downbeat start. Glencore, the commodities trading firm, has fallen by 6%.

Jameel Ahmad, chief market analyst at FXTM, says investors are alarmed by the latest signs of economic weakness in China, where factory output shrank last month.

While it is true that expectations were for a contraction anyway, the data just provided further confirmation that economic momentum is slowing down in China with the economy looking further exposed and increasingly vulnerable to dropping below Beijing’s 7% GDP before the end of the current quarter.

The chances of GDP growth falling below the government’s target are actually intensifying each time an economic announcement is released from China, mainly because all data is consistently pointing towards the economic momentum declining in this major economy.

Updated

Eurozone factory growth slows

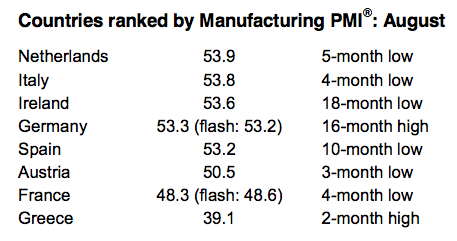

European stock markets are falling deeper into the red, after data firm Markit reported that Europe’s manufacturing growth slowed in August.

Markit’s eurozone PMI dipped to 52.3, from 52.4 in July. Decent growth in Germany, the Netherlands and Spain was balanced by fresh contractions in France and Greece:

Rob Dobson, Senior Economist at Markit, says Europe’s factory sector showed “resilience” last month.

However....

Given the ongoing situation in Greece it was not surprising to see that nation’s manufacturing sector register a further sharp downturn, although a sharp slowing in the rate of contraction raises hopes that the lowest point has been passed.

The French industrial sector also remains in the doldrums and is likely to continue to act as a drag on the broader French economy.

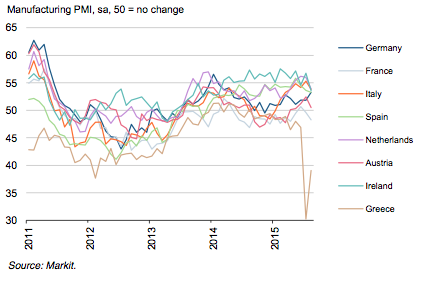

And this charts shows just how Greece’s economy suffered from the introduction of capital controls this summer, as its bailout crisis escalated:

Updated

German factories have bucked the trend, posting their fastest growth in 16 months.

Germanys manufacturing PMI jumped to 53.3 in August, from 51.8 a month earlier.

Firms reported that they received more new orders, from home and abroad, leaving many with larger backlogs of work.

This is worrrying. France’s factory sector shrank at a faster rate last month, adding to the gloom.

The French manufacturing PMI fell to 48.3, from 49.6 in July, indicating a sharper contraction (50 = the cut-off point between expansion and contraction).

Here’s Markit’s bullet points:

- Output and new orders fall at sharper rates

- Further slight drop in employment

- Prices charged decline at fastest pace in three months

Dutch manufacturing #PMI drops to five-month low of 53.9 in August http://t.co/tEHBap8t5G

— Markit Economics (@MarkitEconomics) September 1, 2015

Growth in Italy’s factory sector has slowed to a seven-month low, suggesting its economy remains lacklustre.

The Italian manufacturing PMI dipped to 53.8 in August, from 55.3, with firms reporting slower growth in new orders, output and employment.

The selloff in Europe is deepening, wiping 100+ points off the FTSE 100 index:

Here comes the first European data of the morning.....and it shows that growth in Spain’s factory sector is still growing, but at its slowest rate since last October.

The Spanish manufacturing PMI fell to a ten-month low of 53.2 in August, down from 53.6 in July.

Markit, which compiles the data, says that manufacturing “continued to improve in August”. However...

While output rose sharply, there were signs of a slowdown in growth of new orders during the month.

China’s stock market also suffered fresh losses today, following the confirmation that its factory sector shrank last month.

The Shanghai Composite index just closed, down 1.2% at 3,165 points.

It had been lower earlier today, suggesting that Beijing authorities may have staged one of their regular interventions....

Updated

Germany’s DAX index is dropping back towards last week’s lows:

Scary September after stormy August: #Germany's Dax starts almost 2% lower to the new month. pic.twitter.com/PpoT1KlLMX

— Holger Zschaepitz (@Schuldensuehner) September 1, 2015

Mike van Dulken of Accendo Markets says today’s selloff shows that risk appetite has been “sapped” by the latest disappointing China PMI data.

Manufacturing has contracted to a three-year low low as Beijing’s stimulus effort fail to deliver, maintaining investor anxiety about the impact of economic slowdown on global growth.

The Services sector may remain buoyant (expanding, but more slowly) but this is offering little relief.

Updated

FTSE 100 falls in early trading

Britain’s FTSE 100 index has fallen by 70 points at the start of trading, as September begins where August left off.

That’s a tumble of around 1.2%.

Mining shares are the biggest fallers, with Anglo American and BHP Billiton shedding around 3%. That reflects concerns over China’s weakening economy.

The other European markets are also losing ground, with Germany’s DAX down 1.8% and France’s CAC dropping 1.5%.

The oil price has fallen around 2.5% this morning, sending Brent crude down to $52.82 per barrel.

That follows three extraordinary day’s trading in which oil surged by 25%, having hit its lowest levels since 2009 a week ago.

Updated

Nikkei falls 3.8%

Japan’s Nikkei index has fallen by almost 4% today, as the latest disappointing Chinese data hurts stock markets across Asia.

Here’s the current situation:

The news that China’s services firms reported slower growth is a worry, says Angus Nicholson of IG:

China’s rebalancing of the economy requires robust and steady reallocation of labour to the services sector and away from the over-capacity industrial sector, and it is this element of the PMIs that is most worrying.

Japanese manufacturers are also suffering from the recent strengthening of the yen.

A strong move by the Yen to 120.5 and weak #China #PMI has seen the Nikkei 225 in Japan fall by nearly 4% to 18,165 today #Abenomics

— Shaun Richards (@notayesmansecon) September 1, 2015

Updated

Introduction: Chinese manufacturing hits three-year low

Good morning.

After the drama of August, September is getting underway with fresh falls across Asia’s stock markets. And Europe likely to follow suit when trading begins shortly.

Investor confidence has been hit by fresh data from China overnight, showing that its factory output slumped to a three-year low in August.

China’s official manufacturing purchasing managers’ index (PMI), dropped to 49.7 in August from 50 in July. Any reading below 50 indicates that the sector has begun shrinking, and the survey has added to growing fears over China’s resilience.

As Zhao Qinghe, an economist with the National Bureau of Statistics, put it:

“There is insufficient growth momentum in the country’s manufacturing sector.”

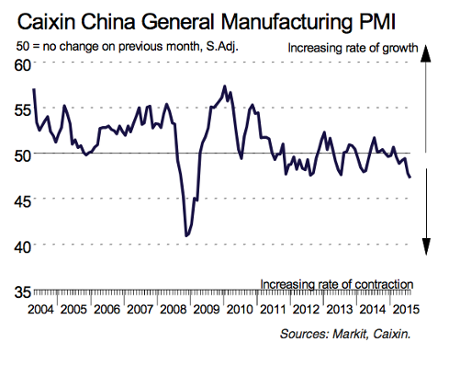

A separate survey of China’s smaller factories, from Caixin, released today fell to a six-year low of 47.3 from 47.8 in July:

Dr He Fan, Chief Economist at Caixin Insight Group, warned that:

“The final Caixin China Manufacturing PMI for August continued to retreat, with sub-indices signalling continued weak demand in the markets for goods and factors of production.

Recent volatilities in global financial markets could weigh down on the real economy, and a pessimistic outlook may become self-fulfilling.”

And if that’s not enough, Caixin also reported that China’s service sector growth had slowed last month.

Spread-betting firm IG predict that the main European markets will suffer fresh losses today:

Our European opening calls: $FTSE 6161 down 87 $DAX 10092 down 168 $CAC 4575 down 78 $IBEX 10077 down 182 $MIB 21653 down 289

— IGSquawk (@IGSquawk) September 1, 2015

It looks like a rocky start to September for European markets with some key markets expected to open down around 2% thanks to #China data.

— Sally Bundock (@SallyBundockBBC) September 1, 2015

Coming up:

Many more manufacturing surveys are published today. That includes the eurozone at 9am BST, the UK at 9.30am, and the US at 3pm.

The latest eurozone unemployment data, for July, is released at 10am BST.

Investors should keep an eye on Greece too; Syriza’s leader Alexis Tsipras will begin his election campaign in Crete, in an attempt to woo voters ahead of the election on September 20.

Updated