European markets slump again

The relentless fall in European markets continued, writes Nick Fletcher, as investors worried about the eurozone economy after the week’s poor figures from Germany and comments from ECB president Mario Draghi that the recovery was running out of steam. And although the US market managed to edge higher in early trading, it was not a convincing rise after the 2% decline on Thursday. So the final scores showed:

- The FTSE 100 finished 91.88 points or 1.43% lower at 6339.97

- Germany’s Dax dropped 2.4% to 8788.81

- France’s Cac closed down 1.64% at 4073.71

- Italy’s FTSE MIB fell 0.94% to 19,200.97

- Spain’s Ibex ended 1.2% down at 10,150.5

In the US, the Dow Jones Industrial Average is currently 88 points or 0.5% higher.

On that note, it’s time to close up for the evening. Thanks for all your comments and we’ll be back tomorrow.

Updated

Here’s the latest views on the eurozone crisis from Dutch finance Minister and Eurogroup president Jeroen Dijsselbloem:

#Eurozone strategy paying off. Countries that vigorously implemented reforms returned to growth and will grow faster than #euroarea average

— Jeroen Dijsselbloem (@J_Dijsselbloem) October 10, 2014

Below average growth is result of reluctance to reform.#Eurozone should get act together, regain competitiveness and job generating capacity

— Jeroen Dijsselbloem (@J_Dijsselbloem) October 10, 2014

#Economic reform should be well designed: fiscal, structural and investment policies should be tailor made and coherent.

— Jeroen Dijsselbloem (@J_Dijsselbloem) October 10, 2014

No monetary or fiscal stimulus can replace the need to make our #economies more competitive & fit for the 21st century. It can only buy time

— Jeroen Dijsselbloem (@J_Dijsselbloem) October 10, 2014

Dijsselbloem Says French 2015 Budget Draft Far Away From Targets, Needs To Be More Ambitious

— cigolo (@cigolo) October 10, 2014

Dijsselbloem To Present New Growth Deal Proposal To EZ Leaders On Oct 23

— Live Squawk (@livesquawk) October 10, 2014

Updated

Here’s hoping for cheaper petrol, at least:

Global oil prices have fallen about 8% in the past four weeks. http://t.co/qeUlETXv0m via @WSJ pic.twitter.com/gT53AWFxQ6

— David Wessel (@davidmwessel) October 10, 2014

Now the Dow has bobbed back into negative territory, in rather choppy trading.

RT @carlquintanilla: Dow goes negative. @CNBC

— Henry Blodget (@hblodget) October 10, 2014

Updated

Back in Washington, UK chancellor George Osborne has warned that Germany’s recent weak factory and export data is a big concern.

- OSBORNE SAYS GERMAN ECONOMIC DATA IS GREATEST CONCERN IN EUROPE

- OSBORNE, ASKED ABOUT GERMANY, SAYS HE IS SKEPTICAL ABOUT REPEATED CALLS FOR MORE PUBLIC SPENDING

- OSBORNE SAYS SUPPORTIVE OF JAPAN’S “THREE ARROWS,” WANTS TO MAKE SURE ARROW OF STRUCTURAL REFORM IS FIRED

After a weak start, the US stock market is actually a little higher in early trading.

The Dow Jones has risen by 49 points, or 0.29%, to 16708. That claws back a little of yesterday’s rout (in which the Dow lost 335 points).

The S&P 500 index is also up, around 0.24%,.

The technology-heavy Nasdaq has lost another 0.5%, though, pushed down by last night’s profit warning from Microchip Technologies.

.@George_Osborne: We are at a critical moment for UK and world economy. I agree with @Lagarde: serious clouds are gathering on the horizon

— Ed Conway (@EdConwaySky) October 10, 2014

Osborne: "serious clouds gathering on economic horizon"

Over in Washington, chancellor George Osborne is reiterating his warning that the eurozone could drag the UK economy back.

He says there are “serious clouds” on the horizon, particularly the bit beyond the White Cliffs of Dover:

Here are the newsflashes:

- BRITAIN’S OSBORNE SAYS SERIOUS CLOUDS GATHERING ON ECONOMIC HORIZON, BIGGEST RISK IS EURO ZONE FALLING BACK INTO RECESSION

- OSBORNE SAYS BRITAIN IS NOT POWERLESS IN FACE OF EXTERNAL RISKS, HAS ECONOMIC PLAN

- REFERRING TO EURO COUNTRIES, OSBORNE SAYS IF YOU CREATE RULES ON FISCAL GUIDELINES, YOU CAN’T BREAK THE RULES AT THE FIRST TEST

Here’s a cautionary tale for anyone eating at their desk and spilling crumbs all over the floor (ahem...), staff at UBS’s offices in London are fighting off an invasion of mice.

Financial News reports:

UBS is looking for a cat with a large appetite, as staff struggle to control a mouse infestation inside its London office.

A number of people at the bank have told Financial News that they have seen mice scamper across desks, run past client meeting rooms and hide in draws.

Two people inside the 100 Liverpool St office blamed nearby construction work as the cause of the rodent invasion, with digging for Europe’s biggest construction project, Crossrail, “forcing them [mice] into surrounding buildings”.

“One mouse went into a managing director’s draw and ate his nuts, while another ran over an MD’s foot and she screamed while on a call,” said one ex-employee, who recently left the bank....

More here: Fat cat wanted as mice invade UBS

Summary: Markets slide, oil hammered

Fears over a looming eurozone recession, the wider global economy, the Middle East turmoil and Ebola have all help to drive stock markets down across Europe and Asia.

The FTSE 100 is down 66 points at 6365, and on track for a new one-year closing low. Earlier it fell as low as 101 points.

Germany’s Dax is also in retreat, having tumbled 2% or 183 points to 8825. That’s also a one-year low, as concern grows that Germany is entering recession.

With the French CAC down 1%, the MCSI index of world top shares is at its lowest point since April.

The copper price fell, on growth worries.

And the Brent oil price remains below $89/barrel, having hit a four-year low in early trading.

#FTSE100 hits intraday low of 6328.39, lowest level in almost exactly one year. #stocks TUI Travel biggest loser, -6% on Ebola spread fears.

— Andrea Tryphonides (@ATryphonides) October 10, 2014

Earlier, the Japanese Nikkei shed 1.1% and Australia’s market suffered its biggest one-day loss in 15 months.

Analysts say that “negative sentiment is rife” in the markets today, although the falls do not, yet any, constitute a crash.

H2O Markets’ chief market strategist, Mike Jarman, sums up the mood:

“The economic cycle has stalled, European macroeconomic data is starting to slow and the U.S. is in a hold position as investors continue to digest the tightening cycle and what it means for future growth prospects”

ETX Capital pointed to four key factors, particularly yesterday’s alarmingly weak German exports (down 5.8% in August)

Weak German export data raised fears yesterday that Europe’s Economic turmoil could drag down the Global economy.

Economic sanctions on Russia are halting Germany’s growth and in turn the Euro zone, causing US and Asian shares to go into meltdown last night.

The mood in Germany was further darkened by rumour that the Berlin government will cut its growth forecasts next week.

In other news...

The Bank of England has released details of its contingency plans for if Scotland had voted for independence

The minutes of the latest meeting of its Financial Policy Committee also show it is worried about the eurozone, and China’s slowing economy.

Eurozone and China risks trouble Bank of England http://t.co/yF5rISoS5x

— Jill Treanor (@jilltreanor) October 10, 2014

The UK trade deficit has narrowed, but Britain is still importing more than it exports.

And UK construction workers took a surprise breather in August, with output down 3.9%. George Osborne won’t be happy...

A couple of dates for the diary... the Bank of England has announced that it will release the results of its stress tests of UK banks on 16 December, at 7am GMT sharp.

And the eagerly-awaited eurozone stress tests, and asset-quality review, is due on Sunday 26 October.

Those results will show which banks need to raise more capital to protect themselves from future losses, and could shake out so-called ‘’zombie banks’ from the eurozone....

Bank of England to release bank stress test results on December 16. Merry Christmas everyone!

— James Titcomb (@jamestitcomb) October 10, 2014

The list of banks stress tested by EBA is here https://t.co/LRlR0QXaFm the list of banks subject to @ecb AQR is here http://t.co/eRahb1cQH3

— Lorcan Roche Kelly (@LorcanRK) October 10, 2014

Updated

German economists are hitting back against the notion that the country is heading off the rails.

Berenberg bank has tweeted this chart, to put August’s poor economic data into some context:

#Germany's August econ data calamity: The wheels are not coming off. #Eurozone not to blame. http://t.co/8F70sE6X6S pic.twitter.com/AkcddWj0hY

— Berenberg Economics (@Berenberg_Econ) October 10, 2014

And Matthias Heisse, managing partner in Munich for law firm Eversheds, pins the blame firmly on other countries - for not buying more of Germany’s goods:

“Exports have always been the backbone of the German economy but are of course dependant on buyers with money and foreign markets. Many eurozone countries are still in crisis and the economic sanctions against Russia did not support German exports.

Nevertheless, future prospects still remain broadly encouraging. The labour market seems to be very stable and domestic demand for goods could well rise, due to the minimum wage. Ultimately, it is exports, not the German economy, that is crumbling.”

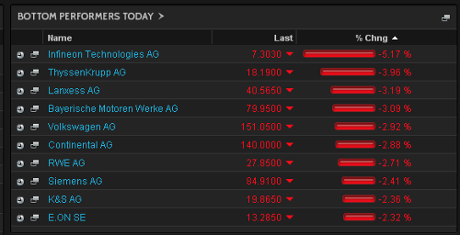

Every share on the German DAX has fallen today.

The biggest faller is Infineon Technologies, down 7% after rival chipmaker Microchip Technology released a profits warning overnight.

Several German automobile makers are also down around 3% , including BMW and Volkswagen.

Here’s the top fallers in the broad-based selloff:

Germany's Dax at one year lows. Ouch. pic.twitter.com/eXrajpjlc8

— kirsten donovan (@KirstenDonovan1) October 10, 2014

Updated

The Frankfurt stock market looked pretty calm this morning, as the DAX hit its lowest level of the year.

No sign of traders with the heads in their hands. After all, it’s only money....

And here’s a chart from Hargreaves Lansdown showing how markets have fallen from their recent highs:

Laith Khalaf, senior analyst at Hargreaves Lansdown, says that “negative sentiment is rife” in the financial markets today.

Worrying scenarios are thick on the ground. Take your pick from the spreading Ebola virus, conflict in the Middle East, withdrawal of QE in the US, and Europe teetering on the brink of deflation.

Another worry is that the US Federal Reserve is likely to end its bond-buying stimulus scheme at its next policy meeting at the end of October.

Khalaf adds:

Markets are likely to fret while they watch central banks pass the relay baton onto economic growth, in the hope they don’t drop it.

It’s obviously been a bad week in the stock markets -- the FTSE 100, for example, has shed 178-odd points or 2.7%.

And that makes it the biggest fall in, err, two weeks; shares also tumbled as September drew to close.

There’s a lot of chatter about whether global markets are entering a serious correction, after a long bull rally. We won’t know for a while, but right now, it certainly can’t be called a crash.

This is shaping up to be as bad as the 5% January correction that nobody remembers anymore.

— Morgan Housel (@TMFHousel) October 10, 2014

Darren Courtney-Cook, head of trading at Central Markets Investment Management, doesn’t reckon markets will turn around quickly (via Reuters):

“I don’t think there’ll be a full-on meltdown, but I think we will be in a bearish market for the next few weeks”.

Tin hats on, then, as some say in the City...

The news that UK construction output fell by 3.9% in August alone will not please chancellor George Osborne, our economics correspondent Phillip Inman writes:

The figures will disappoint the Treasury, which has championed housebuilding as a way out of the current housing crisis.

The fall in infrastructure construction will also prove a blow to George Osborne, who has repeatedly said new transport and digital infrastructure is necessary for sustainable growth.

Full story: Housebuilding falls for first time 18 months, ONS says

The US stock market is expected to suffer further losses when Wall Street opens in three hours time.

Steve Collins, global head of dealing at London & Capital Asset Management, has the details:

US Futures pointing at bad open DOW - 108 S&P -12.25 NAS -43.5 Russel 200 - 9.4

— Steve Collins (@TradeDesk_Steve) October 10, 2014

The selloff in Europe and Asia today has helped to pull down global shares to their lowest level in six months.

The MSCI All-Country World index is down 0.8% to its lowest level since April 18. It’s shed 1.9% this week.

Crumbs, it’s now a triple-digit loss on the Footsie.

The FTSE 100 is currently down 101 points, at 6330, down 1.5%. That means it’s lost 4.4% in October alone.

Mike McCudden at Interactive Investor adds his voice to those blaming the slowdown in Germany’s economy for today’s selloff:

The stuttering global economy continues to spook investors who appear to be on a mass exodus from equities to safer havens.

Furthermore, with the German economy leading the euro zone from the frying pan in to the fire there are grave concerns for the future of the region.

Tui Travel, the holiday firm, is now the biggest faller in the City, down 7%.

Nick Fletcher’s market report has the details:

Tui Travel leads FTSE 100 lower as economy and Ebola fears continue

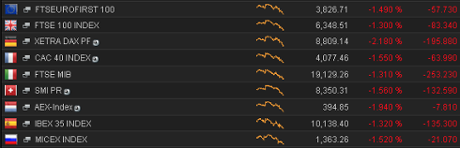

Here’s the situation across the European markets at 11am. Losses across the board....

European stock markets fall further, FTSE 100 down 91 points

The selloff in Europe’s stock markets is accelerating.

Fears over a possible eurozone recession, Ebola, and geopolitical turmoil in the Middle East all hit stocks.

The FTSE 100 is now down 91 points at 6340, a fall of 1.4%, to a new one-year low.

It looks destined to record its third weekly loss in a row, as the selloff that began on Wall Street last night, and then shook Asian markets (details here) reverberates around Europe too.

And in Frankfurt, the German DAX has suffered big losses, down 2.1% at 8799, amid those rumours that the government will slash its growth forecasts.

That’s also the lowest level for the DAX since October 2013.

TROUBLE! #Germany's Benchmark index Dax just hits a new 2014 low. Breaks below the 8800 mark. pic.twitter.com/hJOunFLLL9

— Holger Zschaepitz (@Schuldensuehner) October 10, 2014

And Brent crude oil remains below the $90-per-barrel, having hit a new four-year low of $88.11 this morning (details).

Analysts at ETX Capital blame the slump on “growing fears” about Europe’s weak economy:

Weak German export data raised fears yesterday that Europe’s Economic turmoil could drag down the Global economy.

Economic sanctions on Russia are halting Germany’s growth and in turn the Euro zone, causing US and Asian shares to go into meltdown last night.

Energy and mining stocks are being hit hard, as FT Markets editor Chris Adams flags up:

Stocks: Shell -2.4pct, BP -1.2 pct, Glencore -2.4 pct, Rio -2.7 pct, BHP -3.0 pct, Anglo -3.3 pct, Tullow Oil -4.2 pct, Antofagasta -3.1 pct

— Chris Adams (@chrisadamsmkts) October 10, 2014

That’s because slower global growth will mean less demand for oil, copper, iron ore, etc.... Will Hedden of IG explains:

Any name with a sniff of commodity exposure is struggling, be it oil or metal. Brent crude is below $90 for the first time in over two years, iron ore is in a similar position and this is making related names feel very unloved.

Australian shareholders are nursing losses after its main stock market suffered its biggest one-day fall since July 2013.

Australian shares plummet, with $34bn lost in a day

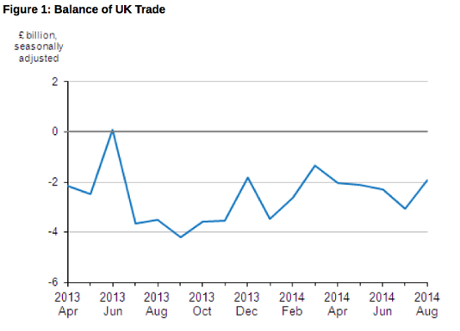

UK trade gap narrows as imports slide

This morning’s UK trade data shows that the gap between what Britain exports and imports has narrowed, for the first time since March.

That’s due to a substantial drop in imports from non-EU countries, rather than a surge in exports.

The ONS says:

Notably, this is the first time in the past five months that the trade in goods deficit has narrowed and although exports fell in August, imports fell more heavily.

Britian’s deficit on trade in goods was £9.1bn, while the surplus on trade in services was £7.2bn. That means the overall deficit was £1.9bn in August, down from £3.1bn in July.

Exports of goods fell by £0.7bn to £23.2bn, mainly due to a drop in oil exports. That’s the lowest since September 2010.

Imports decreased by £2bn to £32.3bn, which is the largest monthly decrease since July 2006. That was primarily due to a fall in ‘erratic items’, aircraft and non-monetary gold into the UK.

Rob Wood of Berenberg warns that the wider picture is still weak:

The UK trade deficit remains sizeable as strong domestic demand drags in imports while exports are being hit by still weak Eurozone growth and recently weakening trade with non-EU countries.

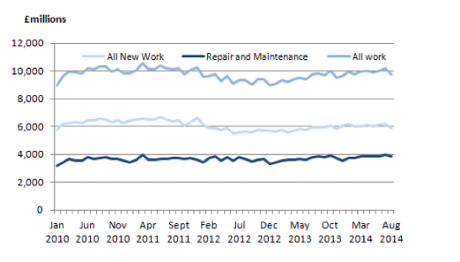

Britain’s construction sector suffered an unexpected drop in activity in August, suggesting the building trade’s recovery slowed over the summer.

The Office for National Statistics reports that construction output tumbled by 3.9% in August, compared with July.

Now, this monthly data can be volatile, especially when it covers the summer holidays.

But the ONS suggests that work fell across most areas of the construction industry, particularly housebuilding.

The ONS says:

All new work decreased by 4.8%, with all types of work except public new housing reporting decreases; infrastructure (6.5%); private commercial (5.6%); private housing (5.5%); private industrial (4.9%); and public other (2.4%).

However, the fall in private housing provided the largest contribution to the overall fall in all new work and all work.

And here’s the key chart:

Bank of England reveals Scottish contingency plans

Now this is interesting... the Bank of England has released some details of the plans it had made in case the Yes campaign had won last month’s referendum on Scottish independence.

The minutes of the last meeting of its Financial Policy Committee show that the BoE was poised to attempt to calm the market panic, had Scotland voted to become an independent country.

The Bank of England would have immediately announced plans to supply extra bank notes and pump extra liquidity into banks.

The BoE would also have immediately pledged that it remained responsible for financial stability across the whole of the UK:

In the event of a ‘yes’ vote it would issue a statement immediately reaffirming its responsibilities for financial stability, prudential regulation, banknotes and monetary policy in the entire United Kingdom, including Scotland, until legislation enacting independence came into force.

On banknotes, the minutes say that:

The Committee noted that the Bank had in place arrangements to meet potential increased demand for Bank of England notes from holders of Scottish notes.

Under current arrangements, Scottish banknotes are backed fully by their issuers’ holdings of Bank of England notes, UK coin and deposits at the Bank of England. This would have been a key public message in the event of a ‘yes’ vote.

The BoE would also held two extra, unscheduled “Long-Term Repo operations”; in which it would have accepted assets from banks in exchange for cash, to ensure liquidity levels remained as high as needed.

The minutes are online here (pdf).

Updated

Here comes the UK trade data for August..... and the top line is that the trade in goods balance fell to £9.099bn, which is the smallest deficit since April.

Exports fell by 2.3% month-on-month, while imports tumbled by 6.2%.

More to follow....

Updated

Unless the FTSE 100 stages a late rally (and it’s currently down 49 points), it will rack up its third weekly decline in a row.

Tony Cross, market analyst at Trustnet Direct, comments:

“This line about Germany slipping into recession is simply layering on another level of angst to a market that is already wary of the threat posed by the likes of Ebola in West Africa and Islamic State in the Middle East,”

It’s been quite a decline. On September 3rd, the FTSE was trading at 6,873. It’s now almost 500 points lower, at 6382.

FTSE 100 heads for one-year low after tumultuous week http://t.co/wtiMDD9gwA

— MarketWatch (@MarketWatch) October 10, 2014

Italian industrial output rose by 0.3% in August, reversing some of July’s 1.0% tumble, according to data just released.

That’s a stronger reading than France, where output was flat (see 8.01am), and much better than Germany’s 4% tumble (see Tuesday’s story).

But.... economists had expected a 0.5% increase, to help pull Italy out of its recession.

In 2008 Germany had a large stimulus whilst decrying 'crass Keynesianism'. Presume we see a quiet fiscal loosening as economy slows again?

— Duncan Weldon (@DuncanWeldon) October 10, 2014

Germany’s economy ministry has just predicted that the country’s exporters could struggle to sell their wares in the coming months.

In its new monthly report, the ministry says that the weak eurozone economy, and lacklustre global demand, will limit demand for German exports.

”In coming months we must count on exports developing in a very restrained way.... robust job market, rising incomes and stable prices will mean private consumption continues to play a positive role”.

The warning comes a day after we learned that German exports had tumbled by an alarming 5.8% in August.

Who laughs last laughs the best? LOVE that #Draghi-Schaeuble pic from yesterday's IMF conference, via @BloombergNews pic.twitter.com/ByZZKuGiW3

— Maxime Sbaihi (@MxSba) October 10, 2014

The copper price has also fallen today, hit by those growth fears.

The price of a tonne of copper dropped by 1.1% to $6,645, still above the five-month low of $6,600 set on October 2nd.

Developments in Germany.....Reuters is reporting that the Berlin government is preparing to slash its growth forecasts.

According to sources, the German government will lower its estimates for GDP expansion in both 2014 and 2015 to around 1.2%, down from 1.8% this year and 2% next year.

That follows weak factory data in August, and Germany’s fall into recession in the second quarter of this year.

Not exactly fine-tuning MT @ReutersJamie German govt to cut growth forecasts to around 1.25% for both 2014 and 2015 from 1.8% and 2.0%.

— Frederik Ducrozet (@fwred) October 10, 2014

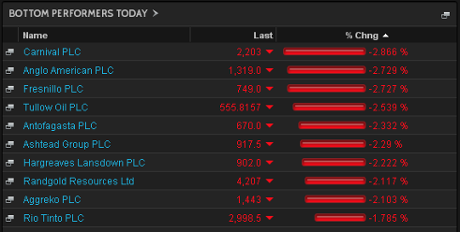

Cruise firm Carnival is the biggest faller on the FTSE 100 this morning, down 2.8%, on fears that the spread of Ebola will hit global tourism.

Most of the other big fallers are mining companies, such as Fresnillo (silver), Anglo American (copper, platinum)and Randgold (gold).

Europe’s main markets are a sea of red this morning, as this chart from the Reuters terminal shows:

The falls aren’t shocking, but it takes the FTSEurofirst index of leading European shares down to a two-month low.

FTSE 100 hits new one-year low

The FTSE 100 index of leading blue-chip shares has hit its lowest level in exactly a year, at the start of trading in Europe.

The FTSE fell as much as 51 points to 6379, a level last seen on 10 October 2013.

Other European markets are also in the red, as global growth fears (see opening post) continue to stalk the trading floors.

The German Dax fell 0.9%, France’s CAC and Italian MIB both shed 0.7% and the Spanish IBEX is down 0.6%.

Michael Hewson of CMC Markets says that:

“concerns about German and European economic growth continue to erode risk appetite, and send investors scurrying for the exits.”

Updated

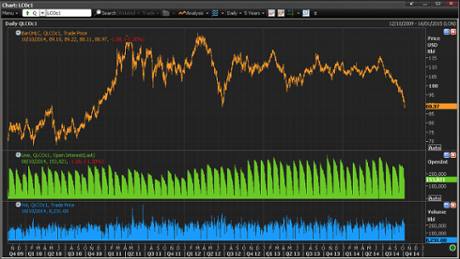

Brent crude oil price hits four year low

The oil price has fallen to its lowest level since 2010 this morning, amid predictions that energy demand will be lower than expected.

Brent crude, which hits the $90 per barrel mark last night, has fallen further today.

It hit a low of $88.11 per barrel this morning, a level not seen since November 2010.

Analysts are now speculating whether the OPEC cartel might intervene to prop prices up:

Ric Spooner, chief market analyst at CMC Markets in Sydney, says:

“I think we’ve arrived at a pivotal support level for both Brent and West Texas Intermediate. $85 is the area where OPEC has intervened in the market in the past,”

”I’m not saying they will come in this time. They need to consider the overall supply situation – it might be too expensive.”

Updated

Just in - French industrial production was stable in August, unchanged from July.

That’s better than expected -- economists had pencilled in a fall of 0.2%.

However, that’s partly due to higher energy and utility production in August (when it was unusually chilly).

The narrower measure of manufacturing output, which strips out energy, shrank by 0.2%, showing that the French economy isn’t exactly firing on all cylinders.

French Manufacturing Production (Aug) M/M -0.2% vs Exp. 0.0% (Prev. -0.3%, Rev. -0.1%)

— Fabrizio Goria (@FGoria) October 10, 2014

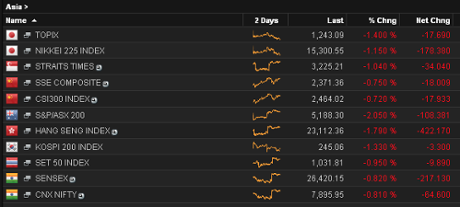

It’s been a bad day’s trading in Asia, with Japan’s Nikkei losing 1%, and the Hong Kong Hang Seng down almost 2%.

Here’s the damage:

Stan Shamu of IG says the selloff was partly due to hawkish comments from US Federal Reserve policymakers, which suggested a US interest rate rise could come in the middle of next year.

He adds:

The sell-off in the US equity market was attributed to concerns around German growth, with some also looking at growing ease about Ebola.

Opening post: Growth fears keep hitting the markets

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, the eurozone and business.

European stock markets are expected to fall sharply when trading begins today, as concerns grow over the strength of the global recovery.

Last night’s selloff on Wall Street -- the Dow shed 335 points in its biggest fall this year -- has triggered a sell-off in the Asia-Pacific region, with Australia’s main index losing 2%.

In London, the FTSE 100 is expected to hit its lowest level in over a year when trading begins.

And the oil price is also coming under pressure, reflecting concerns that global growth will be weaker than hoped, especially if the eurozone enters recession.

The rash of weak economic news from Germany this week (poor exports, factory orders and production), and the flurry of gloomy predictions from the IMF’s Annual Meeting, do seem to have spooked traders.

As Jonathan Sudaria, Capital Spreads trader, puts it:

“Bad economic data is now being viewed as bad, and the dovish signals from central banks are now being taken as a sign of weakness rather than a reason to ramp up equities,”

Here are IG’s opening calls:

-

FTSE 6362: -69 points

-

German DAX: 891,5 -90 points

-

French CAC: 4097 -44 points

-

Spanish IBEX: 10164 -109 points

-

Italian MIB: 19183 -199 points

Once again, October is turning into a volatile month in the markets.

Also coming up today....

We’ll get new industrial production data from France and Italy this morning, giving a new clue to the situation in the European economy.

The latest UK trade data, showing Britain’s balance of payments with the rest of the world, is due at 9.30am.

And a stream of central bank policymakers will be speaking in Washington at the annual meeting of the IMF and the World Bank.

And the Greek government is holding a confidence vote late tonight......

Updated