Bosses at Britain’s services firms are feeling chipper, judging by the latest purchasing managers index survey – in sharp contrast to industrialists, who were markedly downbeat in their own edition of the survey last week.

Such snapshots do not necessarily have much predictive power; but they do gauge a sector’s general mood. And it is not surprising it’s the services firms that are looking forward with optimism.

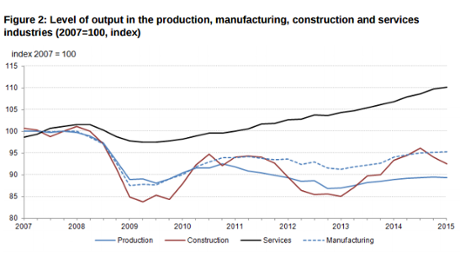

As the Office for National Statistics’ latest economic review – based on actual output data, not survey responses – points out, construction and manufacturing have never recovered from the deep recession in 2008, when output “fell off a cliff”, as it was frequently described at the time.

Not much sign of rebalancing there. Notwithstanding George Osborne’s rhetoric about creating a “march of the makers”, in reality Britain’s recovery has been a march of the hoteliers, the IT consultants and the estate agents.

That’s fine – except to the extent that the success of these parts of the economy is based on a property bubble, or credit-fuelled consumer spending.

And here, the signs are not good. Analysis by KPMG recently suggested a first-time buyer in London would need a salary of £77,000 to afford a home – hardly an indicator of a stable, sustainable market.

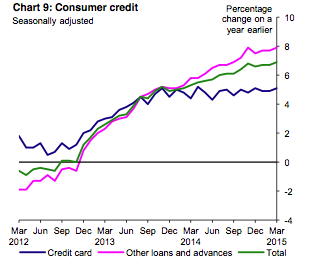

Separate official figures revealed last week that unsecured consumer credit – ie borrowing on credit cards and overdrafts – is expanding at its fastest pace since 2006, perhaps not surprising given the near-stagnation of real wages.

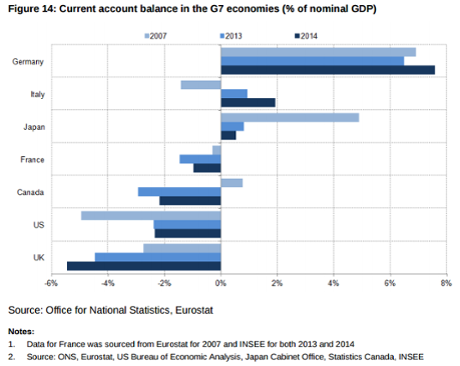

And the UK recorded the largest current account deficit in the G7 in 2014. The deterioration partly resulted from a fall in the returns UK citizens have received on their investments abroad, but it remains a good proxy for whether a nation can “pay its way in the world”, as Osborne likes to say.

Perhaps real wages will stage a steady recovery from here, underpinning the consumer spending that has been a crucial factor in generating the recovery. But if the new government embarks on a vicious new round of spending cuts, don’t bank on it. Five years on from the 2010 general election, questions remain about the viability of the UK’s underlying economic model.