With a market cap of $70.9 billion, Simon Property Group, Inc. (SPG) is a self-managed REIT that owns, develops, and operates large-scale shopping, dining, entertainment, and mixed-use destinations across North America, Asia, and Europe. Through its operating partnership and strategic stakes in companies like Taubman Realty Group and Klépierre, it manages a vast portfolio of retail properties totaling over 183 million square feet globally.

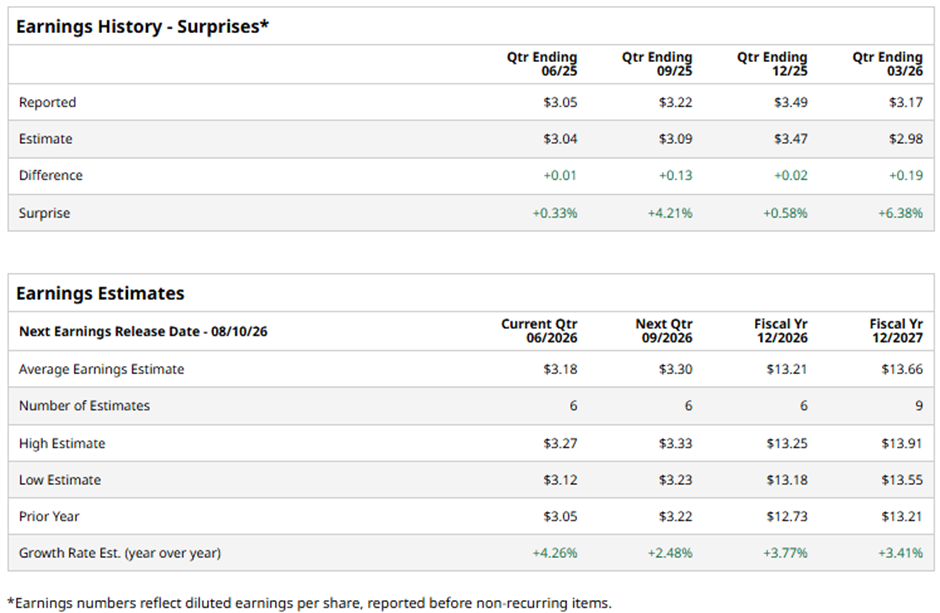

The Indianapolis, Indiana-based company is expected to release its fiscal Q2 2026 results soon. Ahead of this event, analysts project SPG to report a Real Estate FFO of $3.18 per share, a rise of 4.3% from $3.05 per share in the year-ago quarter. It holds a solid track record of consistently surpassing Wall Street's bottom-line estimates in the last four quarterly reports.

For fiscal 2026, analysts forecast Simon Property Group to report Real Estate FFO of $13.21 per share, up 3.8% from $12.73 per share in fiscal 2025.

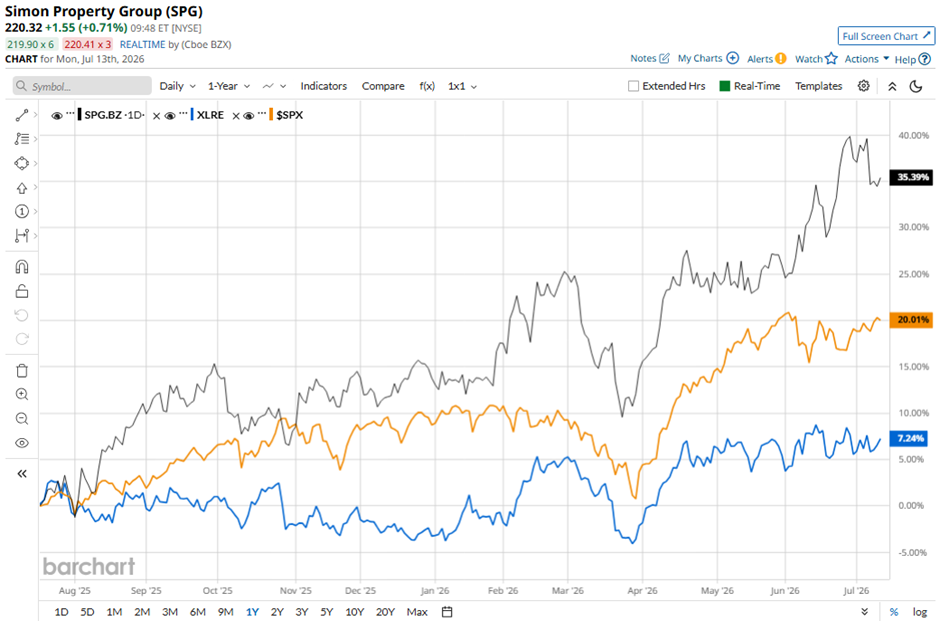

SPG stock has increased 35.5% over the past 52 weeks, outperforming the broader S&P 500 Index's ($SPX) 20.8% gain and the State Street Real Estate Select Sector SPDR ETF's (XLRE) 7.7% rise over the same time frame.

Shares of Simon Property Group rose 2.3% following its Q1 2026 results on May 11, with net income increasing to $479.6 million ($1.48 per share) from $413.7 million ($1.27 per share) a year earlier, while Real Estate FFO climbed 7.5% year-over-year to $1.21 billion, or $3.17 per share. Investors were also encouraged by solid operating metrics, including a 6.7% rise in domestic and portfolio NOI, occupancy improving to 96%, base minimum rent per square foot increasing 5.2% to $61.99, and retailer sales per square foot surging 11.8% to $819.

The stock additionally benefited from management raising its full-year 2026 Real Estate FFO guidance to $13.10 per share - $13.25 per share.

Analysts' consensus view on SPG stock is cautiously optimistic, with an overall "Moderate Buy" rating. Among 21 analysts covering the stock, seven suggest a "Strong Buy" and 14 recommend a "Hold." The average analyst price target is $222.85, indicating a potential upside of 1.1% from the current levels.