/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

While most companies that went public through the special purpose acquisition company (SPAC) route have either gone bankrupt or slipped into oblivion, SoFi (SOFI) is a rare exception. The stock recently rose to record highs and surged past $30, which is three times the SPAC IPO price.

Sell-side analysts were bearish on SoFi over the last couple of years, but the fintech giant got the best of the bears, beating the market hands down in 2023 and 2024. The story is no different this year, as the stock is up 90% for the year already.

I have been a SoFi bull for a long time and used the intermittent dips to add to my position while capitalizing on rallies to book profits. However, amid the recent rally, I sold the bulk of my shares. In this article, we’ll examine the investment case for SoFi and why I find it prudent to take profits off the table at these levels.

SoFi Is a Blend of a Bank and a Tech Company

To begin with, let’s look at SoFi’s business model. As I noted previously, SoFi has the body of a traditional bank with the soul of a fintech. Having the banking charter helps SoFi gain access to low-cost member deposits and lowers its reliance on high-cost wholesale borrowing. The company then deploys these funds in its lending business, through which it offers personal loans, home loans, and student loan refinancing.

At the same time, it has the agility of a fintech, which enables it to launch some products that traditional banks might not. SoFi gets a high (and rising) share of its revenue from non-lending-based ventures, and has pivoted to products like cryptocurrency trading that most traditional banks steer clear of.

Notably, while SoFi has its own lending business, it also generates loans for third parties. While that might sound like a perplexing business model, these are customers who don’t meet SoFi’s credit standards. It is a high-margin, low-risk business for SoFi running at annualized originations of over $9.5 billion with an annual revenue run rate in excess of half a billion dollars.

Meanwhile, one of the key reasons I invested in SoFi in the first place was its widening ecosystem with a rising member count that rose 34% YoY to 11.7 million in Q2. The member count has swelled over 10x since Q1 2020 and represents a cross-selling opportunity for SoFi, especially as it keeps on adding new products to the platform.

Why Were Markets Bearish on SoFi Stock?

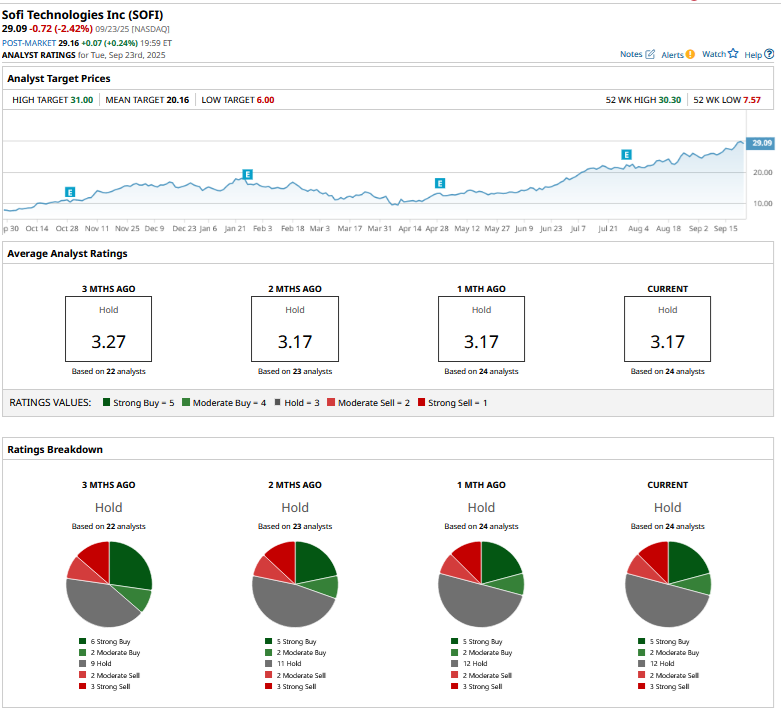

SoFi trades above its mean target price, something it has invariably done over the past few months. Its valuations were perhaps a breaking point for many analysts as its price-book value – currently at 4.79x – is too high for comfort for a legacy bank. The forward price-earnings multiple looks no cheap at 93.7x. However, I have always contended that SoFi deserves a premium to traditional banks given its business model that is increasingly pivoting to fee-based income.

As for the P/E, it should be seen in the context of the strong top-line and profit growth that SoFi brings to the table. The company expects to post earnings per share between $0.55 and $0.80 in 2026 and is optimistic about growing earnings between 20%-25% beyond 2026 as well. At the top end of SoFi’s guidance, we get a 2026 P/E of 36.3x.

Is It Time to Sell SoFi Stock?

While I remain constructive on SoFi’s long-term growth story and still maintain a small position in the company, I believe it is time to take profits for two reasons. Firstly, the broader markets are getting a bit overheated as there is a clear disconnect with the economy – something Federal Reserve Chair Jerome Powell also talked about. Since SoFi is a high beta name, it could see selling pressure if broader markets weaken.

Secondly, I now find SoFi stock overvalued, even based on the long-term earnings potential, and while we are still not in a bubble, these are not levels that I am comfortable with. To sum it up, I believe it is now time to listen to the bearish thesis on SoFi as the valuations are a bit hard to justify, even for a long-time bull like me.