/A%20SoFi%20logo%20on%20an%20office%20building%20by%20Tada%20Images%20via%20Shutterstock.jpg)

SoFi Technologies (SOFI) stock is under immense pressure on Wednesday even though the fintech posted a record $1.1 billion in revenue for Q1, its 10th consecutive quarter of profitability.

Investors are bailing on SOFI mostly because it reiterated full-year guidance for $4.65 billion in revenue instead of raising its outlook.

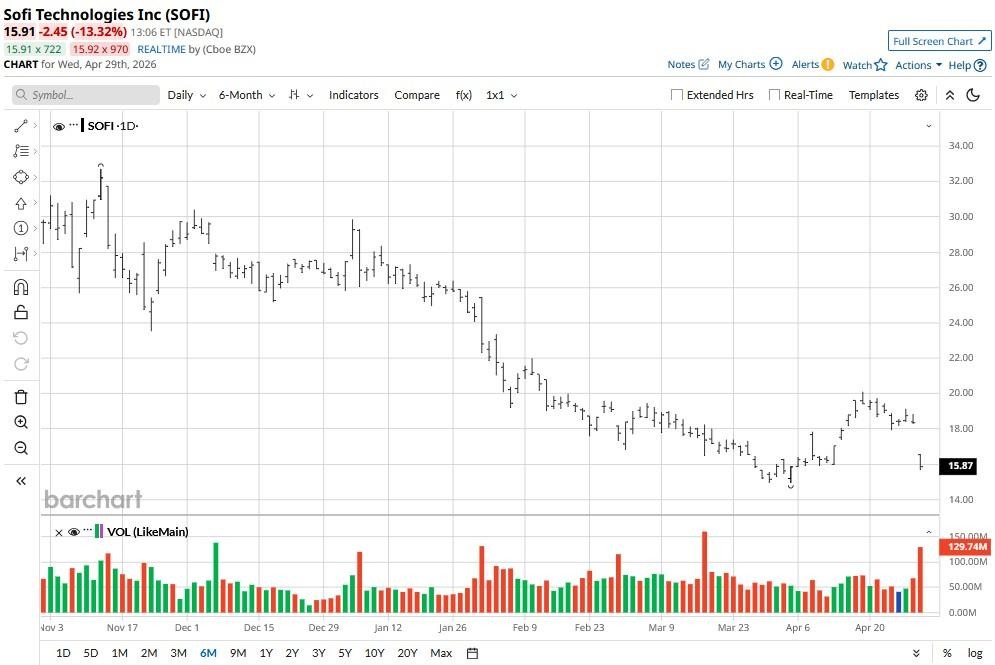

The Nasdaq-listed firm is now trading decisively below its key moving averages (MAs) with an RSI in the mid-30s indicating a little more room before the stock hits “oversold” territory.

Versus its year-to-date high, SOFI stock is now down some 45%.

Should You Invest in SOFI Stock Today?

For long-term investors, SOFI shares’ post-earnings weakness may actually be an opportunity, not a warning sign.

The market’s focus on future outlook appears somewhat misplaced as it ignores a more than 100% year-over-year increase in the firm’s Q1 net income.

More importantly, management’s commitment to non-lending segments for diversification purposes offers another strong reason to stick with SoFi Technologies.

By leaning harder into Technology Platform and Financial Services segments – which grew 24% and 41%, respectively – the company is attempting to shield its business from the volatility of the lending market and interest rate fluctuations.

CEO Sees SOFI Shares as Incorrectly Valued

SOFI stock remains attractive also because management continues to scale its “all-in-one” digital finance strategy as well.

Total members went up 35% in the first quarter to 14.7 million while total products increased 39% to 22.2 million, reinforcing the platform’s ability to deepen engagement and cross‑sell higher‑value financial products.

On the earnings call, CEO Anthony Noto said Q1 marked SoFi’s 18th straight quarter of exceeding the Rule of 40 (growth rate + profit margin > 40).

The company currently sits at 72 on that scale, highlighting the durability of its growth engine and improving efficiency of its operating model.

While the Rule of 40 is traditionally a “software metric,” Noto used it as a headline to suggest SoFi Technologies should be valued like a high-margin tech firm, not a bank.

And if market participants accept that narrative, SOFI’s forward price-to-earnings (P/E) ratio of about 31x will immediately start to look more digestible, alleviating valuation concerns that seem to be haunting it today.

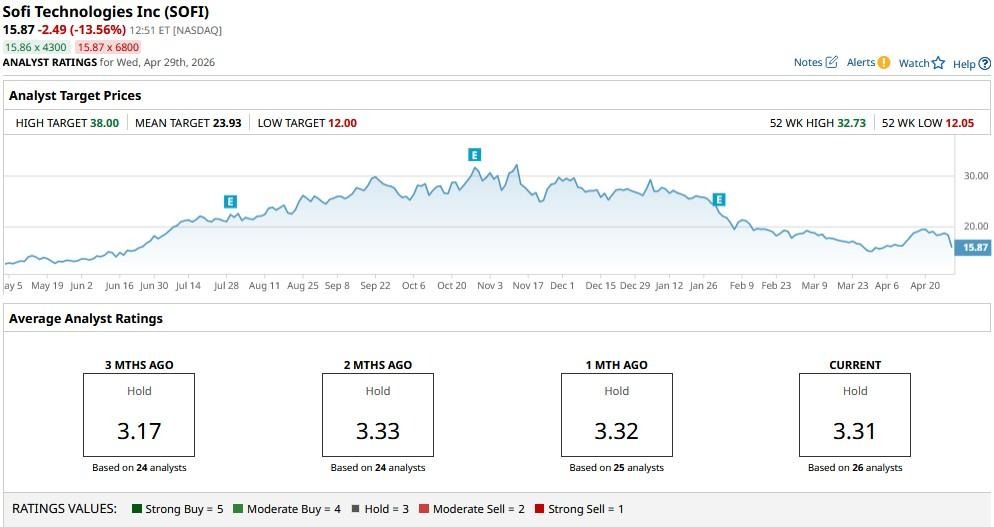

Wall Street Sees Massive Upside in SoFi Technologies

Wall Street analysts also agree that SOFI shares are undervalued at current levels, especially given the firm’s 54% incremental adjusted EBITDA margin.

The sell-off today isn’t about a “bad” quarter. SoFi Technologies is just being a victim of its own success. After 10 straight quarters of profitability and consistent beats, the market has priced in “perfection.”

When management provides a realistic, slightly conservative outlook instead of a “growth-at-all-costs” forecast, momentum traders tend to exit, that’s primarily what is weighing on the fintech stock at writing.

Sure, the consensus rating on SOFI sits at “Hold” only, but the mean target of nearly $24 indicates potential upside of a whopping 50% from here.