Mixed day for markets

Another rally across global markets looked on the cards early on, following the US Federal Reserve’s comments it would be patient over any rate rise and upbeat statements from Japan’s central bank about the country’s economic prospects. The rouble was recovering and oil was fairly steady. But while the UK held onto its gains, European markets slipped back, unsettled by Standard & Poor’s cutting its ratings on a number of Italian banks late on Thursday. The final scores showed:

- The FTSE 100 finished 79.27 points or 1.23% at 6545.27

- Germany’s Dax dipped 0.25% to 9786.96

- France’s Cac closed 0.18% lower at 4241.65

- Italy’s FTSE MIB slipped 0.4% to 18,983.83

- Spain’s Ibex ended down 0.27% at 10,363.6

- In Greece, the Athens market fell 1.41% to 862.4

- Russia’s RTS edged up 0.41% to 768.06

Meanwhile on Wall Street, the Dow Jones Industrial Average is currently down 21 points or 0.12% after two days of rises.

Back with Russia and the rouble has risen by 4% to 59.53 to the dollar, while oil is 2% higher with Brent crude at $60.63 a barrel.

On that note it’s time to close up for the evening. Thanks for all your comments, and we’ll be back on Monday.

Back with Greece, and this week’s presidential vote has been hit by bribery allegations. Helena Smith writes:

Greece’s presidential election descended into accusations of skulduggery on Friday as an opposition MP lobbed claims of attempted bribery at the government.

With just four days to go before a second round of voting in the 300-seat chamber, Pavlos Haikalis, who represents the small, rightwing Independent Greeks party, said he had been approached by a middleman offering him a multimillion-euro inducement to support the ruling coalition’s candidate for the post.

“There was a preliminary discussion which started as a joke but then became very serious,” the MP told Mega TV, adding that the interlocutor had not only offered to hand him €700,000 but to pay off his mortgage and provide advertising contracts.

The Greek chamber reconvenes next Tuesday for a second vote after earlier this week the government fell far short of amassing the necessary 200 ballots for its nominee, the former European commissioner, Stavros Dimas.

Full story here:

Greek presidential elections hit by new bribery allegations

Ukraine has seen its rating cut by Standard & Poor’s from CCC to CCC- with a negative outlook.

Why S&P downgraded Ukraine pic.twitter.com/uInZAMkTjT

— Joseph Weisenthal (@TheStalwart) December 19, 2014

Updated

Capital Economics is also worried about a Russian banking crisis:

The Russian ruble has rallied over the past 24 hours, but there are growing signs that the crisis is spreading to the banking sector. In particular, interbank interest rates have jumped to over 27%, which is well above the cost of central bank liquidity and suggests that the interbank lending market may be starting to freeze up. This has often been a precursor to banking crises and, as a result, the interbank rate will be a key indicator for investors to watch over the coming days and weeks.

Evgeny Gavrilenkov, chief economist at the investment banking arm of Russia’s largest lender Sberbank, has warned that the moves by the central bank to support the finance system could cause a “full scale banking crisis.” According to Business Insider, he said:

“If the Central Bank of Russia continues to provide refinancing in exchange for non-marketable securities that banks can generate in almost unlimited amounts, the system will gradually ramp up to full-scale banking crisis.”

He believes banks may prove unable to pay back loans from the central bank at the current 17% interest rate, and the collateral they provide may not be enough to cover any losses.

Meanwhile Russia’s lower house of parliament hastily approved a draft law on Friday that would give the banking sector a capital boost of up to 1 trillion roubles ($16.5 billion).

Updated

Greece has received an extension to its second Economic Adjustment Programme financed by the European Financial Stability Facility (EFSF). Instead of ending on 31 December 2014, the EFSF programme will now end on 28 February 2015. The EFSF said the decision followed a request from Greek finance minister Gikas Hardouvelis.

#EFSF Board of Directors decided to grant #Greece 2-month technical extension of 2nd Economic Adjustment Program until 28 Feb 2015

— ESM (@ESM_Press) December 19, 2014

Extension of the #EFSF programme and #EFSF bonds for Greece http://t.co/hZecY82VrL

— ESM (@ESM_Press) December 19, 2014

Until 28 Feb 2015 #EFSF can disburse remaining €1.8bn from program to Greece provided Greece & Troika successfully conclude review

— ESM (@ESM_Press) December 19, 2014

Also, upon Greek request, #EFSF CEO #Regling confirmed that availability period for €10.9bn of EFSF bonds is extended until 28 Feb 2015

— ESM (@ESM_Press) December 19, 2014

#Regling: extension of #EFSF facility & #EFSF bonds ensures funds remain available for #Greece until end Feb 2015

— ESM (@ESM_Press) December 19, 2014

#Regling: extension reassures markets; this time should be used to move towards follow-up arrangement for #Greece

— ESM (@ESM_Press) December 19, 2014

Regling: with extension & prospect of ESM future support, one important condition is there for full recovery & full market access for Greece

— ESM (@ESM_Press) December 19, 2014

Back with the IMF, and the fund said it had failed to reach agreement with Ukraine which would allow the country to receive its next bailout trance in January.

The fund said it had held productive discussions with officials in Ukraine this week, and would return for further talks in January. Ukraine has received two tranches under the IMF program worth $4.6bn. The IMF mission chief Nikolay Gueorguiev said:

“The mission held productive technical discussions with the new economic team of the Ukrainian government and with the National Bank of Ukraine in the context of the Fund-supported program, covering key issues facing the economy. We found that the Ukrainian authorities are preparing to move decisively on a broad and comprehensive agenda to stabilize and reform the economy, while coping with the difficult challenges that emerged in the last year. In this context, we advanced substantially our mutual understandings of policy priorities going forward.

“Discussions will continue over the coming weeks, following the mission’s departure. The mission is expected to return to Kyiv for policy discussions with the Ukrainian authorities in January 2015.”

Wall Street is still flat; the FTSE is up 0.6% while the rest of Europe is still trading lower.

Iceland repays some IMF debts early

Iceland has paid back, ahead of schedule, another chunk of the rescue package it received from the International Monetary Fund at the height of the financial crisis in 2008. The IMF announced today that the country had repaid SDR275m ($400.6m).

This amounts to a fifth of the $2.1bn borrowed by Iceland from the IMF under its standby agreement, and cuts its IMF debts to $345.1m, which are expected to be paid back in 2015-16.

On Wall Street, the Dow Jones has opened flat at 17,779.85.

Market round-up

European stock markets have fallen further, while London is still up.

The FTSE 100 index is up 0.47% at 6496.19

France’s CAC is down 0.76% at 4217.05

Germany’s Dax has lost nearly 1% to 9714.95

Spain’s Ibex has tumbled 1.15% to 10271.8

Italy’s FTSE MiB has slid 0.75% to 18,919.07.

Oil prices are holding on to their gains, with Brent crude trading 2.4% higher at $60.68 a barrel.

The rouble has strengthened 4.55% to 59 against the dollar.

Russia’s richest man, Alisher Usmanov, has responded to president Putin’s call on businessmen to bring their assets home.

Usmanov has transferred his holdings in mobile operator Megafon and iron ore producer Metalloinvest to Russian entities, after Putin used his end-of-year press conference on Thursday to ask businessmen to “de-offshore” their assets.

Oil price slide could spark M&A wave

The relentless slide in oil prices since the summer could spark a buying spree in the energy sector, analysts say. Benchmark crude oil prices have nearly halved over the past six months to $60 a barrel, and energy companies have seen their share prices tumble.

This means big oil companies flush with cash could pounce on smaller rivals. Repsol agreed to buy Canada’s Talisman Energy for $8.3bn this week, which it says is the largest international deal by a Spanish company in the last five years.

Investment bank BMO Capital Markets said:

We believe the current environment will precipitate a wave of M&A activity in the European exploration and production sector once the oil price stabilises and begins to firm.

Staying with the oil theme, Sir Ian Wood, the oil veteran who produced a review of the North Sea oil and gas industry last year, has just issued this statement. He believes that, despite some very real challenges in the next 12 months, the North Sea oil industry will find itself in better shape in 2016.

I read with real concern the comments yesterday that the UK offshore oil & gas industry was “close to collapse”. These comments are over the top for an industry which thinks and plans long term, has significant momentum from current production and from major investments made over the last two or three years, and where the operators make their investment decisions based on the anticipated price of oil in two to three years’ time.

It’s important to have a balanced perspective at this time. The UKCS does face a very difficult year to 18 months which will see a slow down in investment, the loss of some offshore production, up to 10%, and the possible loss of around 15,000 jobs within an industry which employs 375,000, although this is difficult to estimate.

It will be a tough time for the industry and the people that work in it, but we are entering a downturn from which we will recover.

There are structural reasons to believe that the price of oil should recover, probably late 2015 early 2016, and there are reasons to believe that the industry should be in better shape to attract even more investment then because of initiatives currently underway.

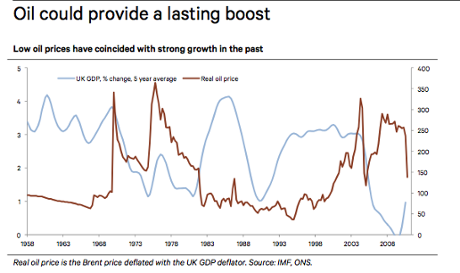

Here’s a chart from Berenberg Bank.

Updated

Analysts at Berenberg Bank believe cheap oil is a gamer changer. Holger Schmieding and Christian Schulz write:

If oil prices remain close to current levels, the western world and many emerging markets can look forward to benefiting from a big de facto tax cut. Even better, the tax cut will be paid for by Russia and the Middle East. Like every major shift in relative wealth and prices, it is disruptive. But lower energy costs will leave consumers with more money to spend on other things. The additional fall in oil prices since late November should boost demand in the US and Europe by at least 0.5% over the next six quarters or so, and possibly more.

Beyond the short-term stimulus to demand, cheaper oil can provide a more lasting boost to the world economy. Over the past 50 years or so the UK has experienced strong growth when the oil price has been low, and vice-versa. The picture is similar for other Western economies. The black gold matters – less so now than the 1970s, but nevertheless important. Slashing the price of a key input could, over time, boost productivity, allowing strong non-inflationary growth. In the jargon, oil may turn out to be a positive supply shock.

They concede that there are risks too.

Shale oil producers may be hurt, while Norway and the UK will lose out from their offshore oil sector. In general, some oil producers may have to cut spending before oil consumers spend their windfall gains. Also, markets may initially focus more on the risks for the few countries and companies that are being hurt badly than on the more widely dispersed gains for the many consumers. The big risks come from economic turmoil in Russia. Will its economy implode? Could this drive the wounded bear to lash out again with another expensive war? We need to watch the risk of a Russian crisis carefully. Most of the Western world barely blinked during the 1998 Russian crisis, but exposed Germany and Italy were hit materially for three quarters.

But, they conclude

The benefits of cheap oil far outweigh the costs. For anybody who ever argued for giving Western economies a fiscal boost, this is it. It is big, non-inflationary and paid for by somebody else.

The euro is heading towards 28-month lows against the dollar as the ECB inched closer towards quantitative easing [see 10:57].

Also, data showed direct and portfolio investments in the eurozone dropped to €53bn in October from €62.6bn the month before, contributing to the euro’s weakness. It hit $1.2253, close to the 28-month low of $1.2247 struck on 8 December.

Eurozone bond yields are expected to stay at their current low levels for the next two years, according to ratings agency Fitch.

In a report on European Government borrowing, Fitch said it expected eurozone and western European governments to borrow €1.8trn next year, in line with 2014. It added:

Gross borrowing in 2015 will be around 13% of GDP and compares favourably with a 20% borrowing requirement in the United States and 50% in Japan. At €393bn or 24% of GDP, Italy has the highest projected borrowing requirement among European countries.

Historically low yields will continue to support fiscal consolidation efforts in the medium term. Fitch expects 10-year yields in the eurozone to remain stable at the current low levels over the next two years, given weak growth and inflation dynamics and an easy ECB monetary policy. As debt stocks are refinanced, the favourable market conditions will feed into countries’ debt servicing costs, providing a helpful boost to debt dynamics. Across Europe, the average effective interest rate paid on all general government liabilities has already fallen by around two percentage points since 2005, and Fitch expects it to fall further.

From the European gross borrowing requirement for 2015, 3% is for Belgium, the only sovereign with a negative rating outlook, and 2% of the borrowing requirement is for sovereigns on positive outlook. 12 months ago, 30% of the borrowing requirement was for sovereigns on negative outlook. The outlooks of Italy (BBB+), the Netherlands (AAA), and Slovenia (BBB+) are now stable, and the outlooks for Cyprus (B) and Portugal (BB+) have been revised to positive from negative during the past year.

Updated

A downgrade of Italian banks by ratings agency Standard & Poor’s is being cited as one reason for the dip in European markets.

The downgrade came late on Thursday, and shares in Italian banks have come under pressure as a result and helped pull the Italian and other peripheral markets lower. Reuters reported:

Standards and Poor’s cut its ratings on a number of Italian banks on Thursday, including UniCredit and Intesa Sanpaolo, citing rising economic risks and a recent downgrade of Italy’s sovereign rating.

“Economic prospects in Italy are likely to be weaker than we had previously anticipated and weak overall in the next couple of years,” S&P said in a statement.

The ratings agency cut Italy’s sovereign credit rating earlier in December from BBB to BBB-, just one notch above junk, saying weak growth and poor competitiveness undermined the sustainability of its huge public debt.

The full story of the downgrades is here.

Updated

The rouble continues to rally, now up around 4% at just over 59 to the dollar.

Meanwhile oil has also edged higher, up 1.1% at $59.92.

European stock markets turn negative

While the FTSE in London is still up, trading 0.57% higher at 6503.09, European markets have turned negative as the Santa rally fizzles out. The Dax in Frankfurt is 0.14% lower, France’s CAC has slid 0.26%, Spain’s Ibex has lost 0.9% and Italy’s FTSE MiB 0.8%.

The survey comes a day after official figures showed a 1.6% jump in retail sales in November from October, with a spending splurge on Black Friday.

CBI retail sales at 27-year high

Retail sales in the UK are the strongest since 1988, according to the CBI’s latest survey. The sales volumes balance more than doubled to 61 in December from 27 in November.

ECB considers making weaker states bear more QE risk

Meanwhile, European Central Bank officials are considering ways to ensure weak countries that stand to gain most from a fresh round of money printing bear more of the risk and cost, Reuters reported.

Officials told the news agency that the ECB could ask central banks in countries such as Greece or Portugal to set aside extra money to cover potential losses from any bond-buying, reflecting the riskiness of their bonds.

This could help persuade a reluctant Germany to back plans to buy state bonds. There is currently a stand-off between the ECB and Germany’s Bundesbank over ECB plans to buy sovereign bonds to shore up the flagging euro zone economy.

The deal would have given state-owned Gazprom greater access to gas trading and storage in Germany, while BASF’s subsidiary Wintershall would have received more stakes in Siberian gas fields.

BASF said:

Due to the currently difficult political environment, BASF and Gazprom have decided not to complete the asset swap panned for the end of the year.

BASFA and Gazprom call off asset swap

In a surprise move, German chemical giant BASF and Russian energy company Gazprom have called off a major asset swap. The swap would have seen BASF subsidiary Wintershall transfer a jointly operated natural gas trading and storage business to Gazprom.

Updated

Russian Duma rushes through bill boosting bank capital

The Russian parliament has rushed through a bill that will give the banking sector a capital boost of up to 1 trillion roubles ($16.5bn), as part of efforts to shield banks from western economic sanctions.

Western sanctions over the Ukraine crisis have restricted banks’ access to international capital markets and sharply driven up their funding costs, in an economy that’s sliding back into recession.

The draft law has sailed through the state Duma and now needs to be passed by the upper house of parliament and then signed into law by president Putin.

The Treasury was pleased. An HM Treasury spokesperson said:

The week before Christmas has seen three pieces of good news confirming that the long term economic plan is working. Inflation has reached its lowest level for 12 years and regular earnings are growing in real terms for the first time since 2009. It is encouraging that today’s figures show borrowing for the month is lower than last year, due to stronger receipts.

However the effects of the great recession are still being felt in our economy and the public finances. That’s why we will continue working through the plan that is building a resilient British economy.

UK public finances improve thanks to bank fine

The state of Britain’s public finances improved sharply last month, boosted by a £1.1bn fine on banks for foreign exchange rate fixing. But income tax receipts, which had been weak until now, also improved.

The government’s deficit came in at £14.1bn in November, down 10% from November 2013, according to the Office for National Statistics. The improvement was better than City economists had expected.

However, it won’t be easy for the chancellor to meet his new, less ambitious borrowing goals. He had to admit in the recent autumn statement that he would miss his target for cutting the deficit in the current financial year and announced a new one of £91.3bn, nearly 6% higher than the old one.

Nissan-Renault suspends order on some models in Russia

Japan’s Nissan and French partner Renault have stopped taking orders for some cars in Russia and could further hike prices on others if the rouble’s slide continues, the head of the Nissan-Renault alliance Carlos Ghosn said this morning.

He told reporters at Nissan’s headquarters in Yokohama (reported by Reuters):

We have suspended taking orders. We didn’t do it overall, just on some models. We said: ‘Sorry, until we see where this situation is going we don’t take orders.’|

Nissan has already raised prices on half the models sold in Russia by 5-8%. Russia is Nissan’s fifth-largest market.

Ghosn remained confident that the Russian car market would “stabilise” but added that the plunging value of the rouble made it hard to plan ahead.

The bad news is that the market is shrinking. This is bad news for everyone. When the rouble sinks it’s a bloodbath for everybody. It’s red ink, people are losing money, all car manufacturers are losing money.

This morning the rouble is actually up, underpinned by encouraging comments from the Russian finance minister – it is currently trading at 60.32 roubles to the dollar, up 2.5% on the day.

Let’s take another look at oil prices. While steady, Brent crude is still below $60 a barrel, close to a 5 1/2 year low amid a global oil glut. Oil prices are heading for a fourth week of declines after oil cartel OPEC decided not to cut production last month.

Ken Hasegawa, commodity sales manager at Newedge Japan, told Reuters:

Following the long and steep decline in oil prices, we have seen some buying interest in recent days. But there is still a lot of selling pressure. For now there is no significant halt in production and no change to the supply and demand situation. So oil prices can still go lower.

European stock markets join in Santa rally

Nearly all European stock markets are trading higher this morning, with the FTSE 100 index in London up 0.65% at 6507.73. Germany’s Dax is 0.45% ahead at 9855.45, France’s CAC has gained 0.68% at 4278.19, and Spain’s Ibex is up 0.44% at 10,437.4. Italy’s FTSE MiB is bucking the trend with a 0.43% fall to 18,977.72.

There was some bad news for Cyprus this morning, as the International Monetary fund said it would not release a further €88m in bailout funds. More here.

Oil prices higher after wild week

Oil prices have steadied after a wild week. Brent crude, the global benchmark, is trading 15 cents higher at $59.42 a barrel while New York light crude is 35 cents ahead at $54.46 a barrel.

Rouble strengthens after finance minister comments

In Russia, the rouble has strengthened 3.4% this morning, going below 60 against the dollar for the first time since Wednesday. Russia’s finance minister Anton Siluanov confirmed his ministry had been selling foreign currency, Reuters reported. He also said the rouble would definitely firm early next year.

Meanwhile, the Russian central bank announced that it did not intervene in the markets on Wednesday. It has spent more than $80bn defending the rouble this year.

Updated

China revises size of economy

China has revised the size of its economy by $308.8bn – adding the equivalent of Malaysia’s economic output. This makes the debt of the world’s second-largest economy look smaller by comparison.

China’s GDP was 58.8 trillion yuan in 2013, according to the results of a nationwide economic census. That’s 3.4% larger than before. Malaysia’s GDP was $312bn last year.

Bloomberg noted that the change was smaller than the last time a revision was made, in 2008, reflecting more accurate counting of the fast-growing services industry.

The FTSE has opened nearly 50 points higher at 6512.11, a 0.7% rise.

As mentioned earlier, German consumers are also more confident about their economy.

The monthly survey by the GfK market research group shows consumer confidence rising to 9 points for January from 8.7 points in December. This is the highest reading since December 2006 when it hit 9.1 points.

Gfk said:

Consumers assume the economic weakness in Germany is only temporary and the domestic economy will return to the growth path in the next few months.

The Bank of Japan held off announcing fresh measures (after unveiling a big expansion of its asset-buying programme in October) and offered a more upbeat outlook, raising hopes the third-largest economy could pull out of recession soon. Japan slipped into recession in the last quarter.

Wrapping up a two-day meeting, the central bank said:

Japan’s economy has continued to recover moderately as a trend ... (while) overseas economies -- mainly advanced economies - have been recovering, albeit with a lacklustre performance still seen in part. In this situation, exports have shown signs of picking up.

Business sentiment has generally stayed at a favourable level, although some cautiousness has been observed.

Private consumption remains “resilient” while real-estate investment has “started to bottom out”, the bank said..

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, the eurozone and business.

The Santa rally is here. The Bank of Japan has struck a more optimistic view of the economy which bodes well for global growth, fuelling a rally in Asian stocks. Japan’s Nikkei gained 2.4% while Hong Kong’s Hang Seng rose 1.3%, following big gains on Wall Street yesterday. The Dow Jones scored a 421 point gain as concerns over a Fed interest rate hike and lower oil prices eased.

Over here, things are also looking more rosy, with German consumer sentiment hitting an eight-year high. European markets are expected to open higher.

Equity market calls from Jasper Lawler at CMC Markets :

FTSE100 is expected to open 77 points higher at 6,543

DAX is expected to open 108 points higher at 9,919

CAC40 is expected to open 56 points higher at 4,305

Updated