Sandisk (SNDK) stock has skyrocketed 692.8% year-to-date (YTD). Such a significant rally raises concerns about valuations. However, the SNDK’s accelerating earnings trajectory, led by exceptional demand for high-performance storage solutions and higher pricing, suggests the stock may still offer meaningful upside despite its extraordinary run.

At the same time, Sandisk is shifting its focus toward higher-value opportunities and moving away from legacy upsell strategies in favor of new business models (NBMs). These initiatives could strengthen revenue growth, expand margins, and support durable growth.

Sandisk: AI Demand Is Fueling Explosive Growth

The flash storage specialist is benefiting from one of the strongest demand environments the memory industry has seen in years. As companies invest billions in artificial intelligence (AI) infrastructure, the need for high-performance NAND storage is rising across data centers, edge computing systems, and consumer devices.

At the same time, industry supply constraints have strengthened pricing, creating a powerful combination for memory producers.

The positive impact of these dynamics is reflected in Sandisk's solid financial results. Notably, strong demand and supply constraints are translating into higher pricing, improving profitability, and substantial revenue growth for Sandisk.

During its most recently reported quarter, Sandisk’s revenue surged 251% year-over-year (YOY), driven primarily by a 248% increase in average selling prices (ASP) per gigabyte.

The data center segment has emerged as the key growth engine. Revenue from this business climbed 645% YOY, supported by a 186% increase in ASP and a 160% rise in exabytes sold. This reflects growing demand for storage solutions that support AI training and inference workloads.

Other segments also delivered impressive results. Edge revenue rose 295% as pricing gains more than offset slightly lower shipment volumes, while consumer revenue increased 44% despite a decline in exabytes sold. Across the portfolio, stronger pricing conditions continue to outweigh volume fluctuations.

The benefits are evident in profitability. SNDK’s adjusted gross margin was 78.4% in Q3, up from 51.1% in the prior quarter. Management expects favorable industry conditions to continue through 2026 and beyond, creating a supportive backdrop for earnings growth.

Sandisk’s Strategic Shift Toward More Predictable Revenue

While favorable memory pricing is helping drive near-term results, Sandisk is also taking steps to create a more stable and predictable business model. Sandisk has introduced NBMs, which are multi-year supply agreements designed to reduce revenue volatility and improve long-term visibility. Historically, memory manufacturers have been heavily exposed to spot-market pricing, making earnings highly cyclical and difficult to forecast.

The new approach aims to change that dynamic. By securing long-term customer commitments, Sandisk gains greater confidence in future demand levels, enabling more efficient production planning and reducing the risk of underutilized manufacturing capacity during industry downturns.

During the third quarter, Sandisk signed three contracts that collectively include minimum revenue commitments of approximately $42 billion and are supported by financial guarantees. Some of these agreements extend for up to five years and contain provisions that allow revenue contributions to increase as customer commitments expand over time.

The structure of these contracts is equally important. By combining fixed and variable pricing components, Sandisk can participate in upside scenarios when memory prices rise while maintaining some protection during weaker market conditions.

Is SNDK Stock Still Cheap?

Despite the stock's enormous rally, valuation remains surprisingly reasonable relative to its expected earnings growth.

Sandisk currently trades at 25.72 times forward price-to-earnings. While that multiple is not cheap, it appears attractive relative to analysts' forecast of nearly 181% EPS growth in fiscal 2027, following massive growth of 3,496% in fiscal 2026.

The Bottom Line

Sandisk's solid stock performance has raised questions about valuation. However, the company's growth story appears far from over. AI-driven storage demand continues to accelerate, pricing conditions remain favorable, margins are expanding, and long-term supply agreements are creating greater earnings visibility.

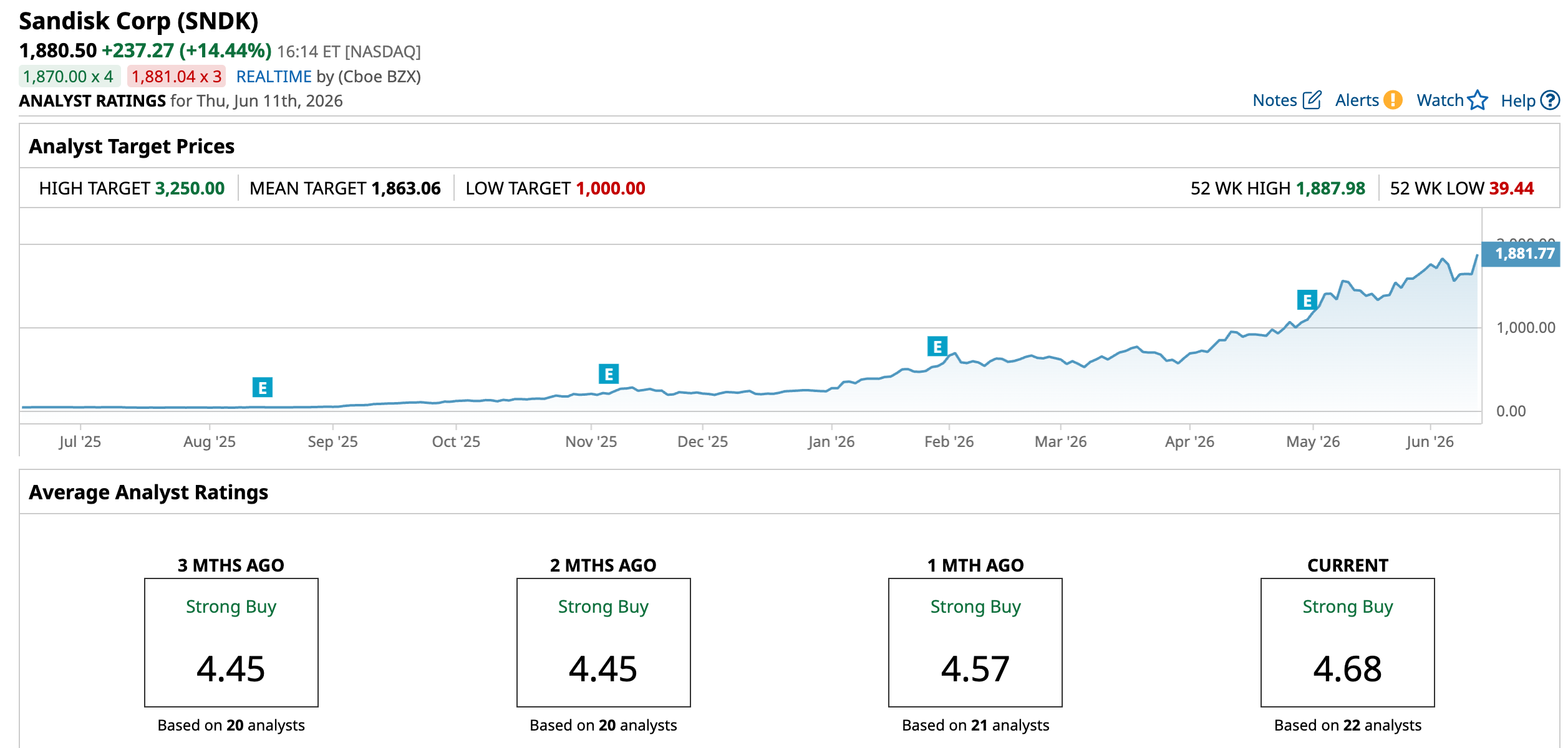

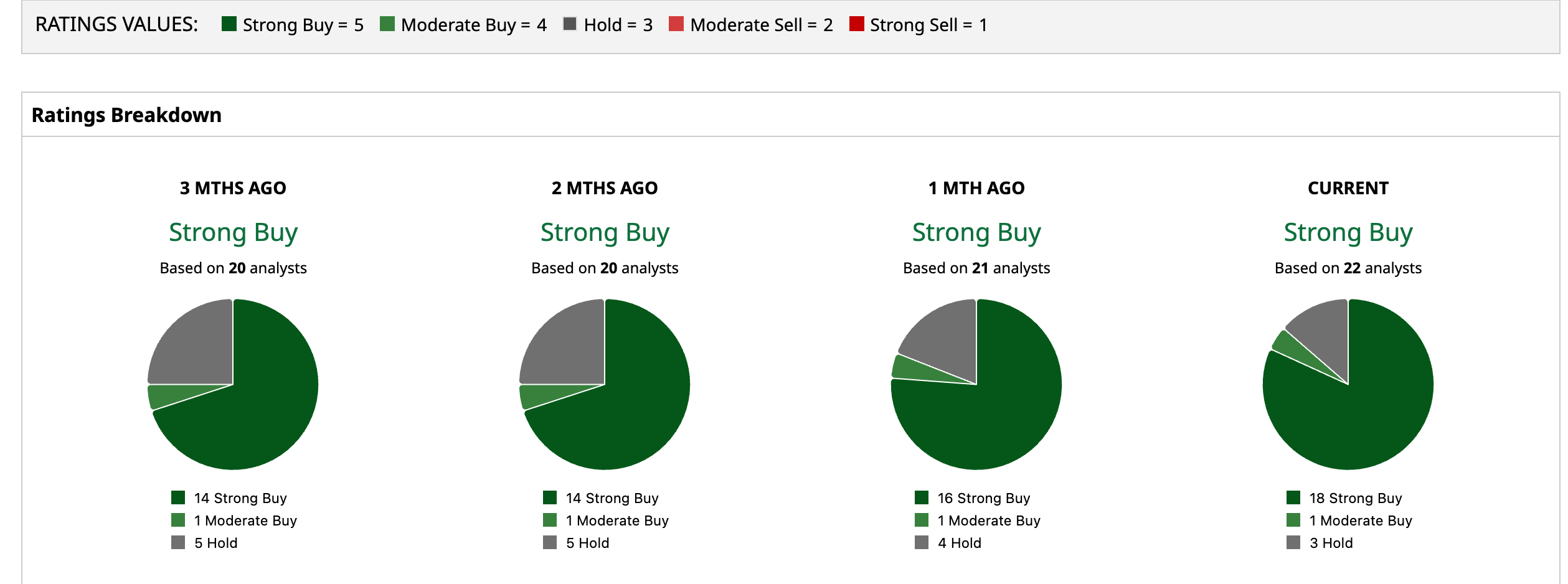

These factors help explain why SNDK stock is still a compelling growth opportunity. Wall Street is bullish, with a majority of analysts maintaining a "Strong Buy" rating on Sandisk.