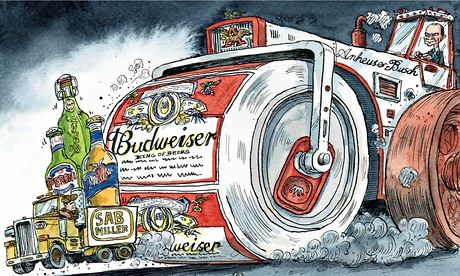

There have been few laughs in Anheuser-Busch InBev’s £65bn pursuit of SABMiller but the bidder’s chief executive, Carlos Brito, at least offered this zinger: the creation of “Megabrew”, as the proposed combination has been dubbed, would lead to “more choice for consumers”. This seemed a highly unlikely proposition, since AB InBev, owner of Budweiser, Stella Artois and Beck’s, is a famously ruthless cost-cutter that doesn’t mess about with small brands and breweries. So Brito tried to explain.

“As an example, since our combination with Anheuser-Busch, we have successfully grown Budweiser globally, with international sales now accounting for over half of total volume,” he said. In other words, “more choice” means more Budweiser in more places around the world. This is a depressing vision. Americans know that Budweiser is as bland as mass-market lagers get: they are drinking it less and turning to craft beers.

What we might call the Coca-Cola-isation of the international beer market is under way and Megabrew, if it happens, would start life with a global share of 30%, or almost one pint in every three. A few local regulators (in the US and China) would force a few disposals, but the new empire could still hope to have top or second slot in 24 of the world’s 30 biggest beer-drinking countries. More choice? Not a chance, whatever Brito adds vaguely about AB InBev using its “innovation capabilities” to introduce “exciting new products”.

How about cheaper beer then? Don’t hold your breath. Brito didn’t even mention pricing in his consumer pitch. AB InBev would be ramping up its borrowings by $60bn to buy SAB and the financial demands mean the priority would be cutting jobs, not prices. SAB’s estimate, issued on Friday, that it could make its operations more efficient to the tune of $1.05bn by 2020 would be out of date on the day AB InBev took control. The new owner would seek at least twice that sum across its enlarged business.

Unfortunately, there is nothing standing in the way of this joyless takeover except SAB’s own shareholders. Altria, owner of Marlboro cigarettes, owns 27% of SAB and has already declared itself in favour. SAB’s board, minus Altria, rejected last week’s £42.15-a-share offer and managed to retain the support of the Santo Domingo family from Colombia, with a 14% stake, plus Kulczyk from Poland (3%), South Africa’s Public Investment Corporation (3%) and the UK’s Aberdeen Asset Management (2.7%). But in the next few days – probably on Monday – AB InBev will put its real bid on the table. If it is £45-a-share or more, the pressure on SAB chairman Jan du Plessis to agree terms will be intense. If the Santo Domingos wish to accept the improved price, SAB’s resistance will start to crumble and the battle will be as good as over.

That’s the way of open markets, of course. Almost all quoted companies are for sale by their shareholders and beer is nobody’s idea of a strategic industry; even South Africa, where SAB has its roots, would struggle to mount a public-interest defence.

Yet this entire adventure embodies the reasons why the debt-fuelled takeover culture, breeding corporate goliaths, eats away at consumers’ trust in big business. SAB is a company that has served its shareholders superbly: in its 16 years on the London market it has been a superstar of the FTSE 100. It has been South Africa’s best corporate export. In independent form, SAB would continue to flourish because it can look forward to decades of growth in Africa. It deserves a better fate than being thrown under the Budweiser steamroller for the sake of a few more quid on the bid price.

The Santo Domingos – let’s hope – could yet decide to say no at almost any price. Sadly, however, it’s odds-on that AB InBev will put up the extra cash and blandness will prevail. Drink responsibly, drink something else.

M&A madness may be about to hit the buffers

It has been a year when superlatives have been wheeled out in the mergers and acquisitions world. Shell’s takeover of BG, announced in April was, at £47bn, the largest deal in a decade. Anheuser Busch InBev’s public – but so far unrequited – courtship of brewing rival SABMiller would be the largest-ever tie-up in the brewing business.

Deal-makers – already the smartest dressed and smoothest talkers in the City – have already announced more activity this year than they did for the whole of 2014. Indeed they have never announced so valuable a string of mergers by this point in any year. According to Thomson Reuters the will-they-won’t-they brewing tussle brings the total size of deals announced so far to $3.38 trillion (£2.2tn), a 35% increase compared to a year ago and the strongest year-to-date total for worldwide M&A since records began in 1980.

Why this flurry of mergers? Interest rates are low, so it is cheap to borrow to finance deals. The environment for growth in the business world is also tough, so buying a rival from which costs can be axed is an easier way to generate returns.

Can it go on? The big investment banks in the US, Goldman Sachs and its rivals, start to report their third-quarter results this week. There may well be updates on their “pipeline”; that is, the number of companies they know are thinking about tie-ups but yet to go public with their intentions. They may be able to say that it looks strong for the next quarter or so (and it is a brave corporate financier who tells his bosses that his pipeline is running dry).

But in reality the M&A race may soon start to lose its legs. An interest-rate rise anticipated on both sides of the Atlantic will start to make it harder to finance deals. This has also been a year in which deals have failed to materialise: RSA is still on the shelf after Zurich Insurance failed to table a formal offer and, to be clear, AB InBev has not yet managed to catch SABMiller. For now, though, the corporate financiers look to be on track for bumper Christmas-time bonuses.

We need brickies, not bonuses

There are many explanations offered by housebuilders for why they’re not building enough homes – planning, nimbies, not enough bricks, and not enough brickies. An unexpected 4.3% fall in construction output in August, revealed on Friday, was blamed partly on skills shortages. Away from the building site, housebuilding bosses are trousering an unprecedented cash bonanza. Five executives at Berkeley recently shared £42m, with chief executive Tony Pidgley getting £23m. A new scheme for the top five bosses could pay out £500m in the next five years.

Jeff Fairburn, the boss at Persimmon – where 40% of buyers use help-to-buy subsidies – also has a bonus scheme that could pay out £100m by 2021.

Given the cross-party agreement to build more homes, running a housebuilder looks like a licence to print money for the foreseeable future. Couldn’t more of that cash be invested in training brickies, chippies and plasterers, and a bit less on bosses’ pay?