/Royal%20Caribbean%20Group%20sign%20by-%20JHVEPhoto%20via%20iStock.jpg)

Miami-based Royal Caribbean Cruises Ltd. (RCL) operates as a global cruise vacation company. With a market cap of $84.5 billion, the company operates cruise brands like Royal Caribbean International, Celebrity Cruises, Azamara, and Silversea Cruises and holds interests in TUI Cruises, Pullmantur, and SkySea Cruises.

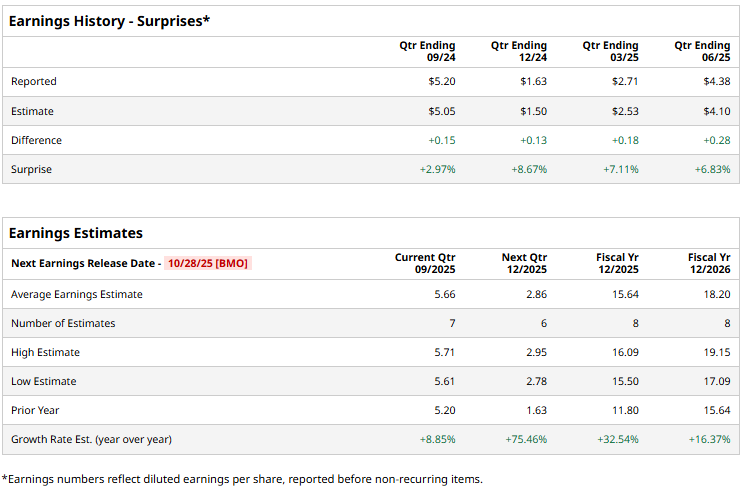

The Cruise operator is set to announce its third-quarter results before the market opens on Tuesday, Oct. 28. Ahead of the event, analysts expect Royal Caribbean Cruises to report an adjusted profit of $5.66 per share, up 8.9% from $5.20 per share reported in the year-ago quarter. Moreover, the company has a solid earnings surprise history. It has surpassed the Street’s bottom-line projections in each of the past four quarters.

For the full fiscal 2025, RCL is expected to deliver an adjusted EPS of $15.64, up a staggering 32.5% from $11.80 reported in 2024. While in fiscal 2026, its earnings are expected to grow 16.4% year-over-year to $18.20 per share.

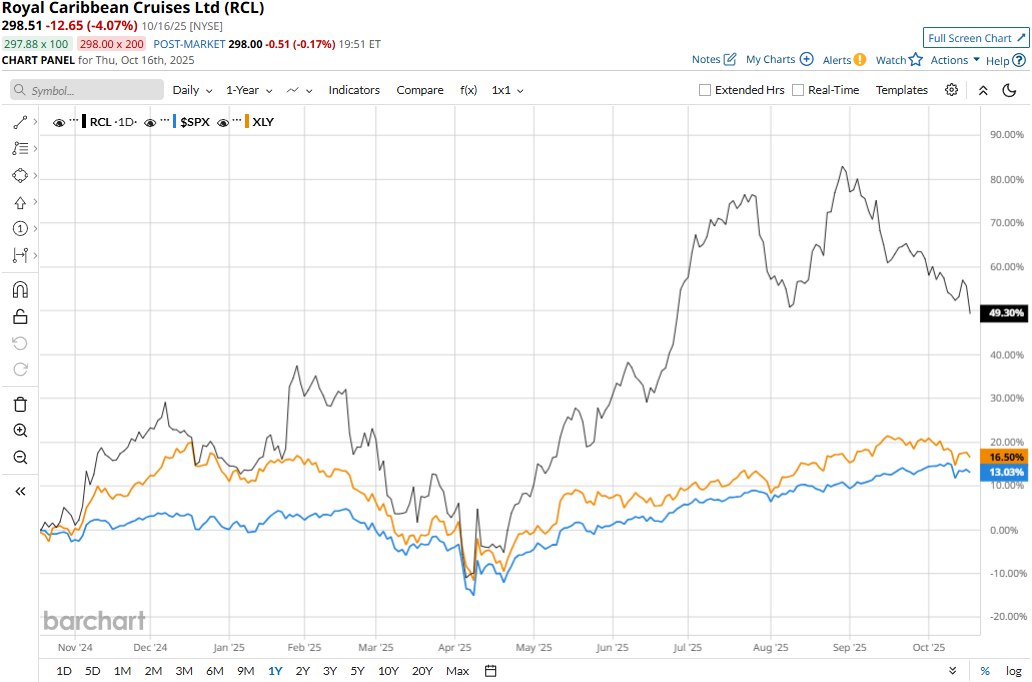

RCL stock prices have soared 48% over the past 52 weeks, notably outperforming the Consumer Discretionary Select Sector SPDR Fund’s (XLY) 17% gains and the S&P 500 Index’s ($SPX) 13.5% gains during the same time frame.

Royal Caribbean Cruises’ stock prices dropped more than 5% in the trading session following the release of its mixed Q2 results on Jul. 29. Driven by continued growth in ticket sales and onboard and other revenues, the company’s overall topline for the quarter grew by a solid 10.4% year-over-year to $4.5 billion. However, the figure missed the Street’s expectations by a tiny margin. Given RCL's outperformance over the past year and its high beta, this triggered profit booking among investors.

Nonetheless, its overall performance remained more than impressive. RCL’s adjusted net income increased 36.3% year-over-year to $1.2 billion, and its adjusted EPS of $4.38 exceeded the consensus estimates by 6.8%. Further, its operating cash flows grew 16.3% year-over-year to $3.4 billion.

Analysts maintain an optimistic outlook on RCL. The stock holds a consensus “Moderate Buy” rating overall. Of the 24 analysts covering the stock, opinions include 16 “Strong Buys,” one “Moderate Buy,” and seven “Holds.” Its mean price target of $358.69 suggests a 20.2% upside potential from current price levels.