There's something uncanny about today's job market: corporate profits are surging, tech companies are delivering blockbuster earnings, and yet tens of thousands of high-skilled jobs are quietly disappearing—replaced not by cheaper labor, but rather artificial intelligence.

Just last week, Amazon.com Inc. (NASDAQ:AMZN) announced 30,000 layoffs, explicitly citing artificial intelligence as the main driver. Meta Platforms Inc. (NASDAQ:META) and Salesforce Inc. (NASDAQ:CRM) are following suit.

These cuts, however, don't come with the usual backdrop of slowing revenue or shrinking margins. Quite the opposite—tech giants are enjoying robust earnings growth, making the timing of these layoffs all the more striking.

Read also: Amazon To Cut Up To 30,000 Jobs, Largest Layoff In Company History

Is AI Fueling A Productivity Miracle—Or A Displacement Shock?

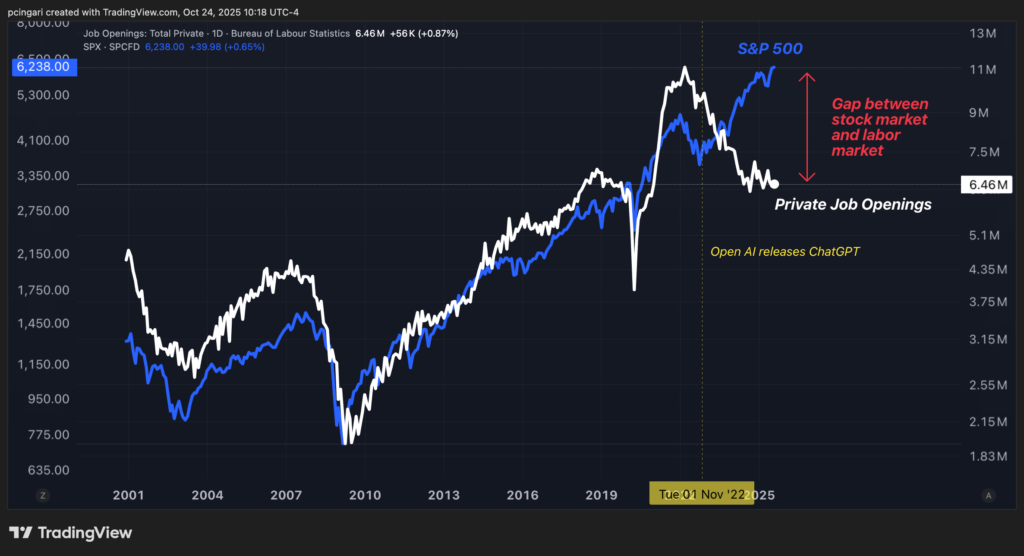

Take a look at the chart below, which tracks the S&P 500 alongside private-sector job openings. For most of the past 25 years, these two metrics moved closely together—more job openings typically meant stronger economic confidence, and the stock market reflected that optimism.

But that historical relationship began to break down after OpenAI launched ChatGPT in November 2022. Since then, a striking divergence has emerged.

Private job openings have fallen sharply—from a peak of 11 million in 2021 to just 6.46 million by mid-2025—signaling weakening labor demand. Yet the stock market has continued climbing to record highs, fueled by robust earnings growth and rising productivity, particularly in tech.

It's become the latest chapter in the Wall Street versus Main Street divide—profits and valuations are soaring, even as job creation lags far behind.

According to Chen Zhao, chief global strategist at Alpine Macro, this decoupling of profits from payrolls isn't just a quirk of the tech sector anymore.

"The combination of booming corporate profits and meager job growth is no longer confined to the tech sector—it has quickly become an economy-wide phenomenon," Zhao said in a report on Monday.

Since 2020, U.S. labor productivity has accelerated to levels more than twice the average of the 2010s, Alpine Macro reports. While some of that growth could stem from post-pandemic restructuring or leaner operations, Zhao highlights there's a deeper explanation.

As machines and algorithms take on more of the cognitive and repetitive workload once handled by humans, companies can do more with less. That, in turn, boosts earnings per employee—even as the number of employees shrinks.

Where Did The Workers Go?

Despite resilient GDP growth, total private-sector employment remains 5% below its pre-pandemic trend. Zhao argues that this points to a structural, not cyclical, shift in the U.S. labor market.

A shrinking workforce explains some of that gap. The labor force participation rate has never fully recovered from the COVID-19 shock and has fallen further since early 2024.

Mass retirements among baby boomers are also a big factor. The Trump administration's stepped-up deportation campaign adds more pressure: with a target of 3,000 undocumented immigrants deported per day, the U.S. could lose 1.5 million workers—about 1% of its labor force—within a year.

With slower labor force growth, the U.S. now requires far fewer new jobs to maintain its unemployment rate. That's one reason why the jobless rate has only ticked up to 4.3%, despite weakening job creation.

Strong Profits, Low Inflation—Too Good to Last?

Here's where it gets tricky for the Federal Reserve. Rising productivity allows companies to absorb higher costs without raising prices, which is inherently disinflationary. With wages rising 3.9% and productivity at 2%, implied inflation barely hits 2%.

If productivity jumps to 2.5%, Alpine Macro estimates core inflation could fall below the Fed's target—particularly as rent inflation, a key component of core Personal Consumption Expenditures (PCE), drops sharply.

Zhao said investors should brace for the Fed to stay cautious on rate cuts. "A jobless expansion allows a temporary decoupling between a softening labor market and solid GDP growth," he said, adding that strong output with weak hiring could delay further easing.

A Bull Market Built On Efficiency

This time around, the stock rally isn't built on hype alone. It's being fueled by real profit growth, something Alpine Macro contrasts with the late-1990s tech boom, when equity valuations surged ahead of earnings.

Still, Zhao warns that the Fed's path forward remains complicated. While inflation may fall over time, the near-term picture—with core inflation still close to 3%—limits the central bank's maneuvering room.

For now, Alpine Macro is betting that the Fed will deliver fewer near-term cuts than markets expect.

In the long run, however, the picture may flip. If inflation falls below target and job growth remains sluggish, the Fed could be forced into more aggressive easing.

"Ultimately," Zhao said, "a jobless boom means the Fed will be less dovish now—but more dovish later."

Read now:

Photo: Shutterstock