AI companies (even those outside the tech sector) have been the recipients of substantial investor attention in recent years, but industrials are among the top-performing sectors so far in 2026. After a period of navigating technology and finding potential applications, companies behind factory automation may be poised for a breakout as manufacturers move to implement AI tools in new ways. Those firms in both the industrial and tech sectors with an interest in machine vision, robotics, and other types of automation could benefit from a new investment cycle.

With PwC anticipating that industrial manufacturers will more than double their usage of automation by 2030, now may be a good opportunity to consider the standout automation names below. An added benefit for investors is that these companies may reap the rewards of AI while providing some essential diversification away from the most popular names in that industry.

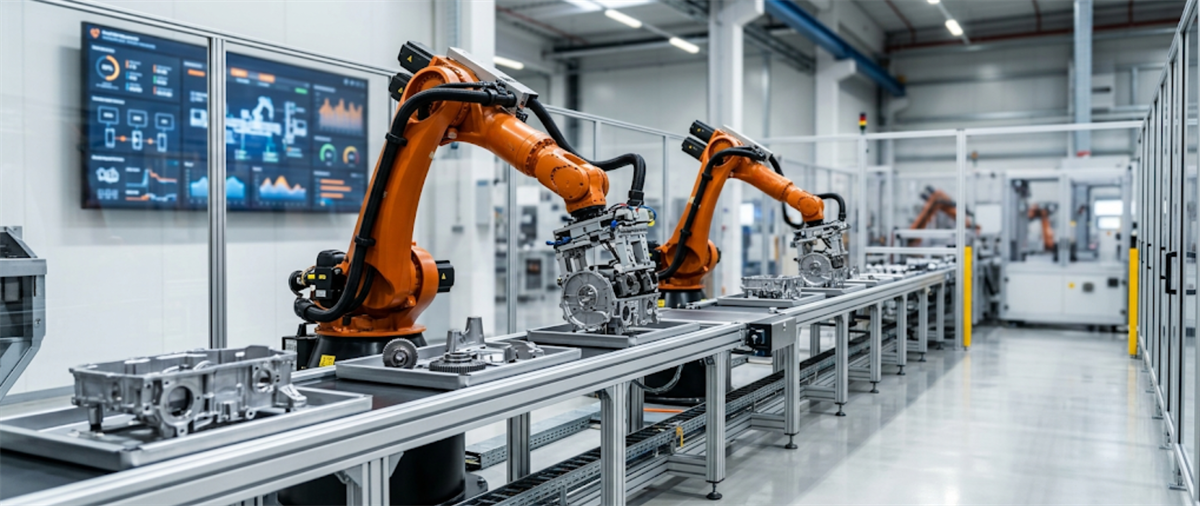

Rockwell's Warehouse Automation Business Drives Multiple Growth Areas

At more than $51 billion in market capitalization, Rockwell Automation (NYSE: ROK) remains among the largest industrial automation companies in the world. The firm's presence in Europe may give it an advantage as the region shifts its manufacturing toward military applications and as global demand for AI, data center, and warehouse automation continues to grow.

In the latest quarter, Rockwell posted a 9% year over year (YOY) improvement to organic sales, ahead of analyst expectations, alongside more than 30% YOY gains to adjusted earnings per share (EPS). At the same time, enterprise operating margin was up thanks to strong volumes, prices, and productivity, among other factors. The company raised its fiscal year guidance on the strength of improving demand for warehouse automation, but this is only one of the areas of Rockwell's large, diversified business that is thriving.

In the near term, investors may still watch for margin pressures from inflationary pressures on input costs and potential tariff-related volatility. Still, these challenges were not enough to stop the company from announcing in June 2026 an additional $1 billion authorization to repurchase shares, on top of a quarterly dividend of $1.38. Analysts remain divided based on 10 Buy ratings and 11 Holds.

A Leader in Machine Vision Consolidating Its Position With New Tools

Often overlooked by investors, machine vision is among the fastest-growing categories in automation. Besides applications in self-driving vehicles, this technology has significant room for adoption across electronics, logistics, semiconductor, and other manufacturing processes requiring precision work. Cognex Corp. (NASDAQ: CGNX) is one of the leading firms in this growing industry.

Despite shares of CGNX already rising by close to 80% year to date (YTD), analysts see another 13% in possible upside based on a consensus price target above $72 per share. Three-quarters of the 16 ratings of CGNX are Buys, with the remaining four being Holds.

Thanks to the success of Cognex's OneVision cloud platform—recently supplemented by new embedded AI vision systems in the In-Sight software suite—the company is experiencing massive revenue momentum. Sales climbed by 24% YOY in the most recent quarter, with adjusted EBITDA margin surging to 26.9% and adjusted EPS more than doubling over the same period.

For Cognex, cost management remains a critical factor, but the firm says it is on track to reduce annualized net costs by up to $40 million by the end of the year, all while strategically repurchasing shares when possible as well. While it's true that the company's price-to-earnings (P/E) ratio of 76.1 means it is not cheap, there seem to be plenty of reasons to expect rapid growth to continue.

A Slump for Teradyne Could Be an Investment Opportunity

Teradyne Inc. (NASDAQ: TER) is best known for its semiconductor testing, but its robotics division is crucial to the development of automation technology. Shares of TER are still up by well over two-thirds YTD, despite a slump since its last earnings report. This may end up being an opportunity in disguise, as the company posted strong Q1 2026 results—including revenue increases of 87% YOY to $1.3 billion and a massive surge in earnings per share (EPS) to $2.56, both well ahead of analyst expectations—but management shared cautious guidance.

For investors, a crucial factor for Teradyne is whether the company will successfully differentiate its business enough so that it is not critically reliant on just a few hyperscaler customers, which tends to make results lumpy and leaves the firm susceptible to industry-wide risks. Robotics could be a way to do that, but investors may want to see signs of further growth or the company's leaning into that segment to confirm.

Nonetheless, most analysts view TER shares favorably: it has 13 Buy ratings and just three Holds, as well as a predicted 14% in potential upside.

The article "Prepare for the Next Wave of Factory Automation With These 3 Standout Names" first appeared on MarketBeat.