Amid a difficult economic environment, investors are looking for more than just strong financial performances: they're seeking a confident, credible narrative moving forward. Software specialist Atlassian Corp (NASDAQ:TEAM) delivered on the former but couldn't muster enough on the latter, sending TEAM stock tumbling. However, with a rare quantitative signal having just flashed, TEAM could be an intriguing wager for those buying volatility.

To recap, Atlassian beat its top-and-bottom line targets for its fiscal fourth quarter (released Aug. 7), generating revenue of $1.38 billion and posting earnings per share of 98 cents. In contrast, Wall Street analysts expected the company to deliver $1.36 billion and 86 cents per share, respectively. However, management guided first-quarter revenue to land between $1.395 billion to $1.403 billion — and that seems to be where the wheels fell off.

The problem? Analysts expected Atlassian to post revenue of $1.413 billion. Subsequently, TEAM stock fell sharply. Despite the security being one of today's biggest movers, in the trailing month, it's down about 15%.

Still, with the red ink, TEAM stock has printed a rare quant signal. Up to Tuesday's close, the market voted to buy TEAM six times and sell four times. Despite accumulative sessions outnumbering distributive, the stock incurred a downward trajectory. For easy classification, this sequence can be labeled 6-4-D. This signal has only appeared 12 times on a rolling basis since January 2019.

To be clear, with Wednesday's pop, TEAM stock is printing a 7-3-D sequence. Such a pattern, though, has never materialized in the past six years, so making statistical inferences (outside of advanced Bayesian inferences) is impossible. Therefore, the analysis must hinge on the 6-4-D sequence.

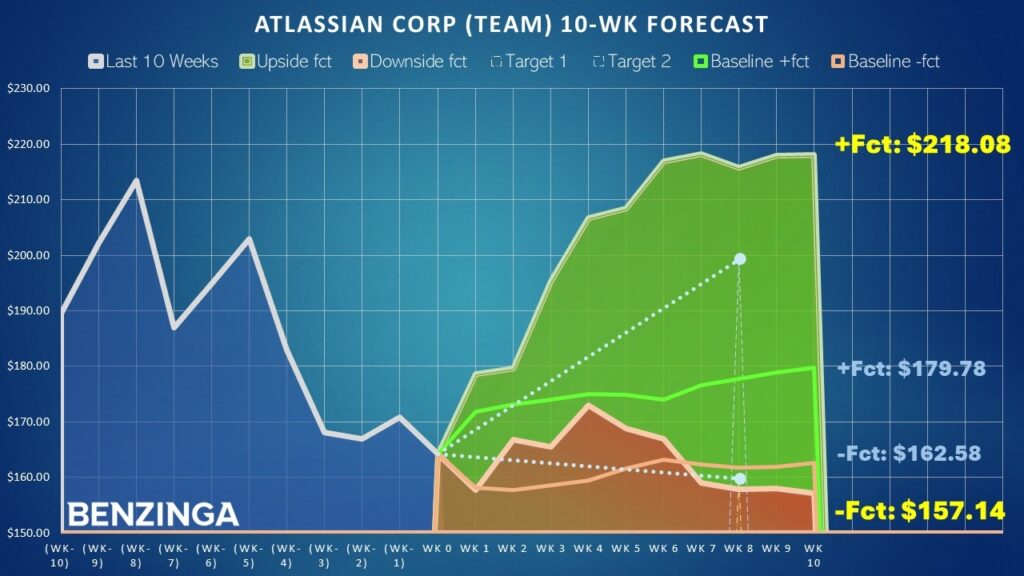

What's fascinating about the quant signal in question is its expected drift over the next 10 weeks: on a projected median basis from past analogs, TEAM stock could potentially hit around $218.08 or fall to around $157.14. Normally, the expected drift (assuming no particular quant signal) would imply a range between approximately $162.58 to $179.78.

With such a wide range of outcomes, a directional thesis would utterly lack statistical conviction. However, there is a solution available for advanced options traders.

Why Buying Volatility For TEAM Stock Makes Perfect Theoretical Sense

For optimistic traders, a multi-leg strategy known as the bull call spread is appealing because of the discounted long position. The geometry involves buying a call and simultaneously selling a call at a higher strike price, with the proceeds of the short (sold) call partially offsetting the debit paid of the long (bought) call.

Of course, this structure caps the maximum upside potential to the short (higher) strike price. Therefore, any movement above this point won't result in a greater reward. However, many traders find that this is an acceptable tradeoff because the downside is capped by the acquisition of the lower-strike long call. Also, the discounted debit paid means that the breakeven price is lower (and thus probabilistically higher to attain).

For pessimists, the bear put spread works the same way but in the inverted direction. Here, the trader buys a put and simultaneously sells a put at a lower price. The premium received from the short put partially offsets the debit paid for the long put. Again, the idea is that the bearish position is discounted at the expense of a capped profit at the short put strike.

As a quick note, buying a put (or a bear put spread) isn't technically a short position. Instead, the trader is long a bearish position. A true short position will be credit-based because the trader is a net seller, not a net buyer.

Going back to TEAM stock, the conditional drift is expected to be massive at the end of week 10 (roughly 39%). In contrast, the normal aggregate drift is less than 11%. Granting the presupposition that the aforementioned quant signal is reliable, the wide delta between the conditional and aggregate drift suggests that there's a mispricing somewhere.

Based on the math, market makers are discounting the likelihood of the upside risk materializing. This skew is to be expected, as demand tends to be heavier for protective puts rather than speculative calls since securities typically decline faster than they rise.

Still, traders can't just rush in and buy bull call spreads because the downside risk is very much real. So, the prudent strategy may be to combine the bull spread with the bear spread in an advanced strategy called the long iron condor.

Having Your Cake And Eating It Too

Condor strategies can be confusing because they're conceptually alien to regular buy-and-hold investors. The open market is very much like Newtonian mechanics. An object can't have maximum potential energy and maximum kinetic energy at the same time. Similarly, if one is fully long TEAM stock, one cannot simultaneously be fully short TEAM stock.

In the wild quantum world, the rules of reality loosen a bit with concepts such as superposition, where two states of simultaneous existence can occur until the wavefunction collapses. In a somewhat analogous manner, a trader can be simultaneously bullish and bearish — in this case by buying volatility.

Here's what that looks like in practical terms. Traders may consider the 160 | 165 || 195 | 200 long iron condor expiring Oct. 17. This transaction combines the 160/165 bear put spread and the 195/200 bull call spread. Basically, the idea is for TEAM stock to either fall through the $160 short put strike or rise through the $200 short call strike at expiration.

At the moment, the risk-reward ratio is 1.63-to-1. The trade requires a net debit of $310 for the chance to generate a profit of $190. No, it's not as richly rewarding as buying one vertical spread. However, a long iron condor combines two spreads (because the trader is betting on two outcomes). Therefore, the payout for probabilistically rational trades is reduced.

For those who are ultra-aggressive, the same long iron condor above but with the bearish leg being modified to a 155/160 bear spread could be attractive. This transaction requires a net debit paid of $280 but with a maximum profit of $220.

The opinions and views expressed in this content are those of the individual author and do not necessarily reflect the views of Benzinga. Benzinga is not responsible for the accuracy or reliability of any information provided herein. This content is for informational purposes only and should not be misconstrued as investment advice or a recommendation to buy or sell any security. Readers are asked not to rely on the opinions or information herein, and encouraged to do their own due diligence before making investing decisions.

Read More:

Image: Shutterstock