And that’s a good enough point to stop for the evening.

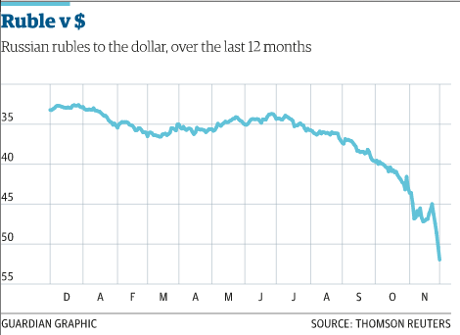

The ruble appears to have stabilised at around 52 to the dollar, a slide of over 3% today. It was down 6.5% one stage, on track for its biggest one-day loss since the crisis of 1998.

The intervention by the Bank of Russia appears to have calmed the situation, as do the comments from the central bank’s deputy governor (details). The currency has still shed over 35% this year.

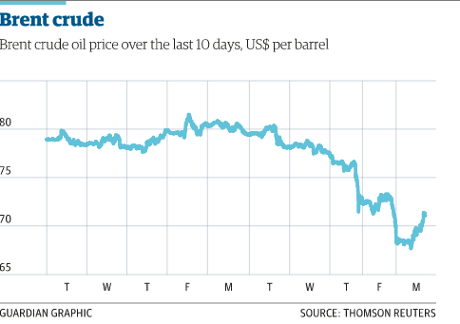

The oil price is clinging on to its earlier gains, having hit five-year lows earlier.

But shares in oil producers and exploration firms have fallen sharply again; the FTSE 100 ended down 66 points, its biggest fall in six weeks.

Nick Fletcher’s market report has the details:

FTSE 100 suffers biggest daily fall since mid-October

Scroll back through the blog for details of this morning’s rather mixed economic data (factories in the US, UK and Spain did OK; those in the eurozone and China did not)

I’ll update the blog again remotely if anything serious happens. Otherwise, thanks, and goodnight. GW

As so often in life, The Simpsons got there first....

we’ve all posted this today, yes? https://t.co/kKZoSwVksv

— Alex Hern (@alexhern) December 1, 2014

The fluctuations in the oil price will have meant big profits, or losses, for speculators, and longer-term investors alike.

Huge moves in commodities (Primarily Gold / Crude) since Thursday, so big margin calls on the way up & down.

— Joe Bond (@Joe_Trading) December 1, 2014

The oil price lives to fight another day, it seems, now up over 2% after earlier tumbling by over 3%:

Ksenia Yudaeva, the Russian central bank’s deputy chairwoman, told Russian newswires today that Russian households should not panic over the ruble’s slide.

She said the recent hike in interest rates, to a chunky 9.5%, should encourage them not to convert savings into euros or dollars.

She said:

“It’s necessary to explain to people that the yield they get on their deposits at the moment will guarantee a high degree of safety for their savings with regards to inflation. They should think twice before rushing out, losing the yield on their deposits, taking on currency risks and losing money on their currency conversions.”

French bank BNP Paribas has just lowered its forecasts for the the oil price over the next year, by up to $25 per barrel at one point

Biiiiiiig revisions in BNP Paribas' oil price forecasts. pic.twitter.com/nxNET34Ad3

— Mike Bird (@Birdyword) December 1, 2014

That implies significant changes to inflation, consumer spending, and income for oil producers.

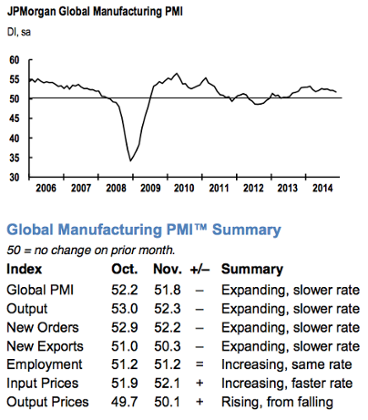

Global factory growth fell to a 14-month low in November.

Analysts at JP Morgan have added up all today’s manufacturing PMI surveys from America, China, the Eurozone, the UK and beyond, and concluded that growth was the weakest since September 2013.

Canada, the US, the UK and Japan all reported above-average growth, while China and the eurozone lagged.

The ruble has been falling steadily since the the Ukraine crisis intensified over four months ago, when a Malaysian Airlines plane was shot down with the loss of 298 lives:

A bad day for the Russian ruble. Here's the slide since Malaysian Airlines flight MH17 was shot down on July 17 pic.twitter.com/JVigGN8mb8

— Stephanie Baker (@StephaniBaker) December 1, 2014

Finally a bounce in the oil price! But US $71 for a barrel of Brent Crude Oil is not much of a bounce is it? #Disinflation

— Shaun Richards (@notayesmansecon) December 1, 2014

The ruble is also clambering back off the mat, after its earlier pounding.

Russia’s currency is still down over 3% today, to around 51.8 to the dollar, having been down around 7% (!) earlier.

That apparent intervention by the Central Bank of Russia appears to have stabilised the situation, at least for now...

Good to see the CRB's Cyber Monday offer on RUB was taken up well

— World First (@World_First) December 1, 2014

Updated

It’s a topsy-turvy day – the oil price is now UP today, with both Brent crude and New York crude up over 1% now (to $67 and $71 per barrel respectively).

It’s a tentative bounce back, driven (I think) by the US dollar dropping in the foreign exchange markets.

A weaker dollar generally pushes up the price of commodities priced in greenbacks, and also explains why gold has rallied today.

Oil traders had hoped that the oil price would find a floor today, having dropped like a stone since Opec declined to cut production levels last Thursday.

But the volatility is bad news for the ruble, as the Wall Street Journal explains:

The slide in oil is “reinforcing the loss of investor confidence in the ruble,” which has also been beset by concerns over Western sanctions against Russia and the conflict in Ukraine, said Lee Hardman, a currency strategist at Bank of Tokyo-Mitsubishi UFJ.

Back to Russia, and the ruble continues to be buffeted around.

Fears of a deep recession, and the rout in the oil price this week, have sent the ruble down 5% today (see earlier summary for details). It’s hovering around 52 rubles to the $1, having earlier been on track for its biggest one-day decline since 1998.

AP reports that Ksenia Yudayeva, deputy chairman of the Russian Central Bank, told Russian news agencies on Monday there is enough currency liquidity in the market.

Yudayeva added that the Central Bank has prepared new economic forecasts based on a price of $60 per barrel. They might be unpleasant reading, given Russia’s oil industry needs a price around $100 to break even.

Here comes the second measure of US manufacturing, from the Institute of Supply Management...

And it confirms that the sector slowed a little in November, but still grew fairly strongly. The ISM’s US factory PMI dipped to 58.7, from 59 last month -- which is a little better than expected.

But the survey also shows that the prices paid by manufacturers fell last month, which is curious (suggesting firms were able to haggle hard in a low-flation environment)

US ISM, manuf 58.7 but look at prices (not) paid at 44.5....

— kit juckes (@kitjuckes) December 1, 2014

The prx paid number v odd indeed : US Headline is 2nd highest since 2011 . so certainly something of a recovery after a run of bad data.

— Steve Collins (@TradeDesk_Steve) December 1, 2014

Back in Europe, the European Central Bank’s new Asset-Backed Securities scheme has got off to a slow start.

The ECB just announced that it bought less than €400m of ABSs last week; the latest stage in its attempt to fight off stagnation, or worse.

Analysts aren’t impressed with this meagre expansion of the ECB balance sheet:

*ECB SETTLED 0.4B EUROS ABS PURCHASES IN FIRST WEEK OF BUYING

— World First (@World_First) December 1, 2014

which is naff all

— World First (@World_First) December 1, 2014

€368m?? Are you f-ing kidding me? @ecb ABSPP

— Lorcan Roche Kelly (@LorcanRK) December 1, 2014

@LorcanRK @ecb At that rate, only another 2,717 months to go to get the €1tn balance sheet expansion.

— James Mackintosh (@jmackin2) December 1, 2014

Markit: US factory PMI hits eight-month low

Markit reports that US factory output grew at its slowest rate since January, but still comfortably outpaced Europe

Their US manufacturing PMI came in at 54.8, down on October’s 55.9. Although that’s the lowest reading since the start of the year, it still shows steady growth.

It’s also much better than the 50.1 recorded by the eurozone this morning, which is basically stagnation.

Slowing global economy having its effect. New export orders by US manufacturers fall at fastest pace in over a year. pic.twitter.com/fCVLm26mem

— Joseph Weisenthal (@TheStalwart) December 1, 2014

We find out in 10 minutes whether the rival survey, by the ISM, agrees....

Gold keeps climbing.... it just touched $1,192 per ounce, up 2.2% today.

Over in New York, shares have dipped in early trading as Wall Street traders get to work.

The Dow Jones industrial average is down 54 points, or 0.3%.

Weak manufacturing data this morning from China (details here) and Europe (and here) are weighing on the US market, as is news that retail spending over the Black Friday long weekend was down this year.

In other commodities news, the gold price has been volatile today after Swiss voters rejected the proposals that its central banks should hold 20% of its total assets in bullion.

The spot price of gold fell sharply in early trading, hitting a three week low below $1,143 per ounce.

But it then recovered, hitting $1.182 per ounce this afternoon, up around $15/oz.

c

The bosses’ protest in Paris comes as the French government prepares to unveil new legislation designed to stimulate growth and activity, later this month.

Unions and left-leaning politicians fear that workers’ rights and protections will be eroded.

Photos: French business leaders protest in Paris

Over in Paris, hundreds of French bosses have held a protest to urge the goverment to cut tax and reduce red tape.

Small business owners marched through the French capital. They carried banners with slogans such as “Taxes, levies, charges: enough is enough”, or calling for the end of the 35-hour maximum working week.

It was organised by the CGPME union, which represents small and medium-sized business owners. It claims that excessive regulations and charges are holding them back. Some even carried locks and chains to symbolise their plight.

Police put the turnout at 2,200, about half that estimated by CGPME.

Updated

Interesting... the oil price has now clawed back this morning’s selloff, which saw it hit fresh five-year lows.

The price of US crude oil is now back at at $66.34/barrel, and Brent crude at around $70. Still sharply lower than a week ago, but broadly unchanged today.

The bounce-back came after the cabinet of Saudi Arabia (the most powerful member of Opec) said the oil cartel had shown “cohesion, unity and foresight” by leaving production levels unchanged at their meeting last week.

The Saudi cabinet also called for co-operation against “market speculators”, suggesting it thinks the selloff hasn’t been driven purely by fundamentals.

Updated

Larry Elliott: Russian banks vulnerable to ruble's slide

Larry Elliott, our economics editor, reckons the Russian central bank had to wade into the markets to prop up the ruble this lunchtime:

A ruble in freefall does pose a threat to financial stability in two big ways. Firstly, it increases the foreign currency value of Russia’s foreign liabilities, currently worth around $200bn (£127bn). Secondly, a continued fall in the exchange rate will encourage Russian citizens to convert rubles into dollars and euros, thus increasing the risk of bank runs.

Russia’s banks are in better shape than they were in 1998 and the government has the financial firepower to help them out should they get into trouble.

But a plunging oil price and a plunging ruble still make the banks vulnerable. Hence the need to intervene.

Here’s Larry’s analysis on the ruble’s slide:

Why the collapse in the Russian ruble matters to the global economy

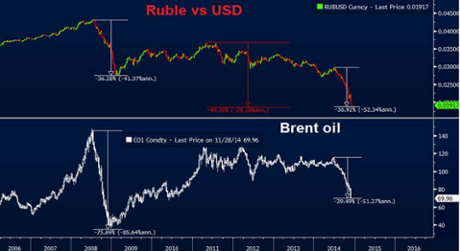

And here’s the chart of the ruble vs the US dollar, showing how it spiked to record lows of 54 rubles/$1 (the high point on the graph) before dropping back:

There’s a strong correlation between the slump in the oil price in recent months and the weakness of the ruble.

But the ruble has actually fallen more than you’d expect, if you compare the current situation to the height of the financial crisis:

Ashraf Laidi, Chief Global Strategist at cityindex.co.uk, explains (and provides a handy chart):

Since making its most recent peak in June at $115.71 per barrel, Brent crude is down 39%, during which the ruble fell 37%.

Interestingly, the ruble’s decline matches that of the 2008-2009 when oil price crashed more than 75%. For the ruble to fall by the same magnitude on the back of an oil decline that’s half that of 2008/9 highlights the sobering fact that there’s more to ruble’s woes than just falling oil.

So what’s changed? The Ukraine crisis is one obvious factor; sanctions imposed by the West could run for several years, and are already hitting trade and growth.

Also, Russia’s fiscal position has deteriorated over recent years. Back in 2006, it needed an oil price of around $21/barrel to break even -- not the $100/barrel today.

Update: the ruble is clawing its way back from the brink, from 54 rubles to $1 to “just” 52.

Traders suspect the Central Bank of Russia has waded into the markets. Analysts at Citi say:

“It looks like the Russian central bank could be the behind it.”

Summary: Oil price slide sends ruble tumbling

Time for a recap after a morning of generally downbeat economic news (with some highlights):

The oil price has hit its lowest level since October 2009 this morning, amid fears that the global economy is slowing

Opec’s decision not to cut supplies continued to reverberate through the markets, too, sending Brent crude down over $3 per barrel to a five-year low of $67.53. It’s recovered a little since, to $69.60, but remains weak:

Energy Aspects’ chief oil analyst Amrita Sen says the oil market “is still very much in panic mode”:

“Once we get over the panic, Brent prices will probably stabilise at around $65-80 a barrel in the short term.”

Russia’s ruble is in freefall today, down over 7% at record lows at around 53.7 rubles to the $1 (at pixel time).

It’s being dragged down by the oil price, and predictions of a sharp recession next year:

Moscow-based investment bank Sberbank CIB said in a morning note:

“In the short term, the Russian market is a victim of OPEC’s apparent decision to reduce the volume of high-cost production through lower prices,”

“The market and the ruble will not stabilize until oil does.”

Rouble getting beaten like it owes money. Down 7.30% vs USD on the session

— World First (@World_First) December 1, 2014

Ack! :/ RT @TheStalwart: 5-year Ruble chart. Amazing crash. pic.twitter.com/vl7Hf5T4Rs

— Elena Holodny (@elenaholodny) December 1, 2014

The falling oil price also hit European stock markets; the FTSE 100 is down 60 points, led by energy producers and miners.

Wouter Sturkenboom, senior investment strategist at Russell Investments, explains (via Reuters)

“There’s downward pressure on many commodities. That is a function of disappointing global growth and especially the slowdown in China,”

That is negative for equities.”

The latest manufacturing surveys have shown that many factories struggled to grow last month.

China’s factory growth slowed to an eight month low, with firms reporting that growth in output and new orders both fell.

The eurozone’s manufacturing sector posted virtual stagnation, with activity falling in Germany, France and Italy.

The UK did better, though - with manufacturing growth touching a four-month high. New exports orders are down again, though, showing weaker demand in emerging markets and Europe.

Japan has been downgraded by Moody’s, on fears about its ability to hits its fiscal and growth targets.

In the City, shares in Vodafone have dropped on reports that it might tie up with America’s Liberty Global:

Market forces live > Vodafone falls 5% on renewed deal talk http://t.co/qw0RUGyOJe

— Nick Fletcher (@nickfletchergdn) December 1, 2014

OIl exploration firm BG Group has bowed to criticism and cut the ‘golden hello’ being granted to its incoming CEO. Helge Lund will no longer be able to earn up to £25m, but might scoop £18m....

BG Group cuts Helge Lund’s ‘golden hello’ after shareholder pressure

The ruble’s selloff continues...

RUBLE TUMBLES TO 53.00 VERSUS US DOLLAR

— Russian Market (@russian_market) December 1, 2014

This chart provides a little perspective on this morning’s rise in unsecured consumer borrowing:

Are Britons loading up on unsecured credit again? Level of debt now highest since Spring 2011 according to BoE: pic.twitter.com/G4UCjbKcCM

— Ben Chu (@BenChu_) December 1, 2014

Ruble hits new record lows

The slump in the oil price has piled more pain on Russia, sending the ruble into freefall today.

The ruble has tumbled by 4.5% against the US dollar today, to 52.5 rubles to the $1.

The fall in the oil price to below &70/barrel is likely to drive Russia into recession next year. It needs an oil price around $100/barrel to break even.

As this chart shows, the ruble has shed over 35% of its value this year.

That makes it the second worst performing currency this year after the Ukranian hryvnia -- which has been routed since the military conflict in Eastern Ukraine triggered a deep and ongoing slump.

#Russia Ruble seems to be about to overtake #Ukraine Hryvnia in 2014 currency ugly contest. Ruble now down 37%ytd. pic.twitter.com/0jXW2NZaLH

— Holger Zschaepitz (@Schuldensuehner) December 1, 2014

Rouble now down 5% today against dollar/euro basket, 34% since beginning of the year. Is it what they call a meltdown?

— Pierre Briançon (@pierrebri) December 1, 2014

Britons piled more debt onto their credit cards in October.

Data from the Bank of England showed that net unsecured consumer credit rose to £1.087 billion in October from £942 million in September.

That may alarm the Bank; policymakers have warned that people have been dipping into their savings to fund spending, while they wait for real wages to rise.

The robust UK factory data has given the pound a lift.

Sterling has gained over half a cent against the US dollar, to $1.571.

The euro is a little higher too, up 0.2% against the dollar, despite factory activity slowing to near-stagnation.

Nicholas Ebisch, currency analyst for Caxton FX, suggests traders are relieved that the situation isn’t even worse. Here’s his take:

“Sterling has rallied this morning after a positive Manufacturing PMI figure.

With the pound steady so far on the day, this latest data has helped bolster the currency against the dollar and many other currencies to start the week off. However, the Euro has had an overall strong morning as well with Final Manufacturing PMI for the Eurozone showing only very slight growth at 50.1, but Spanish Manufacturing beating expectations at 54.7.

A reading over 50.0 indicates that there is growth in the sector, and right now the Eurozone needs all the positive signs of growth that it can get.”

Updated

Today’s forecast-beating UK manufacturing PMI survey shows that British factories are upbeat despite the troubles in Europe, says Rob Wood of Berenberg:

UK manufacturing is resisting the weakness in the Eurozone on the back of strong domestic momentum this side of the Channel.

New export orders fell again, especially from the EU, Russia and emerging markets, but domestic spending kept the show on the road.

The slowdown in the UK housing sector continues, with the number of new mortgages approved by lenders hitting a 16-month low.

A total of 59,426 new loans for house purchases were signed off in October, down from 61,234 in September. It indicates that tighter mortgage rules continue to take the heat out of the market.

Markit economist Rob Dobson blames the weak euro, and the general economic slowdown, for the drop in new exports from UK factories last month:

Slower global economic growth is hitting sales to emerging markets, while a strong sterling-euro exchange rate is also stifling trade with the eurozone nations.

UK manufacturing shrugs off weak export growth

Britain’s factory sector has outpaced the eurozone.

Output, new orders and employment levels all grew last month, thanks to “solid domestic” demand, according to data just released by Markit.

The UK manufacturing PMI (based on data from factory purchasing managers) rose to a four-month high of 53.5 in November, up from 53.3 in October.

That indicates that growth was a little more rapid last month, despite concerns that the UK economy is slowing down.

Good news! UK manufacturing #PMI improves to 53.5 as the recovery continues #GBP

— Shaun Richards (@notayesmansecon) December 1, 2014

However, new export order growth “remained weak” during November, falling for the third month running.

Markit says:

Exporters faced a combination of subdued global market conditions and a relatively strong sterling-euro exchange rate.

David Noble, CEO at the Chartered Institute of Procurement & Supply, agrees that UK factories relied on domestic demand last month.

Noble added:

This domestic uplift has been the counterbalance to disappointing export opportunities with the strength of sterling and lack of activity from emerging markets having an impact.

Updated

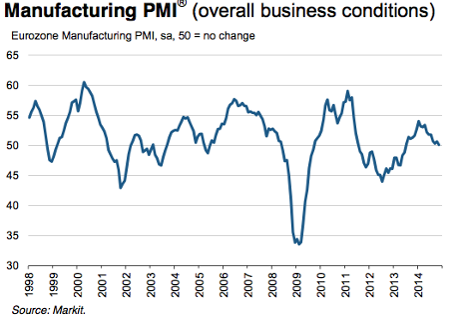

Eurozone manufacturing hits near-stagnation as Big Three nations contract

Europe’s economy woes deepened last month, as growth in its manufacturing sector ground to a near-standstill.

That’s the message from this morning’s purchasing managers surveys, which show that storm clouds continued to gather over the eurozone economy in November.

Markit’s eurozone factory PMI fell to just 50.1 last month - a fraction above stagnation.

It is based on interviews with thousands of firms at eight eurozone countries; five nations reported contractions in November, the highest proportion since July 2013.

Companies reported that new orders fell last month, while output grew at a slower rate again and manufacturing employment was broadly flat.

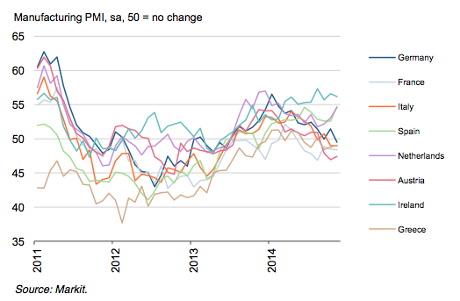

The slowdown was driven by contractions in Europe’s three largest economies -- Germany, France and Italy. That wiped out Spain’s decent performance (see earlier post)

Eurozone manufacturing stagnates as big-three nations contract; #PMI at 50.1 (50.6 in Oct) http://t.co/SBwjyWY7Oq http://t.co/vDdIlPQpB0

— Markit Economics (@MarkitEconomics) December 1, 2014

Chris Williamson, Markit’s chief economist, says “the situation in euro area manufacturing is worse than previously thought” (Markit’s ‘flash’ PMI report, two weeks ago, was less worrying).

Not only is the performance of the sector the worst seen since mid-2013, there is a risk that renewed rot is spreading across the region from the core. The sector has more or less stagnated since August, but we are now seeing, for the first time in nearly one-and-a-half years, the three largest economies all suffering manufacturing downturns.

“Germany’s export engine has stalled, causing the steepest deterioration of new orders in the country since December 2012, and new business is also falling in both France and Italy, boding ill for production in coming months.

Spain, Ireland and the Netherlands all outperformed the rest of Europe, Williamson added, but can they avoid being dragged back?

Updated

PMI Manuf readings not providing great start to new week/month

— Mike van Dulken (@Accendo_Mike) December 1, 2014

Ouch! Germany’s factory sector suffered a small contraction last month, showing that Europe’s largest economy struggled in November.

The German factory PMI fell to just 49.5, as firms reported the sharpest drop in new orders in almost two years.

This is the first time in 17 months that the German manufacturing PMI has come in below 50 points, showing a fall in activity.

Germany Mfg #PMI falls to 17-month low of 49.5, signalling downturn in German manufacturing http://t.co/oMokaWBhl3 http://t.co/oTnlmZylJN

— Markit Economics (@MarkitEconomics) December 1, 2014

Updated

France’s manufacturing base also contracted last month.

The French factory PMI hit 48.4, largely unchanged from October’s 48.5 (but not as bad as the flash estimate released two weeks ago)

More economic woe for #France as its maufacturing #PMI remains in contraction territory at 48.4 #Euro #ECB

— Shaun Richards (@notayesmansecon) December 1, 2014

Italy’s factory sector continued to shrink last month, according to data firm Markit.

The Italian manufacturing PMI came in at 49.0 for November, weaker than expected (anything below 50 indicates a contraction).

Japan downgraded by Moody's

Just in: Moody’s has downgraded Japan’s credit rating, from AA3 (the fourth-highest rating) to A1 (five-highest).

Moody’s blamed ‘heightened uncertainty’ over Japan’s ability to hit its deficit reduction goals, and to achieve the growth targets set by the government.

It says:

The first driver for the downgrade of the Japan government’s debt rating to A1 is the rising uncertainty over whether the government’s medium-term deficit reduction goal is achievable, and whether policy makers can overcome the tensions inherent in promoting growth while simultaneously stabilizing and reversing the rising debt trajectory.....

The second driver for the downgrade is the rising uncertainty over the government’s ability to enhance medium term growth through structural economic reform -- the third ‘arrow’ of Abenomics -- success in which will be crucial to achieve fiscal consolidation. While some indicators suggest a pick-up in economic activity over the past year, potential economic growth remains low.....

The yen wobbled on the news, hitting a new seven year low of ¥119.15 against the US dollar.

But the downgrade isn’t likely to have any immediate impact on Japan. Its borrowing costs are currently at record lows, despite its huge national debt (over 200% of GDP).

Moody's downgrades Japan to A1 from Aa3 ... just as Japan enjoys lowest borrowing costs on record. Last week, 2y yield even went negative

— Jamie McGeever (@ReutersJamie) December 1, 2014

Updated

Australia’s stock market has also been hit hard by the oil price slide.

Fears that the global is slowing down helped to wipe $30bn off the main Australian index today.

That takes the total losses since Friday to $53bn, on an index heavy with mining and energy firms.

The benchmark S&P/ASX 200 Index shed almost 2% today. with the energy sector diving by over 6%.

The Sydney Morning Herald has more details:

Local shares are now trading down 2.7 per cent for the year-to-date, while the dollar is trading around levels not seen since July 2010 as a slide in global oil prices puts pressure on the local market.

At its bi-annual meeting last week, the Organisation of Petroleum Exporting Countries (OPEC) elected to maintain production levels despite a slide in energy prices over recent months as the growth in global supply has outstripped the growth in demand.

“Through OPEC the Saudis have declared an oil price war on the US and Australia is getting caught in the crossfire,” Fiducian Group investment manager Conrad Burge said.

Updated

Shares in oil companies are being hit hard in London this morning, as Brent crude hits a five-year low below $68 per barrel this morning.

The FTSE 100 has fallen by 60 points, or almost 1%, at the start of trading. Energy and commodity firms are leading the fallers; exploration firms Tullow Oil and Weir Group are the worst hit.

Spanish PMI hits seven-year high

Good news from Spain, its manufacturing sector expanded at the fastest rate since June 2007.

The Spanish factory PMI rose to 54.7 last month, beating expectations of 52.1. Markit, which conducted the survey, says:

Output and new orders each rose at rates not seen since prior to the economic crisis, while employment also increased at a faster pace

Firms also reported a widespread drop in raw material costs, with cotton, dairy products and petrol reportedly down in price. That won’t ease fears that the euro area could slide into deflation.

Spain PMI: 'There is little sign of any end to deflationary pressures in the sector as prices for both inputs and outputs continued to fall'

— Markit Economics (@MarkitEconomics) December 1, 2014

That's a nice rebound in Spanish manuf PMI. New orders, output & employment highest since Q2 07. Output prices down though.

— Frederik Ducrozet (@fwred) December 1, 2014

Updated

The sharp fall in the oil price is excellent news for consumers and firms with large transport costs.

Analyst Steve Baines flags up that drivers have already felt some benefit:

Fuel prices at the pump have now declined by 8p/litre since the end of September. Equivalent to a £2.7bn annual boost to disposable income.

— Stephen Baines (@spbaines) December 1, 2014

Analyst Ian Williams of Peel Hunt says the prospect of cheaper oil is dominating the markets today.

The immediate focus will remain on cheaper oil; good news for consumers and for those companies benefiting from reduced input cost pressures, less so for central bankers wrestling with disinflationary concerns.

Oil hits lowest level since 2009

The oil price has hit its lowest levels since October 2009 as the steep selloff than began last week continues.

The news that China’s manufacturing growth had hit an eight-month low helped to drive the price of a barrel of Brent crude down to just $67.76 this morning.

That’s a fall of 3.4%, or $2.40, since Friday night. Brent has tumbled by 14% since Opec decided not to cut this production levels last week:

New York crude also slid to a new five-year low this morning, hitting $63.95 per barrel.

The scale of the selloff has stunned many in the markets:

As Phillip Futures analysts said in a research note:

“Just when the market was thinking that a 4-year low for crude oil was bad enough, we have hit a 5-year low after the OPEC meeting,”

Another worrying sign - Indonesia’s factory PMI fell to its lowest level since the survey began 44 months ago.

HSBC #Indonesia mfg #PMI falls to record low of 48.0 in November (49.2 in Oct) and cost #inflation accelerates http://t.co/AOBGqikzPV

— Markit Economics (@MarkitEconomics) December 1, 2014

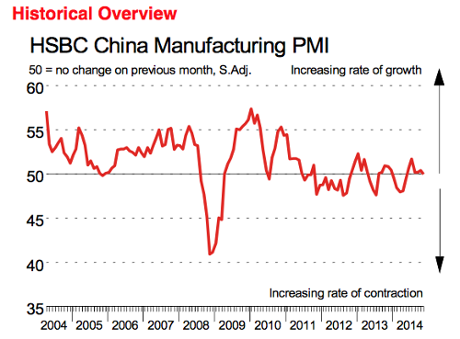

Chinese factory PMI hits eight-month low

Asian factories suffered a drop in growth last month, in the latest sign that the global economy faltered in November.

China’s factories grew at their slowest pace in eight months, according to Beijing’s survey of the sector. Firms reported a weakening in output, and in new orders.

The official Chinese Purchasing Managers Index (PMI) fell to 50.3 last month from 50.8 recorded in October, showing slowing growth in the country’s factories and workshops.

It helps explains why the Chinese central bank cut interest rates unexpectedly last month.

HSBC’s rival measure, which is more focused on small firms, fell to exactly 50.0 - the cut off point between expansion and contraction.

HSBC found that manufacturing production levels fell last month, for the first time in six months. New exports grew at the slowest rate since June, as demand from overseas waned... and input prices fell, as deflationary pressures grew.

HSBC’s chief economist for China, Hongbin Qu, says the data shows China’s economy weakening.

Domestic demand expanded at a sluggish pace while new export order growth eased to a five-month low.

Disinflationary pressures remain strong while the labour market weakened further.

The agenda: Manufacturing PMIs, oil and gold fall

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Today, we’ll be covering the latest health check of global manufacturing, which will probably show that Europe’s factories struggled last month.

Markit’s surveys of factory output are expected to show another contraction in France and Italy, and weaker growth in other parts of the eurozone.

The UK manufacturing PMI is also released, at 9.30am, giving a picture of the British economy ahead of Wednesday’s Autumn Statement.

Fears over global growth are already weighing on the markets, pushing the oil price down again this morning (more in a moment).

Gold is under pressure too, after Switzerland voted not to force its central bank to told 20% of its assets in gold.

The retail sector may be worried, after data last night showed that Americans spent 11% less over the Black Friday period than a year ago.

Oh, and speaking of seasonal (or do I mean spurious?) slogans, its Cyber Monday.