And finally, another business leader has entered the debate on Scottish independence.

The head of Aviva, Mark Wilson, is the latest to flag up concerns over Thursday’s referendum, telling the BBC’s Kamal Ahmed that he’s worried that infrastructure funding (building of schools, hospitals and roads) could become more expensive.:

“Other commentators have pointed out the challenges that the Scottish financial system will face in the event of a yes vote”

“Aviva is a long-standing investor in Scottish infrastructure and we will maintain our commitment.”

The comments come as David Cameron campaigns for a No vote in Scotland:

Cameron tells Scots: "If you don't like me I won't be here forever, if you don't like this govt, it won't be here forever" #scotRef

— Beth Rigby (@BethRigby) September 15, 2014

"I understand why it might be appealing to vote yes.. But when something looks too good to be true that's because it is" PM

— Faisal Islam (@faisalislam) September 15, 2014

European stock markets ended the day pretty calmly, as investors prepare for drama later this week.

European Markets (close) FTSE 6804.21 -2.75 -0.04% DAX 9659.63 8.50 0.09% CAC 40 4428.63 -13.07 -0.29% STOXX600 343.78 -0.49 -0.14%

— Brenda Kelly (@BrendaKelly_IG) September 15, 2014

Jasper Lawler , market analyst at CMC Markets, says worries over weak Chinese factory data were balanced by the takeover talk in the brewing industry:

Trading in Europe has been mixed today with M&A speculation amongst brewers mixing in with fears over a slowdown in China which added to a general uncertainty heading into the Scottish referendum and this month’s Fed meeting.

Afternoon summary

OK, time to recap the key points.

1) The OECD cast a shadow over the global economy by cutting its growth forecasts for most major countries today.

OECD deputy secretary-general Rintaro Tamaki said:

“The global economy is expanding unevenly, and at only a moderate rate. Trade growth therefore remains sluggish and labour market conditions in the main advanced economies are improving only gradually, with far too many people still unable to find good jobs worldwide.

“The continued failure to generate strong, balanced and inclusive growth underlines the urgency of undertaking ambitious reforms.”

The Paris-based thinktank warned that the eurozone remains weak, and at risk of deflation....

....and also cited the Scottish referendum as a threat to the recovery.

2) Economists are urging investors not to panic after US industrial output fell unexpectedly last month. Unusual activity in the auto industry is being blamed.

More encouragingly, the Empire Survey of factories in the New York region has hit a near five-year high.

3) But the latest Chinese factory data has also showed a surprise slowdown, hitting Asian markets overnight.

4) Shares in SABMiller have surged 10% on reports that the world’s largest brewer, AB InBev, is considering a takeover bid. Analysts say SAB’s failed bid for Heineken, which emerged yesterday, may rebound on it.

The deal could value SAB at £75bn. It would bring together many of the world’s biggest drinks brands.

5) Thousands of Phones 4u staff, and many more customers, face uncertainty after it announced it was calling in the administrators. Stores remained shut today.

Dixons Carphone, its high street rival, has said it will hire hundreds of staff, while Phones 4u has promised to refund orders.

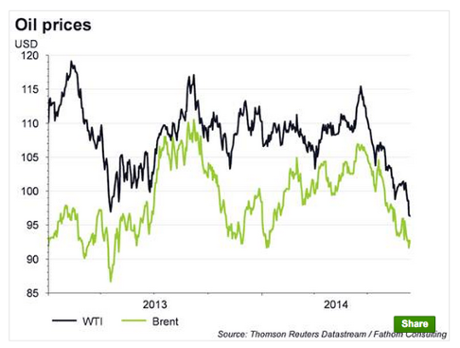

6) The Brent crude oil price hit its lowest level in 27 months this morning, but has risen back over the $97 per barrel mark now.

7) And Microsoft is buying the software firm that developed Minecraft in a $2.5bn deal, turning the founder of the Stockholm-base firm into a dollar billionaire.

Extroardinary letter from an entrepreneur who just became a billionaire. http://t.co/swaHrpncMu

— Joseph Weisenthal (@TheStalwart) September 15, 2014

AP: US factory output drops 0.4% in August

Here’s Associated Press’s take on the US factory data:

US factory output drops 0.4 percent in August

U.S. manufacturing output declined in August for the first time in seven months, reflecting a sharp fall in production at auto plants that was due mainly to seasonal adjustment problems.

Output at manufacturing plants fell 0.4 percent in August after a 0.7 percent rise in July, the Federal Reserve reported Monday. Total industrial production was down 0.1 percent in August, also the first setback for the overall figure since January. Output was up in mining and utility production but these gains were not enough to offset the decline in manufacturing.

Output of motor vehicles and parts dropped 7.6 percent after a 9.3 percent increase in July. The reversal was not viewed as worrisome. The July figure was boosted because many plants did not shut down as they normally do to retool for new models. That made August look weaker.

Economists had been looking for a weaker figure for factory output in August as auto activity returned to more normal levels. The fact that there were fewer plant shutdowns in July made output look stronger after the government adjusted the figure for normal seasonal variations. And that seasonal adjustment then made the August figures look weaker.

Outside of manufacturing, output at utilities rose 1 percent after a big 2.7 percent drop in July which reflected cooler-than-normal temperatures that month. Output in mining, a category that includes oil and gas production, rose 0.5 percent in August after a 0.3 percent drop in July.

Paul Dales, senior U.S. economist at Capital Economics, said he was not overly concerned by the dip in industrial production because it reflected a temporary seasonal adjustment problem. He said gains in a number of industries outside of autos “underlines that industry remains healthy.”

A broad increase in manufacturing this year has pointed to stronger growth across the economy, suggesting that manufacturers expect business investment and consumer spending to improve in the coming months.

Updated

Capital Economics agrees that we shouldn’t panic, saying:

The fall in industrial production in August was just due to problems seasonally adjusting autos production and is therefore not a sign that the recovery is running out of steam.

The more upbeat survey evidence emphasises that industry remains healthy.

ING: Not convinced by fall in US industrial production

Rob Carnell of ING reckons we shouldn’t get too alarmed by the unexpected drop in US industrial production last month.

He reckons it’s a rogue reading, partly due to a seasonal slowdown in the automobile industry.

Carnell told clients that:

A 0.1% month-on-month decline in US manufacturing production in August and a 0.4%mom decline in manufacturing in particular, are at complete odds with survey evidence and almost certainly an aberration that either reflects payback from the 0.7%mom manufacturing gain in July, poor seasonal adjustment (seasonal auto shutdowns in July may be being over-adjusted in July and weighing on the August numbers), statistical noise, or a bit of all of the above.

The polls show it’s neck-and-neck, but the feeling in the City is still that the Better Together side will win Thursday’s Scottish referendum:

Straw poll of just under 200 IG clients (small sample) this morning. 88% think No will swing it.

— Brenda Kelly (@BrendaKelly_IG) September 15, 2014

Here’s our news story on the speculation that SABMiller could be a takeover target (see 12.34pm onwards for details)

SABMiller shares leap 12% on AB InBev takeover rumours

US industrial output falls for first time since January

What were we saying about the US recovery looking solid?

Industrial output across the entire American economy fell by 0.1% in August, the first monthly drop since January 2014, according to data just released.

U.S. Aug Manufacturing Output -0.4 Pct, First Decline Since Jan 2014, (cons +0.3 Pct) Vs July +0.7 Pct (prev +1.0 Pct)

— cigolo (@cigolo) September 15, 2014

Weaker car manufacturing is the main cause:

Autos main drag as motor vehicle output -7.6% lower pulling overall man output down by 0.4%. Excluding autos, man output was 0.1% higher.

— Markit Economics (@MarkitEconomics) September 15, 2014

Microsoft buys Minecraft-maker Mojang for $2.5bn

More takeover news: Microsoft has just announced the acquisition of Mojang, the Stockholm-based software firm, for $2.5bn.

Mojang is the firm behind the hugely popular Minecraft brick-based online building game (a bit like Lego, but without the danger of tripping over half-constructed masterpieces)

Great acquisition. Minesweeper is going to be huge. RT @zerohedge: MICROSOFT TO BUY MOJANG FOR ABOUT $2.5 BLN

— Joseph Weisenthal (@TheStalwart) September 15, 2014

The deal is expected to close by the end of 2014. It will make founder Marcus Persson a billionaire, according to Forbes.

Microsoft has pledged to continue to make Minecraft available across all the platforms it currently runs on.

Updated

Analysts at Grupo Santander also reckon merger fever is alike in the brewing sector, triggered by SAB Miller’s’s failed attempt to merge with Heineken:

“If the wheels were not yet in motion on another brewing mega-deal, they may be now as SABMiller may have thrown down the gauntlet.”

Updated

Photos: Phones 4u remain closed

Phones 4u’s 500 stores are shuttered today, after the company took the shock decision to call in administrators after the loss of its contract with mobile operator EE left it unable to serve customers.

At at least one branch, staff have pinned the customer message that is also displayed on its website today.

Getting reports that customers unable to get through on any of the #Phones4U helplines listed on website. Bitter irony

— Dharshini David (@DharshiniSky) September 15, 2014

Dixons Carphone, meanwhile, has thrown staff a lifeline:

Dixons Carphone ready to hire Phones 4u staff

Updated

US Empire manufacturing survey highest since October 2009

Another sign that the US recovery remains solid -- the Empire manufacturing survey, produced by the New York Federal Reserve, has bounced back this month to a near five-year high.

The Empire survey, which takes the temperature of factories in the New York area, jumped to +27.54, up from +14.69 in August. Any reading above zero suggests conditions have improved.

Sep NY #Fed Empire survey rises to 27.4 from 14.7, highest reading since October 2009. This reinforces underlying strength in manufacturing.

— Joseph A. LaVorgna (@Lavorgnanomics) September 15, 2014

The pick-up was driven by a rise in prices received by manufacturers.

New YOrk area manufacturers appear to be experiencing some pricing power. pic.twitter.com/zDjQtZNRX8

— Joseph Weisenthal (@TheStalwart) September 15, 2014

The new orders index also rose, but the employment measure deteriorated.

SABMiller and Anheuser-Busch InBev may not be household names, but between them they own many of the world’s biggest beer brands.

AB InBev’s range includes lagers such as Budweiser, Stella Artois and Michelob, while it also European classics like Löwenbräu and Leffe.

SAB produces a range of Miller drinks, lagers including Pilsner Urquell and Peroni Nastro Azzurro. It also makes Snow, sold only in China, which it dubs “The biggest beer brand you’ve never heard of.”

Shares in SABMiller jump 12% on a @WSJ report that AB InBev is lining up financing for a bid: http://t.co/uqvpWaqigC pic.twitter.com/tRk5pYhHWz

— CNBCWorld (@CNBCWorld) September 15, 2014

City traders have been anticipating a takeover battle in the brewing sector since it emerged last night that SABMiller had made an unsuccessful bid for Heineken.

Alastair McCaig, market analyst at IG, says:

Over the weekend we have seen SAB Miller rebuffed in its attempts to woe Heineken, with the Danish brewer’s major shareholder preferring to remain independent.

If the M&A activity witnessed in the pharmaceutical sector this year is anything to go by then this will not be the last we hear about this.

Updated

It’s early days, but if Anheuser-Busch InBev do launch a bid for SABMiller then we’d be looking at one of the biggest takeover offers ever.

Before today’s 12% surge, SAB will valued at almost £55bn. The WSJ reports that AB are talking to banks about a possible £75bn offer -- that’s £6bn more than Pfizer’s recent failed bid for AstraZeneca.

A potential $122bn deal! Woah. RT @WSJbreakingnews: AB InBev talking to banks about financing to buy SABMiller. http://t.co/ypO4fKeSt4

— Sven Grundberg (@svengrundberg) September 15, 2014

SABMiller shares jump 12% on takeover talk

Shares in SABMiller have extended their earlier gains, now up 12% today as takeover speculation swirls through the brewing sector.

They surged a few minute ago, after the Wall Street Journal reported that Anheuser-Busch InBev, the world’s biggest brewer, was looking into getting financing for a bid for SAB.

The WSJ says that:

Anheuser-Busch InBev is talking to banks about financing what could be a roughly £75 billion ($122 billion) deal to buy global beer rival SABMiller, according to a person familiar with the matter.

A tie-up between the world’s two largest brewing companies has been rumored for years, but a revival in global merger activity this year has sparked renewed speculation about a deal. AB InBev isn’t in active discussions with SABMiller, said the person, explaining the company is waiting to line up its financing before making a formal approach....

More here: AB InBev Seeking Finance for SABMiller Deal

Bar talks MT @WSJ: Breaking: AB InBev talking to banks about financing deal to buy SABMiller http://t.co/coKpz1pSAh

— Matina Stevis (@MatinaStevis) September 15, 2014

As covered earlier, SAB is ‘in play’ after Heineken rejected a takeover bid from the UK brewer last night.

Fathom: ECB needs a bigger bazooka

Speaking of the eurozone, Fathom Consulting have predicted that the European Central Bank will launch a full-blown quantitative easing stimulus scheme by the end of this year.

One factor is the falling oil price (it hit a 27-month low this morning), which will push inflation lower.

Fathom write:

Earlier this month the ECB pulled out a small bazooka, announcing a 10 basis point cut in all three policy rates of interest, and setting out a programme of ABS and covered bond purchases. We view the latter as a staging post on the path to full-blown QE, which would involve the use of Central Bank money to buy government bonds, and Bunds in particular.

Mr Draghi’s announcement has affected our exchange rate forecasts, with the euro weaker through the remainder of this year than we had thought likely one month ago. But the consequences for euro area inflation are more than offset by falling energy costs.

For now, oil markets appear more focused on continuing signs of a slowdown in both China and Europe than on geopolitical risks stemming from increased tensions in the Middle East. Major oil benchmarks have fallen between $5 per barrel and $10 per barrel over the past few weeks, and this has caused us to revise down our inflation forecasts across the board.

We see euro area inflation hitting 0.0% by the end of the year. On our central view, this prompts the ECB to ramp up the purchase programme announced earlier this month to include purchases of sovereign debt. This brings about a meaningful depreciation of the euro, avoiding a prolonged period of deflation – for now.

Our take on today's OECD report

Here’s Katie Allen on today’s OECD report (highlights and charts start here):

The global economy faces headwinds from a sluggish eurozone and rising political tensions, including the uncertain outcome of Scotland’s independence referendum, a leading thinktank has warned.

The Organisation for Economic Co-operation and Development (OECD) has slashed its growth forecasts for advanced economies and called on the European Central Bank to use quantitative easing to shore up the eurozone.

Updating its economic outlook ahead of a G20 meeting of finance ministers in Australia this week, the Paris-based OECD described continued slow growth in the euro area as the “most worrying feature” of its new projections.

OECD deputy secretary-general Rintaro Tamaki said: “The global economy is expanding unevenly, and at only a moderate rate. Trade growth therefore remains sluggish and labour market conditions in the main advanced economies are improving only gradually, with far too many people still unable to find good jobs worldwide.....

More here: OECD slashes growth forecasts for leading economies

Updated

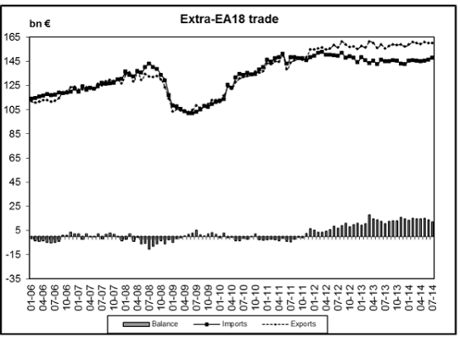

Euro area international trade in goods surplus €21 bn July 2014, +€2 bn for #EU http://t.co/aNyxWMpS0P @EU_Eurostat pic.twitter.com/Bvwz56gt0s

— European Commission (@EU_Commission) September 15, 2014

Eurozone trade data

Back in the eurozone, new data shows that the region’s trade surplus has swelled again, but there are signs that exports may be weakening.

Eurozone exports rose by 3% year-on-year in July, Eurostat reports, while imports only increased by 1%. This pushed the trade surplus to €21.2bn, up from €18bn in July 2013.

But on a seasonally adjusted basis, exports dropped by 0.2% month-on-month, while imports were up by 0.9%.

That has alarmed Howard Archer, economist at IHS Global Insight:

The seasonally-adjusted July trade data do little for hopes that net trade will do much to help the Eurozone return to growth in the third quarter after GDP only stagnated in the second quarter.

In fact, the July data suggests that there is a risk that net trade could actually be negative in the third quarter and hold back Eurozone GDP growth.

OECD: Bullish markets are at odds with growing risks

And if that wasn’t enough, the OECD is also worried that that global investors are too upbeat:

The bullishness of financial markets appears at odds with the intensification of several significant risks.

A number of equity markets are reaching record highs, sovereign bond yields in several countries are near all-time lows and implied share price volatility in the United States and Europe is around pre-crisis levels.

This highlights the possibility that risk is being mispriced and the attendant dangers of a sudden correction.

OECD: Key risks include geopolitics, Scotland and emerging markets....

The OECD has also cited the Scottish referendum as one of several key risks that could hit the global economy.

Here’s the list of risks highlighted in today’s update from the Paris-based thinktank:

- The possibility that euro area inflation will stay low and exacerbate weak demand

- Geopolitical risks have grown with an intensification of conflicts in Ukraine and the Middle East

- Increasing uncertainty about the outcome of the referendum on Scottish independence

- Many emerging economies remain vulnerable to financial market shocks given the build-up of debt, particularly corporate debt, in recent years

There are “upside risks” too, the thinktank notes, such as the current healthcheck of Europe’s banks.

• The successful implementation of the comprehensive assessment of banks in the euro area could be associated with faster-than-expected improvements in credit flows.

Updated

OECD: Eurozone recovery is disappointing

The OECD is pretty blunt about the eurozone’s problems:

The recovery in the euro area has remained disappointing, notably in the largest countries: Germany, France and Italy. Confidence is again weakening, and the anaemic state of demand is reflected in the decline in inflation, which is near zero in the zone as a whole and negative in several countries.

While the resumption in growth in some periphery economies is encouraging, a number of these countries still face significant structural and fiscal challenges, together with a legacy of high debt.

It urges the European Central Bank, which announced a new QE-style asset purchase scheme this month, to be bold:

The euro area needs more vigorous monetary stimulus, whereas the United States and the United Kingdom are moving to the end of their unconventional monetary easing.

And the OECD also warned that the eurozone’s weak inflation rate “raises the risk of slipping into deflation, which could perpetuate stagnation and aggravate debt burdens.”

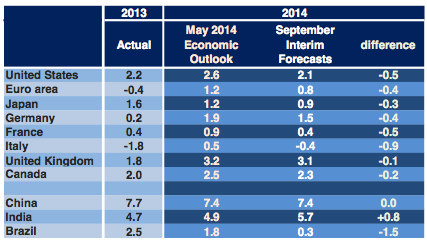

OECD slashes global growth forecasts

Breaking: The OECD has issued a new warning about “weak demand in the euro area” holding back the global recovery, and cut its growth forecasts for major economies.

The organisation has cut its global growth forecasts for most major economies, slashing its eurozone prediction from 1.2% to just 0.8%.

My colleague Katie Allen reports:

Updating its economic outlook published in May, the Organisation for Economic Co-operation and Development (OECD) says the global economy is continuing to expand at a “moderate and uneven pace”.

It adds:

“The tepid rate of growth means that a substantial degree of labour market slack remains, especially in the euro area, and world trade growth remains sluggish. Global growth should be somewhat more vigorous in the second half of 2014 and into 2015 given continued policy support, favourable financial conditions and growing confidence, alongside rising employment.”

The latest assessment also notes a “growing degree of divergence between the major economies.

“The recovery in the United States is solid, and growth is around trend in Japan and China and strengthening in India after the recent weak patch. By contrast, growth in the euro area looks set to remain subdued in the near term and Brazil is expected to make only a slow recovery from recession.”

The thinktank says monetary must remain supportive in all the major advanced economies “while most countries need to make further progress on fiscal consolidation to ensure that debt burdens remain sustainable.”

It flags a key risk as “the possibility that euro area inflation will stay low and exacerbate weak demand”.

Updated

Scottish vote weight on the pound

In four days time, we’ll know whether Scotland has taken the historic, dramatic step of voting for independence.

Amid the uncertainty over the UK’s future, the pound is jittery this morning, down around a tenth of a cent at $1.625.

Alasdair Cavalla of the Centre for Economics and Business Research says Scotland’s referendum will dominate the markets this week:

The economic consequences of a Yes vote are still unclear, with uncertainty over currency predicted, though certainly weaker prospects for certain industries.

As the three main UK parties and the Bank of England have all ruled out a currency union, Scotland would have to choose between a new “Scottish pound”, the euro, and unilateral adoption of the UK pound, where both of the latter two options would mean having no monetary independence. Scotland’s financial services industry would see a very negative outcome, with large numbers of job losses.

The outcome is still in the balance, with the No campaign only a couple of percentage points ahead in the latest polls.

This chart shows how the gap has narrowed....

Sterling nervous as tight Scottish independence referendum looms http://t.co/zfXdSFi9or #indyref pic.twitter.com/N3BVhSlVML

— Robin Wigglesworth (@RobinWigg) September 15, 2014

John Caudwell, the billionaire founder of Phones 4u, has blamed short-term private equity firms and “ruthless” mobile network operators for its demise.

I am sickened and saddened for nearly 6000 wonderful employees who made @Phones4u into a great business. #ruthlessvodafone #ruthlessEE

— johncaudwell (@johndcaudwell) September 15, 2014

Unfortunately combination of short term private equity strategy combined with ruthless network 'partners' & government killed @Phones4u

— johncaudwell (@johndcaudwell) September 14, 2014

Caudwell sold Phones 4u in 2006. It was then acquired by private equity form BC Partners in 2011.

Dixons Carphone shares jump after Phones 4U collapses

Phones 4u’s fall into administration is awful news for its staff, and a blow to customers. But it’s a fillip for its high street rivals.

Shares in Dixons Carphone are up 2.5% this morning, on predictions that it will mop up more sales if Phones 4u’s stores don’t reopen.

Here’s our Q&A on the Phones 4u collapse:

Phones 4u to close - Q&A

Back on the collapse of Phones 4u, and the stricken retailer has said that full refunds will be paid to customers with outstanding orders.

The company’s website is down this morning, complete with a glum emoticon:

As our story explains, Phones 4u blamed its fate on mobile network EE, which decided to stop selling through the company.

It’s a blow to anyone who had trusted Phones 4u to deliver the latest Apple handset:

The retailer has pledged to refund customers in full for any orders that have not yet been dispatched.

While there was grumbling on Twitter from customers who had ordered an iPhone 6 as recently as Friday, the company said it had ceased trading “as soon as practically possible”.

Phones 4u goes into administration – with 5,600 jobs at risk

The takeover talk in the brewing sector has also pushed Carlsberg’s share up around 1.9% this morning.

SABMiller shares up 5% on takeover talk, after Heineken bid rejected

Is the hunter about to turn into the hunted?

Shares in British brewing giant SABMiller have jumped by 5% today, after an attempt to merge with Heineken was rebuffed.

Dutch firm Heineken announced last night that it had rejected an approach from SAB, the world’s second-largest brewer by revenue.

Analysts say that SAB was keen to merge with Heineken to protect itself against a takeover offer from Anheuser-Busch InBev, the world’s biggest brewer.

With the family that controls Heineken determined to “preserve the heritage and identity” of the company, SAB could now be targeted by Inbev.

As Matthew Beesley of Henderson Global Investors put it to Bloomberg:

“SAB is the leading asset that everybody wants to own,”

“If you are InBev looking to truly build a global brewer, which they have been doing in recent years, the next asset that ABI would want to buy is SAB.”

SAB’s brands include Pilsner Urquell, Peroni Nastro Azzurro, Miller and Grolsch.

Heineken’s shares are up 1.4% today.

SAB strong in London +5.3% post #Heineken announcement, will Inbev make an offer?

— Charl Bester (@charlbester1975) September 15, 2014

SAB MILLER'S overtures to Heineken supposedly rejected out of hand. Some believe that SAB Miller could come under attack itself - InBev?

— David Buik (@truemagic68) September 15, 2014

Too early on Monday to talk #beer ? Nah didn't think so...a deal brewing? Watch SABMiller, Heineken & AB Inbev shares on M&A talk

— Caroline Hyde (@CarolineHydeTV) September 15, 2014

Updated

European markets open lower

As expected, the weak Chinese factory data has hit shares in Europe. The main indices have all fallen in early trading.

-

FTSE 100: down 25 points at 6781, - 0.4%

-

German DAX: down 47 points at 9603. -0.5%

-

French CAC: down 21 points at 4420, -0.5%

-

Spain’s IBEX: down 24 points at 10864, - 0.2%

-

Italian MIB: down 99 points at 20971, -0.5%

Mike van Dulken, head of research at Accendo Markets, says markets are also being hit by geopolitical worries, as Ukrainian troops battle with pro-Russian forces.

He adds that the disappointing data from China is:

...adding to last week’s growth uncertainty and giving PM Li little choice but to stimulate or miss 2014’s growth target even if he has distanced himself from the former of late.

Updated

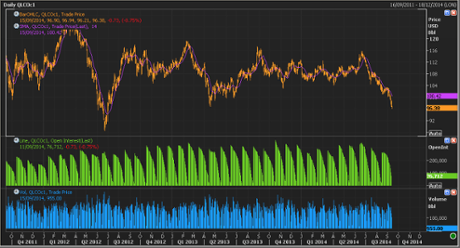

Chart: the falling oil price

As this chart shows, the Brent crude price has fallen by over 15% since June when it hit $115 per barrel.

It’s now hitting levels not seen since the summer of 2012, when the eurozone crisis was raging.

Oil price hits lowest level since June 2012

The Brent crude oil price has hit its lowest level since late June 2012.

Fears that China’s economy weakened in August helped to drive the cost of a barrel of Brent crude down to $96.33, a near 27-month low.

Traders are calculating that Chinese firms may require less energy, if the country’s industrial sector is weakening.

As Ric Spooner, chief market analyst of CMC Markets in Sydney, put it (via Reuters)

“Obviously economic growth in China is one of the key drivers of world growth and generally of oil demand.

As it currently stands, it seems likely that the (oil) demand growth won’t keep up with the growth in supply capacity.”

The oil price is also being pulled down by the strengthening US dollar; the greenback has risen as investors anticipate that the US Federal Reserve could sound hawkish on Wednesday, when it holds its monthly meeting.

Updated

Kevin Lai, senior economist with Daiwa Capital Markets in Hong Kong, was also alarmed that China’s industrial output slowed so sharply last month.

He told Bloomberg:

“This is really bad.

“The economy continues to slow down despite the fact that there has been some policy easing, and the data confirm what import growth has been telling us.”

Australia’s stock market led the fallers in Asia/Pacific overnight, down 1% following the surprise drop in Chinese factory growth:

Capital Spreads trader Jonathan Sudaria says the Chinese industrial slowdown has come at a bad time:

“As if traders didn’t have enough to contend with this week what with the Scottish referendum and the FOMC meeting, China has flapped their hands in the air to remind everyone that they are facing an abrupt slowdown”

Here’s the state of play:

Chinese factory output growth hits six-year low

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, business and finance.

There’s a nervous air in the markets today after China’s industrial sector posted the weakest growth since the financial crisis began six years ago, according to data released over the weekend.

Chinese factory production rose just 6.9% annually in August, a level not seen since March 2009, down from 9.0% in July.

And with retail sales and investment figures also weaker than forecast, there are new fears that China’s economy is slowing faster than official figures show.

Stan Shamu of IG explains:

This reading was the weakest since March 2009, with a big drop off in ferrous metal smelting. This resulted in power and heat production falling 1.7%. In the past, electricity consumption has been used as one of the most accurate indications of activity and this partial read will be a concern.

Growth also slowed in retail sales and fixed asset investment. There will now be plenty of talk around China’s growth target and whether it can be achieved with such mediocre activity.

Most Asian markets have fallen overnight, sending the MSCI index of Asia-Pacific shares down to a five-week low.

European markets are expected to follow, with traders also anxious ahead of the Federal Reserve’s meeting on Wednesday.

Here’s the opening calls:

-

FTSE 100: 6785, -22 points

-

German DAX: 9592, -59 points

-

French CAC: 4417, -25 points

-

Spanish IBEX: 10813, -76 points

-

Italian MIB: 20965, -106 points

In the UK, thousands of staff at Phones 4U face uncertainty after the company announced last night it is going into administration. We should be hearing more from the company today.

Phones 4u goes into administration – with 5,600 jobs at risk

#Phones4U shops to not open this morning as company goes into administration via @SkyNewsBiz http://t.co/WCAw270GZy pic.twitter.com/b2CROt9TUO

— Peter Hoskins (@PeterHoskinsSky) September 15, 2014

We’ll have an eye on the pound, as the Scottish independence battle enters its final few days.

Latest Scottish polls over the weekend lean towards the 'No' camp but still to close to call heading into this Thursday's vote...

— RANsquawk (@RANsquawk) September 15, 2014

Also on the agenda...

The OECD is issuing its latest assessment of the world economy, at 10am BST, ahead of the meeting of G20 finance ministers in Australia this week.

We also get eurozone trade data at 10am BST, and US industrial production data at 2.15pm.

I’ll be tracking all the main events through the day.