The Pension Fund Regulatory and Development Authority (PFRDA) has introduced Retirement Income Schemes (RIS) and new drawdown options under the National Pension System (NPS) to enhance cashflow predictability during the retirement phase and corpus longevity of an NPS subscriber.

The RIS will be a new lifecycle scheme, offering an annual glide path, that will reduce a subscriber’s equity exposure from 35% at age 60 to a floor of 10% at age 75, holding constant thereafter until age 85.

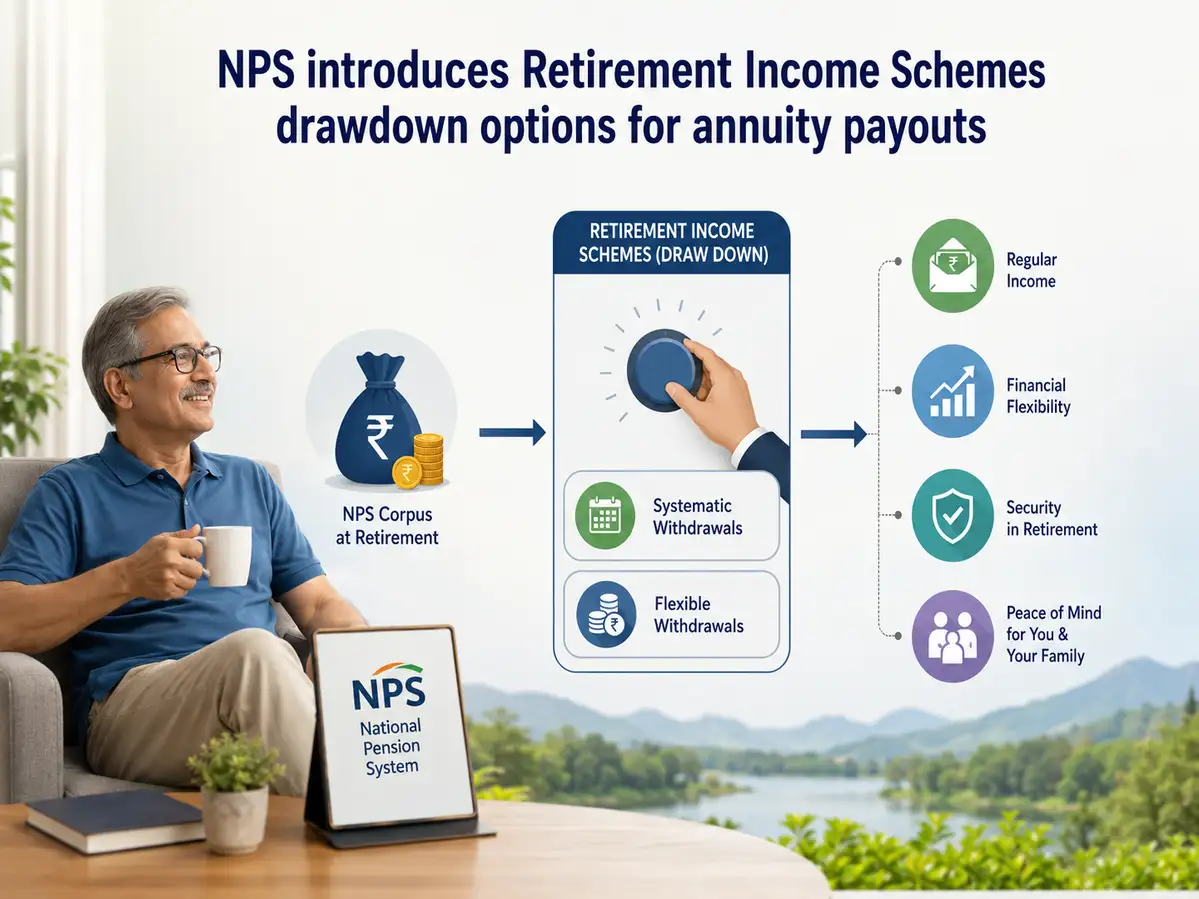

Drawdown options will provide periodic payouts, such as monthly, quarterly, and annually from the lumpsum portion of a subscriber’s corpus. Withdrawals from drawdown options can be made alongside mandatory NPS annuity payouts.

While drawdown options may increase the cashflow of an NPS pensioner, gliding path equity participation may ensure a higher growth of the corpus, says PFRDA in a circular dated May 15, 2026.

However, PFRDA clarified that there will be no guarantee or assurance of a fixed payout under the new schemes and payouts are subject to market risk.

What is the change as PFRDA introduces RIS and drawdown options?

Till now, at retirement, NPS subscribers generally could withdraw up to 60% lump sum tax-free and use at least 40% of the corpus to buy annuity (pension plan). The total lump sum withdrawal allowed in many cases was up to 80% of the corpus for non-government subscribers.

Now, PFRDA is allowing systematic withdrawal-like options where retirees can receive periodic payouts from their NPS lump sum corpus itself. This is while continuing their mandatory annuity payouts.

What is the new Retirement Income Scheme (RIS)?

Under the new system, retirees can choose to withdraw their pension corpus in a phased manner instead of taking the entire lump sum at once. The amount kept under the Retirement Income Scheme will continue to remain invested, allowing subscribers to benefit from potential market growth even after retirement.

“However, these withdrawals will have no impact on the mandatory annuitisation requirement of 20% or 40% of the corpus. This ensures that the minimum statutory requirement for a life-long pension remains intact,” as per the PFRDA circular.

How will Retirement Income Schemes work?

NPS subscribers will have an option called RIS Steady, where their lump sum corpus would be employed in a continuously declining, annual glide path that will reduce equity exposure from 35% at age 60 to a floor of 10% at age 75, and then holding it at the same percentage until age 85.

Payout options available under NPS

Subscribers opting for the drawdown facility can choose how frequently they want to receive payouts. The subscribers will be allowed to receive payouts on a periodical basis viz. monthly, quarterly or annually, for a period up to 85 years of age or as per the choice exercised by them, at the time of their exit from NPS.

Subscribers can opt for any one of the following options for the drawdown-

- Systematic Payout Rate (SPR) (Default)

- Systematic Unit Redemption- SUR-Equal Units

While NPS subscribers opting for the drawdown options can continue with their existing pension fund, they will also have the option to switch their pension fund once in every two financial years.

Calculation of Systematic Payout Rate (SPR) and Systematic Payout

Systematic Payouts (SP) will be a factor of the Systematic Payout Rate applicable at a certain ‘Current Age’ under the SPR option.

The Systematic Payout Rate will be dependent on the drawdown end age and the current age of the subscriber.

Methodologies for Systematic Unit Redemption (SUR)

PFRDA presented it with an example where-

Corpus- Rs 80 lakh

NAV at the time of opting drawdown- Rs 10

Units at the time of opting drawdown- 8,00,000

Age of exit- 60 years

Drawdown period- 25 years

Payout frequency- Monthly, i.e., 12 per year

For such a subscriber,

Number of units per period = The total number of units at start/Drawdown period x payout frequency

Thus, with the figures highlighted in the illustrative baseline, the total number of units to redeemed per month will be as follows

Number of units per month = 8,00,000 25 x 12 = 2666.67 units per month