Angela Merkel’s comments on Greece tonight are being digested by investors; do they make a default less likely?

Greek default probability drops on Merkel remark: Says need to do everything to avoid #Greece running out of money. pic.twitter.com/gjCgZRVcGu

— Holger Zschaepitz (@Schuldensuehner) April 23, 2015

EU summit decides to triple resources to Triton border patrol operation & extend its mandate to respond to distress calls - EU president

— Alan Travis (@alantravis40) April 23, 2015

EU leaders have also committed more resources to border patrols in the Med.

EC president Jean-Claude Juncker wanted more, though.

15 member states have offered new boats and experts to reinforced Triton mission, including UK's HMS Bulwark. Germany offers 11 vessels

— Matthew Holehouse (@mattholehouse) April 23, 2015

Juncker at #EUCO: I'm happy that EU leaders accepted my proposal to triple Trident budget. My proposal 4 legal immigration wasn't supported

— Georgi Gotev (@GeorgiGotev) April 23, 2015

Updated

Angela Merkel is keeping the details of the meeting confidential , alas:

#EUCO Merkel keeps talks with Tsipras "confidential"; says everuthing to be done to prevent a default of Greece

— Mihaela Gherghisan (@GherghisanM) April 23, 2015

Hello again. The European Council summit on migration has ended, so Angela Merkel is holding a press conference.

She’s confirmed that talks with Alexis Tsipras were ‘constructive’, and pointed to Greece’s funding needs:

Germany's Merkel says everything must be done to prevent Greece from running out of money before debt deal can be reached.

— Robert-Jan Bartunek (@RJBReuters) April 23, 2015

Summary: Merkel-Tsipras meeting sets tone for Eurogroup

Time for a quick recap.

Greece’s prime minister has urged the chancellor of Germany to help speed up the negotiations over the Greek bailout, in an attempt to avoid a potentially catastrophic default in the coming weeks.

Alexis Tsipras and Angela Merkel appear to have made some progress, on the sidelines of the emergency EU migration summit , by agreeing that Greece’s primary surplus target should be lowered.

A lower primary surplus target frees up funds for growth-friendly policies, or to undo some of the country’s austerity programmes.

Government MPs have welcomed the news; but Syriza may still face conflict over the bailout negotiations.

Eurozone finance ministers and top Brussels officials are flying to Riga tonight; the Latvian capital will host a Eurogroup meeting tomorrow, where Greece is top of the agenda.

But there’s little hope of a breakthrough before the end of April.

Bond trading giant Pimco reckons there’s a 30% chance that Greece leaves the eurozone. And Citi has warned that Greece could slide into limbo -- or Grimbo, as they dub it.

#Grexit Is So 2012. Citigroup Introduces #Grimbo to crisis lexicon. http://t.co/KYIYNhTjrQ pic.twitter.com/jxy5ihhYqx

— Holger Zschaepitz (@Schuldensuehner) April 23, 2015

These Citigroup guys will never learn #Greece #Grexit #Grimbo #bullshit http://t.co/trxQFuaqaS

— Efthimia Efthimiou (@EfiEfthimiou) April 23, 2015

But other economists think we could see a deal soon, if both sides compromise enough. The big sticking block? Workers’ rights.

CHART:#Greece/creditors ALREADY agree on most structural reforms! Deal reachable if government stops playing politics pic.twitter.com/j1jUHc98Rv

— Maxime Sbaihi (@MxSba) April 23, 2015

In other news....

Germany’s Deutsche Bank has been hit with a record Libor fine, paying $2.5bn for its role in manipulating bank lending rates.

Regulators also blasted Deutsche for obstructing their inquiries, and released details of how traders had conspired to rig Libor rates.

“I’m begging u pleassssssssssssssseeeeeeeeee I’m on my knees” - one of the examples provided by FCA about Deutsche traders lowering Libor

— Jill Treanor (@jilltreanor) April 23, 2015

Private sector growth across the eurozone slowed this month, with France subsiding back into near stagnation. Data firm Markit pinned some of the blame on the Greek crisis.

The news hit European stock markets, with the German DAX and French CAC losing ground.

I’ll pop back into this blog again tonight if there are major developments. But otherwise, I’ll be back tomorrow morning to cover the eurogroup meeting.

Greek MPs cheer signs of progress

Over in Athens tonight, Syriza MPs are welcoming the news that Angela Merkel and Alexis Tsipras have apparently made some progress at their meeting today.

Reports that the two leaders agreed on a reduced primary surplus, of around 1.5%, is being seen as a “huge victory”, even though they’ve not reached agreements on big issues such as labour market reforms.

Helena Smith reports from Athens.

News that creditors had agreed to a substantially lower primary surplus was received with euphoria in parliament where Syriza MPS have been gathering all afternoon. One said it showed Greece was “on the path to overturning the old order.”

Rumours that Athens was close to securing a big cut in the primary surplus formerly demanded of Greece, have been circulating for weeks. Another well-placed government insider declared:

“But this finally confirms it and proves that our partners are at last beginning to see sense.”

The news ironically follows a stormy session of Syriza’s parliamentary group in which MPs had complained bitterly of not being properly informed about negotiations (and the propensity of government ministers to keep their doors firmly shut).

Analysts tonight are saying that the move is clearly aimed at encouraging prime minister Alexis Tsipras to make the boldest move yet: by taking on hardliners in his party now seen as the biggest impediment to reform.

Updated

An update from the FT’s travel correspondent Brussels chief, as European heavy-hitters jet over to the Eurogroup meeting.

I must be on the right flight. @pierremoscovici, @PCPadoan & #Portugal's Albuquerque just boarded behind me. #eurogroup @airBaltic

— Peter Spiegel (@SpiegelPeter) April 23, 2015

And there goes @jvanovertveldt. Is the whole #Eurogroup on @airBaltic 604 to #Riga?

— Peter Spiegel (@SpiegelPeter) April 23, 2015

If only there were some large buildings in Brussels where these meetings could take place....

Updated

#Greece/creditors "have found common ground on the target for the country’s primary budget surplus being set at 1.5%" http://t.co/W4k6kdOIYt

— Maxime Sbaihi (@MxSba) April 23, 2015

Bloomberg has also heard that Angela Merkal and Alexis Tsipras made some progress at their meeting:

Greece and its creditors have found common ground on the target for the country’s primary budget surplus being set at 1.5 percent of economy output for 2015 and also converge on the 2016 target, the official said, without specifying 2016 figure.

The two sides also have converged on privatizations, the official said without providing details.

So, with the two leaders agreeing “in principle” to speed up technical talks, here’s speculation of another meeting of finance ministers soon (as well as tomorrow’s gathering).

#Merkel & #Tsipras agree in principle to speed up Brussels Group talks with view to possible Eurogroup before month's end - @kathimerini_gr

— MacroPolis (@MacroPolis_gr) April 23, 2015

Tsipras and Merkel have agreed that Greece should aim for a primary budget surplus of between 1.2% and 1.5% this year, according to the Kathimerini newspaper tonight.

That counts as progress (reminder, the old bailout deal which the new government rejected set a 3% target)

#Merkel & #Tsipras agree on prim surplus of 1.2-1.5% in 2015/16, privatisation & independence of ELSTAT & revenues gen sec - @kathimerini_gr

— MacroPolis (@MacroPolis_gr) April 23, 2015

BUT they have not solved the other outstanding issues; including how to shake up Greece’s employment market.

But no agreement between #Merkel & #Tsipras on labour market reforms, pension cuts & VAT hikes, gov't sources tell @kathimerini_gr #Greece

— MacroPolis (@MacroPolis_gr) April 23, 2015

Attention is now turning to Riga, the capital of Latvia, where eurozone finance ministers are meeting tomorrow.

The Brussels press pack are jetting off now in -- lets hope airBaltic have stocked up on the inflight drinkies.

For all youze at Justus Lipsius for #EU summit, here's where all the cool kids are headed. #eurogroup pic.twitter.com/P5YbaiAwYu

— Peter Spiegel (@SpiegelPeter) April 23, 2015

You hear a lot about relations between Greece and Germany being strained, with Athens seeking war reparations and many Germans believing Greece should leave the euro.

But Greece’s finance minister, Yanis Varoufakis, has explained today about how German radio kept spirits up during Greece’s military dictatorship.

Writing on his blog, Varoufakis says:

One of the enduring memories from my early childhood is the crackling sound of Deutsche Welle radio transmissions. Those were the bleak years of our dictatorship (1967-1974) when Deutsche Welle was the Greeks’ most precious ally against the crushing power of state propaganda. Mum and dad would huddle together next to the wireless, sometimes covered by a blanket to make sure that nosy neighbours would not get a chance to call the secret police. Night after night these ‘forbidden’ radio programs brought into our home a breath of fresh air from a country, Germany, that was standing firm on the side of Greek democrats. While I was too young to understand what the radio was telling my mesmerised parents, my child’s imagination identified Germany as a source of hope.

As I am writing this preface to the German edition of a book aimed at another child, my daughter, I feel the urgent need to recount that memory. To turn it into a small homage to the idea of Europe as a realm of shared democratic ideals. A small gesture of defiance against the recent tendency for European peoples, who were hitherto coming closer and closer together, to be set apart by a… common currency.

And that’s part of a preface for a German version of a book he wrote, to explain economics to his daughter.

Yanis Varoufakis tells his daughter economics is too important to be left to the economists — http://t.co/qmpFJoY6gG pic.twitter.com/sBu0YmZQon

— Robert Went (@went1955) April 23, 2015

Three months into office, and Alexis Tsipras is sticking to his pledge not to wear a tie until Greece gets a new debt deal with its creditors:

More newsflashes are coming in from Brussels, following Alexis Tsipras’s meeting with Angela Merkel on the sidelines of the summit on migration.

A Greek official is telling reporters that the two leaders agreed that progress is being made between Greece and its creditors.

Importantly, that includes Greece’s primary surplus target -- ie, how much of a surplus (ignoring debt servicing costs) Athens should aim for. The existing bailout calls for a 3% primary surplus; Tsipras’s government want a figures of around 1.5%.

Greek official: Merkel, Tsipras agreed there's progress; Greece, creditors converge on primary surplus target.

— DailyFXTeamMember (@DailyFXTeam) April 23, 2015

Updated

Greek bonds have rallied today, on hopes of a deal.

This has pushed down the yield on its debt -- meaning investors see the bonds as slightly less risky (but still dangerous to own).

Greek yields down quite a bit again today, although remain at very high levels. 10 year 12.30 -55 5 year 17.65 -99½ 3 year 24.99 - 263bp

— Steve Collins (@TradeDesk_Steve) April 23, 2015

Wall Street is shrugging off the Greek crisis.

The tech-heavy Nasdaq index is on track to close at a new record high, beating the previous record set in March 2000 - just before the dot-com bubble burst.

ALERT: Nasdaq rises above all-time closing high. http://t.co/JFwf4VU7yj

— CNBC Now (@CNBCnow) April 23, 2015

Concerns over Greece lingered over Europe’s stock markets again today, pushing shares down across the region.

This morning’s weak PMI surveys, showing weaker than expected growth in Germany and France, also hit confidence.

-

German DAX: down 143 points or 1.2% at 11723

-

French CAC: down 32 points or 0.6% at 5178.

Greek bonds have rallied a little today, though, following reports from Athens officials that a deal could be close.

Investors aren’t convinced, though. Joshua Mahony, market analyst at IG, says:

The widely perceived impending crisis that is Greece took another turn as a Greek government official stated that according to the current rate of progress, a deal would be done by the end of the month.

Unfortunately, for anyone with a memory, this simply reinforces the trend of Greek positivity and disregard for the needs of their creditors, followed by negativity and worry from creditors who repeatedly get their demands rebuffed.

German officials are briefing that Berlin wants to keep Greece in the euro.

But any deal must include detailed, costed economic reforms to make Greece’s public finances sustainable.

One official said:

“At the highest level, the Germans want to keep Greece in the euro area and find a solution, but time is running short and there may have to be more drama before Tsipras can put his foot down and reach an agreement.”

Updated

Alexis Tsipras’s call for negotiations to be accelerated may irk EU officials, who blame the Greek side for the lack of progress this year.

Earlier today, EC vice-president Jyrki Katainen said that trust between Athens and Brussels has been eroded in recent months.

Jyrki Katainen told a press conference in Athens that:

“You cannot negotiate if you don’t trust.

I have to be honest here, it has decreased. It’s not because of the people but it’s very difficult to understand everything, what is going on.”

He was in Greece to promote the EU’s new €315bn investment plan.

Vice-President @jyrkikatainen meets #students in #Greece. #EUdialogues #investEU #Athens pic.twitter.com/T7sIp2FWit

— Ευρωπαϊκή Επιτροπή (@EEAthina) April 23, 2015

"Here in #Greece especially I want to pass my message to private sector: Investment Plan is for you." @jyrkikatainen #SMEs #investEU #Athens

— Aura Salla (@AuraSalla) April 23, 2015

Updated

Here’s Reuters latest story from Brussels.

Greece’s Tsipras urges speeded up process to clinch debt deal

Greek Prime Minister Alexis Tsipras called for a speeding up of the process to conclude a reform-for-cash deal with euro zone creditors after talks with German Chancellor Angela Merkel on Thursday, a Greek official said.

The official said the short meeting on the sidelines of a European Union summit in Brussels - their first since Tsipras visited Berlin on March 23 - took place “in a positive and constructive atmosphere”.

Euro zone officials say little progress has been made in detailed negotiations on a Greek economic reform programme, partly because Athens has denied representatives of its creditors access to state accounting data.

The official gave no details of their discussion but said: “During the meeting, the significant progress made since the Berlin meeting until today was noted. The prime minister asked that the procedures be speeded up so that the Feb. 20 decision, which foresees a first interim agreement by the end of April, be implemented.”

Tsipras pushed Merkel for 'speeded up' process

Alexis Tsipras has ended his meeting with Angela Merkel.

According to Reuters, Tsipras urged the German chancellor to help speed up the negotiations around Greece’s bailout, in an attempt to unlock the €7.2bn of outstanding funds soon.

- BRUSSELS - GREEK PM SAYS AFTER MERKEL TALKS HE CALLS FOR SPEEDED UP PROCESS TO IMPLEMENT FEBRUARY DEBT DEAL

- BRUSSELS - TSIPRAS SAYS TALKS WITH MERKEL TOOK PLACE IN “POSITIVE AND CONSTRUCTIVE SPIRIT”

An official has also told Bloomberg that Tsipras pushed Merkel for an ‘interim’ deal by the end of this month.

*TSIPRAS ASKED MERKEL FOR INTERIM DEAL BY END-APRIL (Bloomberg)

— Alberto Gallo (@macrocredit) April 23, 2015

That would give Greece some of the money it needs to meet its wage and pensions bill on April 30th, and almost €1bn of IMF payments due in May.

Updated

Seasoned euro zone crisis watchers will be aware that today marks the FIFTH anniversary of Athens announcing that it had crashed on the rocks of deficit and debt and had no other choice but to enter an EU-IMF rescue programme, writes Helena Smith from Athens.

The news, broken by the then prime minister George Papandreou on the far-flung Aegean island of Castellorizo, hit the nation with the force of a bomb shell, triggering ferocious protests and riots by Greeks denouncing the painful austerity measures enforced in return for bailout funds.

Interestingly, there has been no mention of the anniversary today - by any political party. Cynics saying it may well be too dark a day to recall.

On this day, 5 yrs ago, PM #Papandreou asked the #EU to bail #Greece out - VIDEO -http://t.co/ZBGNH4C69u pic.twitter.com/NOtLp1d1GA

— enikos_en (@enikos_en) April 23, 2015

#Tsipras #Merkel meeting - perhaps reinforcement of sense that both leaders face v hard decisions/policy alternatives re #Greece?

— Helena Smith (@HelenaSmithGDN) April 23, 2015

Crisis, what crisis?

Angela Merkel and Alexis Tsipras have now met in Brussels to discuss the Greek crisis, and the pair were all smiles (at least for the cameras)

#Tsipras/#Merkel meeting seems to have gone well judging from pix of 2 leaders' body language just released by Greek gov

— Helena Smith (@HelenaSmithGDN) April 23, 2015

Updated

Jürgen Fitschen and Anshu Jain, Co-Chief Executive Officers of Deutsche Bank, just issued a statement on today’s record Libor fine.

“We deeply regret this matter but are pleased to have resolved it. The Bank accepts the findings of the regulators.

“We have disciplined or dismissed individuals involved in the trader misconduct; have substantially strengthened our control teams, procedures and record-keeping; and are conducting a thorough review of the Bank’s actions in addressing this matter.

“This agreement marks another step in addressing the past and ensuring that the Bank earns back the trust of its clients, shareholders and society at large.”

The Greek government has sent some photos over, showing Alexis Tsipras taking an economy flight to Brussels today.

There was still room for an impromptu press briefing...

....and Tsipras did at least bag the window seat. High office does have some privileges, even in a debt crisis....

Updated

German officials say that Merkel will be pushing Alexis Tsipras to speed up the reform process (suggesting she might not appreciate being chivvied by the Greek PM)

Merkel to press #Greece's Tsipras for progress on reforms http://t.co/b9bPfGAVMV

— Efthimia Efthimiou (@EfiEfthimiou) April 23, 2015

Back to Greece....and prime minister Alexis Tsipras has just arrived in Brussels for today’s emergency summit on migration (and a discussion on Greek reforms with Angela Merkel).

Arrival at the European Council #EUCO #Greece #migrationEU #Mediterranean http://t.co/cgvSg9MnvE

— PrimeMinisterGR (@PrimeministerGR) April 23, 2015

Another example of wrongdoing, from the CFTC.

Despite the obvious conflict of interest, Deutsche Bank allowed at times its traders who primarily traded derivatives, such as its Yen derivatives trader, to be responsible for the Bank’s submissions, thus making it easy to skew the bank’s submissions to benefit their own positions and to accommodate the requests of their fellow derivatives traders.

CFTC: How Deutsche rigged Libor

The key to the Libor scandal is that some staff would be taking financial positions on the Libor rate (the official measure of the rates which banks would lend to each other), while their colleagues would be submitting the information used to calculate the rate.

So how did Deutsche Bank take advantage of this?

America’s Commodity Futures Trading Commission says certain Deutsche Bank managers actually encouraged derivatives traders, money market traders, and submitters to conspire to fix the Libor rate.

Some even restructured business lines such that derivatives traders and submitters sat together in the London office.

In this environment, traders often shouted their requests for beneficial submissions across the trading floor to the submitters. A senior manager regularly sat with the traders and encouraged them and their counterparts in other offices to communicate and exchange trading positions, so submitters became clearly aware of the submissions that were most favorable to the various desks’ trading positions.

Senior desk managers in London, Frankfurt, New York, and the Tokyo subsidiary of Deutsche Bank also made requests to benefit their own trading positions, facilitated their traders’ requests for beneficial submissions, and promoted the profit-driven submission practices to help the traders increase profits and minimize losses on their and the desk’s trading positions.

Regulators have also produced evidence of how Deutsche Bank staff conspired to fix the Libor rate by submitting inaccurate information.

One did it for a free coffee, while another pleaded desperately (and irritatingly, frankly) for some help.

“I’m begging u pleassssssssssssssseeeeeeeeee I’m on my knees” - one of the examples provided by FCA about Deutsche traders lowering Libor

— Jill Treanor (@jilltreanor) April 23, 2015

For fixing LIBOR, the price for one Deutsche Bank employee was a mere coffee pic.twitter.com/KgSJAnVPML

— Steve Goldstein (@MKTWgoldstein) April 23, 2015

The NY state fine for Deutsche knows its genre, and that genre is Stupid Typo-Ridden Libor Emails pic.twitter.com/0GOHPWSdXT

— Joseph Cotterill (@jsphctrl) April 23, 2015

Updated

FCA lays into Deutsche over Libor failings

And there’s stinging criticism for Deutsche Bank too; the FCA says it repeatedly misled the regulator over the Libor investigation.

It also warns that the problems at the German bank appear to be “deeply ingrained”.

Georgina Philippou, acting director of enforcement and market oversight, says:

“This case stands out for the seriousness and duration of the breaches by Deutsche Bank – something reflected in the size of today’s fine. One division at Deutsche Bank had a culture of generating profits without proper regard to the integrity of the market. This wasn’t limited to a few individuals but, on certain desks, it appeared deeply ingrained.”

“Deutsche Bank’s failings were compounded by them repeatedly misleading us. The bank took far too long to produce vital documents and it moved far too slowly to fix relevant systems and controls.”

“This case shows how seriously we view a failure to cooperate with our investigations and our determination to take action against firms where we see wrongdoing.”

Deutsche Bank’s (Libor) failings were compounded by them repeatedly misleading us, says FCA

— Jill Treanor (@jilltreanor) April 23, 2015

Deutsche Bank fined $2.5bn over Libor rigging

Breaking: Deutsche Bank has just been hit with a $2.5bn fine for its role in the scandal in which traders manipulated the official interbank lending rates.

Deutsche Bank fined $2.5bn (£1.6bn) for Libor rigging, according to New York Department of Financial Services

— Jill Treanor (@jilltreanor) April 23, 2015

FCA says misconduct involved at least 29 Deutsche Bank employees in London, Frankfurt, Tokyo and New York.

— Jill Treanor (@jilltreanor) April 23, 2015

The penalty includes a £227m fine from Britain’s Financial Conduct Authority -- its biggest ever fine over Libor.

More to follow...

The chief investment officer at bond giant Pimco reckons there’s a 30% chance Greece will exit the euro.

Mihir Worah told reporters today that Grexit could rock the markets, and thus create some tasty buying opportunities:

“We want to reduce our risk and have some dry powder to buy assets in Europe because we think a Greece exit will be volatile,”

“But at the end of the day it’s not going to impact the global economy, it could be a buying opportunity if you’ve got the wherewithal and you’re not in pain yourself.”

#Greece's 5yr default probability drops to 86% as Pimco says 30% chance of a Greek exit. http://t.co/LRUYHbUMlC pic.twitter.com/wVZtimNpOp

— Holger Zschaepitz (@Schuldensuehner) April 23, 2015

A 30% risk is a nice round number; but it’s hard to believe it’s really based on sound maths:

#Grexit probabilities are the most ridiculous figures. Pure cosmetics. Scenarios impossible to quantify with so many (random) parameters.

— Maxime Sbaihi (@MxSba) April 23, 2015

There's a 40% chance this is right https://t.co/lVvjHmCAhi

— Lorcan Roche Kelly (@LorcanRK) April 23, 2015

Two pre-#EUCO meetings scheduled: Merkel-Hollande-Tsipras (on #Greece) and Merkel-Hollande-Cameron-Renzi (on migration). h/t @davcarretta

— Open Europe (@OpenEurope) April 23, 2015

Oh to be a fly on the wall in Brussels today. According to the Kathmerini newspaper, Alexis Tsipras is planning to tell Angela Merkel that he’s compromised, and now it’s her turn.

I did what I said I would. Now it’s your turn to do what you told me,” is the message that the Greek premier was expected to put across to the German leader, according to a top government source, Kathimerini understands.

Athens hopes Merkel meeting can yield a breakthrough

Over in Athens officials are holding out hope that the Greek premier’s meeting with Angela Merkel, on the sidelines of today’s emergency EU migration summit, will help break the deadlock in ongoing negotiations by paving the way to a political solution.

Helena Smith reports from Athens:

In Athens, Paris and Brussels where technical teams have been working feverishly to break the deadlock, there is growing and evident concern that the gridlock in negotiations is going to be hard to break. Ever-shifting deadlines – the next euro group meeting of May 11 is increasingly being seen as the make-or-break date – appear to have given Greek officials little cause for optimism.

Today Kostas Chrysogonos, the prominent Syriza Euro parliamentarian, repeated that a referendum may be the only way out, telling Mega TV that if the talks fail by the cut off date of May 11, a plebiscite should be immediately put to the Greek people.

Athens’s leading negotiator Nikos Theoharakis expressed further pessimism telling reporters in Paris that “the distance between the two sides” was so great only a “political solution” could yield results.

Theoharakis heads up fiscal policy at the finance ministry, so his comments carry plenty of weight.

Helena adds:

In this context today’s meeting between Alexis Tsipras and Angela Merkel could be decisive, analysts say – even if Berlin has gone out of its way to play down the significance of the tête-à-tête. More than ever, the talks will give the Greek prime minister a clearer idea of how much leeway Athens now has given the parlous state of the real economy.

“The meeting is likely to play a major role in the decisions the prime minister will make,” Takis Hadzis, a prominent political commentator told Skai news. On the basis of the talks, Tsipras may well decide whether to call fresh elections or a referendum in the weeks ahead.

Both are being described as potentially catastrophic for Greece’s place in the eurozone by Athens’ political opposition.

We’ve not seen much of Greece’s previous prime minister since January’s election.

But Antonis Samaras has broken cover to warn that the country has now reached “a dead end”, and urge Alexis Tsipras to reach a deal with creditors.

The government has fooled society. At this point it has to clash either with our creditors, or with itself....The country is isolated. If the government does not pay, Grexit returns. There must be a deal.”

Over in Brussels, Greece’s prime minister Alexis Tsipras has confirmed that he’ll meet Angela Merkel on the sidelines of today’s emergency migration summit; and also the French president, Francois Hollande.

During the Summit, I will be meeting with Chancellor #Merkel and President @fhollande #EUCO #Greece

— Alexis Tsipras (@tsipras_eu) April 23, 2015

It’s two months since the three leaders held a special meeting after an EU Summit, that was meant to kick-start negotiations.

Greek bonds are rallying, following that report that a deal is ‘very close’ -- but this still leaves yields at dangerously high levels.

#Greece debt rallying, 3Y -40bps @ 26.57%

— Jonathan Garber (@BondsFx) April 23, 2015

Greece: A deal is very close

Just in: Greek officials are briefing that a deal is “very close”.... and Friday’s meeting of finance ministers could bring it even closer.

*GREECE EXPECTS POSITIVE SIGNAL FROM EUROGROUP MEETING IN RIGA *GREEK GOVT OFFICIAL SAYS DEAL WITH CREDITORS VERY CLOSE

— Bloomberg Markets (@markets) April 23, 2015

Scoop: *GREEK GOVT OFFICIAL SAYS DEAL WITH CREDITORS VERY CLOSE. Gov Official.

— HansNichols (@HansNichols) April 23, 2015

Updated

Bloomberg argues that Greece and its creditors aren’t actually too far from a deal....

CHART:#Greece/creditors ALREADY agree on most structural reforms! Deal reachable if government stops playing politics pic.twitter.com/j1jUHc98Rv

— Maxime Sbaihi (@MxSba) April 23, 2015

Wait. Greece in limbo = "Grimbo"? Stop it, Citi. Just stop it. This is worse than GRIN.

— Katie Martin (@katie_martin_FX) April 23, 2015

Updated

Citi: Get ready for "Grimbo"

I’ve got a personal theory that you can measure the state of the eurozone crisis by the number of ‘catchy’ terms dreamed up by City analysts.

And Citigroup have just added another one to the lexicon -- by warning that Greece risks sliding into a protracted limbo, or “Grimbo”.

In a new note called “Greece: Running Out of Money, Ideas, Time and Patience”, they warn that Greece could potentially stagger on into June without new funds.

They say:

“Over time, the stressed liquidity situation, and notably deposit-withdrawal restrictions for banks, would significantly increase pressure on the Greek government, making fresh elections likely.

Those could produce a mandate for a new bailout agreement with the euro zone or pave the way for an eventual Grexit, but this could still leave Greece in limbo for an extended period of time.”

That scenario looks more and more likely following Valdis Dombrovskis’s warning that technical talks will drag into May (at least).

#Grexit Is So 2012. Citigroup Introduces #Grimbo to crisis lexicon. http://t.co/KYIYNhTjrQ pic.twitter.com/jxy5ihhYqx

— Holger Zschaepitz (@Schuldensuehner) April 23, 2015

Updated

After a steady start, European stock markets have now fallen into the red - not helped by the disappointing PMI data from France this morning.

Wall Street is expected to dip too when it opens in a few hours time.

Equities not looking to good this am DAX - 147 ITALY -242 STOXX -47 FTSE -18 SPX -10.5 DOW -103

— Steve Collins (@TradeDesk_Steve) April 23, 2015

Updated

UK hits deficit target

The ONS has also reported that Britain’s public sector net borrowing requirement (the deficit) fell by 11% in the 2014-15 financial year.

The UK borrowed £87.3bn to balance the books, meaning the government has achieved its target of a deficit of £90bn or below.

That £87bn UK deficit is down £11bn on the year before, say official stats

— Simon Gompertz (@gompertz) April 23, 2015

George Osborne’s original target was to have all-but-eliminated the deficit by this point, of course, a plan that was ditched in 2012 (at which point the economy started to recover again)

Osborne, on @BBCr4today, tries to bluster his way out of basic point: he abandoned his deficit reduction plan (pic) pic.twitter.com/URlrEEL3lP

— Fraser Nelson (@FraserNelson) April 23, 2015

Crumbs. UK retail sales fell by 0.5% last month, dashing expectations of a 0.4% rise.

It’s mainly due to a surprise (and slightly perplexing) slide in fuel sales.

The ONS says:

- On the month, the quantity bought decreased by 0.5% compared with February 2015. The largest decrease was reported by petrol stations which fell by 6.2%.

Monthly UK Retail Sales disappoint UK ONS: On the month, the quantity bought decreased by 0.5% compared with February 2015. #GBP

— Shaun Richards (@notayesmansecon) April 23, 2015

But annual UK Retail Sales growth is still strong UK ONS " increasing by 4.2% compared with March 2014." #GBP

— Shaun Richards (@notayesmansecon) April 23, 2015

And prices continues to fall, suggesting the UK inflation rate may fall into negative territory soon.

Average store prices (including petrol stations) fell for the 9th consecutive month, falling by 3.1% compared with March 2014. The largest contribution to the year-on-year fall once again came from petrol stations which fell by 12.8% and is the 19th consecutive month of year-on-year falling prices in this store type.

Updated

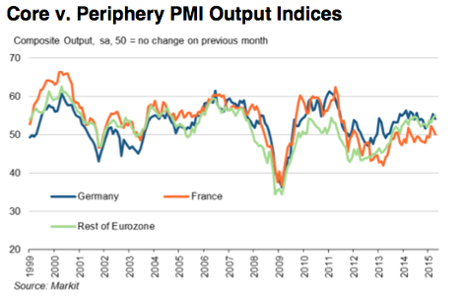

Greek crisis blamed as eurozone growth slows

Private sector growth across the whole eurozone has slowed a little this month, thanks to France’s latest flirtation with stagnation.

Markit’s eurozone composite PMI, which tracks activity across thousands of firms, fell back to 53.3 from 54.0 last month.

#Eurozone growth edges lower at start of 2nd quarter, Comp #PMI Output at 53.5 (54.0 in Mar) http://t.co/T3Z3i8VaIS http://t.co/qUzDuu5efL

— Markit Economics (@MarkitEconomics) April 23, 2015

But firms in the periphery of Europe are powering ahead, with the biggest jump in activity since the credit crunch.

Markit says:

The slowdown reflected weaker rates of expansion in France and Germany, which offset an acceleration of growth in the rest of the region to the fastest since August 2007.

The ongoing Greece crisis may also be causing some firms to rethink their plans, or hold back until it is resolved.

Markit’s chief economist, Chris Williamson, explains:

“There are signs of increased risk aversion creeping in among businesses and their customers, linked in some cases to worries about Greece, which is likely to have dampened demand.

However, in the case of France, the poor performance appears to reflect a longer-term malaise which, after a promising start to the year, in fact shows few signs of lifting.”

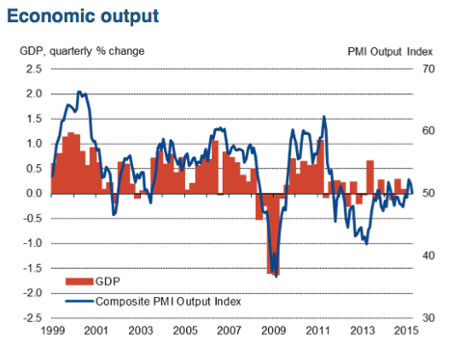

ECB: Europe is gaining momentum

Europe’s economy is ‘turning the corner’, says the European Central bank’s chief economist a few moments ago.

Peter Praet is telling an audience in Berlin that:

The euro area economy seems now to be turning the corner. Both the hard and soft data suggest that the activity is gathering momentum and looks set to strengthen over the course of this year. Consistent with this, all the major forecasting institutions have revised up their expectations for GDP growth in 2015 and the years ahead. We are therefore seeing the beginnings of a cyclical recovery. But it is not yet a structural one.

What I mean by this is that, though the business cycle is improving, the notable decline in euro area’s potential growth rate has not been addressed, which can be imagined as the “speed limit” of the economy – the rate at which it can grow while maintaining stable inflation. International institutions currently estimate the potential growth rate to be below 1% in the euro area, compared with above 2% in the United States...

The solution? Our old friend ‘structural reforms’, to make firms more competitive and productive.

Praet also took a subtle pop at the ECB’s notorious decision to raise interest rates twice in 2011, just as the eurozone crisis was escalating.

The ever polite Peter Praet subtly trolling Trichet pic.twitter.com/meaHNnWaTI

— Jonathan Algar (@jonathanalgar) April 23, 2015

European Commission vice-president Jyrki Katainen is in Athens today, drumming up interest in Brussels’ new €315bn investment plan.

Looks like a nice day for it, too:

Nice start for the #investEU roadshow in Greece. Welcome to #EUdialogues at 11. #Athens pic.twitter.com/a9N6msnKxg

— Jyrki Katainen (@jyrkikatainen) April 23, 2015

That “New Deal” is Commission chief Jean-Claude Juncker’s big idea to pull Europe out of its economic woes; but it’s hard to know what Katainen can achieve in Greece until its funding crisis has been resolved...

The French and German PMI data has sent the euro falling by half a cent against the US dollar.

EUR extends losses to session low after German PMI 1.066 pic.twitter.com/JCPrMCvku6

— Francine Lacqua (@flacqua) April 23, 2015

French Toast German Wurst

— Steve Collins (@TradeDesk_Steve) April 23, 2015

Updated

German PMIs miss forecasts

Just in: Germany’s economy is also performing less well than expected this month.

Activity across German services sector and manufacturing companies is still growing, but at a slower rate.

Germany Manufacturing PMI (Apr) comes in at 51.9 exp 53 Germany Services PMI (Apr) comes in 54.5 at exp: 55.5

— Michael Hewson (@mhewson_CMC) April 23, 2015

(remember, any reading over 50 = growth).

Markit, which compiles the report, says that private sector activity growth in Germany “slowed slightly” this month; again, despite the benefits of cheaper oil and a weak currency.

Let’s not panic; the ‘composite’ PMI is still the second-highest in eight months, at 54.2 down from 55.4 in March. And German companies did report that output and new orders are still rising, but at a slower pace.

But taken with this morning’s disappointing French data, it suggests Europe’s economy is slowing down just when it ought to be picking up pace.

European stock markets are inching higher in early trading, heading back to their highest levels since 2001.

And a French manufacturer is leading the way. Shares in Michelin jumped almost 5%, after reporting a 5.6% rise in first-quarter revenues last night.

That’s partly thanks to the weaker euro boosting overseas sales revenue.

In London, the FTSE 100 is up just 7 points at 7035.

Below consensus services & manufacturing PMI surveys in France. Composite PMI still suggests economy is growing - but v slowly.

— Duncan Weldon (@DuncanWeldon) April 23, 2015

French companies struggle: What the experts say

Bloomberg economist Maxime Sbaihi is disappointed that French factories aren’t taking advantage of cheaper oil prices and a weak currency:

CHART: Ugly French PMIs in April. Manufacturing sector not benefit from lower euro, cheap oil -> Not-so-fast recovery pic.twitter.com/f4o2Ip9v9z

— Maxime Sbaihi (@MxSba) April 23, 2015

Credit Agricole’s Fred Ducrozet, though, is encouraged that service sector firms are more upbeat.

Weak French PMIs, down across the board from already below-average levels.

— Frederik Ducrozet (@fwred) April 23, 2015

Only bright spot in French PMIs: business expectations in services up to their highest level in 3 years; employment up for a 2nd month.

— Frederik Ducrozet (@fwred) April 23, 2015

Updated

The slowdown in French corporate activity suggests the French economy may not grow strongly this quarter:

French private sector growth grinds towards a halt

Hopes that French firms are recovering have just taken a knock, with a survey showing that the private sector slipped back to near-stagnation this month.

That’s according to data firm Markit. Its monthly survey of France’s service sector has dropped to a three-month low of 50.8, near to the 50-point mark separating expansion from contraction.

And the manufacturing PMI fell deeper into contraction territory, down from 48.8 to 48.4.

Flash #France Services Activity Index at 3-month low of 50.8 (52.4 in Mar), Manufacturing #PMI at 2-month low of 48.4 (48.8 in Mar)

— Markit Economics (@MarkitEconomics) April 23, 2015

Jack Kennedy, Senior Economist at Markit, says French companies are still struggling.

“Output growth stuttered almost to a halt in April, signalling a continuation of the moribund economic environment in France.

New business growth weakened despite a further marked fall in prices charged, highlighting the competitive challenge facing French companies. Service providers’ business expectations improved to a 37-month high, although it remains difficult to see much justification for this optimism and sentiment remains historically low.”

Reaction to follow....

Updated

Some early reaction to Dombrovskis’ comments:

#Greece | DOMBROVSKIS SAYS TECHNICAL TALKS WITH GREECE SHOULD BE FINISHED 'BY MAY OR SO' - RTRS ..."May or so" ..so 3 months late

— Ioan Smith (@moved_average) April 23, 2015

Dombrovskis also said that Brussels still reckons Greece will avoid a Grexit:

EUs Dombrovskis tells German TV: "The EU is working on the scenario that Greece will stay in the Euro" but will miss end of April deadline.

— HansNichols (@HansNichols) April 23, 2015

Dombrovskis: Greek talks to finish 'in May or so'

European Commission Vice President Valdis Dombrovskis has warned that Greece is unlikely to hit the latest deadline of a technical agreement with its creditors.

Speaking on the German ARD TV network this morning, Dombrovskis also warned that progress between the two side is ‘not good’.

Reuters have the details:

“We’ve got to conduct the technical talks further and finish them perhaps in May or so,” Dombrovskis told German TV network ARD. He said it is important that all sides, including Greece, stick to their obligations.

He also said: “The talks are going on. Progress is not good.”

April 30 had been inked in as a deadline by Greece’s increasingly exasperated lenders, but progress between the two sides over the details of economic reforms clearly remains slow.

Dombrovskis’s comments means there’s no chance of a reform list being presented to finance ministers in Riga tomorrow, and thus no hope of any cash being extended to Athens.

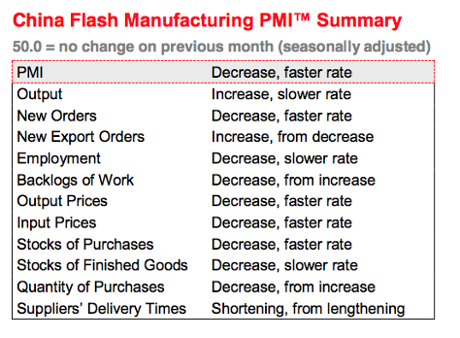

Chinese slowdown fears as factory activity falls

The day has begun with worrying economic news from China, showing that factory activity declined at its fastest pace in a year.

The flash HSBC/Markit Purchasing Managers’ Index (PMI) fell to 49.2 in April, below the 50-point level that shows whether the sector expanded or contracted.

It’s a bigger decline than expected, with Chinese firms reporting that new orders also fell at the fastest rate in 12 months.

And job shedding across manufacturing firms was recorded for the eighteenth month in a row, adding to fears of a slowdown.

#China industr gauge drops to lowest in 12mths, shows China needs to do more to stabilise econ http://t.co/0vX7CJNCCF pic.twitter.com/lUbSxmBDBs

— Holger Zschaepitz (@Schuldensuehner) April 23, 2015

And output and input prices also fell, suggesting deflationary pressures growing:

The Agenda: Eurozone and UK economic surveys

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Coming up today, the usual flurry of chatter and rumours around Greece ahead of tomorrow’s meeting of eurozone finance ministers in Riga.

Greece’s prime minister, Alexis Tsipras, is due to speak with Angela Merkel about the crisis today in Brussels on the sidelines of a summit to discuss Europe’s migration crisis.

Lots of economic data on the agenda. The ‘flash PMI’ surveys showing how the eurozone’s manufacturing and service sector firms are performing this month.

- French composite PMI, 8am BST

- German composite PMI, 8.30am BST

- Eurozone composite PMI, 9am BST

Those surveys will show whether or not the eurozone’s private sector is continuing to grow.

Michael Hewson of CMC Markets explains:

The latest French manufacturing and services PMI numbers are expected to show an improvement to 49.2 for manufacturing from 48.8, and to remain stable at 52.4 for services.

In Germany further improvement is expected for both numbers, to 53 for manufacturing and 55.5 for services.

Then at 9.30am, we get the latest UK retail sales and public borrowing statistics, giving another insight into the British economy ahead of next month’s general election.

I’ll be tracking all the main events through the day.