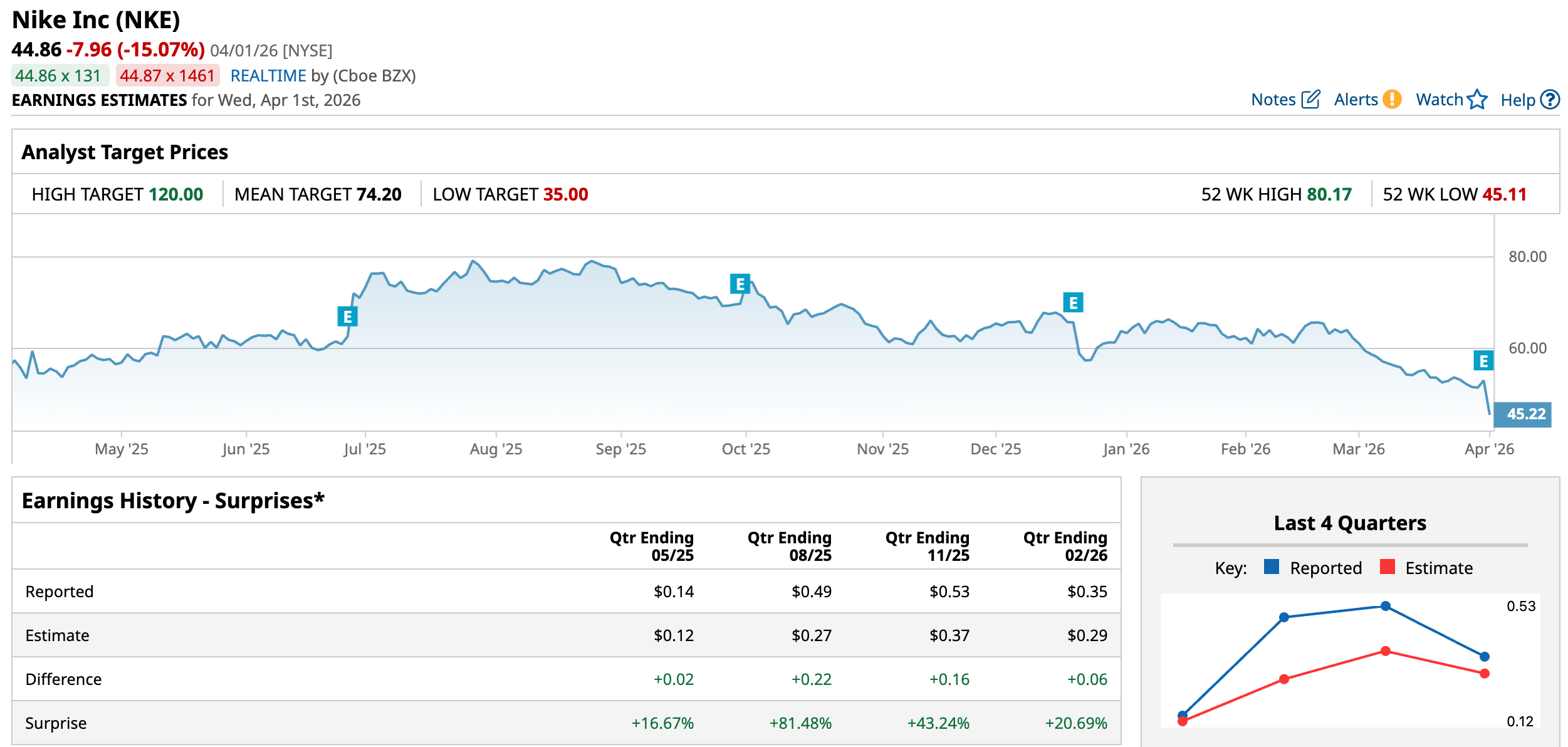

Nike (NKE) released its fiscal Q3 2026 earnings yesterday, March 31, after the markets closed. The stock is trading sharply lower today as the earnings failed to please investors. NKE is having yet another dismal year and is underperforming the markets by a wide margin. Notably, Nike stock peaked in November 2021 but has been sliding since, closing in the red for four consecutive years. The stock is already trading at its lowest levels since October 2017 and looks set to continue its losses even further. Is it time to give up on the sneaker giant after the frustrating underperformance? Let’s explore, beginning with a snapshot of the company’s latest earnings report.

Nike Beat Earnings but Gave a Light Guidance

Nike reported revenues of $11.3 billion for the quarter that ended in February. The sales were flat on a reported basis but fell 3% year-over-year (YOY) on a currency-neutral basis. Its gross margin contracted by 130 basis points to 40.2%, which drove a 35% drop in per-share earnings. Meanwhile, Nike beat on both the top line and the bottom line as markets had quite modest expectations from the company.

However, the earnings beat was more than offset by light guidance. The company expects sales in the current fiscal quarter to fall by between 2% to 4%, while analysts were modeling a low single-digit increase. Nike expects sales to decline YOY in the current calendar year as the top line woes look set to extend. While Nike sees gains in the North America market this year, its Greater China business is expected to continue its downward trajectory.

Nike’s Sales in China Continue To Fall

Notably, China remains a structural headwind for Nike, as not only is that market not growing as fast as it once used to, but Chinese consumers have increasingly been preferring domestic brands over U.S. rivals, from nearly everything, from food chains to cars and smartphones.

In the fiscal third quarter, Nike’s sales in Greater China fell 7%, even as the decline was somewhat lower than Street estimates. In the current quarter, the company expects sales to fall by 20%, though some of the decline is due to intentional actions it took to clean up the marketplace in that region.

Apart from the China sales decline, margin compression has been another recurring story in Nike’s earnings. Several factors have been contributing to this margin contraction. First, a focus on wholesale sales is a likely reason for this erosion, as direct sales are invariably high-margin. Second, the company has had to resort to discounting to clear the marketplace inventory, which has negatively impacted margins. The company’s turnaround costs under the “Win Now” plan have also been taking a toll on profitability, including in the form of severance costs. However, these costs are transitory and would help Nike improve its margins structurally over the long term. Along with these issues, President Donald Trump’s tariffs have been a challenge, and according to Nike, they shaved 300 basis points off its gross margins in the most recent quarter.

To sum it up, Nike’s problems are two-fold. Its sales have been tepid despite its doubling down on wholesalers and third-party retailers, while gross margins have been challenged by multiple factors, most recently tariffs.

Nike Stock Outlook

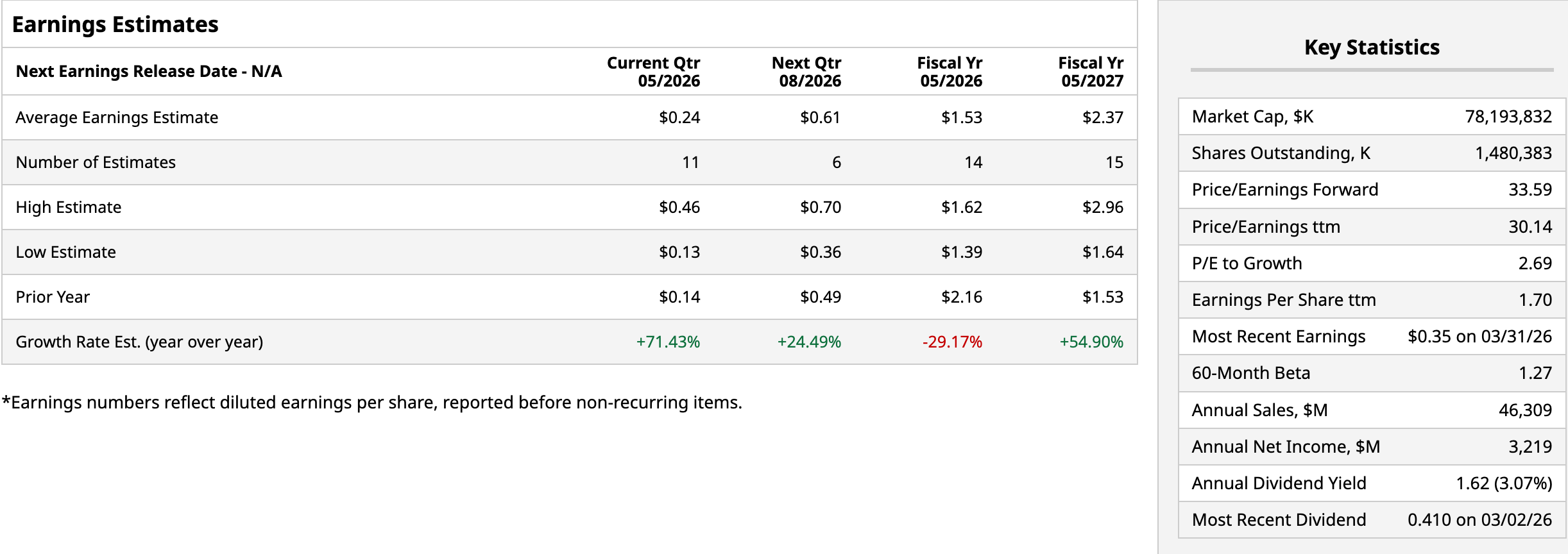

Nike’s turnaround is taking longer than what the markets as well as the company’s management expected. The company is working on reducing aged inventory and is matching supply with demand, and expects these actions to be a headwind to its revenues in the next fiscal year. Consensus estimates call for Nike’s sales to rise at an annualized growth of around 4% over the next two years, but the management’s tone for the next fiscal year sounds a lot more circumspect than Street estimates.

Nike expects tariffs to be a YOY headwind until the first quarter of fiscal year 2027, but is optimistic about an expansion from the second quarter. The company expects its profits to bottom before its revenues as it proactively manages its marketplace inventory. Analyst estimates call for a nearly 55% rise in Nike’s earnings in the next fiscal year.

Should You Buy Nike Stock?

I had been holding Nike stock for the last couple of years on turnaround hopes, but exited my positions earlier this year as the adverse macro environment is making the turnaround harder. Nike still remains one of the iconic brands with a lot of moat, but the company has been gradually losing out to newer brands, both at home and globally.

For now, I would be on the sidelines with Nike as it remains a “show-me” story. However, I would consider buying the shares again if it drops further and the risk-reward gets compelling.