Jerome Powell (see below), a board member of the U.S. Federal Reserve, is set to take over the position of chair from incumbent Janet Yellen in February. Should rate hikes be slowed down in view of the likelihood that sluggish prices will continue for the time being, or should they be accelerated due to worries about overheating the economy? Faced with the reality of opposing policy needs, the new chairman will have to make some difficult decisions.

"I should also thank in advance the creators of all those events ... inflation which always stays put, the stock market which is always a bull, a dollar which is always stable, interest rates which stay low, and employment which stays high," then Chairman Alan Greenspan joked at his swearing-in ceremony in August 1987.

The chair of the Fed is responsible for heading the Federal Open Market Committee (FOMC), which determines the monetary policy of the United States. The committee's decisions affect stock prices, not only in the United States but also abroad, as well as foreign exchange markets.

If not the miracle worker that Greenspan envisioned, the position still requires someone with superior intelligence and grit.

The nickname given to Powell by the U.S. media, however, is "Mr. Ordinary." Powell earned the nickname due to his calm nature and the fact that he eschews actions that attract the attention of the public.

Never once having cast a dissenting vote in the FOMC, he has a reputation as someone who values consensus-building.

When the committee decided to adopt additional monetary easing measures in September 2012, he raised the concern that such a move would elevate future risks but still joined those around him in voting to support it.

Issue of stagnating prices

What this ordinary man faces, however, is an unusual and inexplicable U.S. economy.

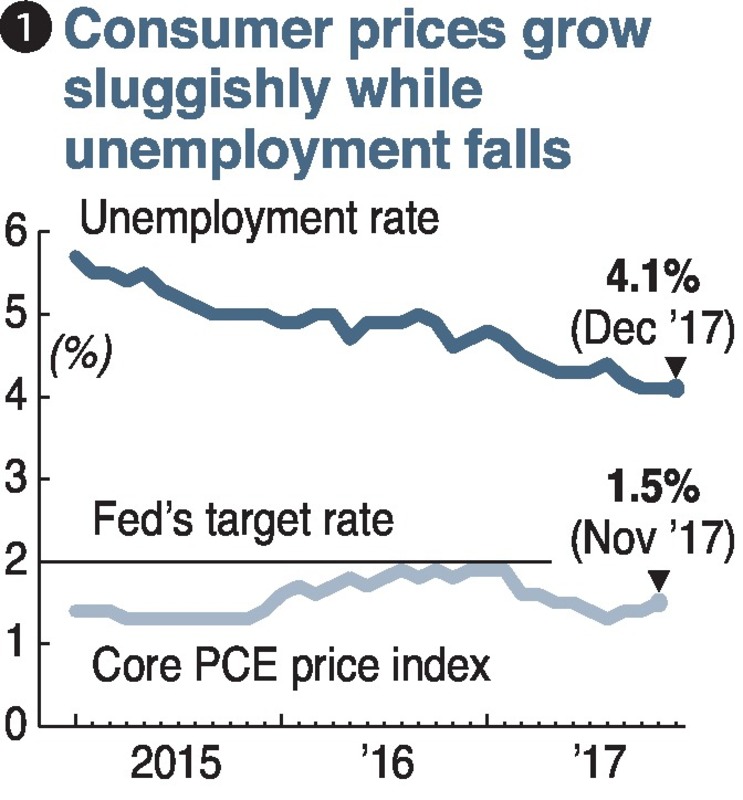

The most vexing issue is that, even with employment increasing, the rate of inflation has not reached the policy objective of 2 percent.

Normally, decreasing unemployment leads to increasing wages, raising purchasing power, which then causes prices to increase.

Currently, however, this normal phenomenon is not occurring, and prices are sluggish (see chart 1).

The rate of unemployment is around 4 percent, a low level also seen just before the so-called Lehman shock in 2008, but price indices remain somewhere between 1 percent and 2 percent.

"Inflation is a little bit below target, and it's kind of a mystery," Powell himself has pointed out.

The Fed has explained the stagnation in prices as a temporary phenomenon due to factors such as lowered mobile phone fees. It is expected to raise interest rates three times this year, assuming that employment will continue to expand and prices will eventually shift to an upward trend.

Recently, however, there is also a viewpoint spreading within the central bank that structural factors such as globalization and the spread of information technology are contributing to the price stagnation.

Imports of inexpensive foreign products, created with low-wage labor, have indeed increased. It has become easier to compare prices on the internet and choose cheaper products.

If such factors are the main reasons behind the stagnation, it is possible that prices will not immediately begin to rise.

Interest rates are raised to prevent prices rising excessively and damaging the economy. Higher interest rates reduce the flow of money and slow economic activity, making it more difficult for prices to rise.

However, if interest rates are raised repeatedly without an increase in prices, economic activity will weaken more than expected and the state of the economy may actually become worse. There will be an increased need to consider slowing or halting interest rate hikes.

Bubble concerns

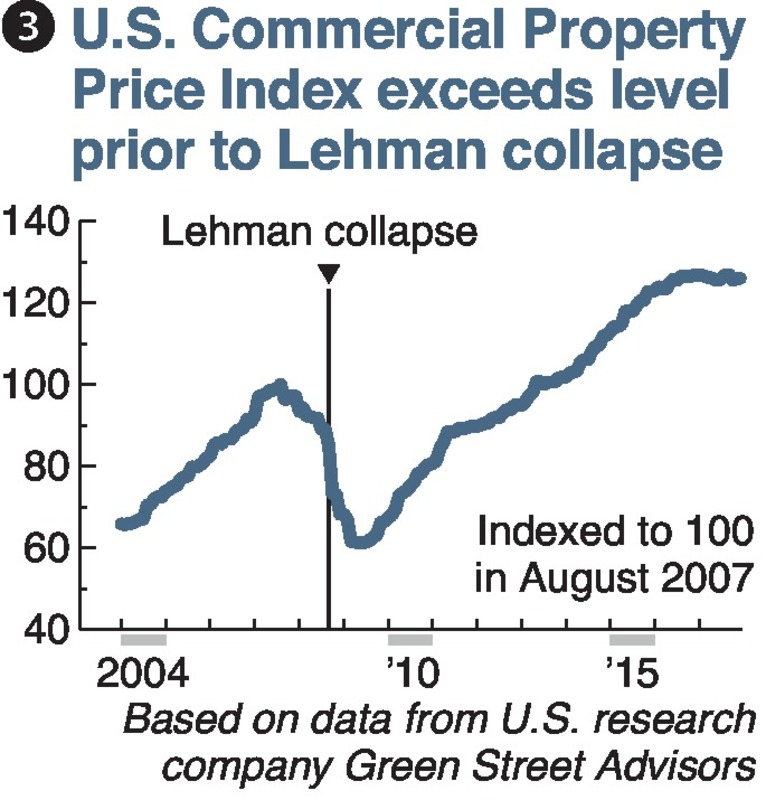

The difficult part is that although prices are stagnating, there are growing concerns about bubbles in U.S. stocks and real estate.

The Buffett indicator (see below) is an indicator widely used to judge whether stocks are overpriced. If the indicator is significantly over 100 percent, prices are considered overvalued (see chart 2).

The indicator currently stands at roughly 170 percent, which exceeds the level seen before the 2008 collapse of Lehman Brothers.

Commercial real estate prices have also risen to approximately 1.3 times their levels prior to the collapse (see chart 3).

It is also possible that large tax cuts will lead to growing expectations of improved corporate performance, accelerating the rise in stock and real estate prices.

If bubble concerns become more prominent, accelerating rather than slowing interest rate hikes will be expected to cool the heat in the markets. However, today's high global stock prices are largely a product of the fact that the Fed has slowly raised interest rates in consideration of the economy.

Caution must be exercised so that accelerating rate hikes do not destroy the favorable environment for stock prices.

Which should be regarded seriously -- the price stagnation or the bubble concerns? The new chairman will need to accurately analyze the actual situation of the economy.

Divided opinions

There is also concern that opinions on policy direction within the FOMC are divided.

Board member Lael Brainard has stated, "We should be cautious about tightening policy further until we are confident inflation is on track to achieve our target."

In contrast, Loretta Mester, president of the Federal Reserve Bank of Cleveland, and some others believe it is desirable to further accelerate rate hikes.

Such conflicts of opinion present a troublesome issue for Powell, to whom consensus-building is important. When necessary, he must firmly dismiss opposing opinions and lead in the direction he thinks is appropriate.

Preserving independence key

It is also the duty of the chair to push aside political pressure and preserve the independence of the Fed.

There are past examples of strong interference from presidents.

In the 1980s, President Ronald Reagan opposed Chairman Paul Volcker's efforts to introduce a monetary tightening policy. The president sent a succession of members who disagreeed with Volcker to the Fed, driving him to resign.

In the 1990s, President George H.W. Bush, in an effort to secure his reelection, pressed Chairman Greenspan for an additional rate cut to stimulate the economy but was refused.

Bush, who was not reelected, later criticized Greenspan, saying: "If the interest rates had been lowered ... I would have been reelected president because the [economic] recovery that we were in would have been more visible ... He disappointed me."

Current President Donald Trump, who comes from the real estate business, has said, "I'm a low-interest-rate person." His thinking is likely that low interest rates enable money to be borrowed more cheaply.

There is a concern that he may put pressure on the Fed if it considers accelerating interest rate hikes.

Powell said he is "committed to making decisions with objectivity and based on the best available evidence, in the long-standing tradition of monetary policy independence." He must firmly adhere to this pledge.

Powell also has another nickname of "owl," which is a symbol of wisdom.

The description spread after a former colleague told U.S. media that Powell is neither a hawk, eager to raise interest rates, nor a dove, emphasizing caution, but a "wise owl."

It is hoped that Powell will steer wise, flexible policy so that the strength of the global economy continues for a long time.

-- Jerome Powell

Born in 1953 in Washington, D.C., Powell has held positions including undersecretary of the Treasury during the George H.W. Bush administration and investment fund partner, before being appointed to the Federal Reserve Board of Governors in 2012. He is unusual for a Fed chairman in that he worked as a lawyer rather than an economist. His assets are estimated to be worth as much as over 6 billion yen, and he is said to be the wealthiest chair since the 1950s.

-- The Buffett indicator

An indicator for assessing overvalued stock prices, espoused by well-known U.S. investor Warren Buffett. It is obtained by dividing total stock market capitalization by the nominal gross domestic product of that country. It is calculated based on the idea that stock prices, which reflect corporate performance, approach a level commensurate with the economic power of a country.

Read more from The Japan News at https://japannews.yomiuri.co.jp/