European markets end on mixed note

Investors remain concerned about a global slowdown and a concurrent US interest rate rise, leaving stock markets in an uncertain mood. Moody’s warning on the knock on effects of slowing growth in China set the tone, along with a weaker than expected rise in the country’s inflation. With Portugal facing new political upheaval and Greece struggling to meet its creditor’s demands, the eurozone crisis was also back in focus. The final scores showed:

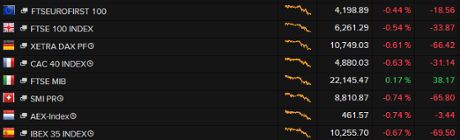

- The FTSE 100 finished down 19.88 points or 0.32% at 6275.28

- Germany’s Dax edged up 0.16% to 10,832.52

- France’s Cac closed up 0.02% at 4912.16

- Italy’s FTSE MIB added 1.52% to 22,444.00

- Spain’s Ibex ended up 0.11% at 10,336.8

- In Greece the Athens market fell 1.65% to 672.19

On Wall Street, the Dow Jones Industrial Average is currently down 25 points or 0.15%.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

New payments for Greece will be released as soon as households’ insolvency issues are resolved; the decision is going to be taken next Monday, said Eurogroup president Dijsselbloem told MEPs.

“The Greek problem will stay with us for many more years but we can cope with that”, he added.

A report on the meeting is here:

Nonperforming loans block the payments to Greece, Dijsselbloem tells MEPs

Outside Portugal’s parliament, demonstrators at an anti-austerity protest by labor groups shouted “Victory!” as the news of the vote spread, reports AP.

Here’s Associated Press:

Anti-austerity lawmakers have forced Portugal’s new center-right government to resign by rejecting its policy proposals.

The showdown comes less than two weeks after the center-right government was sworn in.

The moderate Socialist Party forged an unprecedented alliance with the Communist Party and the radical Left Bloc to get a majority in the 230-seat Parliament and vote down the proposals on Tuesday.

After four years in power the government lost its parliamentary majority in an October 4 general election, which saw a public backlash against austerity measures adopted following a €78bn ($84bn) bailout in 2011.

Socialist leader Antonio Costa is expected to become prime minister in coming weeks, supported by the Communists and Left Bloc. The have promised to alleviate austerity, though critics fear a return to borrow-and-spend policies.

Updated

Reacting to the news from Portugal, Capital Economics said:

Today’s vote of no confidence in the Portuguese Government seems set to usher in a renewed push against austerity and a further rise in bond yields. The one hope is that mounting public resistance to austerity will at some point lead the European authorities to allow a more growth-friendly approach.

#Portugal's political future now hangs on the will of President Cavaco Silva.

— Yannis Koutsomitis (@YanniKouts) November 10, 2015

Portuguese government falls

And the Portuguese government has fallen:

#Breaking #Portugal: Center-right coalition govt falls in parliament. Socialist "motion of rejection" approved by 123 +1 than left majority.

— José Miguel Sardo (@jmsardo) November 10, 2015

Updated

#Portugal: Failure of computer system obliges speaker to ask for vote on "motion of rejection" raw by raw. pic.twitter.com/HkUx5Qz1bX

— José Miguel Sardo (@jmsardo) November 10, 2015

Portugal has begin the vote of confidence in parliament:

#Portugal #Latest: Parliament starts to vote on "motion of rejection" to govt supported by left majority. Live: https://t.co/xVNMm0pAeL

— José Miguel Sardo (@jmsardo) November 10, 2015

#Portugal: PM started his speech as PM and ended as leader of an opposition saying that he'll continue to fight. pic.twitter.com/KYw6VnOWWt

— José Miguel Sardo (@jmsardo) November 10, 2015

Updated

Greek government officials are expressing confidence that the thorniest of all questions dividing Athens from its creditors – the issue of home repossessions - is about to be solved. Our correspondent Helena Smith reports:

Both Athens and its creditors are “very close” to finding the right formula that would protect mortgage holders from losing homes and close negotiations between the two sides. That is according to senior government officials who say foreign lenders are ever closer to agreeing that the ceiling for protecting homes in the event of loan repayment failure should be nearer the €200,000 mark than the €300,000 mark at which it currently stands.

“The goal is to conclude negotiations within the week,” said one high level source insisting that thousands would stand to lose their primary residences if agreement wasn’t reached. “In so far as the first residence is concerned [consensus] is very close to the Greek government’s proposal,” added the official saying both sides had begun to converge on the issue of income criteria and how that would affect foreclosures. If talks were wrapped up this week, the aid disbursement and recapitalization of banks could begin next week, insiders say.

Amid a groundswell of criticism at home and abroad, Greece’s leftist government is keen to put on a brave face. In that spirit, the finance minister Euclid Tsakalotos will address an audience at the LSE tonight with a talk appropriately entitled “Economic blues: the left in government times.” Apparently the interest is such, there is no auditorium big enough to hold the event according to the Hellenic Observatory organising it.

Back with Greece and Klaus Regling, managing director of the European Stability Mechanism bailout fund, has ruled out a haircut or debt relief for the country.

In an interview here he said:

A nominal haircut is certainly not on the cards and the IMF is not proposing it either. In my view, there is also no need for such measures. Let me explain why. Greece today already has benefitted significantly from loans from the ESM and the European Financial Stability Facility (EFSF). We disbursed about €143 billion, which corresponds to 45% of all Greek debt. We did that on very favourable terms. These loans have an average maturity of 32 years and a very low interest rate of currently about 1% because we charge only our own low funding cost.

These generous lending terms save the Greek budget huge amounts of money every year. These gains - in what economists call net present value terms - are so substantial that they are very similar to a haircut from a Greek perspective. If you add up all favourable terms made in the European official lending, the benefit is equivalent to a 50% haircut from a Greek perspective. But this is very different from a nominal haircut. Crucially, our approach neither leads to any loss for creditors nor to any direct transfer from creditors to Greece.

The ESM could improve these financing conditions further provided Greece fully sticks to its reform commitments. For example, we could extend maturities or prolong the interest rate deferral. Member states will look at the reform implementation in Greece and decide whether to engage into discussions on further debt relief. We need to bear in mind that already today Greece’s debt service in terms of gross domestic product is below that of other European countries and there are almost no payments to us until 2023.

He also said:

#ESM’s #Regling: four out of five programme countries are success stories. Greece remains a special case.

— ESM (@ESM_Press) November 10, 2015

#ESM’s #Regling: Greece can only become the next success story if it sticks to the reforms it has committed to

— ESM (@ESM_Press) November 10, 2015

#ESM’s #Regling: Reforms can be painful for countries, but benefits will be tangible and meaningful

— ESM (@ESM_Press) November 10, 2015

#ESM’s #Regling: in return for reforms, countries receive real solidarity from euro area partners

— ESM (@ESM_Press) November 10, 2015

#ESM MD Klaus #Regling speaks at ECON at EU-Parliament along with Eurogroup president @J_Dijsselbloem pic.twitter.com/bzvmvqlZXw

— ESM (@ESM_Press) November 10, 2015

Updated

Trade unions protesting against the austerity measures in Portugal as the government faces a confidence vote in parliament.

Over in Portugal:

#Portugal Communists' De Sousa calls for fall of Passos Coelho gov't. Socialist MPs applaud. pic.twitter.com/nBMUHnew5y

— Yannis Koutsomitis (@YanniKouts) November 10, 2015

Wall Street edges lower

US markets have slipped back in early trading, as the fears of a slowdown in China and the prospect of a rate rise from the Federal Reserve in December dampen investor enthusiasm once more.

The Dow Jones Industrial Average is currently dow 29 points or 0.17%, with Apple down around 2.5% on worries about weak demand for its iPhone 6s. Analysts at Credit Suisse reported that Apple had cut its orders for components by as much as 10%.

Greece’s prime minister Alexis Tsipras has told his cabinet to complete talks with the country’s lenders swiftly this week to allow the release of the latest tranche of bailout money, Reuters is reporting. The two sides have been in dispute over home foreclosures and non-performing loans. Reuters says:

In the first major standoff with lenders since their being re-elected to office in September, Greek officials were told by eurozone finance ministers on Monday Athens would not get any more aid until it implemented a series of reforms, foremost among them being a tighter foreclosures law on problem mortgages.

Tsipras told cabinet it was a “priority” to conclude negotiations this week to allow the disbursement of €2bn in aid, and another €10bn to be released towards the recapitalisation of Greece’s four systemic banks.

“He noted it was a priority to conclude negotiations this week, so as to facilitate approval ...for the disbursement,” a statement from his office said.

Discussions have stumbled on the level of protection Greek mortgage holders should have if they fail to repay their debt.

A government source said that negotiations with lenders were continuing, and there appeared to be a level of convergence emerging.

More on the falling euro:

Divergent EZ/US interest rate exp'ns driving #euro lower. Our rate forecasts suggests more to come. Parity in play. pic.twitter.com/ZB6UP9TBek

— Capital Economics (@CapEconEurope) November 10, 2015

In Portugal, parliament is debating the government’s programme ahead of a confidence vote.

US import prices fell in October by more than expected, helped by the continuing weakness in the crude price and a strong dollar.

They dropped 0.5% compared to expectations of a 0.1% fall and a 0.6% decline in September, itself revised down from 0.1%.

However traders believe this is unlikely to prevent the Federal Reserve from raising interest rates in December, which it seems increasingly keen to do.

The euro has hit a seven month-low against the US dollar, as monetary policy on either side of the Atlantic prepares to diverge.

The single currency has fallen by half a cent this morning, to hit $1.0697. That’s its lowest level since mid-April.

The dollar is buoyant right now, after last week’s strong US jobs report raised the chances that the Federal Reserve hikes interest rates in December.

The euro, though, is weak as investors anticipate fresh stimulus measures from the ECB soon. The political turmoil in Lisbon isn’t helping either.

Richard Perry, sales trader at ETX Capital, says:

The Euro remains weak as Portuguese government bond yields hit a four-month high after the Socialist party reached an agreement with the radical Left-bloc and the Greens on forming a united bloc to try and oust the recently-formed centre-right government.

Essential lunchtime reading: Inside the Bank of England

Few people are ever allowed deep into Britain’s central bank, so my colleagues Larry Elliott and Jill Treanor had a real treat recently when they spent a week inside the Bank of England.

They had remarkable access, from the governor’s “cavernous office” to the bowels of the Bank, its vaults groaning with cash and gold.

They saw how the Bank handles its responsibilities, which have swelled since the crisis, as it tries to avoid missing the next crash or fuelling another bubble.

And they travel with top staff around the country as they assess the state of the economy, and weigh in on the Brexit debate.

Enjoy yourselves:

The wheels are in motion in Portugal, with the opposition left-wing parties preparing to vote down the centre-right government.

#Portugal: Parl speaker has already received 4-left partie's "motions of rejection" to govt. Socialist's 1st & only to be voted from 16hCET.

— José Miguel Sardo (@jmsardo) November 10, 2015

Germany and Greece are at opposite ends of the eurozone spectrum, but they’re both suffering industrial action this week.

Germany’s flagship airline, Lufthansa, has been forced to cancel 136 flights today as a cabin crew strike continues. Workers are protesting about Lufthansa’s attempts to cut pension costs, disrupting tens of thousands of customers.

And the situation is worsening, with unions expanding the walkout to cover the company’s total operation from Wednesday until Friday.

#Lufthansa cabin crews plan full #German network strike 11-13 November

— Peter Hoskins (@PeterHoskinsTV) November 10, 2015

While in Greece, unions are preparing to hold a 24-hour strike on Thursday against the government’s pensions cuts, labour market reforms and other bailout measures. Ferry workers, who downed tools (anchors?) last week have just announced they’ll take part too.

We can expect a protest rally in Athens too.

Updated

Moody’s warning of global shockwaves from China has helped to push shares lower in Europe this morning.

Most of the main indices are down, as traders fret that the world economy isn’t strong enough to handle a US interest rate rise next month (as looks likely).

This morning’s fall in Chinese inflation to 1.3% has also hit the mood in the City, says Conner Campbell of SpreadEX:

Despite starting the day with some mild gains, the wind was taken out of the market’s sail this morning as Moody’s issued an unwelcome reminder about the big trouble in (not so little) China.

Hot on the heels of the country’s inflation slip came a report from the ratings agency that claimed ‘the main risks to the economic outlook are a bigger than expected global fallout from the Chinese slowdown’.

Not necessarily a surprising statement, but given the fact they had already had to endure China’s aforementioned crumbling CPI investors were in no mood for another dour dollop of data reaffirming that the main market-bogeyman is just as terrifying as first thought..

Over in Lisbon, Portugal’s prime minister looks resigned to his fate as MPs debate his government’s programme ahead of this afternoon’s confidence vote.

Political analysts are broadly confidence that a coalition of three left-wing parties will dethrone Passos Coelho.

That alliance could be strained, though, as the Socialist Party, which came second in October’s election, is more mainstream than the two smaller groups:

Why Portugal's new coalition government may not last, in one chart. pic.twitter.com/ga6VU6lsTY

— Mike Bird (@Birdyword) November 10, 2015

Updated

The Greek cabinet has met this morning, to discuss their next move after failing to receive new bailout funds from their euro partners last night.

Alexis Tsipras must now decide whether to agree tougher new rules on defaulting mortgages and other bad loans.

Protests are expected outside the Lisbon parliament today, as the government’s fate is decided:

#Portugal: From 14hCET 2 rival demos will occupy left and right areas in front of parliament: calls for govt resignation vs govt supporters.

— José Miguel Sardo (@jmsardo) November 10, 2015

Portugal’s minority centre-right government could be entering its final act, less than a fortnight after being sworn in.

MPs in Lisbon are now in session, and are likely to vote down the government’s programme later today. A group of left-wing parties, who hold a majority of seats between them, could then form a new government.

#Portugal: Shortest govt ever about to fall at parl tday under left's "motion of rejection" https://t.co/xVNMm0pAeL pic.twitter.com/cO9M2Y2eSP

— José Miguel Sardo (@jmsardo) November 10, 2015

Last night, prime minister Pedro Passos Coelho claimed that an alliance of socialist, communist and other leftist parties would be “ruinous for Portugal”. His centre-right party won the most seats, but was short of a majority.

Updated

Greek banking shares are falling heavily today, after eurozone finance ministers declined to hand over bailout funds last night.

The main Athens stock index has shed 1.5%, led by financial stocks such as Eurobank which has lost almost 20%:

These banks are all due to share in up to €10bn of fresh capital from Europe, but that money won’t be released until Greece has satisfied the remaining ‘milestones’ set with creditors.

Last night, eurozone finance ministers said Athens must complete this task by the end of the week. That means the deadlock over which homes can be repossessed, or foreclosed, from defaulting mortgage holders must be broken fast.

Updated

Reading the IEA report: looks like "peak oil" is almost here. But it's "peak oil demand" not "peak oil supply".

— Duncan Weldon (@DuncanWeldon) November 10, 2015

IEA: Oil price won't hit $80 until 2020

The world’s top energy forecaster has predicted that oil prices will remain below $80 per barrel until the end of this decade, partly due to China’s slowing economy.

In its new annual report, the International Energy Agency predicted that the current glut of oil will probably linger until 2020.

That means the price of crude, currently below $50 per barrel, will only rise slowly in the IEA’s ‘central scenario’.

And China’s slowing economy is one key factor. The IEA says:

The single largest energy demand growth story of recent decades is near its end: China’s coal use reaches a plateau at close to today’s levels, as its economy rebalances and overall energy demand growth slows, before declining.

The watchdog also flags up that the world has made progress towards cleaner fuels, and renewable sources:

There are clear signs that an energy transition is underway: renewables contributed almost half of the world’s new power generation capacity in 2014 and have already become the second-largest source of electricity (after coal).

The IEA also acknowledges that oil demand could be even weaker than its central view, meaning prices stay even lower for longer. That would be welcomed by consumers, but risks “energy-security concerns” by heightening reliance on a small number of low-cost producers. Here’s the full report.

Bloomberg is reporting that three lawsuits have been filed against the European Central Bank in the German constitutional courts.

They apparently all involve the ECB’s quantitative easing programme (under which it is buying government and corporate debt).

We don’t have much detail yet, I’m afraid.

It is presumably tied into concerns that the ECB’s bond-buying programme violates the rules banning monetary financing within the eurozone.

BREAKING: 3 lawsuits targeting the #ECB's QE program filed with the German Constitutional Court. No hearing scheduled yet. #herewegoagain

— Maxime Sbaihi (@MxSba) November 10, 2015

Back in June, Germany’s top constitutional judges approved another ECB bond-buying programme, dubbed OMT, which lets it buy the debt of a eurozone member if it risks being locked out of the financial markets.

ECB threatened with German law suits. So what if ECB don't play ball to any of the outcomes? Send the ECB to prison? Close it? Dont think so

— Polemic Paine (@PolemicTMM) November 10, 2015

Updated

A new Chinese inflation report has also send alarm bells ringing this morning.

China’s consumer prices index rose by just 1.3% annually last month, which is the lowest level since May. That’s another sign that demand is weakening.

Asian markets fell after the data was released:

The copper price highlights why Moody’s is right to be worried about China.

It is hovering around a six-year low today, after trade data released on Sunday showed sharp fall in Chinese imports and exports.

Copper Sinks to Six-Year Low as Chinese Demand Slumps - https://t.co/TbXYQO1Bg4 pic.twitter.com/RlJgPdOt0L

— SoberLook.com (@SoberLook) November 10, 2015

That’s a concern, as copper is seen as a benchmark for the health of the global economy.

Updated

There are some minor shockwaves in the bond markets too, as left-wing parties prepare to take power in Portugal (as explained in the intro).

Portuguese 10-year bonds have hit a new four-month low this morning;, with investors worrying that a new anti-austerity government will soon be pulling the levers in Lisbon.

#Portugal bond rout continues as Portuguese Premier set to be ousted as Socialists eye power https://t.co/gDech0c0eA pic.twitter.com/DXJtN26aN3

— Holger Zschaepitz (@Schuldensuehner) November 10, 2015

Updated

London financial newspaper City AM is alarmed by Moody’s warning:

Commodities slump will hurt poor families

China’s slowdown also means that commodity prices are unlikely to rebound, after slumping to multi-year lows in 2015.

Moody’s says:

A large inventory build-up, a slow supply response and muted demand from China and other key importers will all weigh on prices.

Moody's says #commodity prices are unlikely to rise significantly in the next few years

— Mauro Ippolito (@MauroIppolito) November 10, 2015

And that will ripple into supply chains in emerging markets, and also hurt household income growth in developing nations.

But this isn’t the only reason to worry about emerging markets. Political crises could erupt in Moscow or Rio....

As well as weaker commodity prices, a range of country-specific factors will contribute to lower growth in emerging markets and could lead investors to reassess growth and return prospects in some countries.

For example, political uncertainty will be a negative factor in Brazil and Russia and infrastructure shortages will hamper growth in South Africa.

Updated

Moodys warns of global shockwaves from China

Escalating problems in emerging markets such as China will hold back world growth over the next two years, and could even threaten the stability of the global economy.

That’s the crux of a new report from Moody’s this morning.

The rating agency has warned that global growth will remain relatively weak - seven years on from the financial crisis - hampering efforts to ease the global debt crisis.

And it fears that governments lack the ammunition to fight back if (or maybe when) the global economy hits the rocks again.

There may simply be little little room to manoeuvre with new fiscal or monetary stimulus, given the measures already taken since 2008 and the pressure to cut deficits.

Marie Diron, senior vice-president of credit policy at Moody’s, explains:

“Muted global economic growth will not support a significant reduction in government debt or allow central banks to raise interest rates markedly.”

“Authorities lack the large fiscal and conventional monetary policy buffers to protect their economies from potential shocks.”

Moody’s forecasts that GDP growth across the G20 developed nations will average 2.8% in 2015-17. That’s well short of the 3.8% average recorded in the five years before the global financial crisis.

And the big threat is that China’s economy weakens even faster than expected.

As Moody’s warns:

The main risks to the economic outlook would stem from a bigger than expected global fallout from the Chinese slowdown and a larger impact from tighter external and domestic financing conditions in other emerging markets.

It already expects China’s GDP growth to slow to just under 7% this year, then 6.3% in 2016 and 6.1% in 2017, as Beijing tries to rebalance its economy. If that process falters, the world economy could be in for a nasty shock...

Updated

The Agenda: Austerity problems in Greece and Portugal

Good morning, and welcome to our rolling coverage of the world economy, the financial market, the eurozone and business.

The eurozone crisis is entering another phase this week, with a stand-off between Greece and its creditors and political upheaval in Portugal.

As we covered in last night’s liveblog, Greece has been given one week to push through unpopular rules on non-performing loans. If it doesn’t make it easier to repossess homes from mortgage-holders in default, Athens won’t get €2bn in loans and €10bn to recapitalise its banks.

All sides insisted last night that progress is being made, but it’s an alarming early hiccup for Greece’s third bailout.

The Greek cabinet is due to meet in Athens shortly to discuss the situation.

There will be drama in Lisbon too today, when the parliament votes on the new centre-right government’s legislative programme. Socialist MPs, who won a majority of seats last month, are expected to bring the administration crashing down.

That would allow them to start rolling back some of the country’s tough spending cuts and tax rises.

Crucial vote in #Portugal's parliament on PM Passos Coelho government program. Will the splintered left parties unite in no confidence vote?

— Jens Bastian (@Jens_Bastian) November 10, 2015

It’s not exactly a repeat of Alexis Tsipras’s dramatic surge to power in Greece in January, but certainly a reminder that European-imposed austerity has its limits.

Something for European finance ministers to ponder, as they arrive in Brussels for an Ecofin meeting today:

Agenda highlights of today's #ECOFIN Council: https://t.co/JI3kTKYlM5. #CapitalMarketsUnion #SRM #EMU #BankingUnion #COP21

— EU Council Press (@EUCouncilPress) November 10, 2015

We’ll be tracking all the main events through the day....

Updated