Microsoft’s disclosures about how corporate tech spending is shaping up in 2023 will get close attention as the software giant reports on Tuesday afternoon.

Among analysts polled by FactSet, the consensus is for Microsoft to report December quarter (fiscal second quarter) revenue of $52.99 billion (up 2.4% annually) and EPS of $2.29 (down 7.5%).

Microsoft shares quarterly sales guidance for its reporting segments on its earnings call. For the March quarter, the company’s revenue consensus stands at $52.42 billion (up 6.2%).

Eric Jhonsa, Real Money’s tech columnist, will be live-blogging Microsoft’s earnings report, along with a conference call scheduled for 5:30 P.M. Eastern Time.

Please refresh your browser for updates.

6:41 PM ET: Following some technical issues during the last question (it was about Azure ramps at large customers), Microsoft's call was ended.

Shares are currently down 0.7% after-hours to $240.25. They initially traded higher post-earnings after Microsoft reported fairly good numbers for many of its enterprise-centric businesses, but gave back their gains after the company disclosed on its call that it saw softening business trends in December and guided for its reporting segments to collectively post FQ3 revenue of $50.5B-$51.5B, below a $52.42B consensus. Much of the shortfall stems for the More Personal Computing segment, which remains pressured by weak PC demand.

Azure revenue rose 38% Y/Y in constant currency in FQ2, with Microsoft guiding for a 4-to-5 point sequential slowdown in growth in FQ3. Commercial bookings were up 7% Y/Y, with Microsoft guiding for roughly flat FQ3 bookings growth amid tough comps.

Thanks for joining us.

Correction: Microsoft expects constant-currency Azure revenue growth to slow by 4-to-5 points relative to its exit rate at the end of the December quarter, which was said to be in the mid-30s, rather than from a full-quarter rate of 38%.

6:27 PM ET: A question about Office 365 growth: How much is being driven by seat growth relative to ARPU growth?

Hood says Microsoft is seeing good but moderating seat growth, and that ARPU growth remains strong thanks to E5 plan adoption.

Nadella adds other "per-user" software platforms such as Viva and Power are seeing strong growth.

6:24 PM ET: A question about whether Microsoft can still meet prior guidance for double-digit FY23 revenue growth.

Hood doesn't reiterate the guide. Says Microsoft continues to watch the PC market for signs of improvement. Adds the company's efforts to cut costs are limiting operating margin declines amid top-line pressures.

6:19 PM ET: Nadella asserts usage/engagement for various Microsoft products continue seeing strong growth amid slower deal activity.

Hood adds that Microsoft is often still good demand for product suites, but more deal pressures for standalone product sales.

6:17 PM ET: Microsoft is now close to flat AH, as investors digest the company's FQ3 guidance and demand commentary.

6:15 PM ET: A question about the U.S. IT spending environment.

Nadella says his comments about the spending environment were about global spending. Reiterates Microsoft still expects IT spending to keep growing as a % of GDP, even as it sees some caution and efforts to "optimize" tech spend in the short-term.

6:12 PM ET: First question is about the OpenAI deal and its top-line impact.

Nadella asserts Microsoft thinks AI will be "the next big platform wave," and is looking to integrate it across its solutions. Highlights current AI-based services for the Power platform, GitHub, etc.

6:08 PM ET: The Q&A session is starting. Shares are now up 1.9% AH.

6:08 PM ET: Operating expenses are expected to be up 11-12% Y/Y in FQ3.

Regarding the second half of fiscal 2023, Hood says Microsoft expects decelerating revenue growth relative to the first half. Opex growth is expected to drop to the low single digits in the June quarter. Higher energy costs are now expected to be a smaller headwind than previously expected.

6:05 PM ET: FQ3 segment guidance:

Productivity & Business Processes - $16.9B-17.2B vs. a $16.94B consensus

Intelligent Cloud - $21.7B-$22B vs. a $22.19B consensus

More Personal Computing - $11.9B-$12.3B vs. a $13.43B consensus

Constant-currency Azure revenue growth is expected to decelerate by 4 to 5 points Q/Q. Windows OEM revenue is expected to be down by a mid-30s percentage.

Shares are up 2.9% AH.

6:00 PM ET: Forex is expected lower revenue growth by 3 points and opex growth by 2 points in FQ3 (less than in FQ2).

5:58 PM ET: The Xandr acquisition provided a 6-point boost to search and news ad revenue, which was up 10% in dollars and 15% in CC.

5:57 PM ET: Hood says Devices revenue (down 39% Y/Y) was hurt by "execution challenges" related to new product launches.

5:55 PM ET: Hood says Microsoft exited FQ2 with constant-currency Azure growth in the mid-30s (compares with 38% growth for the full quarter).

5:53 PM ET: Hood is now going over Microsoft's FQ2 segment performance. Notes Office commercial sales continue benefiting from seat growth among SMBs and frontline workers, and from greater enterprise adoption of costlier E5 plans.

5:50 PM ET: Hood recaps Microsoft's FQ2 performance. Notes there was some weakening of business in December, with moderating Azure consumption.

Microsoft has trimmed its AH gains a bit on those remarks: Shares are now up 3.3% AH.

5:48 PM ET: Amy Hood is now talking.

5:48 PM ET: Gaming monthly active users topped 120M.

5:46 PM ET: LinkedIn is said to now have over 900M registered users. Users for the Start feed are said to be up over 30% Y/Y.

5:44 PM ET: Nadella says (amid weak PC demand) time spent per Windows PC remains up 10% relative to pre-pandemic levels. Also says the Azure Virtual Desktop service is seeing strong growth.

5:42 PM ET: Nadella says Teams now has more than 280M monthly active users, while asserting the platform is taking share across every category it participates in. Teams Phone is said to have added more than 5M PSTN seats over the last 12 months.

5:39 PM ET: Power Automate customers are up over 50% Y/Y.

5:38 PM ET: GitHub is said to now be home to more than 100M developers. More than 1M people have used the GitHub Copilot (AI-based code generation) service.

5:37 PM ET: Nadella asserts (following the OpenAI deal) Microsoft has the most powerful cloud-based supercomputer infrastructure for AI workloads. Says Azure ML revenue has risen over 100% Y/Y for 5 quarters in a row.

5:35 PM ET: Nadella says twice as many CPU cores are run on Azure as were run two years ago, and that the Azure Arc hybrid cloud service now has 12K customers (up 2x Y/Y).

5:34 PM ET: Nadella says firms are now "optimizing" their spend after accelerating it during the pandemic, and are exercising caution in an uncertain environment.

5:33 PM ET: Satya Nadella is talking.

5:31 PM ET: The call is starting. Microsoft is going over its safe-harbor statement.

5:28 PM ET: Microsoft's call typically features prepared remarks from CEO Satya Nadella and CFO Amy Hood, after which the execs take questions from analysts. Guidance is shared by Hood towards the end of her prepared remarks.

5:26 PM ET: Hi, I'm back to cover Microsoft's call. Here's the webcast link, for those wanting to tune in.

4:53 PM ET: I'm taking a short break, but will be back to cover Microsoft's earnings call, which is set to kick off at 5:30 PM ET and will include the sharing of the company's quarterly sales guidance.

Shares are up 4.1% AH to $251.90 after Microsoft posted mixed FQ2 results (revenue slightly missed, EPS slightly beat), while reporting 7% commercial bookings growth and 29% commercial RPO (contract backlog) growth.

4:48 PM ET: One other bright spot: Dynamics 365 business app revenue was up 21% in dollars and 29% in CC, as the platform continues taking share among SMBs and midmarket firms. Total Dynamics revenue was up 13% in dollars and 20% in CC.

4:41 PM ET: The Office 365 installed base keeps steadily growing. Office 365 commercial seats were up 12% Y/Y, and Microsoft 365 consumer subs were up 1.9M Q/Q and 6.8M Y/Y to 63.2M.

4:39 PM ET: Free cash flow was down 43% Y/Y to $4.9B, with Microsoft noting it would've been down 16% if not for a one-time tax payment. The company ended FQ2 with $99.5B in cash/equivalents and $48.1B in debt.

4:35 PM ET: $4.6B was spent on stock buybacks in FQ2, even with FQ1.

4:31 PM ET: As a reminder, Microsoft's quarterly sales guide, which tends to have a big impact on how its stock trades the next day, isn't in the earnings report. It'll be shared on the call.

4:29 PM ET: The segment breakdown helps explain why Microsoft is higher post-earnings in spite of a slight revenue miss: The miss was caused by More Personal Computing, which is dominated by PC and consumer-centric businesses that were known to be weak. The two segments dominated by sales of software and cloud services to businesses beat estimates.

4:26 PM ET: FQ2 revenue by business segment:

Productivity & Business Processes (Office, Dynamics, LinkedIn) - $17B, +7% Y/Y and above a $16.79B consensus

Intelligent Cloud (Azure, server software) - $21.51B, +18% and above a $21.43B consensus

More Personal Computing (Windows, Xbox, Surface, ads) - $14.24B, -19% and below a $14.76B consensus.

4:23 PM ET: $6.8B was spent on capex in FQ2, compared with $6.6B in FQ1 and $7.4B a year earlier.

4:21 PM ET: Weighing on EPS some: While revenue grew 2%, Microsoft's operating expenses were up 19% Y/Y on a GAAP basis to $14.9B, and 11% excluding one-time charges.

With Microsoft having slowed down hiring and just announced layoffs, opex growth will likely slow in the coming quarters.

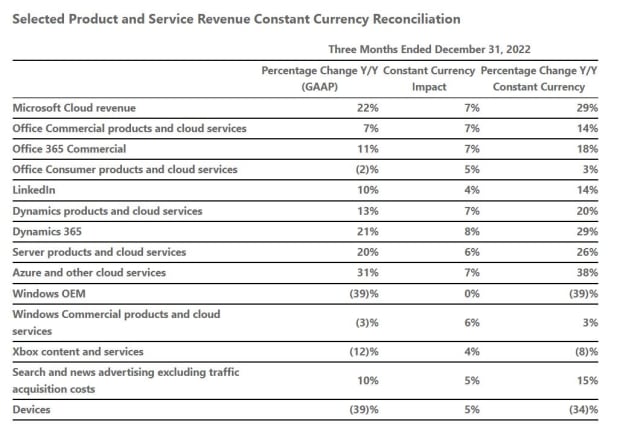

4:16 PM ET: Dollar-based and CC revenue growth for various Microsoft businesses. As the numbers show, forex was a big headwind across the board, and big declines in Windows OEM, Devices (Surface, Xbox, etc.) and to a lesser extent Xbox content/services revenue also weighed on the top line.

On the other hand, Azure, Dynamics, LinkedIn, search/news ads, and server products and cloud services recorded double-digit growth, and Office Commercial grew 7%.

4:09 PM ET: Shares are holding onto their gains: They're now up 4.9% AH to $254.00. Here's the FQ2 report, for those wanting to take a look.

4:08 PM ET: Commercial bookings were up 7% Y/Y in dollars and 4% in constant currency. With bookings up 32% in dollars and 37% in CC a year ago, Microsoft was facing a tough annual comp.

Notably, Microsoft's commercial RPO (contract backlog) was up 29% in dollars and 26% in CC to $189B.

4:05 PM ET: Revenue rose 2% Y/Y in dollars and 7% in constant currency.

Azure revenue rose 31% in dollars and 38% in CC, slightly topping CC guidance of 37%.

4:04 PM ET: GAAP EPS, which bakes in $0.12/share of "severance, hardware-related impairment, and lease consolidation costs," was $2.20.

4:02 PM ET: Results are out. FQ2 revenue of $52.75B slightly misses a $52.99B consensus. Adjusted EPS of $2.32 beats a $2.29 consensus.

Shares are up 4.1% after-hours.

4:00 PM ET: Microsoft's stock closed down 0.2% to $242.04. The FQ2 report should be out shortly.

3:57 PM ET: As usual, Microsoft's Azure revenue growth will be closely watched. In October, Microsoft guided for constant-currency Azure growth (42% in FQ1) to drop about 5 points sequentially.

3:51 PM ET: The FactSet consensus is for FQ2 revenue of $52.99B and EPS of $2.29.

With 2023 IT budgets getting set right now, a lot of attention will probably be given to Microsoft's revenue guide (the FQ3 revenue consensus is at $52.42B), along with its commercial bookings growth and general commentary about corporate spending trends.

3:47 PM ET: Hi, this is Eric Jhonsa. I'll be live-blogging Microsoft's earnings report and call.