European shares suffer mixed fortunes

The euphoria following hints of more QE from the European Central Bank and news of a Chinese interest rate cut has worn off at the start of the new week. Ahead of some key events - UK GDP, the latest US Federal Reserve meeting, eurozone inflation and Apple results - investors turned cautious once more. There was some disappointing economic data, from UK manufacturing to US new home sales, although German confidence figures came in better than expected, enabling the Dax to outperform other stock markets. The final scores showed:

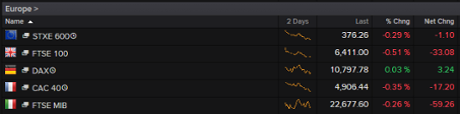

- The FTSE 100 finished down 27.06 points or 0.42% at 6417.02

- Germany’s Dax edged up 0.06% to 10,801.34

- France’s Cac closed 0.54% lower at 4897.13

- Italy’s FTSE MIB lost 0.47% to 22,629.64

- Spain’s Ibex ended virtually unchanged, up 0.02% at 10,478.3

- In Greece, the Athens market added 0.78% to 718.04

On Wall Street the Dow Jones Industrial Average is currently down 22 points or 013%.

On that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

France has reported one of the biggest falls in its jobless numbers since before the financial crisis began.

The number of people out of work fell by 23,800 in September to 3,547,800. This was down 0.7% month on month, but up 3.1% on a year earlier. The number of jobless young people dropped for the fourth month in a row.

In the UK, TalkTalk shares have slumped more than 12% in the wake of last week’s cyber attack on the company.

Since the news was announced that the attack could have led to the theft of personal data from its 4m customers, some £360m has now been wiped off the company’s value.

This was the third data breach to hit the company this year, with investors fearing the attacks would do serious damage to its reputation.

The company could also face compensation claims from customers who have been affected by the data breach.

Despite some differences and more work needing to be done, Greece and its creditors are making progress in talks to allow the country to receive its next batch of bailout funds, Associated Press reported:

Greece and its bailout creditors remain divided over how to toughen foreclosure laws, a European Union official said Monday, though the overall talks on getting the country the next batch of loans are on track.

Valdis Dombrovskis, a European Commission vice-president for the euro, said Greece has already done many reforms, quickly. But he warned “there is no time to lose. There is a need to work very actively to modernize the Greek state and economy.”

There is no time to lose. Lot to do and much effort on-going. Successful 1st review will be a key step for #Greece to return to growth.

— Valdis Dombrovskis (@VDombrovskis) October 26, 2015

Greece has committed to broad reforms, savings and tax hikes to secure its third bailout package from its European partners. Bailout creditors are currently reviewing the government’s compliance with the measures they had agreed upon before paying the country a €2bn loan installment.

Greece is under pressure to lower the income and wealth criteria based on which non-compliant borrowers’ primary residences enjoy protection.

Dombrovskis and the Greek government officials he met in Athens at the start of a two-day visit agreed that differences remain on the issue of foreclosures.

About 40% of all Greek bank loans are now in serious arrears, as successive income cuts over more than five years have left borrowers struggling to repay. At the heart of the issue are housing loans.

The left-led government says it wants protection for borrowers whose homes are worth up to €300,000, and who earn up to €35,000 a year, about 75% of those affected. It says the creditors’ counter-proposal protection for homes worth up to €120,000 would expose nearly 80% of borrowers to the threat of foreclosure.

Dombrovskis said the Commission wants protection limited to households that “clearly” need it. “But there is a clear willingness (on) both sides to find a compromise,” he added.

Government spokeswoman Olga Gerovassili said Athens will fight “all the way” to prevent an explosion in foreclosures.

Spanish prime minister Mariano Rajoy has called a general election for 20 December, in the hope that a recovery in the economy would see his party returned to power. Associated Press reports:

Rajoy said he had fulfilled a promise made on taking office in 2011 by reducing sky-high unemployment and spurring economic growth.

He said the country had gone from being threatened with needing a bailout to one of full confidence among investors and from record unemployment to a situation of job creation.

The ruling Popular Party hopes the recovery will boost its electoral fortunes but polls indicate the party is running neck and neck with the opposition Socialist party and could lose its parliamentary majority.

The polls indicate one of the two main parties will have to do a deal with one of the two newcomers, the centrist Ciudadanos (Citizens) party or the far-left Podemos (We Can) group.

Global markets are edging lower, with the weak US home sales dampening sentiment. But the real market moving events come later in the week. Spreadex analyst Connor Campbell said:

It is likely that today is a mere moment of respite between last week’s market-moving announcements from the European Central Bank and the People’s Bank of China and the wave of important figures and earnings releases still to come before October ends (including the mid-week peak of the latest Federal Open Market Committee statement).

On Tuesday alone there is the preliminary third quarter GDP number for the UK, US consumer confidence and durable goods figures and arguably the most anticipated release of the entire earnings season in the form of Apple’s fourth quarter results.

The Bank of England will not raise rates until the second quarter of next year, according to a poll of economists by Reuters.

This is later than previously thought: two weeks ago in a similar poll, economists believed a rate rise would come in the first quarter.

In this latest survey, the median forecast from nearly 60 economists was for the Bank to raise borrowing costs in April, and even then it is expected to be only a 25 basis point rise. The economists pushed back their forecasts since UK inflation remained stubbornly lower than the Bank’s target.

More mixed US data.

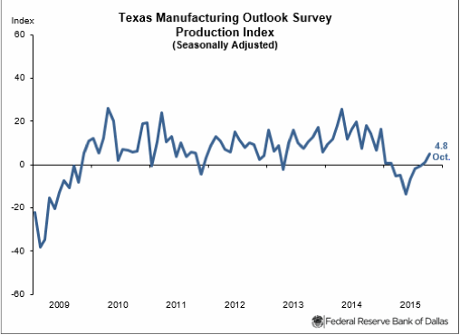

The Dallas Fed manufacturing index of business activity for October has come in at -12.7, compared to -9.5 in September and forecasts of an improvement to -6.5.

But some other indices in the survey moved moved higher. The production index, which the Fed calls “a key measure of state manufacturing conditions”, rose from 0.9 in September to 4.8, the first month of output growth this year.

Updated

The home sales figures have helped push Wall Street lower, with the Dow Jones Industrial Average now down 30 points.

Biggest miss in New Home Sales relative to expectations since August 2013. $ITB $XHB

— Bespoke (@bespokeinvest) October 26, 2015

US home sales drop in September

There are signs that the US housing market may be cooling off.

New single-family home sales fell 11.5% to a near one year low in September after two months of gains, according to the US Commerce Department. The seasonally adjusted annual rate of 468,000 units was the lowest level since November 2014 and well below expectations of 550,000.

August’s figure of 552,000 was revised down to 529,000.

New homes in the northeast slumped by 61.8% to the lowest level since April.

Even if the decline proves temporary, it provides another piece of downbeat evidence for the US Federal Reserve to ponder as it considers whether to raise interest rates this year.

Disruption in new home sales will definitely influence Fed decision on rates.

— Yannis Koutsomitis (@YanniKouts) October 26, 2015

Updated

US will avoid debt default - Moody's

Worries about the US government reaching its debt ceiling if Congress does not vote to raise it seem overdone, according to ratings agency Moody’s. In a new report it said:

Failure to raise the US government’s statutory debt limit before the Treasury has exhausted the “extraordinary measures” that it is using to fund the government’s spending, does not mean that the US is about to default on its debt.

US Treasury Secretary Jacob Lew told Congress earlier this month that the government will have exhausted the measures in place to fund the government by, or around, November 3. Without an agreement to raise the statutory debt limit by then, the Treasury will be forced to begin cutting expenditures to ensure that its spending matches its income.

Moody’s expects that an agreement to raise the debt limit will be in place before the measures are exhausted, and if not by then, certainly before November 15, when the Treasury is scheduled to make interests payments of $35 billion. If an agreement is still not in place by this time, the government could delay other expenditures to ensure it has enough cash to pay bondholders.

“Even if the debt limit is not raised, we believe the government will order its payment priorities to allow the Treasury to continue servicing its debt obligations,” says Moody’s Senior Vice President Steven Hess.

However, the risk that Congress will fail to raise the debt limit in time to prevent this scenario is small, Moody’s says in a report entitled “Debt Limit Deadline Next Week Does Not Imply Debt Default.”

In the unlikely event that an agreement is not reached, Moody’s estimates that total government expenditures would have to be reduced by an average of 11 percent during the fiscal year 2016, so that it can run a balanced cash position. However, on a month-to-month basis, the pattern of revenues and expenditures varies considerably, with five months of the year recording surpluses, while the other months are in deficit. November typically records a fairly large deficit, meaning that during that month expenditures would have to be cut by a larger

Updated

Cautious opening on Wall Street

US markets have opened virtually unchanged, with investors remaining cautious ahead of the latest US Federal Reserve meeting this week. Almost no one expects any movement on interest rates this month - there is no scheduled press conference for a start. But economists will be looking for clues about the Fed’s current thinking as to whether it will move at the December meeting. That debate still seems finely balanced.

Markets are also a little hesitant ahead of a big week for technology company results, including Apple.

So the Dow Jones Industrial is currently down just 9 points. Shortly there are new US home sales and the latest Dallas Fed manufacturing survey.

Updated

Lunchtime summary

Time for a very quick recap:

UK factories have suffered their biggest drop in export orders since 2012. Economists are blaming the strength of the pound, and weakness in emerging markets.

Germany is shrugging off the impact of the Volkswagen scandal. Although business conditions deteriorated this month, executives say they are more optimistic about future prospects.

VW has lost its crown as the world’s biggest carmaker, by sales, to Toyota.

It’s been a subdued morning’s trading in Europe, where China’s interest rate cut has failed to spur much euphoria. The FTSE 100 is now flat, while France’s CAC is slightly lower.

Investors are watching the latest Communist Party Plenum meeting. Officials will lay out a new five-year plan - and perhaps accept that the target of 7% growth can’t be sustained.

As FXTM Research Analyst Lukman Otunuga puts it:

The Chinese five year plan, which is currently being formulated by China’s top leadership, may play down growth targets for 2016-2020, since despite the vigorous efforts of the government the Chinese economy has failed to pick up.

Elsewhere in the City....

Shares in UK telecoms firm TalkTalk have slid by 9% after it was hacked.

Advertising giant WPP lost almost 2%. It warned that business leaders are rather risk averse right now, faced with geopolitical tensions and rising competition from tech upstarts and activists investors.

Alexander Aldinger, senior analyst at Bayerische Landesbank, explains:

“The uncertainty whether the proposed minority government will be tolerated by the parliament had a negative impact on the country’s bonds.”

Portuguese bonds hit by political crisis

Portuguese government bonds are coming under some pressure today as investors react to the unfolding political crisis in Lisbon.

While most eurozone bonds have strengthened today, Portugal has gone the other way, pushing up the yield (or interest rate) on its 10-year debt from 2.37% to 2.45%.

The move came after opposition parties vowed to bring down Portugal’s new government in a confidence vote later this week. They’re furious that the centre-right coalition, led by former PM Pedro Passos Coelho, has been invited to form another administration despite failing to win a majority in this month’s election.

In taking this decision, Portugal’s president Cavaco Silva has enraged some certain commentators who argue that he’s “banned” the Portuguese left-wing a fair crack at power in a massive failure for democracy.

It’s a complicated situation, though. No party won an overall majority, although Passos Coelho’s group came first with 38% of the vote. The socialists came second with 32% followed by the hard left Left Bloc with 10% and the communists with 7%.

Those three left-wing parties *could* form a majority, but instead president Silva passed the mandate to Passos Coelho. Crucially, and controversially, he also warned that the far-left parties’ anti-EU views were a threat to Portugal.

Enough of a threat to block them from power?!

It’s certainly a mess. But politics lecturer Chris Hanretty has written a good blogpost here, explaining why talk of a coup in Portugal is a little simplistic.

He says:

Often, there is no right or obvious answer to the question, “who won the election?”. But if Cavaco Silva’s decision is wrong, then it will be righted automatically by the actions of Parliament in less than a fortnight’s time.

If that happens, the alarmists will have been proven wrong. Unfortunately, attention will likely have moved on.

Very clear & convincing explanation (to me, at least) of what has actually happened in Portugal, by @chrishanretty : https://t.co/NUYGSaG6J5

— Anna H. (@drlangtry_girl) October 25, 2015

RE #PortugalCoup - IT'S NOT A COUP FFS pic.twitter.com/n0BidFjOty

— Joana Ramiro (@JoanaRamiroUK) October 25, 2015

Updated

Sam Tombs of consultancy firm Pantheon Macroeconomic fears that UK factories will continue to struggle because of the strong pound.

He’s created a chart showing how exports fall after the the pound strengthens (the inverted left-hand scale, shifted forwards nine months).

No surprise CBI ITS weak; it always is in Oct. Still conditions in man. are awful; strong £ yet to have full effect: pic.twitter.com/wcGGQ3FPGg

— Samuel Tombs (@samueltombs) October 26, 2015

And that correlation means factory orders could continue to weaken, Tombs explains:

The chart shows that the worst is not over for the manufacturing sector; sterling’s further appreciation over the last year will continue to depress export orders until mid-2016, at least.

IHS economist Howard Archer is alarmed by the drop in UK factory orders reported by the CBI:

This is a thoroughly disappointing survey through and through which indicates that manufacturers’ struggles are intensifying as a moderation in domestic demand adds to a still weakening export outlook.

Persistent and seemingly deepening manufacturing weakness is very worrying for hopes that UK growth can ultimately become more balanced and less dependent on the services sector and consumer spending.

Factory fears as UK exports fall at fastest pace since 2012

More signs that UK manufacturers are having a tough time as they contend with China’s downturn and a stronger pound.

The latest survey of factory bosses by business group CBI suggests orders have dropped from both within the UK and outside. The report’s key order book balance is the weakest for more than two years.

This does not bode well for official GDP figures due on Tuesday that will give the first snapshot of UK growth in the third quarter. The consensus forecast is for quarterly growth of 0.6% in the July-September period, down from 0.7% in the second quarter, according to a Reuters poll.

The CBI’s report suggests that in the three months to October new export orders fell at the fastest pace in three years. That was possibly down to the continued strength of the pound, which makes UK goods more expensive to overseas buyers, the CBI said.

Total new domestic orders fell over the quarter for the first time since April 2013.

Manufacturing production also edged downwards during the three months to October, marking the first decline in the last two years, according to the CBI Quarterly Industrial Trends Survey.

Against that backdrop, manufacturers’ optimism about both their business situation and export prospects for the year ahead fell at the fastest pace since October 2012, according to the poll of 463 companies. But they predicted that overall manufacturing conditions will stabilise in the next three months, with a small rise in output.

Rain Newton-Smith, CBI director of economics, says UK manufacturers are being buffeted at home and abroad.

“Manufacturers have been struggling with weak export demand for several months, because of the strength of the pound and subdued global growth. But now they’re also facing pressure back home as domestic demand is easing.”

And here are the key figures from the report:

- 22% of businesses reported an increase in total new order books and 30% a decrease, giving a balance of -8%, the lowest since October 2012.

- 20% of businesses reported an increase in domestic orders, with 31% noting a decrease. The balance for domestic orders (-11%) was below the long-run average (-5%), the lowest since April 2013 (-14%).

- 15% reported an increase in export orders, with 33% signalling a decrease. The resulting balance for export orders (-17%) signalled a faster decrease in orders than the historic average (-7%). This marks the lowest rate since October 2012 (-17%).

Germany’s central bank reckons that the country’s economy remains “quite strong”, despite signs that growth slowed in the last three months.

Bundesbank monthly report (Oct): Despite slower Q3, German economic growth is quite strong.

— pau fernandez (@0128paufer) October 26, 2015

Former hedge fund boss Magnus Peterson has just been banned from the City, over one of the biggest rogue trading scandals of recent years.

Peterson’s Weavering Macro Fixed Income Fund collapsed in 2009, costing investors around £350m. It had been marketed as a safe and secure investment, which investors could easily reclaim their funds from.

But once the financial crisis struck, Peterson embarked on a series of risky wagers on financial derivatives which failed to reverse its fortunes. He was convicted of several counts of fraud, after the high court heard how he had taken out $600m of swap contracts, which turned out to be worthless, with another company under his control.

Mark Steward, director of enforcement and market oversight at the FCA, says Peterson has been banned to protect consumer and markets.

“Mr Peterson defrauded investors who should have been able to trust him. Over a prolonged period he purposely used investors’ money to prop up his business, and then lied in order to cover up his deception.”

This makes little practical difference to Peterson, aged 51, right now, as he was jailed for 13 years in January.

Updated

9% hacked off TalkTalk shares after cybercrime attack

Back in the City, UK telecoms group TalkTalk is the biggest faller on the stock market after suffering a major cybercrime attack last week.

TalkTalk shares have slumped by around 9.5% this morning. Last week, the firm admitted that customers’ personal and financial details could have been stolen by cybercriminals who breached its security systems.

TalkTalk boss Dido Harding told my colleague Josh Halliday last night that it’s too early to say if the company will compensate those affected.

She also argued that TalkTalk’s security was better than its rivals, despite the breach:

“Nobody is perfect. God knows, we’ve just demonstrated that our website security wasn’t perfect – I’m not going to pretend it is – but we take it incredibly seriously.

“On that specific vulnerability, it’s much better than it was and we are head and shoulders better than some of our competitors and some of the media bodies that were throwing those particular stones.”

And despite criticism from shareholders, Harding is determined to hold onto her job:

Front page of @CityAM today may be @Hariboconomics' finest hour. pic.twitter.com/Ay3ZCSr5Xd

— Mike Bird (@Birdyword) October 26, 2015

Updated

IFO: German car industry unfazed by VW scandal

IFO economist Klaus Wohlrabe has confirmed that Germany’s auto industry is shrugging off the revelations that VW deliberately cheated on emissions tests.

Speaking to Reuters about today’s IFO report, Wohlrabe pointed out that business expectations and the assessment of current conditions in the sector had both improved this month.

That helped to push IFO’s measure of business confidence higher this month, from 103.3 to 103.8.

Wohlrabe says:

The German automobile industry appears to be unfazed by the VW scandal.

Updated

German business leaders aren’t frightened by the crisis at Volkswagen, and the slowdown in emerging markets, explains Carsten Brzeski of ING.

Here’s his analysis on today’s IFO report:

Surprised but not frightened? German businesses showed an interesting reaction to the recent series of uncertainties and turmoil. In fact, the reaction can be summarized as impressed but not frightened.

Germany’s most prominent leading indicator, the just released Ifo index dropped to 108.2 in October, from 108.5 in September. The first drop since June this year. Interestingly, the drop was exclusively driven by a weaker assessment of the current situation. The expectation component, on the other side, increased to 103.8, from 103.3, continuing its recent positive trend and actually reaching the highest level since June last year.

Of course, one should not interpret too much in a single confidence indicator but today’s Ifo reading suggests that the German business community is filing the Volkswagen scandal as a one-off and also shrugs off the risk from a possible Chinese and emerging markets slowdown. Despite these external uncertainties and regular concerns about the real strength of the German economy, German business remain highly optimistic.

There are two possible explanations for this trend: either German businesses are naive optimists or ice-cold realists, sticking to the facts. In our view, there are many arguments in favour of the latter.

Suprised but not frightened? Quick take on today's Ifo index. https://t.co/GgnAev19aS

— Carsten Brzeski (@carstenbrzeski) October 26, 2015

Updated

The euro is slightly higher following the IFO survey:

#BREAKING German Oct IFO confidence 108.2 Vs est 107.8 pic.twitter.com/JE4YZ7f4kW

— Jonathan Ferro (@FerroTV) October 26, 2015

Updated

German IFO survey: What the experts say

Today’s German business confidence survey shows Europe’s powerhouse economy remains in decent health, say City experts.

Economist Frederik Ducrozet is encouraged by the rise in business expectation this month:

German IFO expectations - one of the most reliable forward-looking indicators - rose for the 2nd consecutive month in October.

— Frederik Ducrozet (@fwred) October 26, 2015

Separate IFO index for services set a new record high in October. Best summary of the state of the German economy. pic.twitter.com/BrkWVymQQ5

— Frederik Ducrozet (@fwred) October 26, 2015

Die Welt’s Holger Zschaepitz points out that confidence in the German carmaking industry rose this month:

#Germany's Ifo: Volkswagen scandal no impact on German Auto industry. Business climate in Auto industry rose in Oct. pic.twitter.com/RTDhUHvjeM

— Holger Zschaepitz (@Schuldensuehner) October 26, 2015

Bloomberg’s Maxime Sbaihi points out that demand within Germany is still robust:

Resilient IFO survey minimizes downside risks on German outlook. Current assessment down but expectations up. Domestic factors remain strong

— Maxime Sbaihi (@MxSba) October 26, 2015

Updated

German business climate worsens, but expectations rise

Business conditions in Germany have fallen this month, according to the latest survey of corporate confidence in Europe’s latest economy.

The IFO thinktank has just reported that current conditions in the German economy have deteriorated this month, for the first time in four months.

But IFO also found that business leaders are more upbeat about future prospects than in September. That suggests the VW emissions scandal has not caused major trauma.

IFO’s business climate index fell to 108.2 in October, down from 108.5 in September, but rather higher than expected.

The current conditions index fell to 112.6, from 114 a month ago. That suggests that business leaders are finding life a bit harder -- after seeing exports and factory orders deteriorate over the summer.

But the expectations index rose to 103.8, from 103.3, indicating that Germany PLC expects to ride out the slowdown in China and other emerging markets, and the Volkswagen saga.

#Germany surprises on the upside: Oct Ifo business climate drops less than exp to 108.2 from 108.5; Forecast 107.8, shrugged off VW scandal.

— Holger Zschaepitz (@Schuldensuehner) October 26, 2015

I’ll mop up some reaction now...

Updated

Speaking of carmakers...Japan’s Toyota has overtaken Germany’s Volkswagen to become the world’s largest carmaker.

Toyota has reported that it sold almost 7.5 million cars in the third quarter of 2015, while VW sold 7.43m.

Does that show that the diesel emissions scandal has hurt VW? Not really -- that news only broke in mid-September, giving little opportunity for it to show up in these figures.

But it does show that VW may already have been finding life tougher, even before admitting that around 11 million vehicles were sold with software to trick emissions tests.

Shares in French carmaker Peugeot are down 2% this morning, after reporting a 4.4% drop in sales in China and South East Asia.

That took the shine off a 3.8% rise in sales in Europe.

WPP: business leaders remain 'risk averse'

Advertising titan WPP is among the biggest fallers in London, down around 2%, despite reporting a 3.3% rise in net sales in the last six months.

Traders may be discouraged by a warning that “risk averse” business leaders are reluctant to stick their necks out too far, given the current geopolitical tensions.

WPP told shareholders that:

Country specific slowdowns in China and Brazil and geopolitical issues remain top of business leaders’ concerns. The continuing crisis in the Ukraine and consequent bilateral sanctions, principally affecting Russia, continued tensions in the Middle East and North Africa and the risk of possible exits from the European Community, driven by further political and economic trouble in Greece, top the agenda.

Corporate bosses are also facing a two-pronged squeeze -- from new technology rivals on one side, and cost-cutting activists on the other, WPP added:

If you are trying to run a legacy business, at one end of the spectrum you have the disrupters like Uber and Airbnb and at the other end you have the cost-focused models like 3G in fast moving consumer goods, and Valeant and Endo in pharmaceuticals, whilst in the middle, hovering above you, you have the activists led by such as Nelson Peltz, Bill Ackman and Dan Loeb, emphasising short-term performance.

Not surprising then, that corporate leaders tend to be risk averse.

European markets in muted mood

As predicted, Europe’s stock markets have fallen into the red this morning.

The FTSE 100 has shed arounds 33 points, or 0.5%, as Tony Cross of Trustnet Direct, explains:

It has been a surprisingly muted overnight session in Asia with markets showing little reaction to Friday’s rate cut news out of China.

London’s FTSE-100 is failing to find any inspiration off the back of the news either, with the vast majority of stocks mired in red ink shortly after the open.

The other main markets are also down, apart from Germany’s DAX which is flat.

Mining and energy stocks are generally lower, showing that concerns over global growth haven’t gone away.

Connor Campbell of SpreadEx says:

The FTSE, falling by around 25 points soon after the bell, was weighed down by (what else?) its mining and oil stocks, with investors seemingly less sure about the Chinese rate cut than they were last Friday

Larry Elliott: Why China's interest rate cut may be bad news for the world economy

By cutting interest rates, China’s central bank risks creating further instability in a global economy that is already hooked on ultra-cheap money and regular hits of stimulus.

As our economic editor Larry Elliott explains, such stimulus measures may already be less effective too:

Problem number one is that by deliberately weakening their exchange rates, countries are stealing growth from each other. Central banks insist that this does not represent a return to the competitive devaluations and protectionism of the 1930s, but it is starting to look awfully like it.

Problem number two is that the monetary stimulus is becoming less and less effective over time. There are two main channels through which QE operates. One is through the exchange rate, but the policy doesn’t work if all countries want a cheaper currency at once. Then, as the weakness of global trade testifies, it is simply robbing Peter to pay Paul.

The other channel is through long-term interest rates, which are linked to the price of bonds. When central banks buy bonds, they reduce the available supply and drive up the price. Interest rates (the yield) on bonds move in the opposite direction to the price, so a higher price means borrowing is cheaper for businesses, households and governments.

But when bond yields are already at historic lows, it is hard to drive them much lower even with large dollops of QE. In Keynes’s immortal words, central banks are pushing on a piece of string....

Here’s Larry’s full analysis on the rate cut:

Copper, a classic measure of the health of the global economy, hasn’t benefitted much from China’s rate cut. It’s only up by 0.2% this morning.

China's surprise rate cut sent emerging-market stocks higher, while copper was little changed on growth concerns. pic.twitter.com/XICaKZx2F3

— Francine Lacqua (@flacqua) October 26, 2015

Chinese officials to agree next five-year plan

China is also in the spotlight today as top communist officials gather to hammer out its 13th five-year plan, setting the country’s economic programme until 2020.

Premier Li Keqiang has already indicated that slower growth is on the agenda, by declaring that Beijing will not “defend to the death” its target of 7% growth (which was narrowly missed in the third quarter of 2015).

He declared:

“We have never said that we should defend to the death any goal, but that the economy should operate within a reasonable range.”

Trade links and green issues will also be discussed, as China’s top brass try to manage the country’s economic rebalancing.

China’s leaders gather in Beijing this week to formulate the 13th five-year plan pic.twitter.com/Qx4ap6rTGL

— Francine Lacqua (@flacqua) October 26, 2015

With China easing monetary policy last week, and the ECB expected to follow suit in December, it could soon be Japan’s turn to stimulate its economy again....

Nikkei ends up 0.7% at 18947.12 as #China and #ECB pave way for more easing by Bank of #Japan. pic.twitter.com/cB4i8KZ2HE

— Holger Zschaepitz (@Schuldensuehner) October 26, 2015

No jubilation in Hong Kong either, where the Hang Seng index just closed 0.2% lower.

Asian market creep higher after Chinese rate cut

Investors in Asia have given China’s interest rate cut a cautious reception overnight, but there’s no sign of euphoria.

In Shanghai, the main index of Chinese shares rose by just 0.5%, or 17 points, to 3430. Although Friday’s stimulus move has been welcomed, traders are also worrying about whether China is still going to suffer a hard landing.

Gains in shares fading after China boosts stimulus. Barclays& @blackrock say measures underscore economic weakness pic.twitter.com/QnFER9RlOK

— Caroline Hyde (@CarolineHydeTV) October 26, 2015

Said Zhang Qi, an analyst at Haitong Securities in Shanghai, says shares got a small lift from the rate cut:

“But the market appeared to be in correction after it rose a lot in October, and some investors sold stocks on the short-lived rise from the rate cuts. So overall, the market stayed stable today.”

Japan’s Nikkei gained around 0.7%, but the Australian S&P market dipped a little despite hopes that its mining sector would benefit from Chinese stimulus moves.

Updated

The agenda: Investors await German confidence figures

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Today we’ll find out whether business confidence in Germany has been badly hit by the Volkswagen saga, and the slowdown in emerging markets.

The latest IFO survey, due at 9am GMT, is expect to show that German firms are gloomier about their prospects. That’s understandable, given the drop in German exports, factory output and orders in August.

We’ll also be mopping up the reaction to China’s interest rate cut, announced late last week.

That did give shares a boost on Friday afternoon, but European stock markets are tipped to fall back this morning, as concerns over the situation in China reemerge.

Our European opening calls: $FTSE 6427 down 17 $DAX 10798 up 4 $CAC 4920 down 3 $IBEX 10488 up 12 $MIB 22720 down 16

— IGSquawk (@IGSquawk) October 26, 2015

China’s rate cut came just a day after the European Central Bank hinted that it could boost its stimulus package soon, so investors have lots to ponder.

China cuts interest rates in surprise move - as it happened

In the corporate world, traders are digesting results from advertising giant WPP and French carmaker Peugeot.

And we’ll also be keeping an eye on Portugal, where the president has dramatically asked centre-right leader Pedro Passos Coelho to form another government, rather than two eurosceptic left-wing parties.

Portugal Government Fuels Debate About Democracy in Europe

We’ll be tracking all the main events through the day.....

Updated