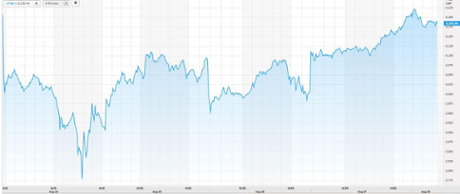

FTSE recoups Black Monday losses but worst month since 2012

The FTSE 100 has now closed having recouped the deep losses from earlier this week.

But looking over the month as August as a whole, things are not so rosy. The index suffered its worst monthly loss since 2012.

At tonight’s close it’s up 0.9% on the day at 6247.94. That compares with 6,188 at the start of the week from where it quickly tumbled through the 6,000 level and lost 4.7%, or a huge £74bn in combined market value, on Monday alone. The index of leading London-listed shares had managed to claw back most of its losses on Thursday, bouncing 3.5% in one session following a surge in stocks in China and the US.

For August as a whole, the index dropped 6.7%, the worst performance since May 2012, after it was battered by crumbling investor confidence as China made a string of interventions to shore up its economy, includin a shock devaluation of the yuan currency. The bleak August has left the index in the red for the year.

European bourses have ended slightly higher on the day with the pan-European FTSEurofirst 300 up 0.34% and at 1,435 was just above its starting point for the week of 1,427.

Wall Street has a while to go until its close and for now the Dow Jones industrial average is down around 0.2% at 16,615. It opened the week at 16,459.

After a week of wild swings, that seems like a good place to close for today.

Thanks for reading and for all the comments.

Reuters has been snapping the highlights from Fischer’s CNBC interview, where importantly he has also said that with the economy getting back to normal the Fed will have to show that at some point by normalising rates and he has made no decision on September.

There’s a lot for markets to weigh up in what he says, perhaps a good reflection of the particular quandary central bankers find themselves in right now.

Here are highlights from the Reuters alerts:

- 28-Aug-2015 16:32:47 - ASKED ON SEPTEMBER HIKES, FISHER SAYS THERE WAS A STRONG CASE BEFORE

- 28-Aug-2015 16:36:24 - FED’S FISCHER SAYS WE’RE GETTING BACK TO NORMAL AT SOME POINT WE WILL SHOW THAT BY NORMALIZING RATES

- 28-Aug-2015 16:36:46 - FED’S FISCHER SAYS MARKET VOLATILITY DOES AFFECT TIMING OF DECISION

- 28-Aug-2015 16:36:57 - FED’S FISCHER SAYS THINGS COULD SETTLE QUICKLY

- 28-Aug-2015 16:37:51 - FED’S FISCHER SAYS CONCERN IS THAT CHINA IMPACTS MANY COUNTRIES

- 28-Aug-2015 16:38:27 - FED’S FISCHER SAYS WE’RE HEADING IN DIRECTION OF HIGHER RATES

- 28-Aug-2015 16:38:43 - FED’S FISCHER SAYS NOT CERTAIN ECONOMY BACK TO NORMAL YET

- 28-Aug-2015 16:38:54 - FED’S FISCHER SAYS MADE NO DECISION ON SEPTEMBER

- 28-Aug-2015 16:39:14 - FED’S FISCHER SAYS STILL HAVE 2 MORE WEEKS WE HAVE TIME TO SEE INCOMING DATA

- 28-Aug-2015 16:39:50 - FED’S FISCHER SAYS IF DECISION IS CLOSE RECENT DATA WILL INFLUENCE IT

- 28-Aug-2015 16:40:28 - FED’S FISCHER SAYS CANT WAIT FOR CASE TO BE OVERWHELMING TO HIKE

Updated

Fed's Fischer hints turmoil could delay US rate hike

Comments from US policymaker Stanley Fischer are just hitting the wires, and he seems to share his fellow rate-setter William Dudley’s view that the latest bout of market turmoil could push back a rate hike that, until this week, many had expected to come as soon as next month.

Fischer has told broadcaster CNBC that market volatility does affect the timing of interest rate decisions.

Fischer to CNBC: Economy is returning to normal; we've not yet made decision about September. http://t.co/ddr59GYiHq pic.twitter.com/tnBvYhbXeB

— CNBC Now (@CNBCnow) August 28, 2015

With the FTSE 100 hovering around the unchanged mark and the Dow Jones industrial average on Wall Street similarly flat on the day, there is tentative talk that calm has returned to markets.

Translated into Twitter-speak (using a cute cat, naturally), that’s:

Stocks today vs. this week @CNBC pic.twitter.com/frj9Tk7xPg

— Carl Quintanilla (@carlquintanilla) August 28, 2015

Central banks are very much in focus over coming days and policymakers’ words will be scrutinised for hints their fingers will be kept off the rate hike trigger for now given the latest market turmoil and signs global growth might have lost some steam. In the case of the ECB attention will be on clues to further loosening.

After the Jackson Hole meeting of central bankers in Wyoming over this weekend, when the Bank of England’s Mark Carney is set to speak, attention will shift to the ECB’s latest decision on policy for the eurozone next Thursday and particularly the accompanying press conference by president Mario Draghi.

Economists at Morgan Stanley say we should expect dovish messages from Draghi even if there is no extra stimulus.

In their European Economics Weekly, they write:

On balance, we expect the ECB to reiterate its easing bias, using the same language used at the July meeting, when the risk of Grexit seemed imminent. At this stage, we would not expect the Bank to take any tangible policy actions, e.g. , by increasing the pace, the scope or the overall size of its QE programme. But we would not completely rule out any action either.

Philip Shaw at Investec is also not entirely ruling out more support from the Frankfurt-based central bank. He comments:

No change is expected with the refi rate likely to stand on hold at 0.05% and QE continuing at a pace of €60bn/month.

Most interest will, as ever, be focused on Mario Draghi’s press conference, where questioning is certainly set to focus on the recent market turmoil. But attention will also be on the outlook for ECB policy in light of a return in disinflationary pressures following the continued fall in commodity prices and a stronger euro. Recent comments from the Vice President, Vítor Constâncio, and Chief Economist, Peter Praet suggested the Governing Council would be willing to consider additional supportive action should it be warranted.

There is just under an hour to go until UK stock markets close and traders can breathe a big bank-holiday-weekend sigh of relief after a week of dramatic swings.

As my colleague David Hellier reports global share prices look to be closing this rollercoaster week barely changed from how they began it, despite volatile movements that saw indices fall more than at anytime in the the past six years.

Right now, the FTSE 100 is up around 7 points at 6200, having started the week at 6,188. On Wall Street the Dow Jones industrial average is down around 0.4% on the day at 16,584. The index started the week at 16,459.

Beyond the volatile markets, analysts are pondering what it all means for the real economy.

The consultancy Oxford Economics believes the market turmoil shouldn’t hit the UK too hard. We learned earlier today that the UK clocked up relatively solid GDP growth of 0.7% in the second quarter.

Lead UK economist at Oxford Economics, Martin Beck, comments:

The UK hasn’t been able to escape the consequences of China’s ‘Black Monday’, with equity prices on course to see one of the largest monthly falls since 2008. But while global turmoil will hit the economy, it shouldn’t undermine the expansion too much.

UK households’ direct equity holdings are fairly small, suggesting that the effect of the drop in the FTSE on household spending will be limited. And while China’s troubles are bad news for exporters, they are already delivering a silver lining in the form of cheaper oil and other commodities.

Summary

Time for a mid-afternoon summary:

- It’s been a mixed day for global stock markets. Asian markets saw gains as optimism about the health of the US economy continued to bubble over, while Japan notched up some better-than-expected inflation data. The Shanghai Composite ended the day up 4.8%, while the Nikkei was up 3.03%.

- But it’s been a wobbly day in Europe and the US. Wall Street has started the day with falls across its three main indices. The FTSE100 has been seesawing up and down, and is currently up 0.3%, with gains for oil and mining stocks.

- The latest data has shown that Germany’s low inflation trend continues, adding to the chatter about more eurozone stimulus.

- On a busy day for statistics, we also found out the UK economy grew by 0.7% in the second quarter, while the Greek economy grew by 0.9% over the same period.

- Greece has a new government, in caretaker mode until elections on 2o September.

At least one part of the Greek government handover has gone smoothly.

Twitter updated too #Greece @PrimeministerGR pic.twitter.com/lB4Y0XZXBf

— Derek Gatopoulos (@dgatopoulos) August 28, 2015

Watch this space to see how the bailout unfolds...

Wall Street starts on a downer

The main US stock markets have opened lower this morning, dampening the mood after a two-day rally.

- The Dow Jones is down 0.38% at 16,596 points;

- The Nasdaq has fallen 0.12% at 4,807;

- The S&P 500 fell 0.26% to 1,982 points in the first minutes of trading.

Updated

A quick history lesson:

Say hello to Greece’s new prime minister, Vasiliki Thanou....

... and finance minister Yiorgas Houliaràkis ....

... and good-bye (for now?) to the outgoing PM.

It’s quite a telling contrast. Alexis Tsipras was all smiles as he arrived for a party meeting earlier today.

The relaxed mood apparently continued after the meeting.

"No case" for US rate rise in 2015 - central banker

The increase in US consumer spending leaves economists pondering whether the Federal Reserve will raise interest rates next month.

One senior policymaker said he did not see the case for a change unless there is a major change in economic outlook.

Narayana Kocherlakota, president of the Federal Reserve Bank of Minneapolis, told CNBC

Barring that [change in the economic outlook], I don’t see a near-term increase as being appropriate, and by near-term I mean really though the course of 2015.

Kocherlakota is leaving the Fed at the end of the year.

Updated

US consumer spending rises in July

US consumer spending picked up a little in July, as drivers splashed out on new cars, in yet another sign that the world’s largest economy is doing well.

Reuters has the details:

The Commerce Department said on Friday consumer spending increased 0.3%, after an upwardly revised 0.3% rise in June. Consumer spending, which accounts for more than two-thirds of U.S. economic activity, was previously reported to have gained 0.2% in June.

Economists polled by Reuters had forecast consumer spending rising 0.4% last month.

Greece's finance minister "knows what he's doing" says eurogroup chief.

Greece’s new finance minister has received the stamp of approval from the head of the eurogroup, Jeroen Dijsselbloem.

According to Dijsselbloem, Yiorgas Houliaràkis “knows what he’s doing”. Well, that’s a relief.

Dijsselbloem hopes that Greece’s interim government will continue preparing for the bailout in the run-up to elections on 20 September.

IMF counts cost of Greek bailout

The International Monetary Fund broke its own rules to get involved in the Greek bailout, lending money that many officials knew would never be repaid. The sorry saga of the IMF’s involvement in the Greek bailout is recounted in a Reuters special report that adds many new and interesting details.

- A majority of IMF directors thought the first Greek bailout would not work. Even those who supported the bailout had their doubts.

As one supporter explains:

Objectively we made Greece worse off ... You’re lending to a country that is already unable to pay its debt, and that is not our mandate.

- Christine Lagarde, the current head of the IMF, opposed its involvement in the bailout when she was France’s finance minister. At the time she hoped

....that the Europeans could put together enough of a package, enough ring-fencing, enough of a backstop so as to show that Europe could sort out its own affairs.

- Some think that an early opportunity to agree debt relief for Greece was missed, following the unexpected departure of Dominique Strauss-Kahn, after his arrest for alleged sexual assault in 2011 (charges were later dropped).

- Strauss-Kahn is also criticised by former IMF officials for allowing the fund to become “trapped in the troika”, working with the European Commission and European Central Bank, at the expense of asserting its own view.

“DSK (Strauss-Kahn) made a tactical error in letting the fund get trapped in this troika arrangement.

The full article is here and well worth reading.

Low inflation trend continues in Germany

Inflation has been almost static for German consumers this summer, mainly as a result of tumbling oil prices.

German consumer prices rose 0.1% in August compared to the previous year, and were unchanged on the previous month, according to the federal statistics office.

The full table shows that energy prices fell 7.6%, while food and rents crept up (0.8% and 1.1% respectively).

The result was expected following the low inflation data published by German states earlier today.

Updated

After a two-day rally on Wall Street, US stock market futures have fallen, suggesting a bumpy ride into the weekend.

However as Reuters reports:

The three major US indexes looked set to end the week higher despite the market’s cumulative 10% drop in the first two days of the week amid fears of a slowdown in China.

Later today (8.30 ET, 13.30 BST) we are expecting data to show a small rise in US consumer spending. Economists have forecast a 0.4% increase in consumer spending in July, compared to 0.2% in June.

It’s been a volatile week on the FTSE100 and the index has yet to make up this week’s lost ground.

The index is currently trading around 6,161 points, down 0.49% on the day, and still short of the 6,187 level it was at a week ago.

Greece’s interim government is due to hold its first cabinet meeting later today.

Here are some pictures that have just arrived of Vassiliki Thanou being sworn in as prime minister on Thursday....

... and talking to the previous incumbent

Consumer spending boosted Greek economy in spring

Greece’s economy grew by 0.9% from April to June, as official statisticians revised upwards an earlier GDP estimate.

Consumer spending was the main driver of growth, rising 2.2% compared with the second quarter of 2014.

But the picture is likely to be very different when we get GDP data for the summer quarter, a period marred by capital controls and weeks of confidence-sapping negotiations over Greece’s place in the eurozone.

Updated

Deflation debate to haunt ECB again

German consumer prices were very low in August, according to the latest batch of data, putting even more pressure on the European Central Bank to expand its stimulus programme (see last post).

Here are the key lines from Reuters:

In North Rhine-Westphalia (NRW), the federal state that tends to act as a bellwether for the national inflation rate, consumer prices held steady at 0.2 percent on the year in August.

In three other states annual inflation remained unchanged, while it slowed in one and turned negative in another. State data is used to calculate Germany’s national inflation rate....

ING economist Carsten Brzeski said he would not have been surprised if inflation had fallen to zero or even slipped into negative territory given the sharp fall in energy prices, but noted this could still pass through into next month’s data.

Nonetheless, the subdued reading is a headache for the ECB, which has been trying to push inflation in the euro zone back towards its target of just below 2 percent over the medium term via bond-buying, or quantitative easing (QE).

“This entire discussion about whether deflation has returned will haunt the ECB next week,” he said.

Economic mood rises in eurozone, but not enough to quell slow growth concerns

Economic confidence in the eurozone ticked up a notch in August, according to the latest official data. The Economic Sentiment Indicator - a survey of businesses and consumers - went up 0.2 points to 104.2 in August. Across the entire EU, the indicator went up 0.4 points on last month to 107.

But despite a positive headline, nobody should get too carried away. Industry confidence in the eurozone fell 0.8 points, with managers less optimistic about future orders. Consumers were more confident about the future (+0.3), but less positive about the outlook for employment. Managers in services were the most upbeat (+1.3), expecting an increase in demand for their business.

Among the largest eurozone economies, the ESI rose in France (+0.9) and Spain (+1.7). But the mood was less confident in Germany (-0.2), the Netherlands (-0.3) and Italy (-0.6). But in Greece, economic sentiment was down by six points - not exactly a vote of the confidence in the country’s third bailout.

Jessica Hinds at Capital Economics thinks the figures will put the European Central Bank under more pressure to accelerate its stimulus programme.

At its current level, the eurozone ESI is consistent on past form with annual GDP growth accelerating to about 1.5%, better than Q2’s 1.2% outturn. But that pace of expansion will do little to erode the spare capacity in the region and thereby provide a boost to inflation. And we expect growth to slow further in the coming months as the twin tailwinds of the previous falls in the euro and the oil price fade.

Moreover, there remains a clear risk that the Greek crisis could flare up again, with another election next month and the distinct possibility that Greece will fail its first bailout review due in October. This has the potential to damage economic sentiment across the eurozone and trigger renewed falls in the ESI. As such, the ECB may come under growing pressure to increase the pace of its asset purchases.

Updated

The FTSE100 is still stuck in negative territory, but oil and mining stocks are racking up gains.

Oil firms are getting a boost from rising crude prices. Mining stocks have been helped by activist investor Carl Icahn, who disclosed on Thursday that he had taken an 8.5% stake in the mining and oil group Freeport-McMoRan. The billionaire investor has said he wants to talk about possible cuts in production, which may be good news for other producers.

Mining firm Glencore was the biggest riser on the FTSE100 this morning, with other miners and oil majors following in its wake.

- Glencore +3.8%

- BHP Billiton +0.9%

- BG Group +2%

- BP +1.7%

- Shell +1%

James Plunkett at Citizens Advice has picked out some of the most interesting economic charts from today’s UK GDP data.

The manufacturing association says the GDP figures are further proof that the British economy has not rebalanced yet.

During the last government, the chancellor George Osborne promised to unleash “a march of the makers”, but progress has has been halting.

But Zach Witton, deputy chief economist at the EEF, the manufacturers’ organisation, said there were “some positive signs”, with business investment up 2.9% in Q2, following a 2% gain in the previous quarter.

However, weakness in the manufacturing sector highlights concerns as to whether this will be sustained. Uncertainty as to whether Greece would leave the eurozone, and the pound strengthening against the euro, probably played a part in the weak performance.

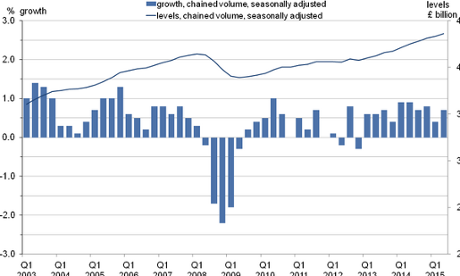

Economists were not surprised that UK growth statistics for April to June were left unrevised. More interesting than the headline figure is where the growth was coming from.

Samuel Tombs, senior UK economist at Capital Economics, notes that the British economy has been boosted by trade, but thinks this is unlikely to last.

Unsurprisingly, consumer spending grew strongly again, rising by 0.7% on the quarter. And overall investment rose by 0.9%, reflecting a hefty 2.9% increase in business investment, putting paid to the idea that uncertainty about the general election would weigh on capital expenditure. But the big news is that net trade made a hefty 1 percentage point (pp) contribution to quarterly growth – the most since Q1 2011....

Looking ahead, the pound’s recent appreciation and the continued weakness of demand in some export markets such as the eurozone and China suggest that net exports are not about to play a sustained role in supporting the economic recovery.

The latest GDP data from the Office for National Statistics means we can update our picture of the UK economy over the last decade.

The ONS has confirmed that the economy grew by 0.7% in the second quarter and by 3% growth in 2014.

GDP has now increased for 10 consecutive quarters, which is certainly good news for the government.

Updated

UK GDP growth confirmed at 0.7%

Hold on to your hats: UK economic output grew by 0.7% from April to June, unchanged on earlier estimates.

Updated

A sense of of déjà vu has returned to Athens this morning with the announcement of a new interim government.

With three women in top posts, including Vassiliki Thanou who takes over as prime minister, the new 22-member cabinet will be sworn in at 1 PM local time (11am BST). The inauguration of the interim government, which will lead Greece to polls on September 20, marks the official start of the election campaign. In a pithy 32-word statement to the leftist newspaper Avgi, the outgoing prime minister Alexis Tsipras said:

Today the big election battle begins. The Greek people will give a powerful mandate [to the next government] for the present and the future. Greece cannot go back. And it will not go back. It will go forward.”

Tsipras’ optimism, however, took a major blow this morning with publication of the first poll in today’s left-leaning Syntaktwn newspaper.

In sharp contrast to earlier this year, the popularity of his leftist Syriza party has dropped from 26% to 23% with ratings for the main opposition centre right New Democracy party rising 4.5 percentage points to 19.5%. The survey, conducted by pollsters ProRata, found the vast majority of Greeks disagreeing with Tsipras’ surprise decision to take the country to snap polls – a move that may well backfire for the leader if he does not win an absolute majority.

Greece's finance minister named as Yiorgas Houliaràkis

We haven’t even had September’s snap election in Greece, but political insiders are already talking about a second autumn poll.

Stavros Theodorakis, leader of the centrist To Potami party, told Kathimerini that former Greek Prime Minister Alexis Tsipras’s refusal to cooperate with pro-European parties after next month’s ballot may complicate the formation of a government and force a new poll.

The risk is that if SYRIZA doesn’t get an absolute majority in parliament, that if the allies it wants don’t make it to parliament, then we’ll go to new elections again in November and December.

Meanwhile details of Greece’s new caretaker government are emerging.

Yiorgas Houliaràkis has been named as interim finance minister.

The full caretaker government will be sworn in at 1pm today (11am BST)*. For more details of how we arrived here, the Guardian’s Athens correspondent Helena Smith has filed this report.

She also profiles Greece’s interim prime minister, Vassiliki Thanou, the first woman to lead Greece in its 200 years as a modern state.

Trained at the Sorbonne in Paris, the 65-year-old mother of three has been described by those who know her as a stickler for detail and “deeply principled.” In the five years that Greece has battled with the demands of international creditors, she has played a leading role as a trade unionist protecting colleagues from pay cuts exacted on the judicial sector.

Read more here.

*Timing changed at 09.11 to reflect latest information.

Updated

So much for that. The early gains on the FTSE100 have largely fizzled out: the index is flat at the moment.

Tony Cross, market analyst at Trustnet Direct, explains what is going on.

London’s FTSE-100 is making some modest gains as the final trading session of the month gets underway but the market doesn’t seem willing to build on the pace seen in China overnight. As we’ve noted before, there’s still a very real chance that further volatility will be seen in the near term and with the long weekend fast approaching, there’s a good chance that some may be hoping to book opportunistic profits ahead of the break.

What is Jackson Hole all about?

Every year, the great and the good of central banking head off to the mountains of Wyoming to ponder the state of the global economy.

This year’s theme is “Inflation Dynamics and Monetary Policy”

As the The Wall Street Journal explains in this handy bluffer’s guide:

It’s an apt subject given the strangely subdued state of inflation in many advanced economies, including persistently sluggish price and wage gains in the U.S. despite the improving labor market.

The official agenda gives the full run-down of the guest list.

This year’s speakers include: Mark Carney of the Bank of England, Víctor Constâncio, vice president of the European Central Bank, Stanley Fischer, vice chairman of the Board of Governors of the Federal Reserve System and Raghuram Rajan, governor of the Reserve Bank of India.

One notable absence is Janet Yellen, governor of the US Federal Reserve.

Why Jackson Hole?

As the WSJ explains, former chairman of the Federal Reserve, Paul Volcker, was fond of fly fishing. The organisers thought holding their economic symposium in Jackson Hole, with its plentiful lakes and rivers, would encourage him to come along. And it worked.

Summary

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and the business world.

After a week of crazy swings on global markets, optimism is breaking out on trading floors.

Stock markets across Europe have made modest early gains. The FTSE 100 is up 0.42% , while Germany’s DAX and France’s CAC40 gained 0.2% in the first minute of trading.

Asian markets have rallied, amid renewed optimism about the US economy - there is nothing like an upgrade to US GDP to lift the mood about global growth prospects.

The Shanghai Composite index is up 1.1%, although it remains 11% down on the week. The MSCI index of Asian shares (excluding Japan) was up 1.3%, while better-than-expected inflation data in Japan lifted the Nikkei by 3.3%.

Oil prices have continued to go up, after two big oil pipelines in Nigeria were forced to close, raising the prospect of tighter supply.

Brent crude was up 69 cents to $48.25 at 06.15 GMT, while US crude was 65 cents higher at $42.21*.

On Thursday oil prices rose 10% - their biggest gain in six years.

Meanwhile, central bank watchers will be paying attention to the Federal Reserve Bank of Kansas City’s annual economic policy symposium - or Jackson Hole, for those in the know. The annual get-together kicked off on Thursday evening and runs into Saturday, with Bank of England governor Mark Carney taking part.

Later today we are expecting trade and consumer data from the US.

I’ll be tracking that and all the latest...

*Corrected 08.36am

Updated