One last thing.... Wall Street has ended the day higher, bucking the general trend in the markets today.

The Dow gained 80 points, or almost 0.5%, led by that Apple rally. Rising oil prices also gave the index a lift.

US Closing Prices: #DOW 16330.4 +0.47% #SPX 1952.29 +0.53% #NDX 4296.29 +1.01% #VIX 24.91 -5.03%

— IGSquawk (@IGSquawk) September 10, 2015

Traders remain edgy after the recent volatility, as CNBC explains:

There’s still continued lack of conviction and any real liquidity,” said Myles Clouston, senior director at Nasdaq. “Investors have been spooked by what’s happened in the last month, month-and-a-half.”

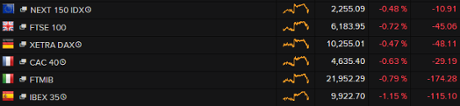

European markets close in the red

It wasn’t a great day in the European stock markets, with the main indices all finishing in the red.

Investor confidence was hit early today, by the producer prices survey showing that Chinese firms are cutting prices sharply. Brazil’s downgrade and New Zealand’s interest rate cut also hit sentiment.

The Bank of England’s rate decision, and accompanying minutes, didn’t move the dial -- although there is (as usual) disagreement over how soon the Bank may raise rates (or even if they should at all)

Jasper Lawler of CMC Markets has helpfully rounded up the main action in the City:

European stocks snapped a three-day winning streak on Thursday. The drop comes one week before the Federal Reserve decides whether to hike interest rates. Until the decision’s made, markets are likely to remain on edge.

House builders topped the FTSE 100 with Barratt Developments leading the field with gains of over 2% after a report forecasting the supply/demand misbalance of housing in the UK is set to send house prices higher still. The report is really just projecting current conditions like strong consumer confidence and low interest rates into the future.

Corporate results from Britain’s high street were a bit of a mixed bag.

Next was a top riser after beating earnings expectations and taking a more muted stance that Whitbread on the minimum wage, saying it was manageable. Dixons Carphone shares jumped after sales rose but a fall in sales at Argos hurt Home Retail Group results sending shares lower.

Morrisons was a top faller after the company reported a massive 47% drop in profits for the first half, a day after reporting the sale of 140 M Local convenience stores. Traditionally targeting the smaller budget consumer, Morrisons has been hard hit by customers switching to discounters Aldi and Lidl.

And that’s all for today, I think. Thanks for reading and commenting. GW

Apple is helping to push the US stock market up today, as analysts digest last night’s flurry of announcements from the tech giant.

Shares in Apple are up 2.1%, leading the Dow Jones industrial average.

That claws back yesterday’s losses, as Wall Street failed to be initially impressed by the new extra-large 12-inch iPad and the Apple Pencil (which generated plenty of fun on social media).

Apple Pencil needs this right pic.twitter.com/SxeKabBMOl

— KStreetHipster (@KStreetHipster) September 10, 2015

The Dow is now up 107 points, or 0.6%.

Updated

Blanchflower: Inflation too low for a rate hike - duh

Economics professor Danny Blanchflower, a former Bank of England policymaker, isn’t impressed by the tone of the minutes of this week’s meeting.

Speaking on Bloomberg TV, Blanchflower argues that the Monetary Policy Committee can’t simply brush aside the weakness in China’s economy.

It’s also risky to ignore recent data showing the UK economy is slowing, with inflation potentially turning negative soon, he added.

He’s now tweeted this message too, in typical rumbustious fashion:

Most struck in MPC minutes by absurd claim some members "saw continued upside risks to inflation relative to the target" CPI=0.1% - really?

— Danny Blanchflower (@D_Blanchflower) September 10, 2015

next month UK CPI drops a 0.4 rise from Aug14 if we get the -.2% we had in Jul15 then CPI will go to -.5% in Aug15 =deflation almost certain

— Danny Blanchflower (@D_Blanchflower) September 10, 2015

Some members of MPC worried about CPI being above target in the month when it looks almost certain UK set to go into deflation= brilliant

— Danny Blanchflower (@D_Blanchflower) September 10, 2015

labour mkt slowing PMIs slowing china slowing but MPC says ignore that because we think hyperinflation coming so we should raise rates duh

— Danny Blanchflower (@D_Blanchflower) September 10, 2015

Blanchflower also told Bloomberg that the situation reminded him of his time on hte MPC in 2008, when the committee was worried about inflation risks rather than the looming financial crisis and global recession.

Mr Carney goes to Beijing

Bank of England governor Mark Carney didn’t hand around in London to catch the reaction to today’s interest rate decision.

He’s in China now, in his role as head of the Financial Stability Board, meeting with Chinese vice-premier Wang Yang.

The Xinhua newswire says the pair are discussing “the economic and financial situation in the world and China”.

A good chance for Carney to judge the situation in China, and the government’s response, for himself.

Updated

Brazilian stocks and currency hit after downgrade

Brazil’s stock market is retreating after S&P downgraded its credit rating to junk overnight (see details here).

The Bovespa index has dropped by 1.7%, back towards the six-year low touched last week.

And the country’s currency, the real, is hitting fresh record lows against the US dollar. It’s now trading at 3.89 to the US dollar, after S&P questioned Brazil’s ability to manage its public finances in the current recession, with commodity prices so weak.

Luiz Carlos Baldan, a director of the Fourtrade brokerage in São Paulo, told the WSJ that traders fear further losses.

“This downgrade wasn’t priced in by the forex market.

If the central bank doesn’t intervene, the real could hit 4 to the dollar in the next few days.”

Today's least-loved: Every major #currency is rising v the #real today after #Brazil was cut to junk... pic.twitter.com/2qd7haAfQx

— Mark Barton (@markbartontv) September 10, 2015

Updated

After a slightly rocky start in New York, the Dow Jones industrial average has gained 0.2%.

The S&P 500 dipped by 0.1% at the open.

US stocks open lower as uncertainty builds ahead of Fed meeting » http://t.co/azy52sFWMn pic.twitter.com/HAkeCfYODz

— CNBC (@CNBC) September 10, 2015

If you’re catching up now, here’s the latest data from China that has worried the markets:

Declining #China producer prices - that's 42 months and counting. Food for thought for Bank of England and Fed. pic.twitter.com/kesnwIaiVm

— RBS Economics (@RBS_Economics) September 10, 2015

Europe’s stock markets are falling deeper into the red, as traders anticipate fresh falls when Wall Street opens in 20 minutes time.

As covered this morning, investors have gone back to worrying about the slowing Chinese economy and the potential that US interest rates are raised next week.

Randy Frederick, managing director of trading and derivatives at Charles Schwab, says China is casting a big shadow over the economy.

He said (via Reuters)

“What is China going to do? That is the biggest unknown for people at the moment.”

On Wednesday, there appeared to be genuine optimism in the markets. But it’s been quickly eroded.

Here are the main European markets:

Martin Beck, senior economic advisor to the EY ITEM Club, predicts that UK interest rates will remain frozen for another year or more.

Today’s Bank minutes show that some MPC policymakers are steering away from an early rate rise, he argues:

“The more dovish tone is largely a function of the changes in the international environment.

Though members felt that global developments had not yet “alter[ed] materially the central outlook described in the August Inflation Report”, there was a consensus that the downside risks had escalated.

Beck predicts the first UK rate hike will come in the third quarter of 2016.

“At the current pace, there may be an EU referendum before we see a rate increase,” says Nick Dixon, investment director at Aegon UK.

He argues that, despite Ian McCafferty’s itchy trigger finger, many MPC members may see the merits in leaving rates unchanged for many months.

With muted consumer spending and earnings growth, coupled with low oil prices and broader inflationary pressures, there is a credible case for the Bank to keep rates lower for longer, or even cut them to provide relief to consumers.

With the strong pound also dragging down exports, we are unlikely to see any upward revision of interest rates until well into 2016.”

We don’t know when Britain will vote on whether to leave the European Union - except that the ballot is before the end of 2017.

It’s no surprise that the BoE sat on its hands this month, given the problems overseas, says Ben Brettell, senior economist at Hargreaves Lansdown:

The concerns are numerous.

A slowing Chinese economy and devaluation of the yuan, concerns over the health of other major emerging markets (Brazil’s debt was downgraded to junk status overnight - the first BRIC economy to lose investment grade status since the financial crisis began), and the resulting volatility in commodity prices could all create headwinds for the UK economy

There’s lots of reaction to today’s decision.

Maike Currie, associate investment director at Fidelity Worldwide Investment, isn’t surprised that the Bank of England resisted raising rates, given problems overseas:

A slowdown in emerging market economies means deflationary forces are mounting across the globe and the net effect on developed markets will be to entrench and embed the ‘ice age’ conditions of low rates, for longer.

There’s little significant reaction in the financial markets.

The pound jumped a little when the Bank’s decision was announced, but has now dropped back:

Sterling had already risen against most other currencies today:

Pound climbs as #BOE says time for a rate increase is approaching http://t.co/aeoB5Ldy7Z via @LukanyoMnyanda #FX pic.twitter.com/tysCLAZLgT

— Lucy Meakin (@lucy_meakin) September 10, 2015

My colleague Heather Stewart is at the Bank of England, digesting the minutes. Here’s her take:

Bank of England policymakers fear China’s slowdown could “add to the global headwinds” facing the UK economy in the coming months, but it is too early to derail their plans to raise interest rates off course.

One member of the Bank’s nine-member monetary policy committee, former CBI economist Ian McCafferty, voted for an immediate increase in borrowing costsfrom their record low of 0.5% at the meeting that concluded on Wednesday — the same voting pattern as in August.

But the minutes of the meeting, published on Thursday, offer the first insight into how UK policymakers are weighing the potential costs of China’s downturn for economic recovery at home.

Developments in China, where crashing share prices and a devaluation of the yuan unleashed shockwaves across global financial markets in August, were, “the main focus of the committee’s decision”, the minutes show. They concede that, “these developments have the potential to add to the global headwinds to UK growth and inflation”.

However, balancing the risks for the UK from a Chinese downturn against robust domestic demand, the MPC concluded there was not yet any reason to tweak the relatively upbeat forecasts for the economic outlook set out in last month’s quarterly inflation report.

“Global developments do not as yet appear sufficient to alter materially the central outlook described in the August Report, but the greater downside risks to the global environment merit close monitoring for any impact on domestic economic activity”, the minutes say.

And here’s Heather’s full story:

The word “China” appears 10 times across the seven pages of today’s Bank minutes.

That underlines the importance of the shock devaluation of the yuan last month, which triggered the Great Fall of China and market turbulence worldwide.

The minutes include this reminder of the drama that unfolded over the summer:

First, on 11 August the People’s Bank of China had lowered the central parity of the Renminbi exchange rate against the dollar by 1.9% compared with the previous day. It also announced a change to the mechanism for determining the central parity of the Renminbi which led to a further depreciation.

Second, against the backdrop of the policy measures to support the stock market announced by the Chinese authorities in June and July, the Shanghai Stock Exchange Composite Index had dropped by 8% on 24 August, leading to substantial falls in both advanced economy and emerging market equity indices.

In total over the period since the MPC’s previous meeting, equity prices had fallen by 5-10% in the United Kingdom, United States and euro area.

Ian McCafferty, the lone hawk on the committee, argued once again that rates should begin rising now.

He believes that private domestic demand will remain strong, with consumer and business confidence at high levels. And by raising rates a little now, the Bank runs less risk of having to hike aggressively in the future.

This argument has been raging on the MPC for months.

It’s worth noting that there are a range of views among the Monetary Policy Committee about the risks of inflation.

Some see “continued upside risks to inflation relative to the target”, suggesting they are closer to voting to raise rates.

Bank expects UK recovery to remain 'healthy'

The Bank of England’s message is that the recent volatility in the financial markets, and the Chinese slowdown, does not radically change their view of the economy.

They do warn that “the downside risks to world activity had probably increased”, but argue that it’s simply too early to conclude that Britain’s economy is at risk

Indeed, the Bank still expects to see “healthy domestic expansion” in the UK.

Here’s the key section of the minutes:

Domestic momentum is being underpinned by robust real income growth, supportive credit conditions, and elevated business and consumer confidence. The rate of unemployment has fallen by over 2 percentage points since the middle of 2013, although that decline has levelled off more recently.

Global developments do not as yet appear sufficient to alter materially the central outlook described in the August Report, but the greater downside risks to the global environment merit close monitoring for any impact on domestic economic activity.

Updated

The Bank of England is encouraged that Greece agreed its third bailout last month, although this calm may not last for long:

It says:

The outline agreement between Greece and its euro-area partners had reduced the likelihood of further harm to activity and confidence from that source, at least in the near term. By contrast, concerns about China and other emerging economies had grown.

Bank: economic risks have risen since August

The Bank of England is concerned that the risks faced by emerging markets such as China have increased, since its last meeting in August.

The Monetary Policy Committee says:

The Committee noted in the August Report that the risks to the growth outlook were skewed moderately to the downside, in part reflecting risks to activity in the euro area and China.

Developments since then have increased the risks to prospects in China, as well as to other emerging economies. This led to markedly higher volatility in commodity prices and global financial markets.

However, these developments are not yet serious enough to materially damage the UK recovery, it adds.

Updated

Today’s decision means that UK borrowing costs have been pegged at 0.5% since March 2009.

The summary of the meeting is online here:

Updated

The Bank voted 9-0 to leave the current quantitative easing programme unchanged.

It has already bought £375bn of government bonds under the scheme.

Bank of England maintains #BankRate at 0.5% and the size of the Asset Purchase Programme at £375 billion…

— Bank of England (@bankofengland) September 10, 2015

…Minutes of the MPC meeting reveal a vote of 8-1 to maintain #BankRate and a unanimous vote to maintain the stock of Asset Purchases

— Bank of England (@bankofengland) September 10, 2015

Bank of England rate decision

Here we go! The Bank of England has decided to leave interest rates at their current record low of 0.5%.

But the decision wasn’t unanimous -- the MPC was split 8-1, with Ian McCafferty again voting to raise borrowing costs to 0.75%.

Jus time to flag up that the Bank of England wants your help to reform the financial markets and make them work better:

Join the conversation by tweeting us your questions using #BoEOpenForum and we'll put them to Andy Haldane on Monday pic.twitter.com/OsGGXcIgK7

— Bank of England (@bankofengland) September 10, 2015

Bank of England minutes: What to watch for

Just 30 minutes to go until the Bank of England announces this month’s monetary policy decision.

The real interest, though, lies in the minutes of the meeting which will be released at the same time.

Economists will be looking to see

-

How the committee split. Last month it voted 8-1 in favour of no change.

-

The Bank’s view of China. August’s meeting was held before Beijing devalued the yuan, spooking market worldwide. Has that decision, and its impact, changed the MPC’s view of the global situation?

-

Whether the Bank is worried about the UK economy. Recent economic data has been rather soft, suggesting growth is tailing off a little.

-

The inflation view. Does the Bank see inflationary pressures building, especially as retailers warn that they’ll raise prices to cover the cost of the ‘national living wage’?

And here’s another handy chart from RBS, showing how the City has constantly over-estimated the chance of UK interest rates rising since the crisis began.

Predicting no change in Bank Rate - amazingly hard. pic.twitter.com/PpCjnwkJAk

— RBS Economics (@RBS_Economics) September 10, 2015

City economist have pushed back their expectations for the first UK interest rate hike over the last month, as the global economic picture darkened:

Ahead of today's Monetary Policy Committee meeting, here's how market expectations have changed since last time. pic.twitter.com/DMI8LdQz5z

— RBS Economics (@RBS_Economics) September 10, 2015

Irish GDP beats forecasts

Ireland has shaken off the malaise in the global economy, by posting remarkably strong growth figures.

Irish GDP jumped by 1.9% during the quarter, beating forecasts of 1%. This means the economy grew by a stonking 6.7% over the last year.

Ireland’s GNP, or gross national product, also rose by 1.9% quarter-on-quarter, and was 5.3% higher year-on-year. GNP strips out the impact of multinational companies, so is a better guide to the underlying health of the economy.

Updated

Global worries hit European stocks

After three days of gains, Europe’s stock markets are slipping back this morning.

The main indices are down by between 0.5% and 1.1%, as the rally that began on Monday is derailed.

The usual culprits are to blame. Namely:

-

China, after today’s data showed producers slashing prices at a faster rate to generate demand.

-

The US, with investors continuing to fret that the US Federal Reserve might raise interest rates next week.

Brazil’s credit rating downgrade, and New Zealand’s interest rate cut, have also dampened the mood, as traders brace for the Bank of England’s decision at noon.

The markets will probably remain volatile until the Fed’s decision, next week.

Brenda Kelly of London Capital Markets explains:

It would seem that market participants will have to get used to swings in every direction on equity indices while the market makes up its mind about whether a Fed rate hike would be positive or not.

Probability of a move next week has now fallen to 28%.

She also predicts that Ian McCafferty will be the only BoE policymaker to vote to raise UK interest rates this month:

No change is expected in terms of the rate but the voting structure will still be watched.

Expected to be 8-1, any hawkish change to this will likely see UK house builders under pressure. Given the dearth of inflation and yesterday’s horrific industrial and manufacturing data and the headwinds from China. It would certainly be a big surprise to the markets if any major swings in the votes are evident.

Hectic swings hint at a fragile recovery #Japan #Nikkei $NKY http://t.co/s8UcVG2OOg

— Ipek Ozkardeskaya (@IpekOzkardeskay) September 10, 2015

Updated

In the currency markets, the New Zealand dollar has taken a tumble after the country’s central bank cut interest rates.

The Kiwi dropped 2% against the US dollar at $0.6275, and is down 1.6% against the pound at around 41p. Not great news for All Black fans ahead of the Rugby World Cup, which begins in England later this month.

Updated

Peter Cameron, associate fund manager at EdenTree Investment Management, reckons that the case for raising UK interest rates is “flimsy”.

The UK’s exports are already struggling against the strength of Sterling, a problem that would be exacerbated by a rate rise. Hawks may point to wage growth finally showing signs of life but even this trend slipped into reverse last month and could slow further if the outlook for the global economy darkens.

Cameron also suggests the BoE could consider raising borrowing cost by just 0.1 percentage points, rather than a quarter-point, to avoid scaring the markets.

Last month, only one Bank of England policymaker (Ian McCafferty) voted to raise interest rates.

Yann Quelenn, market analyst at Swiss online bank Swissbank, reckons other MPC members will sit tight again:

“It is likely that the Bank of England will leave its rate unchanged today. We believe that policymakers are not only considering domestic conditions but also global conditions. Markets are currently driven by the next U.S. Fed rate hike, China’s current turmoil and lingering low oil prices.

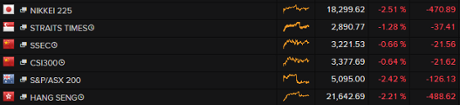

China’s stock market has closed in the red, after premier Li Keqiang warned that the country’s economy was vulnerable to global shocks.

The Shanghai Composite index ended the day down 1.45%, ending a two-day rally.

Investors’ nerves were rattled by the news that manufacturers had cut prices at the fastest rate in six years in August, showing rising deflationary pressure.

They also heard premier Li admit that the economy is facing tricky times, as Reuters reports:

Li acknowledged that the economy had “come under quite a number of difficulties and downward pressure” while stressing it remained in a “proper range”, a favourite phrase.

But he admitted that “deep-seated problems” were being exposed.

“China is an economy that is closely integrated with the international market,” he said. “Given the weak growth of the global economy, China cannot stay unaffected and the deep-seated problems that have built up over the years are also being exposed.”

Updated

It’s a bad morning for workers at supermarket chain Morrisons, as my colleague Graham Ruddick explains:

Around 900 jobs are at risk at Morrisons after the grocery retailer announced it plans to close 11 supermarkets.

David Potts, the new chief executive, has proposed shutting the supermarkets as part of a drive to turnaround the struggling company.

The closures were announced as Morrisons reported that pre-tax profits fell by almost half from £239m to £126m in the six months to 2 August.

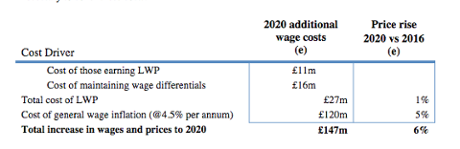

Next: National living wage will cost us £27m

High street retailer Next is coping pretty well with the economic conditions.

Shares in Next have jumped around 2% to the top of the FTSE 100 leader board, after it posted a 7.1% jump in profits thanks to selling more products at full price.

The company, run by Conservative peer Simon Wolfson, has also calculated that Britain’s new ‘national living wage’ will cost it £27m per year.

Of this, £11m relates to the wages of those who will be paid the Living Wage Premium (LWP).

The remaining £16m is the knock-on effect of maintaining wage differentials for supervisors, junior managers and other more skilled or demanding roles within the business (such as specialist call centre work).

Next expects to raise prices by 1% to compensate for this cost, plus an extra 5% to cover general wage inflation.

It also suggests that wages across the sector could be driven up by the LWP.

Next boss Lord Wolfson warns national living wage will cost extra £27m per year and risks "creating a potentially harmful inflationary loop"

— Graham Ruddick (@GrahamtRuddick) September 10, 2015

Updated

After years of steady success, things aren’t looking quite so good at John Lewis as it reports a 26% fall in pre-tax profit today.

Group chairman Sir Charlie Mayfield has admitted that trading conditions were tough for John Lewis’s deparment stores and Waitrose supermarkets, where sales fell for the first time in seven years.

Business leaders: Don't raise interest rates this year

UK business chiefs have urged the Bank of England to leave borrowing costs unchanged at today’s meeting, and at every gathering until the middle of 2016.

The British Chambers of Commerce argues that the economy could be shunted by problems overseas in the months ahead, and needs the cushion of low borrowing costs.

BCC chief economist David Kerr says:

“Global uncertainty – including the current situation in China, weakness in the eurozone, and the widely expected rise in US interest rates – could trigger further bumps in the road.

Factors outside our own control reinforce the case for the Bank of England to keep interest rates on hold until well into 2016.”

Updated

FTSE 100 drops 1%

Trading is under way in Europe, and the main stock markets are all dropping.

The FTSE 100 has lost 59 points, or almost 1%, to 6175.

Mining stocks are leading the falls, reflecting today’s worries about Chinese deflation. BHP Billiton shares are down 5%, and Glencore has lost 2.4%.

Overnight, Brazil was stripped of its investment grade credit rating, as the country’s political and economic problems deepen.

Standard & Poor’s downgraded Brazil to BB-plus, the highest junk rating.

S&P blamed political uncertainty and the country’s deteriorating fiscal position for the downgrade. It’s another headache for president Dilma Rousseff, whose approval ratings have already hit record lows.

Brazil was also struggling to deal with high inflation and a weakening economy, plus the impact of falling commodity prices on its mining and energy firms.

#Brazil cut to junk by S&P. Mkts already priced country as junk. 5y default probability >20% http://t.co/IFyqvEgHuv pic.twitter.com/kGRHzhUIya

— Holger Zschaepitz (@Schuldensuehner) September 10, 2015

#Brazil has lost its investment grade rating at S&P, Outlook still Negative as debt keeps rising Greek style. pic.twitter.com/FXVxIoMG5O

— Holger Zschaepitz (@Schuldensuehner) September 10, 2015

Updated

Chinese deflation worries hits Asian markets

Stock markets in Asia have dropped back today, amid fresh fears of Chinese deflation.

The prices charged by China’s manufacturers fell by 5.9% in August, compared to a year earlier, a new survey showed. That’s the biggest fall since late 2009.

It indicates that demand is falling, in the face of a slowing Chinese economy.

Li Huiyong, economist at Shenyin & Wanguo Securities, explains that it could have a serious knock-on effect

“The change in the producer prices index is very worrying. It could affect corporate profitability, which in turn could affect consumption and the economy,”

Reuters has more details:

China deflation fears grow as producer prices sink most in six years

The data hit markets across the region. Japan’s Nikkei fell 2.5%, as traders were brought back to earth after Wednesday’s 7.7% surge.

China’s market is also down in late trading:

Updated

The agenda: Bank of England decision and UK retail news

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Today we’ll find out how worried the Bank of England is about the state of of the world economy, and the situation here in the UK.

The Bank’s monetary policy committee are meeting in the City today, and will announce their decisions on interest rates at noon. We’re not expecting any change to borrowing costs.

The Bank will also release the minutes of the meeting, revealing how MPC members voted. This will also reveal the Bank’s view on inflation prospects, the slowdown in the emerging economies, and the recent market turmoil.

Rob Gardner, CEO of investment advisor Redington, predicts that the Bank of England will be pretty cautious, and vote 8-1 to leave interest rates at their record lows.

“Given this gloomy outlook, it is unlikely we are to see any more hawks perch on the committee with Ian McCafferty expected to remain the only dissenting voice in favour of a hike.

Indeed, it is more likely that the committee will throw cold water over any imminent rate rise.”

Another topsy turvy day looms in the financial markets. After yesterday’s rally, European stock markets are expected to fall back today after a weak finish on Wall Street.

Our European opening calls: $FTSE 6192 down 37 $DAX 10229 down 74 $CAC 4619 down 45 $IBEX 9934 down 104 $MIB 21941 down 185

— IGSquawk (@IGSquawk) September 10, 2015

Fears over China’s economy are rife again, after new data showed that manufacturers slashed prices at the fastest rate in six years in August.

Rally ruined already...European #stocks set for down day after US gets jitters about rate rise & poor China producer price data

— Caroline Hyde (@CarolineHydeTV) September 10, 2015

There’s also a flurry of financial results from Britain’s major retailers today.

My colleague Graham Ruddick is digging through them - and the early signs aren’t great, with profits down at both supermarket chain Morrisons, and John Lewis, owner of Waitrose (and those department stores).

Underlying pre-tax profits down 35pc to £117m for Morrisons, like-for-like sales down 2.7pc for first half of the year

— Graham Ruddick (@GrahamtRuddick) September 10, 2015

John Lewis Partnership profits down 26pc before one-off items. Waitrose sales down for first time in seven years

— Graham Ruddick (@GrahamtRuddick) September 10, 2015

And while Next has posted a 7% rise in profits, Home Retail has reported a drop in sales at its Argos chain. Not great signs for the state of the UK economy.

More on all those later, along with all the main developments through the day....

Updated