Photograph: Lino Arrigo Azzopardi/EPA

European markets end higher after Draghi hints

Stock markets have enjoyed a buoyant day, after the European Central Bank stuck with its quantitative easing programme and hinted that it would consider whether further measures were necessary in December. The news pushed the euro lower and helped support European markets. US markets also put in a strong performance in early trading, helped by better than expected results from eBay and McDonalds, and strong housing figures and lower than expected weekly jobless claims, albeit with a 3000 rise to 259,000. The final scores in Europe showed:

- The FTSE 100 finished 27.86 points or 0.44% higher

- Germany’s Dax jumped 2.48% to 10,491.97

- France’s Cac closed 2.28% higher at 4802.18

- Italy’s FTSE MIB rose 2% to 22,616.9

- Spain’s Ibex ended up 2.05% at 10,365.4

- In Greece, the Athens market added 1.62% to 710.22

On Wall Street the Dow Jones Industrial Average is currently up 234 points or 1.37%.

On that positive note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back tomorrow.

Mr Draghi announced that alongside producing its updated forecasts for the December meeting, the ECB will also review ‘a whole menu’ of monetary stimulus options. QE remains part of that menu, with Mr Draghi re-iterating a commitment to adjust the ‘size, composition and duration’ of the programme if needed. But other options are possible. For example, it was revealed that the general council discussed the possibility of a further cut to the deposit rate, which currently stands at -0.20%. Indeed, a whole array of options are bound to be discussed in the runup to the December meeting, with Mr Draghi highlighting that the ECB is currently in a state of ‘work and assess’ rather than ‘wait and see’. Beyond the hint of additional monetary stimulus options, we gleaned a couple of other dovish titbits from the press conference. First was the revelation that some general council members ‘hinted’ that they were disposed to adding more stimulus at this month’s meeting. Second, Mr Draghi stated he wants to be ‘vigilant, as people used to say in the old times’. The word ‘vigilant’ has some significance in ECB policymaking – it used to be seen as the expression that ex-ECB President Jean-Claude Trichet employed soon before making policy changes. All told, this was a dovish press conference. Our central case is that the ECB will add more monetary stimulus in the next few months, and December seems increasingly like the most natural date. On the nature of that stimulus though, a QE boost is still perhaps the most likely, the list of possible instruments on the table has lengthened. The euro fell by over 1½ cents against the dollar in response to today’s comments, to as low as $1.116. Or current view is that the euro will fall further, to a trough of $1.06 at the turn of the year, as the ECB looks to stimulate while the Federal Reserve looks to start raising rates.

Greece has reportedly sacked its top tax collection official in a row over alleged delays in collecting taxes, a move which could increase concern about the political independence of its tax authorities. It comes at a time when the country is still in the throes of tackling reforms to satisfy its bailout terms. Reuters reports:

Katerina Savvaidou, head of the Public Revenues Authority, had denied any wrongdoing. She was charged by a Greek prosecutor with breach of duty for extending by about a year tax collection on revenues on TV advertising.

Prosecutors alleged she acted in violation of existing regulations. Savvaidou, who earlier refused to resign, said all of her actions had been vetted by relevant legal authorities of the state.

“By law, when someone is charged with a misdemeanour, the cabinet has the ability to take such a decision (of dismissal),” a government source told Reuters.

Gov spox @olgagerovasili says cabinet decided to dismiss Greece's top tax official Katerina Savvaidou. Says firms got preferential treatment

— NikiKitsantonis (@NikiKitsantonis) October 22, 2015

Does Tsipras have a death wish? Sacking tax chief could throw entire bailout programme, including bank bailout and debt relief, off track.

— Hugo Dixon (@Hugodixon) October 22, 2015

Updated

Judging by today’s ECB conference, leading central banks will continue to head in opposite directions regarding policy:

So in December we could have further easing by the ECB and rates rise by the Fed? That would be very interesting timing.

— Yannis Koutsomitis (@YanniKouts) October 22, 2015

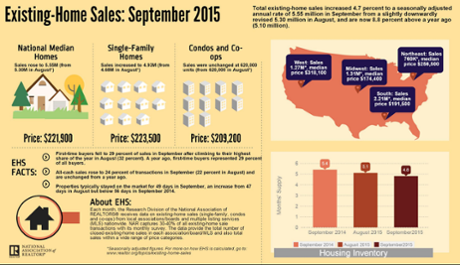

US housing market remains strong

Over in the US, and existing home sales came in at a better than expected 5.55m in September.

That compares to 5.3m in August and expectations of 5.38m, according to the National Association of Realtors.

Unsold inventory fell back to a 4.8 month supply, down from 5.1 months in August. Lawrence Yun, the association’s chief economist said:

As we enter more softer demand months, we may not really feel the squeeze of tight inventory, but come spring of next year...we could be facing a very tight inventory situation.

Existing #home sales up 4.7% to 5.55M as all 4 regions posted gains. Over last year sales are up 9%

— Joseph A. LaVorgna (@Lavorgnanomics) October 22, 2015

Updated

Howard Archer at IHS Global Insight said:

The strong suspicion has to be that the ECB want the possibility of lower interest rates to push the euro down (it has recently tested $1.15 compared to its March near 12-year low of $1.0457). While Mario Draghi stated that the ECB does not have an exchange rate target for the euro he did acknowledge that it is significant to the growth and inflation outlook and is currently a downside risk.

The ECB will undoubtedly be pleased to see that the euro fell markedly as the possibility of ECB interest rate cuts was revealed, and the bank will no doubt be hoping that this possibility continues to weigh down on the euro.

More reaction to the Draghi hints at further easing in December at the ECB’s meeting in Malta. Carsten Brzeski of ING Bank said:

Back to back with one of Malta’s biggest casinos, the ECB today clearly increased its bets, sending strong hints on new monetary stimulus at the December meeting. While no decision was taken today, the ECB’s sounded more concerned about the growth outlook for the Eurozone and signaled its willingness to act. According to ECB president Draghi, some members of the Governing Council were already willing to act today....

All in all, Draghi has been more explicit than we had expected. The door for more monetary stimulus is wide open and does not necessarily have to be more QE. It could also be a lower deposit rate, maybe even foreign exchange interventions or purchases of other assets (previously excluded). Draghi’s u-turn on the lower bound of interest rates has made him walk in the footsteps of former German chancellor Adenauer who once said “why should I care about my chatter from yesterday”. So everything is possible. In our view, the main triggers for more action in December will be the ECB’s staff projections, particularly the headline and core inflation forecasts for 2017.

Even though market participants should know from recent experiences with the Fed that crucial and groundbreaking decisions can be postponed more often than markets believe, it will be hard for the ECB not to deliver anything in December. Maybe inspired by the casino next door, the ECB today increased its bets. The ECB has to have strong cards, because it will have to show its hand in December.

Eurozone consumer confidence weaker than expected

Eurozone consumer confidence has come in much lower than expected in October - perhaps partly due to the fallout from the Volkswagen emissions scandal.

The confidence indicator in the eurozone came in at -7.7 compared to -7.1 in September and lower than the forecast -7.4.

In the wider EU of 28 countries it fell by 0.2 points to -5.7 in October.

Back to Draghi, and Jeremy Cook, chief economist at the international payments company World First said the European Central Bank dropped enough hints to suggest that some form of monetary policy weaponry would be unleashed at its next meeting on 3 December. But what? Cook said:

Firstly, we have to be looking for an extension of the current plan beyond its current deadline of September 2016. Working on the basis that the European Central Bank remains a conservative institution and that the December publication of new economic forecasts does not show a dramatic decline in medium-term inflation expectations then we would look for an extension of 6 months i.e. until March 2017.

A slight increase in the amount spent on a monthly basis [currently €60bn] would not go amiss either.

The problem with this plan however is that it has been done before. Any student of central banks and their policy through the Global Financial Crisis knows that asset purchase plans have done little for the wider economy, particularly inflation metrics, except drive stock markets higher and bond yields into the ground.

What is needed is an interest rate pressed evermore below zero.

But so far the hints of further action have done enough to give the ECB some breathing space:

Look at the performance of the euro in the aftermath of the press conference. Draghi and the Executive Council couldn’t have been clearer that additional policy easing was coming if they’d had the words “SELL THE EURO” tattooed on their faces. For now scaring the cattle is sensible.

They’ve bought time to gain a consensus and deal with internal European issues – the VW scandal and the migration situation in the east of the continent - and external global matters – a Federal Reserve that seems happy to procrastinate and a wobbling emerging market picture. We may have the answers to these questions by December.

There are issues with this kind of cut especially given the Bank’s insistence that the lower-bound of rates has been reached already. This could be avoided by gaming what kind of deposits this new, lower rate applies to as the Swiss and Danish Central Banks have done recently.

For now the euro is lower and the bulls have been scurried away from the taking the single currency higher. We must now wait to see what kind of present Draghi delivers in December.

Wall Street opens higher

US markets have made a strong start to trading, following positive results from McDonalds and eBay.

The Dow Jones Industrial Average is currently up 139 points or 0.8%, while the S&P 500 has added around 0.6%.

Dennis de Jong, managing director at UFX.com said:

The ECB are supposedly pleased with the early results from their stimulus plan, but now is not the time for back-slapping. The eurozone remains in a perilous state, especially with inflation falling back below zero. Mario Draghi now needs to concentrate on diverting a prolonged period of deflation, and the outlook for growth is far from positive.

The slowdown in China and other emerging markets is a big threat to the long-term health of the eurozone. Consumer confidence needs to pick up quickly across Europe but, against a backdrop of poor global growth and an influx of refugees, that is going to be easier said than done.

Alex Lydall, senior trader at Foenix Partners, has sent us his thoughts.

Mario Draghi sent shockwaves through the chambers of the ECB and the euro-area this afternoon with a considerably dovish ECB statement. He noted that emerging markets were still a significant concern to the bloc state and that QE will run to September 2016, or beyond. Draghi’s tone indicated that the ECB were certainly ready to expand the stimulus package, mentioning that the notion would be re-addressed in the December meeting.

The ECB’s concerns over inflation is clearly the driving force and such negative language from the ECB President would imply that it is just a matter of time before further easing was undertaken. With downside risks to growth and inflation prospects outlined once again, a cut in the deposit rate is now on the agenda and it seems the divergence between economic progress in the UK and the US as well as in the euro-area is growing wider as the year progresses.”

Final question in the ECB press conference. It’s about Malta.

Updated

Draghi has been asked about the impact of the Volkswagen emissions-rigging scandal on the eurozone economy. He replied: “It’s very, very early to say.”

Alastair George, chief strategist at Edison Investment Research, said:

It is looking increasingly likely the ECB is being taken down the road followed by other bond-buying central banks - which is if QE has not proved effective, the answer is to do more. Draghi’s comments today indicate to us that the ECB has noted the stubbornly slow return of inflation to target and raises the possibility of further unconventional easing before the end of the year, pushing the euro lower today.”

#Draghi: no doubts whatsoever about effectiveness of monetary policy regardless of structural reforms implemented or not

— Open Europe (@OpenEurope) October 22, 2015

#Draghi: the discussion today was "wide open" and “a few members of the Governing Council hinted at the possibility of acting today"

— Maxime Sbaihi (@MxSba) October 22, 2015

Draghi: Today’s discussion was “wide open” - when asked about possibility of rate cuts. A few members of the governing council hinted at acting today.

Draghi: There was no specific preference for one instrument in the discussion today

— ECB (@ecb) October 22, 2015

Updated

Draghi has been asked about the impact of the Chinese economic slowdown, should it prove to be sharper than expected.

He said the eurozone’s exposure to China via the trade channel is “not very significant” with 6% of eurozone exports going to China, although in some cases the figure is higher: 10%, for example for Germany. There is an indirect impact on oil and commodity prices, but he added that oil prices are low mainly due to supply rather than demand issues.

Financial channel: the eurozone has no significant exposure

In terms of the confidence channel: We think so far what has happened to growth in China hasn’t affected the rest of the world - but if there is a big negative surprise there could be an impact.

ECB VP Constancio deflation is prolonged period (more than one year) not just a few months of negative inflation

— Open Europe (@OpenEurope) October 22, 2015

#Draghi: euro-area exposure to China "not very significant" via trade, indirect & financial channels but confidence channel problematic.

— Maxime Sbaihi (@MxSba) October 22, 2015

Updated

Earlier, the ECB president called on eurozone governments to support monetary policy.

Monetary policy should not be the only game in town. All countries should strive for growth-friendly fiscal policies.”

Draghi: When we are at zero rates, the real rates are being driven by inflation expectations. When expectations of inflation become more negative, we have higher and higher real rates.

But he stressed that nothing was decided on rate cuts and that there was an “open discussion” of this and other measures.

You can read the full text of Draghi’s opening remarks here. This is the key bit:

While euro area domestic demand remains resilient, concerns over growth prospects in emerging markets and possible repercussions for the economy from developments in financial and commodity markets continue to signal downside risks to the outlook for growth and inflation. Most notably, the strength and persistence of the factors that are currently slowing the return of inflation to levels below, but close to, 2% in the medium term require thorough analysis.

In this context, the degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting, when the new Eurosystem staff macroeconomic projections will be available.”

Updated

The euro has fallen below $1.12 for the first time since early October, after Draghi revealed that the ECB’s governing council discussed rate cuts.

Updated

As a reminder, you can watch the ECB press conference here.

Further lowering of the deposit rate was discussed this month, the ECB president said in response to a question from Claire Jones of the Financial Times.

Draghi said:

There was a very rich discussion about all monetary instruments that might be used... and the conclusion was: we are ready to act if needed.

He said it was not a case of “wait and see but a work and assess”.

Draghi has finished his opening remarks and is now taking questions.

Draghi said:

The asset purchase plans are proceeding smoothly and continue to have a favourable impact.”

But he added that falling commodity prices and concerns about emerging markets meant that inflation pressures remained negative. As a result, he said the ECB would re-examine its bond-buying programme in December.

Draghi & co coming in several degrees more dovish than market was expecting - more QE clearly on the mind $EURUSD

— Christopher Vecchio (@CVecchioFX) October 22, 2015

#ECB to reexamine degree of stimulus in December, says #Draghi. Cuts in forecasts then will probably provide good excuse for policy change

— Maxime Sbaihi (@MxSba) October 22, 2015

The euro has lost ground following that comment, falling 1% against sterling to hit a one-month low of 72.70p.

Draghi: The degree of monetary policy accommodation will need to be re-examined at our December monetary policy meeting

Aha! Translation: we may extend QE in December. Markets will like that. #Draghi https://t.co/DdowMSQgfZ

— Peter Spiegel (@SpiegelPeter) October 22, 2015

Updated

Mario Draghi has kicked off his monthly press conference – on time.

The ECB press conference will start in 10 minutes. You can watch it live here.

Economists at JPMorgan said:

We think the ECB will signal that it stands ready to act if needed, and that the door is open for further easing but more likely at the December or January meetings.”

Here’s the ECB’s brief statement:

At today’s meeting, which was held in Malta, the Governing Council of the ECB decided that the interest rate on the main refinancing operations and the interest rates on the marginal lending facility and the deposit facility will remain unchanged at 0.05%, 0.30% and -0.20% respectively.”

The ECB cut rates to record levels to kickstart the economy over a year ago. The main refinancing rate determines the cost of credit in the economy, while the marginal lending facility is the emergency overnight borrowing rate for banks. The deposit facility is the rate on bank overnight deposits, which banks pay to park funds at the central bank.

ECB president Mario Draghi will set out the central bank’s thinking at a press conference at 1.30pm UK time, and whether the bank will make any adjustments to its €60bn a month bond-buying programme.

The ECB has kept its key interest rates unchanged at record lows, as expected.

Updated

The ECB comes to you from Malta today, which is once again pretending that it's a country.

— Mike Bird (@Birdyword) October 22, 2015

However...

Malta's economy is thriving in a way many other European nations can only dream of https://t.co/6DLfZ3BP1y pic.twitter.com/A19nw0vRuD

— Bloomberg Business (@business) October 22, 2015

Markets steady ahead of ECB decision

Markets are steady ahead of the ECB’s policy decision at 12.45 UK time. The FTSE is trading 0.1% lower at 6340.48 after a profit warning from building merchant Travis Perkins dragged down housing stocks. Germany’s Dax has climbed 0.4% and France’s CAC is 0.15% ahead.

Chris Beauchamp, senior market analyst at spread-betting firm IG, said:

A steady battle of attrition continues in London, with the index still unable to establish a direction after four days of relentless grind. However, at least today we have a real reason for not moving too far – namely the ECB meeting. The general consensus is that Mario Draghi needs to do something to get things moving in the eurozone, but there is a sense that neither the ECB nor financial markets know exactly what that will be. We can hope for some indication that action is on its way, although the ECB president will be understandably keen to keep the details under wraps for now.

Housebuilders are jittery this morning after building merchant Travis Perkins warned on earnings. Weaker demand of late has taken the shine off a steady rise in sales overall, raising concerns that such names as Persimmon, Taylor Wimpey and others may be in line for a more sustained correction.”

Labour has responded to George Osborne’s comment that he is “comfortable” with his decision to cut tax credits. Shadow chancellor John McDonnell said:

Once again we’re seeing the true face of the Tory Party. It is shameful that David Cameron talked about his ‘delight’ at tax credit cuts and now George Osborne has said he is ‘comfortable’ with his decision to take £1,300 a year away from working families.

It’s time for David Cameron and George Osborne to think again and reverse these tax credit cuts.”

Expectations that ECB policymakers will announce fresh stimulus measures have gradually faded since governing council member Ewald Nowotny said last week euro area inflation is ‘clearly missing’ the ECB’s target, noted Jasper Lawler, market analyst at CMC Markets UK. Christian Noyer’s submission that the current QE is “well calibrated” is probably a better reflection of opinion on the governing council.

The ECB embarked on a scheme of sovereign bond purchases (quantitative easing) in March – more than €1 trillion in all at a rate of €60bn a month.

Lawler has looked at the ECB’s options:

A change to QE can really take three forms; increasing the size of asset purchases, increasing the length of the program or adding new assets to the mix such as corporate bonds. It is ten months until the programme is scheduled to end so increasing the length of the program seems rather premature.

Europe’s corporate bond market is not as deep as in the US with most companies traditionally favouring bank lending. Adding corporate bonds to the mix would probably work more as a signal of dovish intent than for any real impact on yields or the euro. If the ECB decided to buy shares or ETFs like the Bank of Japan, that would be a game changer and we’d be off to the races in European equities, but chances are slim.

Increasing the size of the programme would probably put the most downward pressure on the euro of all the likely options. However, the ECB runs the risk of crowding out private bondholders with more purchases, and would add to exit risks once the program finishes.”

So what are we expecting from the European Central Bank today?

As my colleague Graeme Wearden reported:

Economists predict that ECB president Mario Draghi will repeat his pledge from September to add more stimulus if needed. However, few expect decisive action this week.

“The ECB’s October meeting is for watching. Draghi’s message will be dovish, but it’s not time to act yet”, said Holger Sandte, chief European analyst at Nordea Bank.

The ECB is currently committed to buying €60bn (£40bn) of government and corporate bonds each month until September 2016, in an €1.1tn (£810bn) attempt to stimulate growth, inflation and bank lending.

Capital Economics’s Jonathan Loynes expects the ECB to boost its QE firepower to €80bn a month in December, but does not totally rule out an announcement this week.

Updated

George Osborne has welcomed the intervention of Mark Carney in the debate about Britain’s future in the European Union, saying the Bank of England governor has set out the principles for renegotiation, Heather Stewart writes. Read the full story here.

Osborne defends tax credit cuts

My colleague Heather Stewart, the Observer’s economics editor, reports:

George Osborne has defended his planned tax credit cuts to backbench MPs on the cross-party Treasury select committee.

The chancellor has come under growing pressure to soften the proposals; but he insisted: “this is fundamentally a judgment call, and I’m comfortable with the judgment call that I have made, and that the House of Commons has supported this week.” He urged the House of Lords not to overturn parliamentary convention by rejecting the tax credit cuts.

The chair of the committee, Andrew Tyrie, also repeated his demand for the Treasury to provide more detailed analysis of how the proposed cuts will hit households at different points on the income scale.

Updated

Earlier this morning, Lord Lawson, one of the leaders of the Conservative campaign to leave the EU, strongly criticised the Bank of England governor for wading into politics. But Osborne said the former chancellor was “probably a bit disappointed that Mark Carney didn’t agree with him”.

Osborne argued, in front of MPs on the Treasury Committee: “What Mark Carney’s speech shows today is that there is a strong argument for reform.”

Alan Clarke of Scotiabank’s reaction to the strong UK retail sales figures was: Wow!

We know that the consumer has the wind in his / her sales:

- Solid employment growth of 1.25% y/y;

- Wage inflation over 3% y/y in the private sector;

- Zero inflation

That all adds up to robust real income growth. With house price inflation picking up too, that is even more motivation for people to go shopping.

Last but not least, with expectations for the timing of the first rate hike being pushed back to end-2016 / early 2017 then consumer spending is clearly well supported.

In terms of the bigger picture, with Q3 GDP (1st estimate) scheduled for next week, I am all the more confident to go for 0.6% q/q rather than be cautious with 0.5.%.

I’m also starting to think about black eye Friday. Sure, it’s a good scheme to get people into the shops, but with sales volumes like this, do I really need to cut my prices? Not convinced.

Anyway - a great reading, and restores my faith that sooner rather than later is the right call on the first Bank Rate hike.”

George Osborne says the UK is ready to "up the temperature" on the EU over renegotiation demands if necessary.

— PoliticsHome (@politicshome) October 22, 2015

The chancellor has been asked why the UK government has not clearly set out what it wants to achieve in its negotiations with the EU.

Osborne said it’s not sensible to turn up with a final list of demands on day one. “That’s not the way to start a negotiation.”

Updated

Osborne: not looking for special deal for City of London

Osborne told MPs on the Treasury Committee that the government is not looking for “special deals or carve-outs for the City of London” as it tries to renegotiate the terms of Britain’s EU membership, but wants a fair deal for all non-eurozone countries.

He said the other EU members have accepted the principle of a renegotiation and that discussions are now moving into a technical phase.

We are looking for a fair deal for non-euro members, including the United Kingdom.

We don’t want to be part of ever-closer union.

We are getting into specific discussions, technical discussions with the EU Commission and the Council.

He promised that this autumn more details will emerge as the EU talks move into a new phase.

Updated

An important part of the renegotiation is the relationship between non-euro and euro members of the EU, Osborne said.

You can watch the Treasury Committee hearing live here.

George Osborne is being quizzed by the Treasury Committee. MPs are asking about Mark Carney’s remarks on Britain’s EU membership.

The chancellor said:

I agree with the speech the governor made. The analysis he outlined was that EU membership has helped create a more open and dynamic economy, but, and there’s a crucial but, developments in the eurozone mean we do need safeguards for the UK.”

That’s why the UK has embarked on negotiations to secure reforms of the European Union, he added.

As the governor pointed out it’s [EU membership] not an unalloyed good. It’s presented challenges.

The single market in financial services is on balance a good thing for the UK.

The government’s position is not that we are against immigration. We are for controlled migration.

Updated

JPMorgan economist Allan Monks has taken a closer look at Mark Carney’s Brexit speech, which said “ensured there was more than just one liberal Canadian taking the headlines this week”.

The speech will be seen as another foray by Carney into a heated political debate, and its tone comes across as friendly to the campaign for keeping the UK within the European Union - ahead of a referendum which is to be held before the end of 2017.

Accompanying the speech was a chunky 100 page BoE report discussing the impact of EU membership on the central bank’s policy objectives. Despite Carney earlier this week having described the report as “a bit of a yawner” it will not prevent some from asking whether the BoE should be taking a more neutral stance on such a highly charged political issue (especially after similar interventions by Carney on Scottish independence and climate change).

Carney emphasised the report is not a thorough quantitative review of the pros and cons of EU membership, but rather is designed to assess the impact of membership on the Bank’s policy objectives.

In doing so, however, Carney highlights the beneficial impact EU membership has likely had in lifting sustainable growth in the UK (through fostering greater competition, efficiency and openness in key markets). The flip side of this openness to Europe is the higher sensitivity to external shocks, although Carney believes policy makers in the UK have adequate capacity to deal with these challenges.

A key concern for Carney looking forward is that UK policymakers retain adequate flexibility and control over policy, even as euro area countries go through a process of greater integration and risk sharing in the wake of the financial crisis. Carney’s comments have clear parallels with the government’s position in the debate.

The assertion that EU membership is a net positive for the UK, with caveats that the terms of membership need to reflect UK domestic interests and flexibility, will go down well with the Prime Minister - who seeks to renegotiate the terms of membership ahead of the referendum vote, and remove a requirement for the UK to commit to ‘ever closer union’.”

What difference could the BoE’s intervention make? The opinion polls suggest that the result of the referendum will be very close.

Our view has been that opinion will shift as the campaign heats up, with polls indicating a comfortable lead for the campaign to remain within the EU. While a natural status quo bias is central to this view, it also reflects our belief that the “in” campaign will gain the backing of at least a majority in the business community.

This week the CBI - which represents a broad cross section of small and large businesses - moved off the fence by coming out in support for the UK staying within the EU. The rhetoric behind Carney’s remarks put the BoE in the same camp, even if the Governor stops short of offering an explicit endorsement. The impact of these interventions may not be visible in the opinion polls right away, but we would expect them to grow in significance as the referendum draws closer.”

The ONS said retail sales will add 0.1 percentage points to overall economic growth in the third quarter, boosted by beer sales during the Rugby World Cup.

Tills are ringing on the high street: The breakdown of the retail sales figures showed that household goods retailers saw the biggest increase in sales last month, of 4.7%. Supermarkets and other food stores posted a 2.3% rise. Petrol sales were also strong, up 3.8%. However, clothes and shoe retailers did not have a good month, reporting a 0.9% drop.

Excluding petrol, overall retail sales rose by 1.7% in September.

The Rugby World Cup boosted retail sales last month, according to statisticians.

Kate Davies, ONS head of retail sales statistics, said:

Falling in-store prices and promotions around the Rugby World Cup are likely to be the main factors why the quantity bought in the retail sector increased in September at the fastest monthly rate seen since December 2013. The retail sector is continuing to grow with September seeing the 29th consecutive month of year-on-year increases.”

Average store prices (including petrol stations) fell by 3.6% in September from a year earlier, the 15th consecutive month of year-on-year price falls. It was the joint-lowest reading since the series began in 1988.

Updated

Sterling has hit a one-month high of 72.95p against the euro on the strong retail sales figures, up 0.8% on the day. Against the dollar, the pound climbed to $1.5510, up 0.5% on the day.

Updated

UK retail sales jump 1.9%, biggest rise since end 2013

News flash: UK retail sales jumped 1.9% in September from the previous month – the biggest rise since December 2013, according to the Office for National Statistics.

Bank of England paper analyses positive impact of migration

A Bank of England paper on EU membership analyses the positive impact of migration, as Jonathan Portes, director of the National Institute of Economic and Social Research, notes. Click on the link in his tweet to read the paper. It says:

Openness to labour flows – via migration – can allow an inflow of skills not otherwise available in the domestic economy. Ortega and Peri (2014) find that migration boosts long-run GDP per capita, acting both through increased diversity of skills and a greater degree of patenting. At the firm level, several studies further find that migration has a positive impact on productivity by diversifying the high-skilled labour employed by firms.”

Full BoE EU paper notable (even more than Carney speech) for positive analysis of impact of migration (see eg p 37): https://t.co/5KCEST1VIL

— Jonathan Portes (@jdportes) October 21, 2015

Updated

Round-up of headlines this morning, Carney's speech overwhelmingly interpreted as endorsement of EU membership. pic.twitter.com/GPRCUuxdCz

— Mike Bird (@Birdyword) October 22, 2015

Mark Carney's EU speech: the In and Out camp will each find lines to support their argument in the referendum battle https://t.co/FnjJpfgmRG

— Financial Times (@FT) October 21, 2015

Updated

In other news, Britain’s competition watchdog said highstreet banks will be forced to encourage their customers to switch to rivals. Switching could potentially save bank customers £70 a year, it said.

But consumer groups called on the Competition and Markets Authority to take tougher action to inject competition into banking, after it refrained from more radical measures to break up the biggest players. The market is dominated by the big four banks – Lloyds Banking Group, Royal Bank of Scotland, HSBC and Barclays – which together control 77% of the current account market.

Would Carney have said anything on EU unpalatable to government? No way. Should have said nothing, or issued "non-independent" disclaimer

— Gabriel Sterne (@GabrielSterne) October 22, 2015

Major intervention, stronger than the one on scotland: “@SkyNews: Carney: EU Has Made UK 'Dynamic And Stronger' https://t.co/DofxpUuUTG”

— Faisal Islam (@faisalislam) October 21, 2015

"Carney has not had to live with the EU for 40 years, and when his time is up, he'll go home…" — CrocodileGunnD https://t.co/wKyxxGOCsU

— David Gunn - UKIP (@DavidAGunn1) October 22, 2015

The prime minister and the chancellor both welcomed the governor’s comments last night.

Mark Carney's impressive speech right to argue that we need safeguards for non-euro countries like Britain in the EU

— George Osborne (@George_Osborne) October 21, 2015

An important speech from Mark Carney - making clear where reform is needed in Europe, as well as the benefits of the single market.

— David Cameron (@David_Cameron) October 21, 2015

Updated

Howard Archer, chief UK and European economist at IHS Global Insight, said:

Despite Mark Carney’s stressing that his speech and the BOE report is not a comprehensive view of the pros and cons of UK membership of the EU, our strong suspicion is that the pro-EU membership camp will find more to grab hold of and champion than the Out camp.

Carney said Britain was possibly “the leading beneficiary” of the EU’s single market, and that being in the bloc had been one of the drivers of its strong economic performance in the four decades since it first joined.

He made some positive remarks on the free movement of labour, observing that it “can help better match workers with firms, alleviating skill shortages and boosting the supply side of the potential growth rate of the economy.”

In addition, he noted that the UK has been the top recipient of foreign direct investment in the UK since the single market was established in 1992.

Updated

However, Carney’s intervention is also likely to be seen as strengthening David Cameron’s hand in negotiations on reforms with Britain’s EU partners. Carney urged the prime minister to demand “clear principles” to safeguard Britain’s interests outside the euro, as he warned that botched European integration could threaten financial stability.

Lawson slams Carney for wading into EU debate

But former chancellor Nigel Lawson slammed the Bank of England governor for wading into the debate on EU membership, saying his remarks were “regrettable”.

Bank of England governor Mark Carney's remarks about the EU were "regrettable" says Nigel Lawson pic.twitter.com/5KH3vqrGVQ

— BBC Radio 4 Today (@BBCr4today) October 22, 2015

The Spectator’s Coffee House team agreed.

Mark Carney should avoid the #euref and stick to plain monetary economics - @VanderWeyer https://t.co/gCCBcaTAdT pic.twitter.com/Qg7kE6r1Hr

— Coffee House (@SpecCoffeeHouse) October 22, 2015

Updated

Catherine Bearder MEP, chair of the Liberal Democrat EU referendum campaign, was quick to seize on Carney’s comments:

The Bank of England’s intervention confirms what we already know: being in the EU brings huge benefits to the UK economy.

Those calling for EU exit have failed to present a credible alternative that would protect the economy and secure jobs.

Instead of retreating to the side-lines, Britain should stay and lead reform in Europe from within.”

More on Carney’s speech on EU membership at St Peter’s College in Oxford last night. The governor concluded:

Overall, EU membership has increased the openness of the UK economy, facilitating dynamism but also creating some monetary and financial stability challenges for the Bank of England to manage. Thus far, we have been able to meet these challenges.”

You can read the speech on the Bank of England’s website, and watch the webcast.

ECB chief Draghi to hint of more QE

Good morning and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and the business world.

Policymakers from the European Central Bank have gathered in Valletta, Malta, for their monthly policy meeting (the governing council occasionally departs from its Frankfurt HQ to meet in other parts of the eurozone). The ECB is widely expected to keep its key interest rates unchanged along with its stimulus programme, despite fears over deflation.

But ECB president Mario Draghi may well strike a dovish tone again, and hint at further action towards the end of the year. Falling consumer prices (they slipped by 0.1% in the eurozone in September) and fears over the world economy suggest the central bank will ease policy at some point, unless things improve.

At the last press conference on 3 September, Draghi pointed to “renewed downside risks” to eurozone growth and inflation prospects, reflecting concerns about the outlook for emerging markets. He said that the ECB stood ready to adjust the size, composition or length of the QE programme if necessary.

Investec economist Chris Hare said:

Despite the QE teasers offered last month, our view is that Mr Draghi will not pull the trigger for now. In part, that is because developments since the then have seen a mixed bag, rather than an obvious worsening in conditions.

We still think that additional QE will be appropriate at some point, given global growth risks and the weakness of eurozone inflation (we are fairly agnostic on whether it will come in terms of size, composition or duration). More natural trigger dates would be the December, or perhaps next March’s, policy meeting. That would allow the ECB to announce the expansion alongside updated forecasts. December is also the month where we think the Federal Reserve will start raising rates: that, alongside a QE boost announcement, might give the euro a double kick down, offering a double whammy of stimulus to get inflation back on track.”

European stock markets are set to open lower ahead of the ECB’s decision, which will be announced at 12.45pm UK time, followed by Draghi’s press conference at 1.30pm.

Over here, Bank of England governor Mark Carney gave his “Brexit” speech in Oxford last night. He said that EU membership opened up the UK economy and made it more dynamic, although he added that it also left it more exposed to financial shocks like the eurozone debt crisis.

Updated