With this, we are wrapping up for the day. Good-bye and thank you for all your great comments. We’ll be back tomorrow.

Commissioner Jonathan Hill, the EU’s financial services chief, said:

Europe’s economy is about the same size as America’s, but our equity markets are less than half their size. In the US, SMEs get about five times as much funding from the capital markets – or non-bank financing - as they do here in the EU.

And if our venture capital markets were as well developed as they are in the US, companies could have raised an extra EUR 90 billion over the past five years. And perhaps even more importantly, the differences that there are between EU Member States are greater than the differences between the EU and the US.

So I think that if we can build stronger more sustainable capital markets and remove these barriers to cross-border investment, that there would be very clear benefits.”

The European Commission published its action plan on the Capital Markets Union initiative today, as expected, to create a “true single market” for capital access across the core 28 EU member states.

The Bank of England said in response:

We consider this Action Plan to be a further important step in moving closer to a single, integrated capital market in the EU, although we are yet to review the Commission’s detailed proposals. CMU requires carefully planned measures combining early quick wins to maintain momentum and sustained effort over a number of years, all in a very wide range of areas, and we therefore welcome the Commission’s step by step approach.

In the short term, the proposed Regulation on a European framework for simple, transparent and standardised securitisation, represents a significant milestone. Given the potential implications for financial stability at European and domestic level, we have worked with the European Central Bank to promote a sustainable model of securitisation and support the European Commission’s proposal on an EU framework for securitisation as part of the longer-term objective of growth in stable, market-based financing markets alongside bank lending.”

Updated

Over in Greece, newly re-elected prime minister Alexis Tsipras has predicted that the crisis-plagued country could soon be returning to international markets – if a deal on its debt burden is reached by the end of the year. Our correspondent Helena Smith reports from Athens:

Greece’s return to the capital markets from which it has been shut would essentially mark the end of its great economic crisis.

Barely ten days after his triumphant return to power – and before his new administration has even had time to make its policy statements before the Greek parliament – Alexis Tsipras has announced that his government’s goal is to return to markets once it has sealed a deal over its monumental debt.

In an interview with the Wall Street Journal – that has reverberated widely through the Greek media this afternoon– the leftist leader said: “The goal is to return to the markets … if there is a good decision on the debt issue, Greece could return to markets shortly after debt restructuring.”

At more than €320bn – and just over 180% of GDP - Greece’ s debt load is by far the highest in Europe with the International Monetary Fund repeatedly saying that debt relief is imperative if the country’s shattered economy is ever to recover.

Talks aimed at debt restructuring are scheduled to begin once international creditors complete a much-anticipated review of the economy later this year.

Speaking in New York, where he has been attending the UN General Assembly, Tsipras also said fiscal targets outlined in the country’s latest bailout agreement – the third since its near brush with bankruptcy in late 2009 – were likely to be derailed by government efforts to cope with the migrant and refugee crisis that is also afflicting Greece. In the event that the crisis worsened the Greek premier said Athens would call on its partners to relax budget plans.”

Updated

$11tn wiped off global markets in worst quarter since 2011

Global markets have suffered their worst quarterly performance since the depths of the eurozone crisis in 2011, with an estimated $11tn (£7tn) wiped off the value of world shares, despite a bounce today. Our markets correspondent, Nick Fletcher, writes:

After a summer of wild swings, sparked by growing fears of a slowdown in China, leading shares have slumped from the record highs of a few months earlier, and are on track for their second quarterly decline in a row.

The MSCI all-country world index, which monitors 23 developed and 23 emerging markets, has fallen nearly 11.5% since 30 June, marking its poorest quarterly outcome since the three months to September 2011.

The FTSE 100 index, which hit a record high of 7103 in April, fell below 6,000 during the quarter and is down 7% over the three months despite a 152 point bounce on Wednesday to 6061.

During the quarter the UK’s leading index has seen £117bn wiped off its value. Again, this is its worst performance since September 2011 when it lost 13.7% during the quarter.

The poorest performer is the Shanghai composite index, down 26% since the start of July and suffering its worst quarter since 2008.”

Markets have shrugged off warnings from IMF chief Christine Lagarde about the slowing world economy and rallied on the last day of a dismal quarter. Worries over Greece’s debt crisis gave way to new fears over China’s economic slowdown and market turmoil during the past three months.

Most European indices rose more than 2% today, while stocks on Wall Street leapt over 1%.

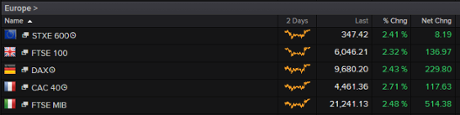

FTSE 100 index in London up 2.58%, or 152.37 points, at 6061.61

Dax in Frankfurt up 2.2% at 9660.44

CAC in Paris up 2.57% at 4455.29

Updated

“There was no sign of slowdown this afternoon, with a 200 point jump for the Dow Jones continuing the Western indices’ attempts to end this most awful of awful quarters with a bang instead of a more apt whimper,” says Connor Campbell, financial analyst at Spreadeax.

Perhaps this evening’s comments from Janet Yellen will provide more insight into what the US markets want at the moment; when the Fed chair suggested last week that a rate-hike will most likely occur in 2015 the American indices surged on the signs of some much-needed clarity. It will be interesting, then, to see if the markets have a similar reaction if Yellen drops any newsworthy nuggets of information into her speech in St Louis.

With the Dow continuing the end of quarter party, the European indices could maintain the muscular, if meaningless, growth that began this morning. The UK’s supermarket sector, buoyed by better-than-expected profit-promising comments from Sainsbury’s, only widened its gains as the day went on, whilst the commodity stocks continued to rebound from Monday’s mayhem.

So that’s effectively it for another quarter. Not that things will be radically different at the start of Q4; the timeline for a US rate-hike is still non-existent, Volkswagen is still only at the beginning of a long and costly scandal, and, most importantly, the Chinese economy is still stalling, more (unneeded) evidence of which will likely arrive tomorrow in the form of the country’s manufacturing PMIs.”

Strong labour market data in the US lifted the dollar, while the euro was already under pressure from the eurozone’s return to deflation on the back of weaker oil prices.

The euro is trading 0.7% down against the dollar at $1.1170. It also dropped against the pound, by 0.6% to 78.83p.

Eurozone prices dipped 0.1% on the year in September after rising 0.1% the previous month, remaining well below the European Central Bank’s target of 2%.

Updated

Global equities are rallying on the last day of a bad quarter. Jasper Lawler, market analyst at CMC Markets, sums up today’s developments in the UK and European stock markets.

There was a healthy sense of relief about the move higher in European shares on Wednesday. For a minute there on Monday, stocks were on the precipice of another China-induced thrashing. The past two days have just not produced the catalyst for the follow-through to the downside.

A melt-up in copper prices which surged over 4% helped commodity-trader Glencore to another day of double-digit gains. Other mining stocks followed suit with Rio Tinto a top riser after the sale of its coal mine stake in Australia to New Hope. The mine sale gave Rio’s balance sheet a welcome boost in the context of fears of over-leverage in the sector.

Supermarket shares were the surprise leaders of the FTSE 100 after a well-received update from Sainsbury’s. Shares of Sainsbury’s jumped as much as 14% after the supermarket said profits would be “moderately” higher than expected this year. Profits at Sainsbury’s are still well down year over year but the slowing decline in like-for-like sales means 2015 profitability looks better than it did six months ago.

Sainsbury’s is a household name, and retail investors especially, will keep trying to pick the bottom before profits grow again. An unusually large part of Sainsbury’s float is being shorted for a large cap stock so there’s some big time short-covering going on. Even the smallest sign that the worst is behind the big supermarkets is likely to see double digit reactions in share prices like today.

The problem for the Big Four is that there doesn’t seem to be much letup from the discounters. Aldi is going all guns blazes with plans for online shopping and an aggressive store expansion in London expected to accelerate the discounter’s UK market share growth.”

The IMF chief concluded her speech by quoting from the organisation’s founding father, John Maynard Keynes. In the midst of the 1930s Great Depression, he wrote this:

‘It is common to hear people say that the epoch of enormous economic progress is over. But I believe that is a wildly mistaken interpretation of what is happening to us.

We are suffering not from the rheumatics of old age, but from the growing pains of over-rapid changes, from the painfulness of readjustment between one economic period and another.’

Keynes’s note of realism – and optimism – proved to be right, of course. I believe it is a fitting note on which to end.

Photograph: Hulton Getty

Updated

“So much for the diagnosis. What should be done?” Lagarde asks.

The risks can be managed by supporting demand, preserving financial stability, and implementing structural reforms.

Lagarde: Fed faces 'delicate balancing act'

Lagarde warned of a new “mediocre”.

If we put all this together, we see global growth that is disappointing and uneven. In addition, medium-term growth prospects have become weaker. The “new mediocre” of which I warned exactly a year ago – the risk of low growth for a long time – looms closer.

Why? Because potential growth is being held back by low productivity, population aging, and the legacies of the global financial crisis. High debt, low investment, and weak banks continue to burden some advanced economies, especially in Europe; and many emerging economies continue to face adjustments after their post-crisis credit and investment boom.”

She said the US Federal Reserve faces a “delicate balancing act: to normalise interest rates while minimising the risk of financial market disruption”.

The prospect of rising U.S. rates has already contributed to higher financing costs for some borrowers, including emerging and developing economies.

This is part of a necessary adjustment in global financial conditions. The process, however, could be complicated by structural changes in fixed-income markets, which have become less liquid and more fragile – a recipe for market overreactions and disruptions.

Outside the advanced economies, countries are generally better prepared for higher interest rates than in the past. And yet I am concerned about their capacity to buffer shocks.

Why? Because many emerging and developing economies responded to the global financial crisis with bold counter-cyclical fiscal and monetary actions. By using these policy buffers, they were able to lead the global economy in its time of need. And over the past five years, they have accounted for almost 80% of global growth.

These policy actions generally went together with an increase in financial leverage in the private sector, and many countries have incurred more debt – a significant portion of which is in U.S dollars.

She warned that rising US interest rate and a stronger dollar could reveal currency mismatches, leading to corporate defaults.

Updated

WATCH LIVE: Christine Lagarde discusses IMF policy http://t.co/HntreaVVqH pic.twitter.com/RuwGFUSC9N

— Bloomberg TV (@BloombergTV) September 30, 2015

IMF managing director Christine Lagarde has warned that a deceleration in emerging markets will cause global economic growth to slow this year. Bright spots are the eurozone and Japan, where growth is picking up, and the US and the UK, where growth is still solid.

She said:

Global growth will likely be weaker this year than last, with only a modest acceleration expected in 2016.”

The good news is that we are seeing a modest pickup in advanced economies. The moderate recovery is strengthening in the euro area; Japan is returning to positive growth; and activity remains robust in the US and the UK as well.

The not-so-good news is that emerging economies are likely to see their fifth consecutive year of declining rates of growth.

India remains a bright spot. China is slowing down as it rebalances away from export-led growth. Countries such as Russia and Brazil are facing serious economic difficulties. Growth in Latin American countries, in general, continues to slow sharply. We are also seeing weaker activity in low-income countries – which will be increasingly affected by the worsening external environment.”

She warned that emerging markets could be hit by a prolonged period of low commodity prices.

The Washington-based organisation will release its World Economic Outlook next week.

Updated

Here’s a chart showing the performance of major commodities so far this year, via market watch. And no, oil and metals are not the worst performers:

YTD commodities tally: #Rice gains the most, #lumber falls the most. http://t.co/KUE6mPfAh7 (Chart: @AdamKoos) pic.twitter.com/SXNjGQn8xg

— Myra Saefong (@MktwSaefong) September 30, 2015

But there has also been some weak manufacturing data from the US.

After contractions in manufacturing in the Empire, Philadelphia, Richmond and Dallas Federal Reserve regions in recent weeks, Chicago is the latest area to disappoint.

The Chicago purchasing managers index for September fell from 54.4 in August to 48.7, well below forecasts of a level of 53. This is the lowest since May and the first contraction since June.

USA Chicago PMI announcement - Actual: 48.7, Expected: 53.0 pic.twitter.com/ruWR4Qis2S

— Spreadex (@spreadexfins) September 30, 2015

These figures come ahead of the ISM manufacturing figures for September, and do not bode especially well.

Consensus forecast for mfg ISM is 50.6, risk is for sub-50 print. As latest trade data reminds us, a strong dollar has real consequences.

— Carl Riccadonna (@Riccanomix) September 30, 2015

Updated

Dow Jones climbs more than 1%

Wall Street has indeed opened sharply higher, in tandem with other global markets which are recovering some ground from their recent slump, writes Nick Fletcher.

The US markets have also been helped by better than expected jobs figures with the monthly ADP report showing private employers added 200,000 jobs in September, up from 186,000 in August. That suggests that we could see a strong non-farm payrolls number on Friday, easing fears that the US economy is weaker than expected.

So the Dow Jones Industrial Average is currently up 1.2% or 203 points while the S&P 500 has added 0.7% in early trading.

But this will not stop global markets recording their worst quarterly performance since 2011, on growing fears about the state of the Chinese economy, a possible rise in US interest rates and the fallout from the VW emissions scandal.

My colleague on the Money desk, Miles Brignall, has done a helpful Q&A for UK consumers on which cars are affected by the Volkswagen emissions scandal and what they can do. You can read it here.

Which engines are involved?

Anyone with a EA189 engine – which to most buyers means 1.2 litre, 1.6 litre and 2.0 litres diesel engines. The affected vehicles were sold roughly between 2009 and 2014. This include Golfs, Passats, Škoda Octavias and Fabias, plus a host of Audis.

What about other models?

All petrol models, as well as V6 TDI and V8 TDI diesel engined vehicles, are unaffected, VW has said.

The FTSE 100 index is still up strongly, boosted by Sainsbury’s and other supermarket groups. Sainsbury’s said today it is trading well and expects to beat annual profit forecasts. It is the top riser on the share index, up 13% or 29.9p at 259.2p. Tesco is up 6.8% while Morrisons is 5.6% ahead.

The FTSE is nearly 2.1% ahead at 6032.41, a gain of more than 120 points. Germany’s Dax is up 2.4% and France’s CAC has gained 2.7%.

Over in the US, Wall Street is set to open higher after strong labour market data. The ADP National Employment Report showed that private employers added 200,000 jobs in September, more than expected and up from 186,000 in August. This has boosted expectations of a strong payrolls number on Friday – the official data.

Fed chair Janet Yellen and St Louis Fed president James Bullard are due to speak at a conference in St Louis later today, and markets will be looking for any clues regarding the timing of the first interest rate hike in years.

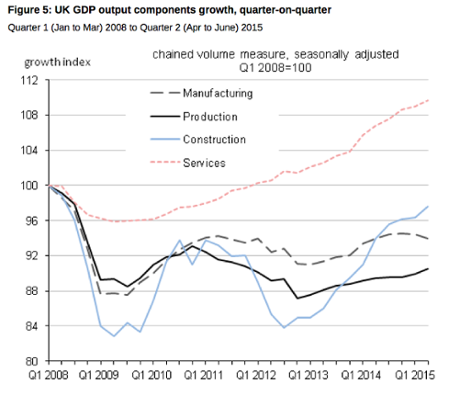

... But Britain’s recovery from its economic slump and the financial crisis has been slower than previous recoveries. Output is only 5.9% above its previous peak in early 2008. Adjusted for the growing population, it’s just 0.6% higher.

UK living standards pick up

Let’s have another look at today’s batch of UK data. Several bits of good news: living standards picked up, as companies spent more on wages and real household disposable incomes, adjusted for inflation, rose at the fastest rate in five years (3.7%).

Companies’ wage bills rose by 4.7% in real terms, the biggest rise since before the financial crisis (late 2007), although this is partly due to people working longer hours and extra pension payments, according to the Office for National Statistics.

Thanks to a surge in exports, Britain’s current account deficit with the rest of the world narrowed much more sharply than expected in the second quarter – to £16.8bn from £24bn in the first quarter – although this could be hard to sustain in light of the global economic slowdown. The deficit, which has been a worry for the Bank of England, dropped to a two-year low of 3.6% of GDP, after the UK’s trade deficit shrank to the smallest since 1998.

This is a welcome turnaround from last year, when Britain recorded its largest current account deficit on record at 5.1% of GDP, even though it was the fastest-growing G7 economy for a second year in a row.

The prospects for the UK’s economic recovery remain bright, judged Paul Hollingsworth, UK economist at consultancy Capital Economics.

Admittedly, the economic recovery does not look to have maintained this pace in Q3. Indeed, the CIPS/Markit composite PMI points to quarterly growth of a more modest 0.5%. However, we expect that the recovery will pick up pace again soon. After all, business and consumer confidence remains strong, credit is cheap and becoming more available, and households are yet to spend all of their windfall from lower energy and food prices. The upshot is that we remain upbeat about the prospects for the UK’s economic recovery.”

Updated

The UK transport secretary, Patrick McLoughlin, said:

The government’s priority is to protect the public and I understand VW are contacting all UK customers affected. I have made clear to the Managing Director this needs to happen as soon as possible.

The government expects VW to set out quickly the next steps it will take to correct the problem and support owners of these vehicles already purchased in the UK.”

The BBC have done “a brief history” of Volkswagen, with pics. You can read it here.

In the wake of the VW emissions scandal, Consumers International, the federation for more than 240 consumer groups around the world, is calling on all global carmakers to come clean about in-car technology and its impact on emissions tests.

They are also demanding an urgent review of emissions and fuel efficiency tests, and the introduction of stronger oversight of manufacturers testing, and independent testing where necessary.

Amanda Long, director general of Consumers International, said:

This scandal reflects long standing demands from many consumer organisations for more accurate testing of vehicles emissions and fuel efficiency and better oversight including independent testing where necessary. Regulators and manufacturers need to act urgently to restore consumers’ confidence and trust in the car industry. Car manufacturers must step up and prove they have had no such similar breaches, and then spell out what they intend to do in the future to ensure they are meeting consumers expectations of openness and transparency.

This crisis underlines the need to build stronger and more effective regulations and testing protocols that defend consumers’ rights and stop unscrupulous companies from cheating the system.”

Lunchtime summary

Time for a quick recap.

Eurostat reported that the eurozone Consumer Prices Index dipped by 0.1%, the first negative inflation reading since March.

Economists aren’t panicking, as the decline is mainly due to cheaper oil. But it could raise the chances of more aggressive stimulus measures from the European Central Bank soon.

ECB will extend timeline for QE in December, HSBC reckons. S&P thinks the ECB will more than double the programme. http://t.co/6ytDdoj4QW

— Katie Martin (@katie_martin_fx) September 30, 2015

2) World stock markets are about to post their worst quarterly performance since 2011.

Almost $11tn has been wiped off shares worldwide, after three months dominated by growing concern over the global economy.

European markets are rallying today:

But FXTM chief market analyst, Jameel Ahmad remains cautious.

There are just too many anxieties for investors right now with this including concerns over a complete lack of timing for a US interest rate hike, fears over China entering a deep economic downturn, continual growth concerns in both Europe and Japan alongside depressed commodity prices.

The timely combination of all these factors together is exactly why I am refusing to believe that the overall market sentiment is going to transform into a positive one as we enter the final quarter of the year.

3) Volkswagen has announced that almost 1.2m cars in the UK contained software designed to evade emissions tests. Drivers will hear more soon....

Julia Kollewe will guide you through the afternoon....

It’s been a rough quarter for metals prices as well as for shares.

Gold has shed around 4% since July, to $1,122 per ounce, while platinum has shed 15% - its worst quarter since 2008.

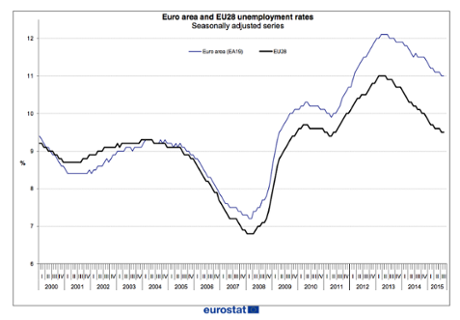

Hopes that Europe’s jobless crisis is easing have taken a knock today. The eurozone unemployment rate came in at 11% in August, not the 10.9% expected.

The Eurozone jobless rate in July has also been revised up to 11% from 10.9%, which is another disappointment.

The lowest rates were recorded in Germany (4.5%), the Czech Republic (5.0%) and Malta (5.1%), and the highest in Greece (25.2% in June 2015) and Spain (22.2%).

A reminder that Europe’s weak inflation rate is part of a broader pattern:

global inflation rate...edging down pic.twitter.com/CzPqrKnNNN

— RBS Economics (@RBS_Economics) September 30, 2015

Here’s a breakdown of the Volkswagen vehicles in the UK affected by the emissions scandal:

- Volkswagen Passenger Cars – 508,276

- Audi – 393,450

- SEAT – 76,773

- ŠKODA – 131,569

- Volkswagen Commercial Vehicles – 79,838

They’re all diesel models - VW says that its petrol cars are unaffected.

Updated

Volkswagen: UK customers will be contacted soon

Volkswagen says that the 1.1m UK drivers who own cars caught up in the emissions scandal will be contacted soon:

In the coming days, the VIN (Vehicle Identification Number) details of affected cars will be released to retailers.

In addition, a self-serve process for customers to check if their vehicle is affected will be set up.

Step by step, affected customers will be contacted, with details of a process to get their vehicles corrected in the near future. In the meantime, all vehicles are technically safe and roadworthy.

The company is aiming to present a technical solution to the crisis to authorities next month.

Volkswagen: 1.1m UK cars affected by emissions scandal

Breaking: Volkswagen has announced that over 1.1m cars designed to evade emissions testing were sold in the UK.

More than a million cars in the UK affected by Volkswagen scandal

— Graham Ruddick (@GrahamtRuddick) September 30, 2015

UK customers with affected VW cars will be contacted in next few days about fixing issue

— Graham Ruddick (@GrahamtRuddick) September 30, 2015

Updated

One month’s negative inflation isn’t enough to spur the European Central Bank into its quantitative easing scheme.

So argues Bill Adams, senior international economist at PNC Financial Services Group, adding:

Despite the year-ago decline in headline inflation, this report does not meet the definition of deflation that ECB President Draghi has repeatedly cited this year: A self-perpetuating decline in prices that occurs across a wide range of goods and services.

Analyst: Negative inflation is "disappointing" but not disaster

Today’s inflation report is “disappointing news” for the European Central Bank, says Howard Archer of IHS Global Insight.

A marked relapse in oil prices and very weak commodity prices first undermined and then reversed the upward trend in Eurozone consumer prices that had seen it move from deflation of 0.6% in January to inflation of 0.3% in May.

Archer adds, though, that core inflation (stripping out energy and food) remained at +0.9%.

It remains highly unlikely that Eurozone consumers will start to delay purchases in anticipation of falling prices; rather they are likely to continue to enjoy the boost to their purchasing power coming from mild deflation or low inflation.

Mario Draghi must be disappointed that his €60bn-per-month bond-buying spree hasn’t had a bigger impact.

The ECB launched its QE programme in January after inflation sagged to minus -0.6%. It did then turn positive in May, but has been stubbornly weak since:

#Eurozone back in technical #deflation. Inflation Rate Turns Negative as ECB Debates Stimulus http://t.co/TBab08lBwI pic.twitter.com/vUKnmhfLs9

— Holger Zschaepitz (@Schuldensuehner) September 30, 2015

ECB president Mario Draghi has already hinted that more stimulus measures could be needed to stimulate the eurozone; today’s inflation data means that’s more likely to happen.

But I suspect the ECB won’t be *too* alarmed that inflation has turned negative again, given that this is mainly due to cheap oil.

Lower energy costs are, on balance, a good thing for the wider European economy - and could leave consumers with more cash to spend on other goods instead.

Euro-area inflation did drop below zero in September but core measure remains stable and services inflation rose. Much better than it looks.

— Maxime Sbaihi (@MxSba) September 30, 2015

This is the first time in six months that the eurozone has experienced negative inflation:.

Here’s the details from Eurostat:

Looking at the main components of euro area inflation, food, alcohol & tobacco is expected to have the highest annual rate in September (1.4%, compared with 1.3% August), followed by services (1.3%, compared with 1.2% in August), non-energy industrial goods (0.3%, compared with 0.4% in August) and energy (-8.9%, compared with -7.2% in August).

Updated

Eurozone falls into negative inflation again

Here we go! Prices across the eurozone fell by 0.1% year-on-year this month, putting the single currency region back into negative inflation.

As explained in the introduction, this may raise the chances of the ECB increasing its stimulus programme in the next few months.

The weak oil price is the primary cause - energy prices fell by 8.9% year on year in September. Service sector and food prices did rise, though.

Euro area inflation down to -0.1% in Sept 2015 (Aug +0.1%) - flash estimate from #Eurostat http://t.co/O6MrTccMZm pic.twitter.com/c1JVlP6QNS

— EU_Eurostat (@EU_Eurostat) September 30, 2015

Euro area flash inflation: Food +1.4%, Services +1.3%, Other goods +0.3%, Energy -8.9% in Sept 2015 #Eurostat http://t.co/O6MrTcuonW

— EU_Eurostat (@EU_Eurostat) September 30, 2015

Updated

Some reaction to the UK growth data:

UK economy is 5.9pc bigger than pre-crisis peak, new ONS revisions show, up from 5.2pc previous estimate, as 2015 Q2 GDP confirmed at 0.7pc

— Philip Aldrick (@PhilAldrick) September 30, 2015

UK annual GDP growth revised down to 2.4% from 2.6%. Every one of 35 economists polled by @Reuters expected no change or upward revision.

— Jamie McGeever (@ReutersJamie) September 30, 2015

UK GDP in Q2 unchanged at 0.7% in final estimate; Current account deficit a lot smaller than expected (but still pretty massive) at £16.8bn

— Ed Conway (@EdConwaySky) September 30, 2015

Updated

Phew. Britain’s alarmingly wide current account deficit has narrowed.

The gap between what the UK pays out to the rest of the world and what comes back in dropped to just 3.6% of GDP in the last quarter, down from 5.2% in January-March.

Current account deficit was 3.6% of #GDP in Q2, down from 5.2% in Q1 http://t.co/xPzcqUsCgV pic.twitter.com/F11VViJe70

— ONS (@ONS) September 30, 2015

That’s still wider than economists would like, but it suggests the ‘forgotten deficit’ may be less of a threat to the recovery.

A much more reassuring UK current account deficit from the ONS.

— Duncan Weldon (@DuncanWeldon) September 30, 2015

UK 2014 growth revised down (a bit)

Britain’s Office for National Statistics has trimmed its estimate for UK growth last year.

It now believes the economy expanded by 2.9% - healthy enough, but not the 3% previously eyed.

The ONS also confirmed that UK GDP grew by 0.7% in the second quarter of 2015. That means the economy is 5.9% larger than its pre-crisis peak, driven by the service sector:

City analyst Louise Cooper says emerging market fears helped to wipe $11 trillion off global markets this quarter:

India is slowing, so much so the central bank cut rates earlier this week in a surprise move. China is slowing rapidly according to the data but its difficult to get a handle on exactly how much. Commodities prices are falling indicating this lack of demand.

The emerging markets have been important contributors to global growth over the years since the crisis, contributing something like 60% to global growth. The question is whether the US, Europe and Japan can grow enough to make up for their weakness? And what impact an emerging market slow down will have on the rest of the world? These are unknowns. We don’t even know how serious the slowdown. Andy Haldane of the Bank of England believes this is the third stage of the global crisis. But no one knows the answers to those questions yet. Thust markets are volatile and investors and traders nervous.

In a note today Macquarie bank writes that the price of rough diamonds has fallen and sentiment is weak due to “Weakness in global demand for jewellery and other luxury goods, in particular in emerging markets”. If even diamond prices are falling, that says a lot about demand!

There’s better news from Italy. The jobless rate has dipped to its lowest level since February 2013, dropping to 11.9% in August from 12% in July.

That’s a good sign, ahead of the eurozone jobs data in 45 minutes.

German unemployment total rises

Is the shine coming off Germany’s labour recovery?

Data just released shows that Germany’s unemployment total rose by 2,000 this month, on a seasonally adjusted basis. Economists had expected a drop of 5,000.

That still leaves the German unemployment rate at a post-reunification low of 6.4%.

#Germany #Unemployment Unexpectedly Rises in Sign of Economic Risks http://t.co/i3ozgUwJl5 via @aspeciale pic.twitter.com/Y3mj7qwrtI

— Forward Guidance (@ecoeurope) September 30, 2015

This screengrab shows the scale of this summer’s market rout:

European shares rally

Like a schoolboy scribbling his homework on the bus, European traders are making a late attempt to improve their performance in the last quarter.

Shares are rallying across Europe, as investors wonder whether this quarter’s huge selloff has been overdone.

In London, the FTSE 100 has gained 103 points or 1.75%. Sainsbury’s is leading the way after today’s upbeat statement:

Tasting Different...? UK supermarket optimistic on profit! What rally,biggest since 2007 for @sainsburys pic.twitter.com/E4WB4b5Tn1

— Caroline Hyde (@CarolineHydeTV) September 30, 2015

Shares in Glencore have jumped by 7%, after it reiterated that it can ride out the commodity downturn.

Our business remains operationally and financially robust - we have positive cash flow, good liquidity and absolutely no solvency issues.

The German DAX and French CAC are both up around 2.3%. Shares in Volkswagen are up almost 4%, after its new CEO promised to deliver a technical fix to remove the illicit software that allowed its cars to fool emissions testers.

This won’t make much of a dent in the huge losses incurred this quarter, though.

Updated

Bloomberg: $11tn wiped off global markets this quarter

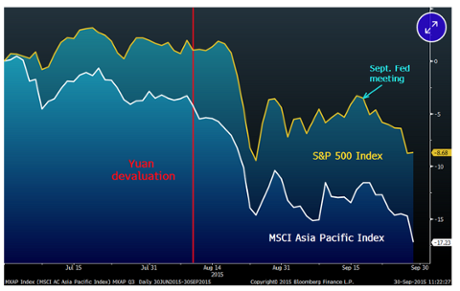

Wowsers. Bloomberg has calculated that this summer’s stock market rout has destroyed 11 trillion US dollars of value.

They identify two key factors -- China’s shock devaluation of the yuan in August, and the Federal Reserve’s decision not to raise interest rates this month.

Angus Nicholson of IG adds that German carmaker Volkswagen, and US presidential hopeful Hilary Clinton, also contributed to the selloff in the last 10 days:

In the wake of the worldwide selloff in equities that began in August, global markets have been in a heightened state of sensitivity. Rarely does one see so many major event-driven selloffs in quick succession. Last week the VW emissions scandal prompted a major selloff in European markets, carmakers and related companies worldwide.

Then Hilary Clinton, who had been planning to announce some new healthcare policies, jumped on the egregious price increase in a toxoplasmosis drug by new internet hate-target Martin Shkreli to decry the price of drugs in the US. This prompted a major selloff in healthcare and biotechnology stocks.

Updated

Bloomberg economist Maxime Sbaihi agrees that eurozone inflation could turn negative today, but doesn’t expect the European Central bank to panic.

Ready for negative inflation? Euro-area HICP released this morning after very weak German/Spanish readings yesterday. #ECB to look through.

— Maxime Sbaihi (@MxSba) September 30, 2015

Shares in supermarket chain J Sainsbury have surged by 11% after it told the City that it expects to beat profit forecasts this year.

Total sales across the company rose by 0.3%, suggesting the company is riding out the price war raging in the sector.

CEO Mike Coupe told investors that “volume and transactions grew”, while the drop in average basket spend stabilised.

My colleague Sean Farrell is on Sainsbury’s conference call now, and grilling Coupe about staff wages:

Sainsbury's CEO Mike Coupe says his staff take home about as much as Lidl and Morrisons staff will once they get the living wage.

— Sean Farrell (@farrell_s) September 30, 2015

Sainsbury's CEO Mike Coupe says expects that over time his staff will be paid more than the full living wage.

— Sean Farrell (@farrell_s) September 30, 2015

China’s stock market has endured a torrid quarter.

The Shanghai composite index just closed, having fallen 26% since the start of July after fears over the country’s slowdown sparked panic selling during the summer.

That, according to Reuters, is the worst quarter for Chinese shares since 2008.

Updated

UK house prices rise again

The north-south divide in house prices increased in the summer, as growth in London moved back into double figures, the UK’s biggest building society reports.

The latest monthly figures from Nationwide showed across the UK average prices rose by 0.5% in September, to a new high of £195,585. This brought the annual rate of growth to 3.8% - up from 3.2% in August.

And in London, house prices jumped by 10.6% -- up from 7.3% in the previous quarter.

That means the gap between London house prices and the rest of the UK was at its widest ever. At £443,399 the average price in the capital is more than three-and-a-half times the £124,345 paid in the north of England.

Markets suffer biggest quarterly losses since 2011

After a summer of wild swings, world stock markets are about to post their worst quarterly performance since the dark days of the eurozone crisis.

Fears over the global economy have hit equity values across the globe. Many of the main indices are facing double-digit losses since the start of July.

As Barclays analysts explain:

“Global equities are closing in on their worst quarter since 2011, with a number of factors fueling fears in an already jittery market, including weak global growth, driven by deceleration in emerging markets, particularly China,”

With one day to go, the FTSE 100 is down over 9%, closely followed by the Dow Jones industrial average. European shares are down around 11%, while Japan’s Nikkei has shed 14%.

Worst Q since 2011 pic.twitter.com/hLokctK0V8

— Guy Johnson (@GuyJohnsonTV) September 30, 2015

Updated

Introduction: Eurozone inflation could spark more ECB stimulus

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

We’re about to get a big clue about whether the European Central Bank will have to take new steps to stimulate the eurozone economy.

New consumer pricing data, released at 10am BST, is expected to show that inflation across the eurozone has subsided back to zero, from 0.1% in August.

But it could even turn negative -- as we already know that prices in Spain and Germany fell this month.

If prices are deflating again, there will be even more pressure on the ECB to reach for a bigger bazooka and expand its bond-buying programme.

Also coming up today....

The latest eurozone unemployment data is also released at 10am; that’s expected to show the jobless rate stubbornly high, at 10.9%.

In the UK, we get the final reading of second-quarter growth at 9.30am - probably confirming that GDP rose by 0.7%. The Office for National Statistics is also expected to revise its historical data, and could show that the economy performed better than expected.

We’ll also be watching Glencore; the mining and commodity firm is expected to meet with key bondholders today.

In the corporate world, Sainsbury’s are reporting financial results (they say they’re on track to beat forecasts).

Across in the eurozone, France’s finance minister, Michel Sapin, is due to present the nation’s budget this morning.

And after two rough days trading, the markets are expected to rally at the open.

Our European opening calls: $FTSE 5976 up 67 $DAX 9560 up 110 $CAC 4394 up 50 $IBEX 9486 up 92 $MIB 20918 up 192

— IGSquawk (@IGSquawk) September 30, 2015