European markets fall back

After a mini-revival by stock markets last week, a mixed bag of manufacturing data across the globe has given investors an excuse to take some profits on the first trading day of the new month. Purchasing managers data from China and the eurozone proved disappointing, while two surveys from the US pointed in different directions. So overall the final scores were:

- The FTSE 100 finished down 58.50 points or 0.89% at 6487.97

- Germany’s Dax dropped 0.81% to 9251.70

- France’s Cac closed 0.92% lower at 4194.03

- Italy’s FTSE MIB fell 2.1% to 19,369.03

- Spain’s Ibex ended down 0.99% at 10,374.4

On Wall Street, the Dow Jones Industrial Average is currently 17 points or 0.1% lower.

And on that note it’s time to shut the blog for the evening. Thanks for all your comments, and we’ll be back again tomorrow.

Poul Thomsen, who was head of the IMF team for Greece, has been appointed as director of the European department.

He succeeds Reza Moghadam who resigned from the IMF in July this year. The fund said:

During the global financial crisis, Mr Thomsen was mission chief for Iceland, the first advanced country to suffer the consequences of the crisis. He then led the IMF’s programs for Greece and Portugal. He was appointed Acting Director of the European Department on July 30, and has retained oversight of the IMF’s relations with Greece and its European partners, as well as other IMF programs in Europe—including Romania and Ukraine.

He did a great job RT @SpiegelPeter IMF announces Poul Thomsen, head of #Greece IMF team, is new head of IMF's European Dept.

— MineForNothing (@minefornothing) November 3, 2014

Updated

Rob Carnell at ING Bank, commenting on the ISM report, suggested the strong data could revive thoughts of an earlier than expected rise in US interest rates:

The October manufacturing ISM survey for the US was very strong, coming in at 59.0, a rate historically consistent with a GDP rate of about 5%, though to put it into perspective, we don’t think the underlying rate of GDP growth is anything like that strong, though manufacturing is clearly doing better than the larger, service sector of the economy. Cheap energy is doubtless to thank for part of this outperformance.

In terms of Friday’s payrolls release, the employment index rose to 55.5 from 54.6. Order backlogs also rose sharply, suggesting a need for greater investment or employment, or probably both in the months ahead.

Interestingly, although new orders were up strongly to 65.8 from 60.0, the new export orders series actually fell slightly to 51.5 – in keeping with the weaker external environment, and suggesting that most of the US growth momentum currently comes from within.

Over the next few days, we look for similar, though perhaps not so pronounced strength from the non-manufacturing ISM and ADP surveys of employment. With the Fed seeming to take a more hawkish stance with their latest statement, this could encourage thoughts of earlier Fed tightening than currently priced, pushing up bond yields, particularly at the front end of the yield curve, and providing the US dollar with further support.

US manufacturing stronger than expected, says ISM

Meanwhile the Institute of Supply Management has estimated that US manufacturing rose more strongly than expected.

Its index of national factory activity rose to 59 in October from 56.6 in September, and better than the 56.2 expected by a Reuters poll of economists, helped by a rebound in new orders. That brought the index back to the level seen in September, which had been the highest since March 2011.

Ahead of Friday’s non-farm payroll numbers, the employment index recovered to 55.5 in October from 54.6 the previous month.

ISM New Orders Seasonally Adjusted vs Unadjusted http://t.co/3I4J66ksWQ pic.twitter.com/JnTza46ZUi

— zerohedge (@zerohedge) November 3, 2014

The dollar has ticked up after stronger-than-anticipated October ISM Manufacturing PMI data (59.0 vs. 56.5) eyed ^MW

— FOREX.com (@FOREXcom) November 3, 2014

Updated

And here comes the first of two rival US manufacturing surveys.

In October, the sector slowed to its lowest rate of growth since July, according to Markit, hit by a decline in exports as the eurozone slump continues and emerging markets slow down.

Markit’s US manufacturing purchasing managers index fell to 55.9 from 57.5 in September, a further decline from the preliminary reading of 56.2 on October 23.

The index of new orders dropped from 59.8 in September to 57.1, its lowest level since January.

Tim Moore, Markit senior economist, said:

October’s survey highlights that the revival in U.S. manufacturing conditions remains on track. Production levels expanded at an impressive rate by international standards and overall momentum is still stronger than the post-recession trend.

However, the latest figures indicate that the recovery has lost some intensity at the start of the fourth quarter, reflecting subdued export demand from the euro area and key emerging markets.

Updated

A late lunchtime summary

Time for a recap.

Italy and France both saw their manufacturing sectors shrink last month, as the eurozone economy continued to struggle.

Markit’s monthly PMI surveys showed that European factory activity rose a little in October, thanks to growth in Germany, Spain and Ireland.

But there were few bright spots. New orders fell across and firms in Italy and France cutting jobs as activity contracted.

No Cheer.Italy & France grim. Spain grows but jobs elusive, Germany hangs on in there @graemewearden #PMI #eurozone http://t.co/QdtYjDxnBu

— Annajoy David (@AnnajoyDavid) November 3, 2014

And the overall manufacturing PMI was only just above the 50-point mark separating expansion from contraction:

Markit warned that:

The eurozone manufacturing sector remained in a state of near-stagnation in October, as weak demand continued to restrict growth of both output and employment across the currency union.

In Britain, though, manufacturing growth beat forecasts despite the European slowdown.

UK manufacturers cranked up production in October to meet growing domestic demand but export orders fell again as strains in the eurozone continued.

Full story: UK manufacturing boosted by domestic demand, survey shows

Mike Rigby, head of manufacturing at Barclays, warned that the UK would suffer if the eurozone economy did not improve:

“Overseas markets have long been viewed as a crucial component for improved UK economic growth but this current lack of penetration could hamper the ability of manufacturers to lead the recovery as we move towards 2015.”

The day began with mixed PMI reports from Asia, with manufacturing growth falling in China, South Korea and Indonesia.

And this has pushed European stock markets down -- the FTSE 100 is currently off 28 points, or 0.44%, at 6517.

In the eurozone...

Greek bond yields have climbed above the 8% mark.... as an EU official told reporters that Athens could not achieve a ‘completely clean’ bailout exit.

In the corporate world....

HSBC has set aside £236m to cover settling its role in the foreign exchange-rigging scandal.

Ryanair’s shares are now up 9% today, after it raised its profit forecasts. CEO Michael O’Leary says that the new strategy of trying to treat customers well is paying off.

Not everyone is impressed:

@graemewearden @BusinessDesk Now there's a surprise. Get rid of the sexist advertising and he'll be ready to face the challenge of the 1980s

— Graham Salisbury (@grahamsalisbury) November 3, 2014

And Britain’s living wage has gone up by 20p per hour...

With that I’m handing over to my colleague Nick Fletcher.

Updated

Britain’s living wage -- the minimum amount needed to provide a basic, decent, standard existence -- is going up.

Around 35,000 low-paid workers in the UK will benefit from the 20p per hour increase, to £7.85. But as my colleague Katie Allen explains, the voluntary scheme still faces opposition:

There has been a big rise in companies signing up and now more than 1,000 employers are accredited by the scheme. But low pay remains prevalent in Britain, campaigners warn, with bar staff and shop assistants among the most likely to live “hand to mouth”.

Full story: Living wage increases to £7.85 an hour

This @LivingWageUK ad near Piccadilly Circus is a great lesson in how to de-wonk-ify cost-of-living politics: pic.twitter.com/Fxq22V1R5e

— Jeremy Cliffe (@JeremyCliffe) November 3, 2014

A reminder that Greece remains a tense place - students and university staff have been demonstrating in Athens today against the government’s education reforms, and budget cuts.

Highschool students protest in Athens against govt's changes in education #Greece pic.twitter.com/C84eSziUTh

— dromografos/Skar_ (@Skar_) November 3, 2014

#Greece: University staff protest now in Athens pic.twitter.com/K2AXdK7fup

— dromografos/Skar_ (@Skar_) November 3, 2014

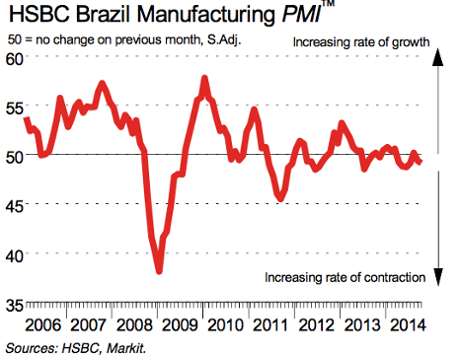

Conditions in Brazil’s factory sector have worsened, according to a survey by HSBC and Markit just released.

The Brazilian manufacturing PMI fell to 49.1, from 49.3 in September, showing the sector shrank again. Output and new orders declined at a faster rate, and firms cut staffing levels.

Production also fell, as manufacturers “adjusted their output according to the generally depressed state of the market and the negative influence of the election”.

It is the sixth month of contraction since the beginning of the year; Andre Loes, HSBC’s chief economist for Brazil, warned that conditions are tough.

The decline was spread through almost all of the sub-indexes, with output particularly weak. It suggests another challenging quarter for manufacturing.”

Operating conditions in #Brazil deteriorate for sixth time in past 7 months. #PMI at 49.1 (49.3 in Sep) http://t.co/1wS1rDlO5l

— Markit Economics (@MarkitEconomics) November 3, 2014

A quick markets catch-up -- and the main European indices are mostly in the red after an uninspiring morning’s trading.

After a big rally on Friday (after Japan boosted its monetary stimulus plan), some investors have returned to fretting about growth prospects.

The weak PMI reports from Asia (see 7.37am) and the eurozone (see 9.15am) haven’t provided much cheer:

Back to the future as Syriza scares markets again, pushing Greek bond yield above 8% http://t.co/oGfpRVzZXL pic.twitter.com/n7jdWrrhxQ

— Robin Wigglesworth (@RobinWigg) November 3, 2014

Greece’s government debt is under pressure again this morning, pushing the yield on its 10-year bonds up to 8.2%, from 8.1% on Friday night.

Uncertainty over Greece’s bailout plans and its political situation (as discussed earlier) continue to hit confidence.

These high bond yields make it increasingly likely that Athens will have to agree new restrictions or budget commitments in return for a credit line.

Speaking of Brussels....

I'm never sure that putting a large photo of yourself on your own building is a good idea #TeamJunckerEU pic.twitter.com/stfTRQy0gY

— Chris Morris (@BBCChrisMorris) November 3, 2014

Eurasia: Greece to get precautionary credit line in December

Mujtaba Rahman of Eurasia Group agrees with our unnamed EU official that Greece will not be given a completely clean exit from its bailout.

“Recent market turbulence”, which saw Greece’s borrowing costs jump, have nixed Athens’ hopes of going it alone, he says.

Instead, Rahman predicts that Greece will sign up for a precautionary credit line with the European Stability Mechanism, perhaps early as next month.

He writes:

Recent market turbulence has changed the calculus in Athens, Brussels and Berlin, increasing the chances of agreement on a European Stability Mechanism Precautionary Credit Line (ECCL) in early December.

Here’s the logic:

Firstly, the Troika and Eurogroup will not, indeed cannot, fully internalize the emerging difficulties in Greece’s domestic political situation by offering the government a free pass. Hence to qualify for the ECCL, the coalition will have to promulgate VAT, pension and labour market reforms over the next several weeks in order to conclude the fifth review. Secondly, the fact the ECCL will not require new money but rather be based on now unused HFSF funds [money set aside to recapitalise Greek banks] will make passage easier in Conservative Northern Eurozone parliaments.

Finally, the Greek government will (on some level) be able to argue this deal is very different from its two previous bailouts. This is because several elements of the ECCL will probably be repackaged and presented in a way that helps the government minimize domestic political and public blowback. For example, the dreaded “Memorandum of Understanding” containing Greece’s reform commitments could be relabeled a “partnership agreement”; quarterly visits of Troika officials could become bi-annual ones, take place in Paris not Athens, and be attended by deputies, not senior officials, from the participating Troika institutions -- the EC, ECB and also the IMF.

Rahman also forecasts that Greece will head to the polls again in March, and that the anti-austerity opposition Syriza party will form the next government.

He says:

We remain of the view early national elections will take place in March next year, resulting in a Syriza-led coalition government.

The likely agreement on the ECCL (especially but not only the aspect of IMF financial participation) will play into [Syriza leader Alexis] Tsipras’ hands, who will reiterate Syriza’s position that they will not accept any agreement between the government and European lenders that creates a “negative fait accomplis”.

Tsipras will argue Samaras got nothing from European creditors for all of the reforms that have been pursued to date (and still need to need to be pursued) -- no clean exit; no debt relief.

Updated

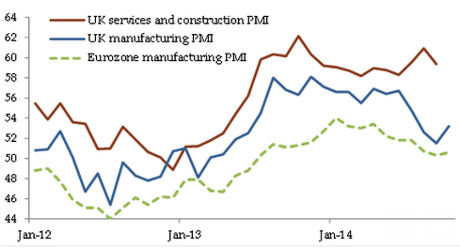

How UK factories have outperformed Europe

This chart, from Berenberg bank, shows how the UK’s manufacturing sector (in blue) has grown faster than the eurozone’s (green) since the start of 2012:

Berenberg economist, Rob Wood, warns that Europe’s problems could yet hurt the UK:

The risk to the UK from the Eurozone is not the direct impact of weak exports, which Britain could easily ride out, but rather the potential for uncertainty to infect UK domestic demand as companies perhaps put off investments.

Wood also reckons that today’s PMI data shows the eurozone economy may be stabilising:

With the conflict in Ukraine now frozen confidence on the continent could stabilise soon.....external risks seem to be fading, and we expect a clearer turn-around in Eurozone confidence to begin before the end of the year.

Updated

EU: Greece 'highly unlikely' to achieve completely clean bailout exit

Over in Brussels, an unnamed EU official is briefing the press pack that Greece is ‘highly unlikely’ to exit its bailout package without some new arrangement.

Eu official says a complete clean exit of #Greece to the markets is highly unlikely. Have to explore other options.

— Maria Aroni (@aronimar) November 3, 2014

"A completely clean exit is highly unlikely," says sr #EU official on #Greece bailout. #eurogroup

— Peter Spiegel (@SpiegelPeter) November 3, 2014

Last month, the IMF suggested that Greece might need a precautionary credit line -- ie, a safety net tied to various commitments or restrictions.

UK factory growth accelerates, but export orders decline

Britain’s factory sector has outperformed the eurozone, despite a drop in demand from overseas.

The UK manufacturing PMI rose to a three-month high of 53.2 last month, up from 51.5 in September. That shows faster growth, and beating expectations.

However it’s not all rosy -- UK firms reported a drop in new export orders, for the second straight month.

Markit says that UK manufacturing sector made a bright start to the final quarter of 2014, despite the weakness of the euro area.

The pick up in growth mainly reflected the resilience of the domestic market, as overseas demand was impacted by the ongoing economic weakness of the eurozone and the euro-sterling exchange rate.....

Many UK firms reported a drop in demand from the eurozone; some also cited slower growth in other key markets, such as the US and China.

David Noble, CEO at the Chartered Institute of Procurement & Supply, comments:

“The manufacturing PMI this month received a domestic-fuelled boost as the index reported growth at a three-month high. With new export business declining, it was the UK picking up the new business tab, as the Eurozone continued to experience weakened economic growth with the added punch of unfavourable exchange rates.”

France and Italy both remain “serious sources for concern”, says Howard Archer of IHS Global Insight, who has rapidly digested today’s PMI reports.

Archer adds:

Heightened geopolitical tensions particularly related to Russia/Ukraine have weighed down on confidence across the Eurozone, reinforcing still challenging conditions in many countries and this has likely caused some orders to be delayed or even cancelled.

Meanwhile, credit conditions are currently still tight in many countries, unemployment is still elevated and seems likely to creep down at best over the coming months, private and public debt levels remain high in several countries, while consumer purchasing power is constrained by generally limited wage growth.

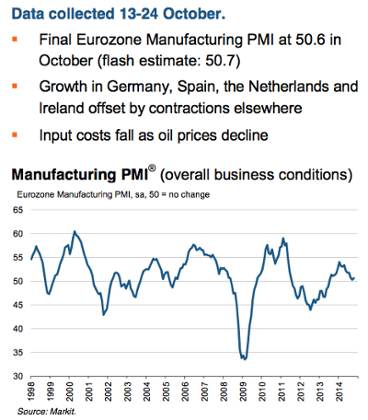

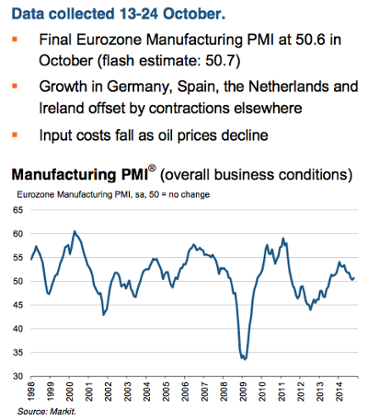

Eurozone manufacturing struggles to grow, says Markit

The eurozone manufacturing sector remains wedged in near-stagnation, according to analysis of this morning’s surveys from firms across the region.

The growth in Germany and Spain (details start here) was wiped out by Italy’s disappointing return to contraction, and the ongoing weakness in France.

Many companies reported a decline in new orders.

It suggests that the eurozone economy is struggling to grow after grinding to a halt this summer.

As Markit puts it:

Weak demand continued to restrict growth of both output and employment across the currency union.....

The downturn in France accelerated and Italy fell back into contraction. The rate of deterioration in Greece eased, while Austria fell further from the rest of the pack as its PMI sank to a two-year low

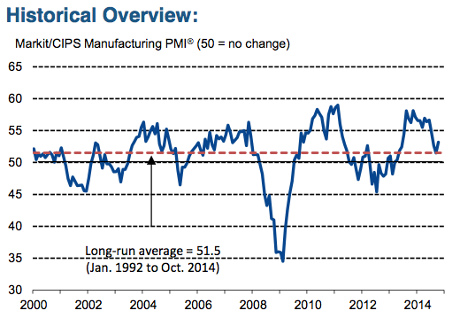

The overall Eurozone manufacturing PMI inched up to 50.6 in October, up from September’s 14-month low of 50.3. That does show a small increase in activity, but not enough to pull Europe out of its malaise.

Average input costs and output charges both fell; partly due to lower energy prices, and partly due to firms cutting prices to win (or retain) business.

Here’s the key points:

Rob Dobson, Senior Economist at Markit, says eurozone manufacturing is struggling to recover from its mid-year slowdown.

Manufacturing is unlikely to provide any meaningful boost to the currency union’s anaemic GDP growth.

“Perhaps most worrying is the trend in new orders, a key bellwether of future output growth, which declined for the second month running. It is hard to see any significant near-term boost to performance while market demand remains insipid and beset by lacklustre domestic conditions, slowing export growth and ongoing economic uncertainties.

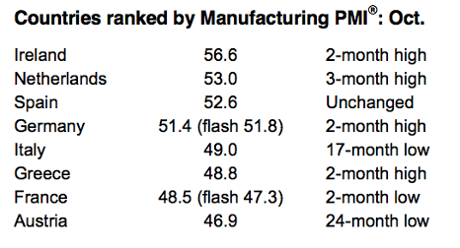

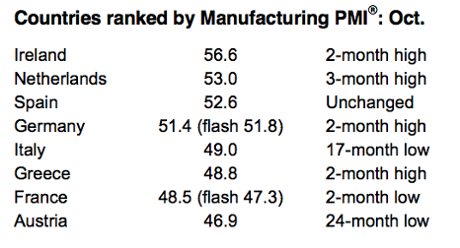

“National growth disparities also remain a concern, as solid expansions in Ireland, the Netherlands and Spain provide a marked contrast to the downturns in Italy, Greece, France and Austria. The German industrial engine is also achieving only modest growth.

And here’s a summary:

Updated

Greece’s factory sector suffered another decline in output last month.

Its manufacturing PMI rose slightly to 48.8, from 48.4 in September, with export orders picking up.

Further evidence that Greece’s economy remains very weak, even though its long recession may be over.

Further contraction in Greek manufacturing: #PMI at 48.8 in Oct (48.4 in Sep) http://t.co/j2xi36570D

— Markit Economics (@MarkitEconomics) November 3, 2014

It’s a better picture in Germany, where factories reported a rise in activity last month, and an increase in job creation, despite a small drop in new orders.

The German manufacturing PMI rose to 51.4 for October, up from September’s 49.9 (which showed a very slight contraction).

Here are the key points:

- Production growth accelerates despite marginal decline in new orders

- Rate of job creation hits 33-month high

- Input costs decline at sharpest rate since April

The drop in new orders was blamed on “a slowing economy and the Russian sanctions”.

French factories continued to cut staffing levels last month, Markit reports:

French manufacturers cut jobs again in October and for the 7th consecutive month - Markit

— MineForNothing (@minefornothing) November 3, 2014

France’s factory sector has shrunk again -- with its manufacturing PMI coming in at 48.5 in October.

That shows a sharper contraction than in September (when the PMI was 48.8), but it’s better than feared.

Italian factories cut staff as orders fall

Bad news from Italy -- its factory sector has suffered a decline in activity, adding to fears that that country is sliding into recession.

The Italian manufacturing PMI fell back to 49.0 last month, down from 50.7 in September, indicating that it contracted (50 is the cut-off point between growth and contraction).

Italian firms reported that output levels and new orders both fell last month, forcing them to lay off staff.

Here are the key points:

- Weakness on order front leads to job cuts as well as lower output

- Export growth dips to 22-month low

- Fastest decrease in backlogs of work for 18

Phil Smith, economist at Markit. says:

“The manufacturing PMI resumed its worrying slide seen since May after having ticked up slightly in September. Falling back below 50.0, the index points to Italy’s manufacturing sector returning to contraction.

“The survey showed that output dipped in October and, furthermore, a drop in new orders, rapidly shrinking backlogs of work and further accumulation of finished goods bodes ill for November’s output prospects.

“Manufacturers are back in retrenchment mode, cutting staff that are surplus to requirements and lowering buying levels in order to minimise unwanted build-up of stocks. This scaling back of purchasing activity continued to weigh on input price inflation, which in October reached a five- month low.”

Spain's manufacturing sector grows again

Spain’s factory sector has expanded for the 11th month running, but - disappointingly - job creation has slowed.

The Spanish PMI was unchanged at 52.6 in October, showing that factories grew at the same pace as in September.

Output and new orders both picked up during the month. However Markit, which compiled the report, also found that employment growth had slowed to five-month low.

And new export order growth slowed, “amid reported weakness in European demand”.

The report also shows that deflationary pressures are building. Input costs fell, while output prices (what firms charge) declined at the fastest rate in seven months.

So, some reasons to be cautious, as Markit’s Andrew Harker explains:

“The recent solid performance of the Spanish manufacturing sector continued in October in spite of a challenging economic environment.

Further rises in output and new orders provide some cause for optimism that the sector won’t head into another downturn as 2014 draws to a close.

That said, a couple of the indices sound a note of caution; firstly the rise in new orders was partly driven by price discounting, a trend that has been increasingly evident in recent months. Secondly, employment growth eased to the weakest in five months, suggesting that firms might be lacking some confidence in the sustainability of the recovery.”

Updated

Banking giant HSBC’s results have just been released, and profits have has missed expectations.

#HSBC misses on earnings, reports Q3 profit of $4.61bn vs. $5.47bn expected. $HSBA $FTSE RO

— IGSquawk (@IGSquawk) November 3, 2014

The results also show that HSBC has set aside £236m to cover the cost of settling an investigation by UK authorities over alleged foreign exchange rigging.

It has also taken a $550m charge to cover a settlement with the US federal housing finance agency.

The City isn’t impress, pushing HSBC’s shares down over 2% to 626p.

HSBC shares how down 2.3% following earnings, probes and provisions

— RANsquawk (@RANsquawk) November 3, 2014

HSBC is holding a press conference shortly, so we might get more details soon....

Updated

Back to today’s factory data, and there’s good news from Poland.

It’s manufacturing PMI rose to 51.2, showing growth after three months of contractions.

Output and new orders both rose last month.

Ryanair shares soar after profits soar

Europe opens flat ahead of euro zone PMI data, Ryanair up over 6% http://t.co/JjdJy7UpmJ

— CNBCWorld (@CNBCWorld) November 3, 2014

Shares in Ryanair have jumped by 6% after it raised its profit forecasts this morning.

The budget airline also reported a 32% jump in half-year profit to €795m, having recently revamped its customer service.

Michael O’Leary, the company’s voluble founder and CEO, says Ryanair is benefitting from treating its customers better, and offering allocated seating and a new business service.

He told BBC Breakfast that

“I’m a very shy, retiring, Irish farmer.”

"I'm a shy and retiring Irish farmer" - so says @Ryanair Michael O'Leary on #bbcbreakfast - company profits are up by a third

— BBC Breakfast (@BBCBreakfast) November 3, 2014

He’s also just appeared on Sky News, saying that Ryanair is benefitting from (belatedly) prioritising customer service.

It’s “better late than never”, O’Leary concedes, adding:

“This being nicer to customers is a new and winning strategy”.

Updated

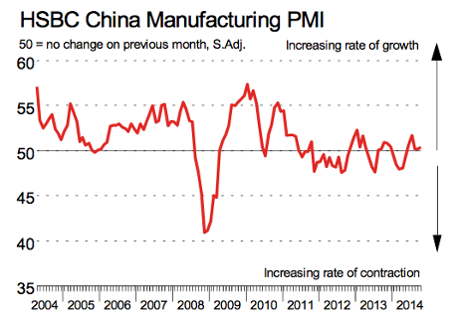

HSBC’s survey of the Chinese factory sector also found signs of deflation; factory bosses reported a fall in the cost of raw materials, and in their own finished goods.

China HSBC Manufacturing #PMI signals marked declines in both input and output prices http://t.co/9qXAnYDadS

— Markit Economics (@MarkitEconomics) November 3, 2014

Ireland has bucked the trend of weak growth in Europe and Asia, with factory output growing at a faster rate last month.

The Irish manufacturing PMI rose to 56.6 in October, from 55.7 in September, showing that growth accelerated.

Firms reported a rise in new orders and production, encouraging them to take on more staff. And “stocks of purchases” rose at the sharpest pace since the survey began in May 1998

Philip O’Sullivan, chief economist at Investec Ireland said:

“The latest Investec Manufacturing PMI report for Ireland shows a substantial strengthening in business conditions in October....

“October’s improvement is chiefly attributed to a combination of inventory building and resilient client demand .”

Updated

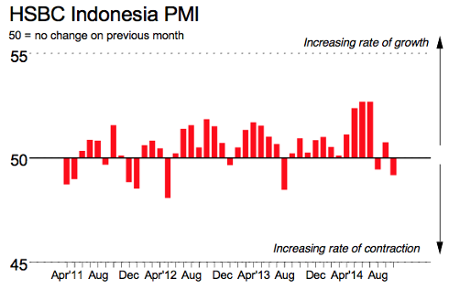

Asian PMIs show loss of momentum

The latest manufacturing surveys from Asia have suggested that China’s economic growth slowed last month, with manufacturers in South Korea and Indonesia also reporting tough times in October.

The official PMI survey conducted by the Chinese government, released on Saturday, showed growth slipping to a five-month low last month.

A rival survey conducted by HSBC, which is weighted towards small firms, looked slightly better -- with activity inching up to a three-month high. But it also found that output and new order growth slowed.

Reuters has a good round-up:

Asia’s factories are reporting a generalised loss of momentum that speak volumes about the need for more policy stimulus, on top of Japan’s latest efforts to ignite growth.

A raft of regional manufacturing surveys on Monday were littered with unwelcome landmarks, including a five-month low for activity in China, a four-month trough for South Korea and a 14-month low for Indonesia.

Even China’s long resilient services sector saw growth ebb to the slowest in nine months as the cooling property sector weighed on demand.

“We still see uncertainties, given the property downturn as well as the slow pace of global recovery, and expect further monetary and fiscal easing measures in the months ahead,” said Hongbin Qu, chief economist for China at HSBC.

HSBC’s own version of the purchasing management index (PMI) compiled by Markit was a whisker firmer at 50.4 in October, from the September’s 50.2, but showed growth slowing in output and new orders, while companies trimmed staff levels for the 12th straight month.

Beijing has already cut taxes, quickened some investment projects, offered short-term loans to banks, instructed local governments to spend their budgets and reduced the amount of deposits that some banks hold as reserves to spur lending.

So far, lower mortgage rates have not revived the housing market as quickly as some had hoped, with prices falling for a sixth consecutive month in October, according to one private survey.

Updated

Opening post: Eurozone manufacturing data in focus

Good morning, and welcome to our rolling coverage of the financial markets, the world economy, business and finance.

There’s lots of economic data coming up this morning, with the publication of October’s manufacturing Purchasing Managers Indexes (PMIs) for many European countries.

These PMI reports will show whether factories managed to expand their output, hire more staff and attract more orders last month. Or not.

Economists predict a mixed picture -- particularly from France and Italy.

Michael Hewson of CMC Markets has summed up those expectations:

Today’s latest October manufacturing PMI numbers for Spain, Italy, France and Germany could well serve to increase pressure for additional action on the ECB, particularly if the recent trend of poor Italian and French data continues.

Expectations are for slightly weaker numbers of 50.6 and 47.3 respectively, while Spain and Germany are expected to be slightly firmer at 52.4 and 51.8.

The eurozone data comes between 8am and 9am GMT, followed by the UK manufacturing PMI at 9.30am.

It’s likely to be a calm start to the month in Europe’s stock markets, after last week’s gains:

Expect a neutral opening & a touch of indigestion for European opening after such a euphoric rally last week - FTSE -2, DAX +4, CAC+4

— David Buik (@truemagic68) November 3, 2014

And banking giant HSBC releases its latest financial results, at 8.15am....