/Lowe)

Mooresville, North Carolina-based Lowe's Companies, Inc. (LOW) operates as a home improvement retailer. It offers a wide range of products used in construction, maintenance, repair, remodeling, decoration, and home improvement. With a market cap of $130.7 billion, the company operates over 1,750 physical stores spread across the US.

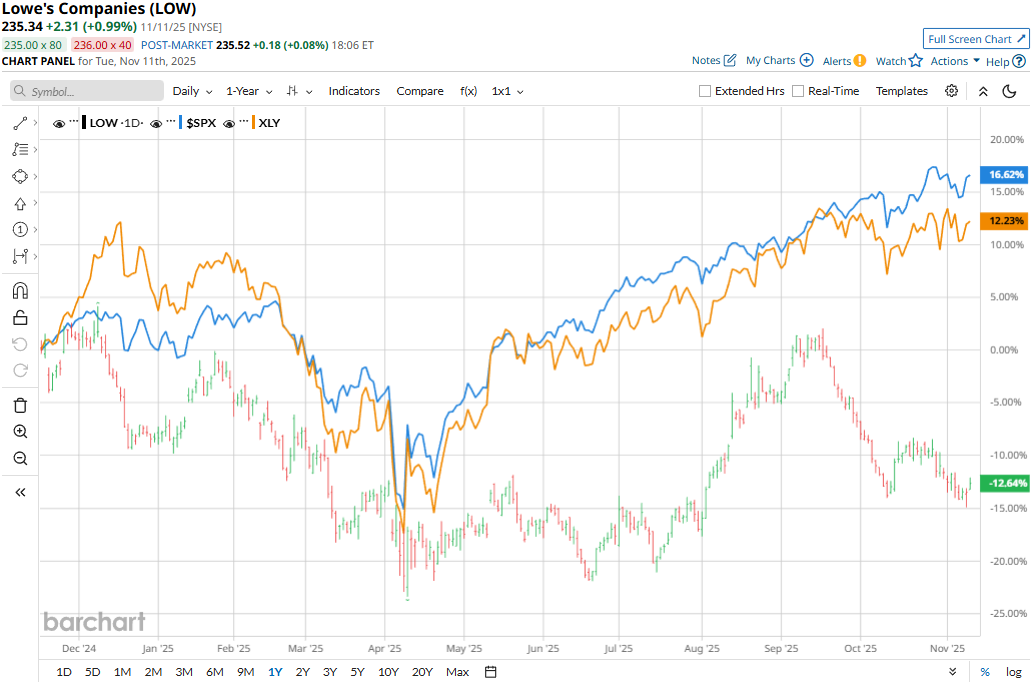

The home improvement retailer has substantially underperformed the broader market over the past year. LOW stock prices have declined 4.6% on a YTD basis and 14.3% over the past 52 weeks, compared to the S&P 500 Index’s ($SPX) 16.4% returns in 2025 and 14.1% gains over the past year.

Zooming in further, Lowe’s has also underperformed the sector-focused Consumer Discretionary Select Sector SPDR Fund’s (XLY) 6.8% uptick in 2025 and 9.2% gains over the past 52 weeks.

Lowe's stock prices observed a marginal uptick in the trading session following the release of its mixed Q3 results on Aug. 20. Driven by solid performance in both Pro and DIY, the company observed notable improvement in comparable sales. Its net sales for the quarter grew 1.6% year-over-year to approximately $24 billion, missing the Street’s expectations by a whisker. Meanwhile, its adjusted EPS increased 5.6% year-over-year to $4.33, beating the consensus estimates by 2.4%.

For the full fiscal 2026, ending in January, analysts expect Lowe’s to deliver an adjusted EPS of $12.31, up 2.6% year-over-year. On a positive note, the company has a solid earnings surprise history. It has surpassed the Street’s bottom-line estimates in each of the past four quarters.

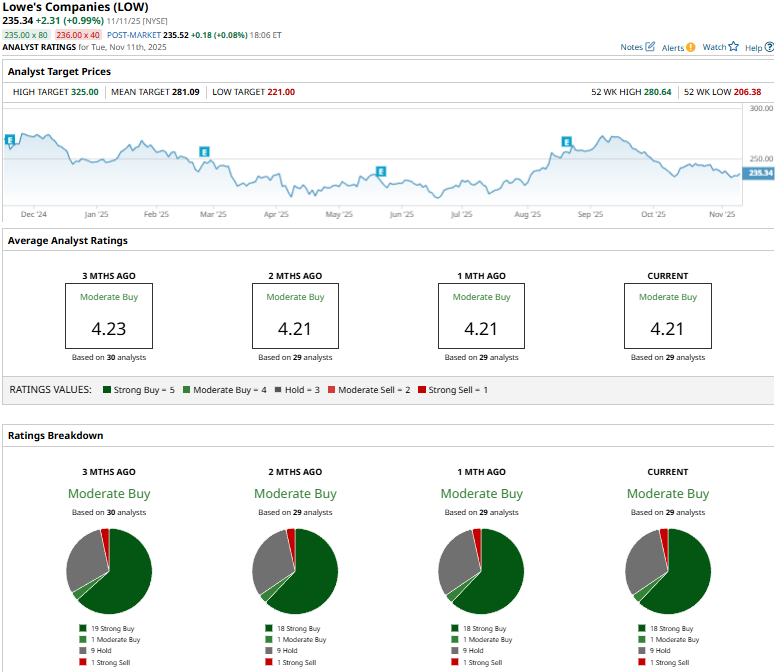

Among the 29 analysts covering the LOW stock, the consensus rating is a “Moderate Buy.” That’s based on 18 “Strong Buys,” one “Moderate Buy,” nine “Holds,” and one “Strong Sell.”

This configuration is slightly less optimistic than three months ago, when 19 analysts gave “Strong Buy” recommendations.

On Nov. 11, Evercore ISI analyst Greg Melich maintained an “In-Line” rating on LOW, but notched down the price target from $245 to $240.

Lowe’s mean price target of $281.09 represents a 19.4% premium to current price levels. Meanwhile, the street-high target of $325 suggests a notable 38.1% upside potential.