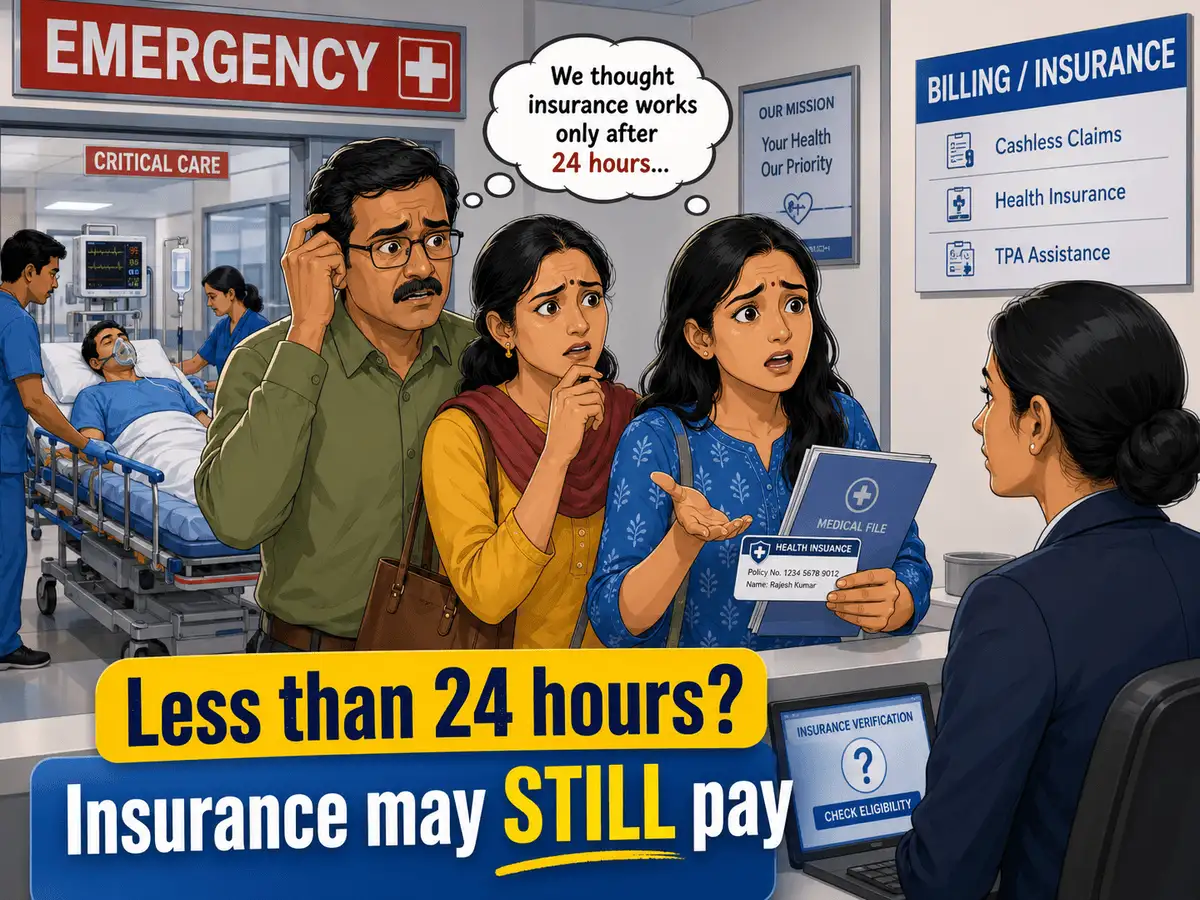

A lot of policyholders still believe that health insurance claims are approved only if a patient is hospitalized for at least 24 hours. Even if they know that shorter stays might be covered, many are still confused about the specific situations and medical emergencies that allow claims before hitting that 24-hour mark.

That said, not every brief hospital visit qualifies for a claim. Coverage usually depends on whether the treatment is medically necessary, included in the policy and meets the insurer’s conditions.

So, when can you actually file a health insurance claim for a hospital stay of less than 24 hours? Here’s what policyholders should be aware of:

Can you file health insurance claims for a hospital stay of less than 24 hours?

According to insurance experts, policyholders can still be eligible for claims even if they haven’t spent a full day in the hospital.

“Yes, health insurance claims can be made for less than 24 hours hospitalization provided the procedure falls under day care treatment approved by the insurer,” says Sarita Joshi, Head of Health and Life Insurance, Probus.

Earlier, 24-hours of hospitaliztion was needed for claims; however owing to the advanced technology, many treatments can now be covered in a few hours and hence covered if they are medically necessary & mentioned in the policy, she adds.

Moreover, standard health insurance covers accidental emergencies as well. If you are rushed to the ER after an accident, many policies cover the stabilization and immediate treatment, even if you aren't admitted overnight, says Siddharth Singhal, Head of Health Insurance, Policybazaar.

Common day care treatments covered under health insurance

|

Specialty

|

Procedures/Treatments |

| Ophthalmology | Cataract surgery, Vitrectomy |

| ENT | Septoplasty, Tympanoplasty (eardrum repair), Tonsillectomy |

| Urology | Kidney stone removal (Lithotripsy), Hydrocele surgery |

| Gastroenterology | Colonoscopy, Appendectomy (laparoscopic), Piles/Fistula surgery |

| Oncology | Chemotherapy and Radiotherapy sessions |

In which cases are claims allowed before 24-hour hospitalisation?

Several modern treatments and minimally invasive procedures are now commonly covered even if the patient is discharged the same day.

“Some cases such as cataract surgery, tonsil removal, dental treatment (arising from accidents), radiotherapy, chemotherapy, eye/ear surgeries, kidney dialysis, minimal invasive procedures etc. are usually covered before 24 hour hospitalization,” says Joshi.

According to Shilpa Arora, Co-founder and COO, Insurance Samadhan, the list now includes many specialised treatments.

Cases where health insurance claims are allowed before 24-hour hospitalization are like chemotherapy, radiotherapy, cataract, procedures of fractures done under GA/LA, angiography and other specialized and advanced procedures, she explains.

What is day care treatment in health insurance?

Day care treatment in health insurance means a medical procedure or surgery that is performed without an overnight hospital stay (i.e. treatment is completed within 24 hours) and is covered under the policy’s inpatient benefits even though the patient isn’t admitted overnight.

“Day Care Treatment refers to medical procedures or surgeries that require hospitalization but can be completed in less than 24 hours due to technological advances (such as laparoscopy or robotic surgery),” says Singhal.

However, Day Care treatment should not be confused with ordinary OPD consultations.

Day Care is not the same as OPD (Outpatient Department). Visiting a doctor for a viral fever or a consultation is OPD; undergoing a surgical procedure under anesthesia is Day Care, he adds.

Day care treatment procedures covered under health insurance

The list of day care procedures that are covered under health insurance has expanded significantly over the years.

“Day care treatments include cataract surgery, chemotherapy, dialysis, ENT procedures, eye surgeries, dental treatment due to accidents, lithotripsy, and certain laparoscopic surgeries are commonly covered. One must note that this cover may vary across insurers and plans,” says Joshi.

Most modern policies cover between 150 to 500+ specific procedures, according to Singhal.

Hidden clauses and exclusions related to day care claims policyholders often overlook

Although day care coverage is common in most health insurance plans today, many policyholders often miss important conditions hidden in policy wording.

According to Singhal, policyholders often get caught off guard by these "fine print" details:

- The "positive list" vs. "all-inclusive": Some old policies only cover a specific list of day care procedures. If your surgery isn't on that list, they won't pay. Modern policies usually cover "all" day care treatments.

- Diagnostic exclusions: If you are admitted for less than 24 hours solely for "observation" or "investigation" (such as an MRI or a series of blood tests) without a surgical procedure, the claim is usually rejected.

- Maternity/dental: Even if these are covered within 24 hours, they are often excluded unless you have a specific rider.

- Room rent limits: Even in day care, if you are kept in a private room for 6 hours, some insurers may apply "proportionate deductions" if your room category exceeds your limit.

What policyholders should check before buying health insurance

Before buying a health insurance policy with day care cover, policyholders should check the exact list, exclusions, and limits on specific procedures.

“Policyholders should carefully check the list of covered day care procedures, review the waiting period of the policy and check exclusions if any. They should also go through the hospital network conditions and co-payment clauses,” says Joshi.

She further adds that they should check if modern treatments & advanced procedures are included. It is also important to review claim documentation requirements to avoid any unpleasant surprises during the claim process.

According to Singhal, before you sign or head to the hospital, verify these three things:

- Scope of day care: Does the policy cover a specific list (e.g., "140 procedures") or all day care treatments? Aim for "all."

- Pre and post-hospitalization: Ensure that the policy covers expenses incurred before (usually 30–60 days) and after (usually 60–180 days) the day care procedure.

- Sub-limits: Check if there is a "cap" on specific surgeries. For example, a policy might cover your surgery but limit Cataract claims to Rs 30,000 per eye.