/Lam%20Research%20Corp_%20HQ%20sign-by%20Michael%20Vi%20via%20Shutterstock.jpg)

Fremont, California-based Lam Research Corporation (LRCX) is a leading supplier of semiconductor manufacturing equipment and services. Valued at a market cap of $194.9 billion, the company’s solutions play a crucial role in enabling advanced logic, memory, and 3D semiconductor architectures across nodes used in data centers, AI, mobile devices, and automotive electronics.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and LRCX fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the semiconductor equipment & materials industry. With deep industry partnerships, a strong focus on innovation, and exposure to long-term growth drivers like AI and cloud computing, Lam Research remains a key player in the semiconductor equipment supply chain.

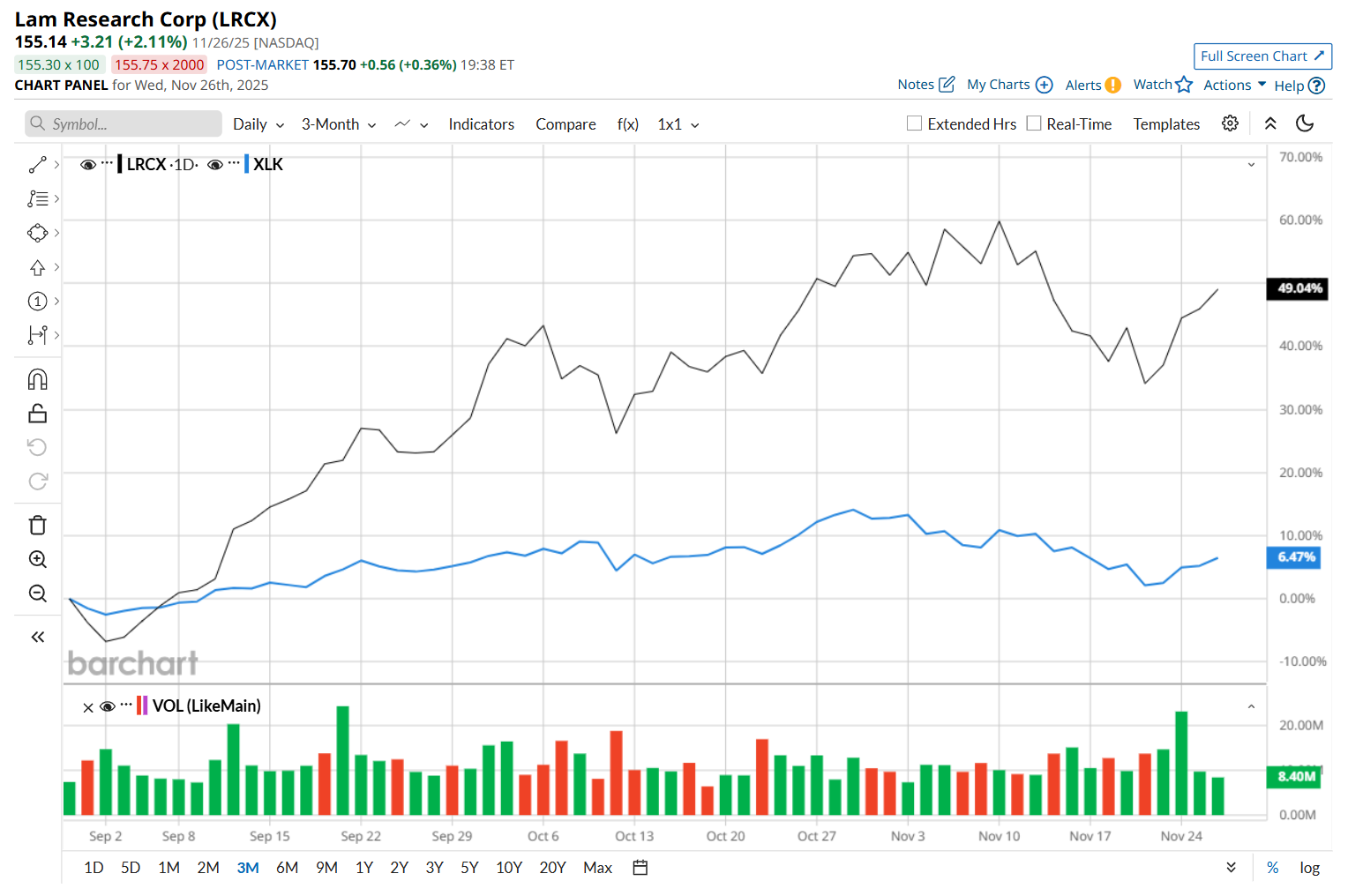

This tech giant is currently trading 7.2% below its 52-week high of $167.15, reached on Nov. 10. Shares of LRCX have rallied 49.7% over the past three months, considerably outpacing the Technology Select Sector SPDR Fund’s (XLK) 7.9% return during the same time frame.

Moreover, on a YTD basis, shares of LRCX are up 114.8%, compared to XLK’s 22.1% rise. In the longer term, Lam Research has soared 113.4% over the past 52 weeks, significantly outperforming XLK’s 20.9% uptick over the same time frame.

To confirm its bullish trend, LRCX has been trading above its 200-day and 50-day moving averages since early May, with slight fluctuations.

On Oct. 22, shares of LRCX dipped 2.6% after its Q1 earnings release, despite delivering a better-than-expected performance. Due to strong growth in systems revenue, the company’s total revenue improved 27.7% year-over-year to $5.3 billion, surpassing consensus estimates by 1.9%. Moreover, its adjusted EPS of $1.26 also came in 4.1% ahead of analyst expectations. However, its bottom line declined 5.3% from the last quarter, which might have made investors jittery. Nonetheless, its stock rebounded and surged by 4.5% in the following trading session.

LRCX has also considerably outpaced its rival, Applied Materials, Inc. (AMAT), which soared 44.3% over the past 52 weeks and 53.7% on a YTD basis.

Given LRCX’s recent outperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 31 analysts covering it, and the mean price target of $162.78 suggests a 4.9% premium to its current price levels.