Kellanova (K), headquartered in Chicago, Illinois, manufactures and markets snacks and convenience foods. Valued at $28.9 billion by market cap, the company offers snack products such as snacks, cereal, noodles, plant-based foods, and frozen breakfast with online delivery services.

Shares of this snacks giant have underperformed the broader market over the past year. K has gained 3.2% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 18.5%. In 2025, K stock is up 2.7%, compared to the SPX’s 15.1% rise on a YTD basis.

Zooming in further, K’s outperformance is apparent compared to the First Trust Nasdaq Food & Beverage ETF (FTXG). The exchange-traded fund has declined about 14.7% over the past year. Moreover, K’s single-digit returns on a YTD basis outshine the ETF’s 10.1% losses over the same time frame.

On Oct. 30, K shares closed up marginally after reporting its Q3 results. Its revenue stood at $3.3 billion, up marginally year over year. The company’s adjusted EPS increased 3.3% year-over-year to $0.94.

For the current fiscal year, ending in December, analysts expect K’s EPS to decline 5.2% to $3.66 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimate in two of the last four quarters while missing the forecast on two other occasions.

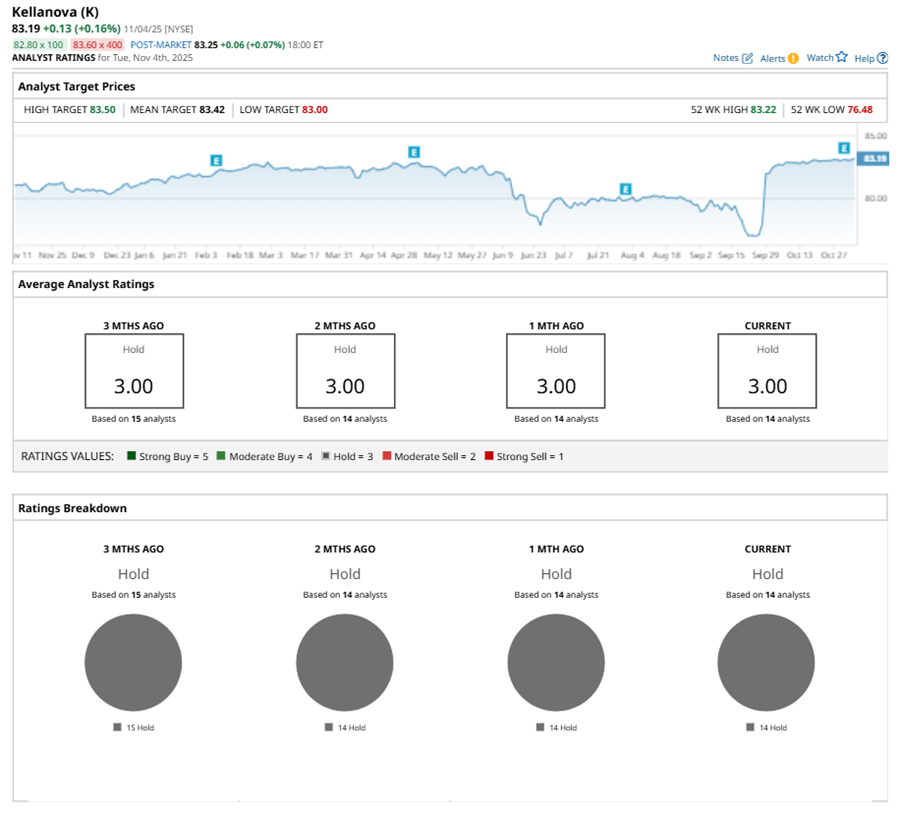

Among the 14 analysts covering K stock, the consensus is a “Hold.”

The configuration has been relatively stable over the past three months.

On Oct. 31, Barclays PLC (BCS) analyst Andrew Lazar maintained a “Hold” rating on K and set a price target of $83.

The mean price target of $83.42 represents a marginal premium to K’s current price levels. Similarly, the Street-high price target of $83.50 suggests a slight upside potential.