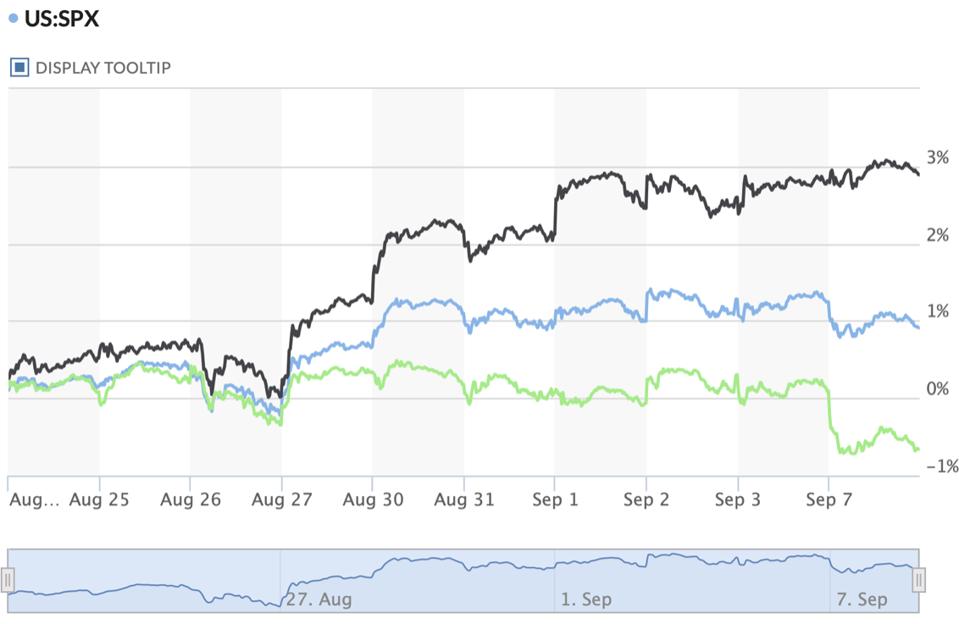

The Dow Jones Industrial Average fell 260 points on Tuesday after investors reevaluated the market’s potential for growth following a stellar earnings season. Meanwhile, the S&P 500 fell around 0.3%, though the tech-heavy Nasdaq

Investors may also be weighing the upcoming months, often seen as the weakest performing season of the year, in their decisions. And thanks to specific legislative and fiscal decisions regarding healthcare, Afghanistan, Covid-19, and stimulus tapering, the next few months are set to carry an increasingly outsize risk. And because the market has yet to pull back from its record recovery run, others may be preparing for at least one drawdown before the year’s end.

Q.ai runs daily factor models to get the most up-to-date reading on stocks and ETFs. Our deep-learning algorithms use Artificial Intelligence (AI) technology to provide an in-depth, intelligence-based look at a company – so you don’t have to do the digging yourself.

Sign up for the free Forbes AI Investor newsletter here to join an exclusive AI investing community and get premium investing ideas before markets open.

Kansas City Southern (KSU)

Kansas City Southern slipped 1.5% Friday and an additional 1.4% on Tuesday, ultimately closing down at $287.50 per share. The stock sits up 40.9% YTD, though it’s trading below both its 10- and 22-day price averages of $291.76 and $288.93, respectively. Currently, KCS

Kansas City Southern is a railroad holding company that specializes in North American railroad investments from the United States down to Panama. The company hit our trending lists twice this year thanks to a bidding war between two larger railway companies, Canadian National (CN) and Canadian Pacific (CP).

While CN won the bidding war after much ado in May, the company faced regulatory pressures after the White House denounced railroad mergers on the whole. When the company stated its intention to form a trust to purchase KCS, the Department of Justice condemned its workaround as a “mockery” of the U.S. Surface Transportation Board’s oversight.

The STB ultimately ruled that KCS could not be bought by an independent trust on 31 August. This occurred just weeks after the Kansas City Southern Board of Directors declared that the company had received a “superior” bid from Canadian Pacific in light of the issues plaguing the merger’s legality. CP has given the smaller railroad until September 12 to decide if KCS will go through with the merger or wait out the STB’s final ruling.

Over the last three fiscal years, Kansas City Southern’s revenue slipped from $2.7 billion to $2.6 billion, largely due to pandemic-related pressures. But in the same period, operating income grew 12% from $968 million to $1.04 billion, while per-share earnings nudged up from $6.13 to $6.54. Additionally, return on equity saw a slight increase from 12.6% to 13.5%.

All told, Kansas City Southern is expected to see around 5% revenue growth in the next year. Our AI rates this railroad holding company A in Technicals, B in Growth, and C in Low Volatility Momentum and Quality Value.

HyreCar, Inc (HYRE)

HyreCar, Inc closed up 1.7% on Friday before surging an additional 5.7% by Tuesday’s close, ending the day at $12.20 per share. The stock is trading above both its 10- and 22-day price averages of $11.28 and $12 even, respectively. Currently, HyreCar sits up almost 73% YTD.

HyreCare is a web-based marketplace that lets fleet and vehicle owners rent their cars to gig drivers working for companies like Uber

HyreCar is trending this week thanks to a class action lawsuit against the marketplace. The lawsuit alleges that the company engaged in securities fraud between 14 May and 10 August of 2021 due to knowing or “recklessly disregard[ing]” a number of adverse facts.

These include the company understating its insurance reserves; failing to pay valid insurance claims; incurring “significant expenses” transferring to a new claims processing; failing to appropriately price risk in its insurance products; and dramatically reforming its policies and procedures in response to “unacceptably high claims severity and customer complaints.”

As a result of these factors, the lawsuit alleges, the stock was misrepresented to investors as the company was not on track to meet its financial estimates. Those who wish to register in the case have until 26 October 2021 to seek appointment as a lead plaintiff.

Specters of the lawsuit, unfortunately, have already done a number on the company’s stock – though its bottom line over the last three years may leave room for optimism. In the period, revenue surged 211% from $10 million to $25 million, bringing operating income up from $9 million to over $15 million. Additionally, return on equity more than doubled from 548% to 1,309% – though EPS shrank from $1.31 to 87 cents.

At this time, HyreCar’s forward 12-month revenue is expected to grow around 25.4%. Our AI rates this trending investment B in Growth, C in Technicals and Low Volatility Momentum, and D in Quality Value.

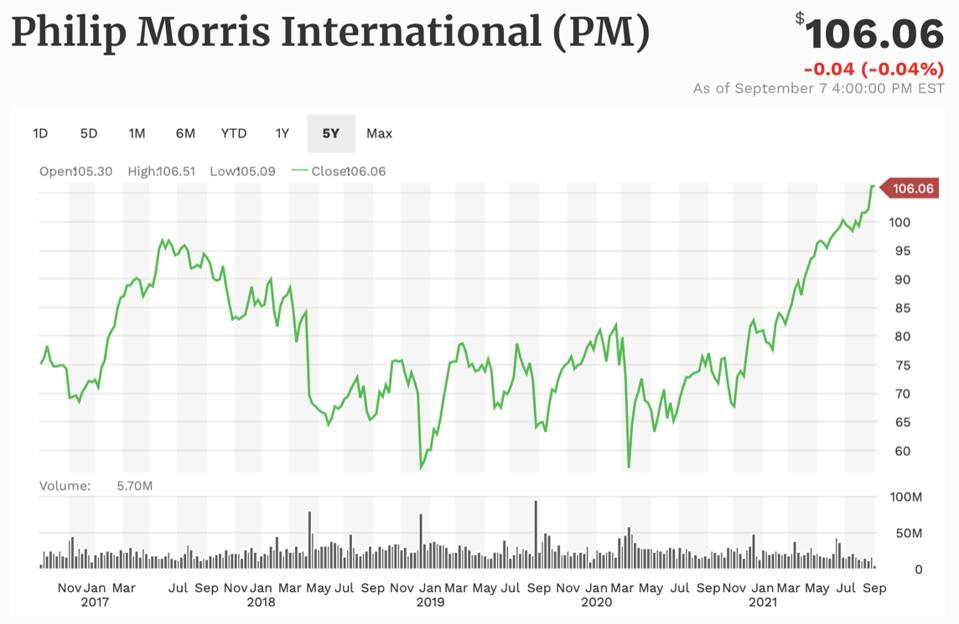

Philip Morris International, Inc (PM)

Philip Morris International, Inc nudged up 0.4% Friday to $106.10, ending the day on the back of 2.96 million trades. The stock sits up 28% for the year and trades at 16.8x forward earnings.

Philip Morris began trending over the summer after its own CEO stated that the U.K. should ban cigarettes within a decade, likening them to gas-powered cars. And while the company stands to gain from the conversion to vape pens and e-cigarettes, that’s not the controversial move that’s kept it on our trending lists. Rather, Philip Morris has had its sights on buying into the same healthcare companies that treat the lung diseases its products cause, including asthma.

Notably, the tobacco giant received tentative regulatory approval to acquire U.K.-based Vectura, which produces respiratory therapies such as asthma inhalers. As of 18 August, the cigarette giant had managed to purchase 22.6% of the company’s total shares as part of its $1.51 billion deal to purchase Vectura. Shareholders have until 15 September to decide whether they want to sell to Philip Morris.

However, under market rules, Philip Morris cannot build its stake purchasing shares from United States investors, leaving the company to target international shareholders, instead. Thus far, Vectura’s board has unanimously recommended that shareholders sell out, despite public health experts and a number of charities urging shareholders to vote against the takeover on grounds that Vectura would no longer be a credible force in the medical industry.

In the last three fiscal years, Philip Morris’ revenue slipped from $29.6 billion to $28.7 billion, with operating income barely inching up from $11.3 billion to $11.7 billion. In the same period, per-share earnings gained 8 cents to $5.16 per share.

Currently, Philip Morris is expected to see around 2.3% revenue growth in the next year. Our AI rates this trending company A in Low Volatility Momentum, B in Quality Value, and C in Technicals and Growth.

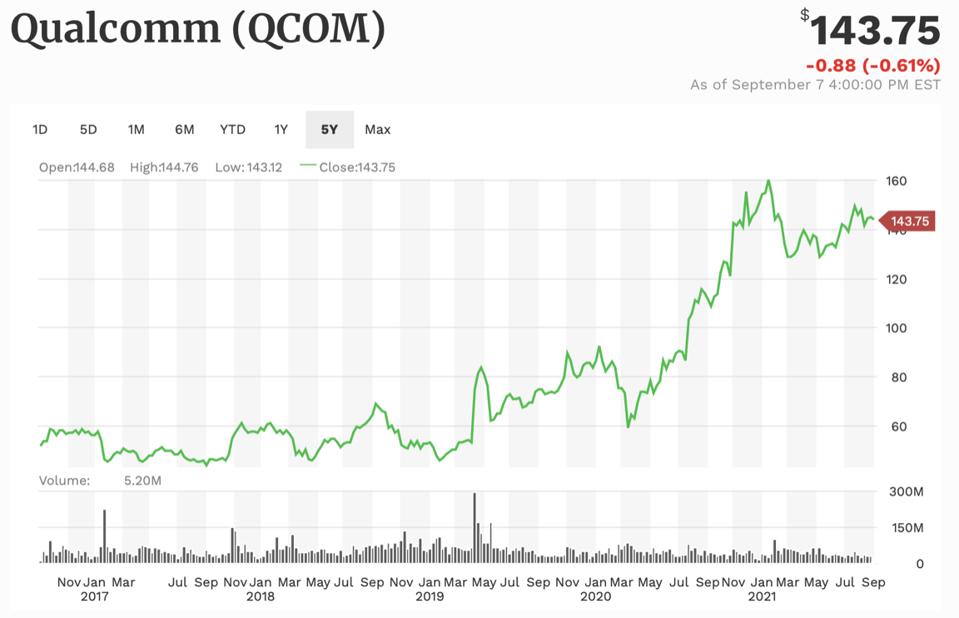

Qualcomm, Inc (QCOM)

Qualcomm, Inc slipped 0.3% Friday to $144.63 per share, closing out the session with 5.5 million trades on the docket. The stock sits within a dollar of each its 10- and 22-day price averages, though it’s down 5% YTD. At this time, Qualcomm trades at 16x forward earnings.

Qualcomm is trending this week after the chipmaker reported on Monday that it will supply a key chip for the new Renault electric vehicle, the Mégane E-TECH Electric, which is expected to debut later this month in Munich. Though San Diego-based Qualcomm is best known for its position in the mobile phone chipmaking industry, this marks the second deal this year with an automaker to provide chips for dashboards and infotainment systems.

Over the last three fiscal years, Qualcomm’s revenue surged 44% from $22.6 billion to $23.5 billion, with operating income nearly doubling from $3.77 billion to $6.23 billion. In the meantime, EPS leapt from $3.39 to $4.52 as return on equity tripled from 31.5% to 94.6%.

Currently, Qualcomm is expected to see its forward 12-month revenue grow around 8.8%. Our artificial intelligence algorithms rate this trending pick A in Quality Value, B in Low Volatility Momentum, and C in Technicals and Growth.

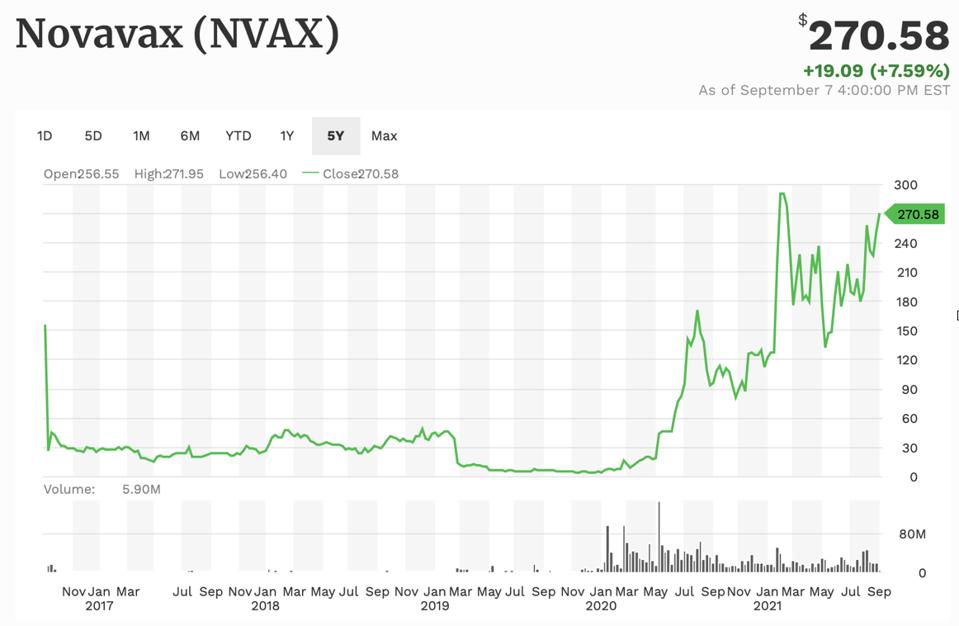

Novavax, Inc (NVAX)

Novavax, Inc slipped 2.9% Friday to close out the week at $251.49 per share on the back of 4.3 million trades. However, the stock surged a whopping 7.6% in Tuesday’s session, gaining more than $19 to close at $270.58. At this time, Novavax sits up almost 143% for the year and trades at 12.2x forward earnings.

The sudden change in Novavax’s stock price comes about as Japan’s Ministry of Health, Labour, and Welfare agreed to buy 150 million doses of Novavax’s Covid-19 vaccine (subject to regulatory approval). The vaccine will be produced in Japan and licensed by the country’s own Takeda Pharmaceutical. If all goes to plan, the healthcare giant plans to distribute this new vaccine as soon as early 2021, pending the outcome of the company’s Japanese clinical trials.

Over the last three fiscal years, Novavax – which has never successfully produced a vaccine of any description – has seen its revenue surge over 3,347% to $475.6 million compared to $34.3 million. Operating income rose nearly two and a half times from $174 million to $414 million in the period as return on equity grew to 90.4%. That said, per-share earnings have fallen in the three years from $9.99 to $7.27.

All told, Novavax is expected to see forward 12-month revenue growth in the ballpark of 88.4%. Our AI rates this trending stock C in Technicals, D in Quality Value, and F in Growth and Low Volatility Momentum.

Liked what you read? Sign up for our free Forbes AI Investor Newsletter here to get AI driven investing ideas weekly. For a limited time, subscribers can join an exclusive slack group to get these ideas before markets open.