Back with Greece, and here’s Reuters’ take on the latest opinion poll showing Alexis Tsipras’ Syriza party in second place to New Democracy:

Greece’s conservative New Democracy party has taken a tiny lead among voters over leftist Syriza before the September 20 election, an opinion poll published on Friday showed.

New Democracy has rapidly closed the gap with Syriza in recent days, and the Metron Analysis poll on Friday was the second this week to show it overtaking former prime minister Alexis Tsipras’s party.

Syriza is on course to get 23.4% of the vote while New Democracy would take 24%, the latest poll showed. Over 11 percent of respondents were undecided.

Just a few weeks ago, a Syriza victory in the snap election had appeared almost certain...

The latest poll, conducted on behalf of the Parapolitika newspaper, showed New Democracy leader Evangelos Meimarakis, with his rating at 47%, was more popular than Tsipras, who was backed by 43%.

#Greece poll [MetronAnalysis/@parapolitika]: ND 24 +2.8 Syriza 23.4 +1.2 KKE 5.2 GD 5.1 Potami 4.8 PASOK 4 EK 4 LAE 3.4 ANEL 2

— Yannis Koutsomitis (@YanniKouts) September 4, 2015

On that note it’s time to close up for now, so once again thanks for all your comments and we’ll see you soon.

European markets end with further losses

Another volatile week finished with further woe for investors. Among the day’s data, German factory orders fell 1.4% month on month in July, but the big event was the US non-farm payroll numbers. As it turned out the headline figure disappointed, with 173,000 jobs added in August compared with the 220,000 or so expected. But the unemployment rate dipped to 5.1% and hourly wages were steady, so there were few clues as to whether the US Federal Reserve would raise interest rates this month or not.

Despite the turmoil caused by worries about China, many analysts believed there was nothing in the jobs data to prevent an increase. Equally, many others believed the Fed would keep its powder dry. The markets seemed to side with the hawks, especially since just before the figures were released, Richmond Fed president Jeffrey Lacker said the non-farm numbers should not derail the case for a rate rise.

So the upshot was another slide in shares, with the final scores showing:

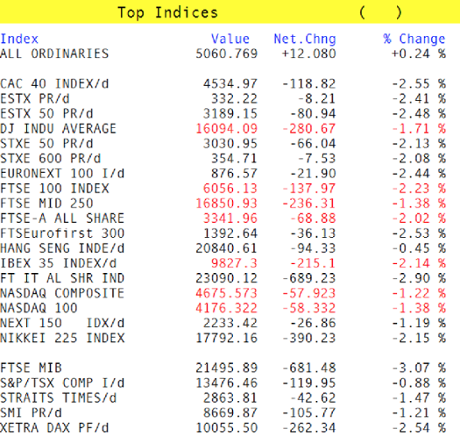

- The FTSE 100 finished down 151.18 points or 2.44% at 6042.92

- Germany’s Dax dropped 2.71% to 10,038.04

- France’s Cac closed 2.81% lower at 4523.08

- Italy’s FTSE MIB fell 3.18% to 21,472.68

- Spain’s Ibex ended down 2.2% at 9821.8

- The Athens market edge down 0.37% to 646.62

On Wall Street, the Dow Jones Industrial Average is currently 292 points or 1.8% lower.

Meanwhile Moody’s has downgraded the senior debt ratings of four Greek banks to C, in the expectation that holders will suffer losses in the forthcoming recapitalisations. It said:

The downgrade...primarily reflects Moody’s expectation that junior and senior debt holders will be bailed in and sustain material losses as part of the upcoming recapitalisation process...

Although Moody’s expects uninsured depositors to be excluded from bail-in, as indicated by a recent Eurogroup statement, the negative outlook reflects the ratings agency’s opinion that the recapitalisation process remains fluid and banks continue to face significant credit risks.

The banks are Alpha Bank, Eurobank Ergasias, National Bank of Greece and Piraeus Bank.

It may have been another volatile week but there is likely to be more to come. Tony Cross, market analyst at Trustnet Direct, said:

Any hopes that markets may have been through the thick of the volatility have been squarely dashed today with a combination of risk mitigation ahead of the long weekend in the US and concern as to what the Fed is supposed to do with interest rates serving to knock sentiment in markets on a global basis. London has been left nursing triple digit gains and it’s the commodity stocks that are bearing the brunt.

The fact that the US jobless rate has fallen to its lowest level since 2008 has reopened the idea that the Federal Reserve could push through higher interest rates in two weeks time. This will further punish emerging markets currencies and make dollar denominated goods – like oil and metals – more expensive for many. There can be no doubting that the Fed has an enormous weight on its shoulders – calling this wrong could have wide-reaching effects.

Next week may get off to a slow start with the US Labor Day holiday, but Chinese trade data on Tuesday will be closely watched. There’s no argument that the world’s second largest economy is slowing and that will affect the pace elsewhere, but the big question mark hangs over the speed of any contraction.

Also on Monday the Chinese stock market is set to reopen after its closure due to the World War II remembrance events. With Chinese authorities seemingly hinting at no more intervention to stabilise the markets, it could prove another tricky session.

The US Federal Reserve could raise rates faster and further than people expect, according to John Higgins of Capital Economics:

Given the lack of a clear steer from [today’s] report, we continue to think that the probability of US monetary policy being tightened later this month is around 50:50. The bigger picture, though, is that we still forecast that the Federal Open Market Committee will raise the federal funds rate further and faster over the next year or so than most expect, as a tightening labour market puts significant upward pressure on wage and core inflation. Indeed, the unemployment rate has already fallen to the mid-point (5.1%) of the “central tendency” of FOMC members’ latest projections of its longer-run level.

With this in mind, we think a big winner will be the dollar, as the contrast between the monetary policies of the Fed and other major central banks becomes increasingly stark. A big loser, though, could be Treasuries – even if term premiums remain low, there is plenty of scope for yields to rise as expectations for interest rates are revised up. Otherwise, while we anticipate that the US stock market will weather tighter monetary policy well, we think its upside will be capped by the squeeze on profit margins that results from diminishing slack in the labour market.

Updated

Here’s a couple of charts from the Bureau of Labour Statistics release:

And here’s the positive version of the jobs data from the President’s twitter account:

The economy added 173,000 jobs in August—a record-breaking 66 consecutive months of private-sector job growth.

— Barack Obama (@BarackObama) September 4, 2015

And this sums it up:

- Bank of Tokyo: "We would be shocked if Fed officials delay any further!’" - Goldman: "No hike" ... who to believe

— zerohedge (@zerohedge) September 4, 2015

The market slide is accelerating:

Meanwhile over in Greece, a new poll ahead of this month’s election and it’s not good news for former prime minister Alexis Tsipras and his Syriza party:

GREECE'S SYRIZA PARTY TO WIN 23.4 PERCENT OF VOTES AT SNAP ELECTION, NEW DEMOCRACY PARTY TO WIN 24 PERCENT - METRON ANALYSIS POLL

— Ishaq Siddiqi (@IshaqSiddiqi) September 4, 2015

The jobs report muddies the monetary policy outlook, says Unicredit Research economist Harm Bandholz:

Fed Vice Chair Stan Fischer said during his Jackson Hole speech that “we now await the results of the August employment survey.” If he had hoped that the numbers will speak a clear language and basically make the decision for the FOMC – in the one or other direction – he will be disappointed...

In our view, a generally risk-averse Federal Reserve does not want to risk to add to the uncertainty, and prefers to get a better sense of how the global headwinds might affect the US economy.

To be sure, that view is far from being shared by all [Federal Reserve] members. Only today, Richmond Fed President Lacker reiterated his view that the US no longer requires zero interest rates – a view that we fundamentally share. And Mr. Lacker will certainly dissent at the upcoming meeting, if the Fed leaves its target rate unchanged

But while the hawks are usually more vocal, they in our view do not have the majority to get the rate hike just yet. Other voting regional Fed presidents, such as Charles Evans and Dennis Lockhart, will probably be more than happy to stand pat for now. Finally, in a divided Committee, it is up to the Chair to forge the Consensus. And while Janet Yellen has not spoken in public about the policy outlook since mid-July (!), her approach so far has always been to err on the side of caution.

Wall Street opens sharply lower

As expected, US markets have fallen back in the wake of the mixed jobs data.

The Dow Jones Industrial Average is down 204 points or 1.27% in the first few minutes of trading, while the S&P 500 is 1.01% lower.

Meanwhile G20 finance ministers and central bankers, currently meeting in Turkey, will not call on the US to delay a rate rise, Reuters is reporting:

The U.S. Federal Reserve is coming under pressure from emerging markets not to raise rates too soon as turmoil in China threatens global growth, but the G20 will not publicly call for any delay, delegates meeting in Turkey said on Friday.

Slower growth in China and rising market volatility have boosted the risks to the global economy, the International Monetary Fund warned ahead of the G20 meeting. It cited a mix of potential dangers such as depreciating emerging market currencies and tumbling commodity prices.

Finance ministers and central bankers from the Group of 20 leading economies were pressing for more on China’s plans to tackle its slowdown, delegates at the meeting in Ankara said. Emerging market economies are concerned that a U.S. rate hike on top of the Chinese turmoil would pile on extra pressure, they said...

[But] a push by emerging market countries to characterise possible rate hikes in developed nations as a serious risk for the global economy was rejected by drafters of the G20 communique, a source from the Russian delegation said.

“Some emerging market countries wanted to fix a position,” the source told reporters, when asked whether the Fed’s expected rate hike would be mentioned in the communique...

Another G20 source said the wording would probably not go beyond a general caution to central banks to bear in mind the consequences of policy shifts.

“There will be no open demand to the Fed to act,” the source told Reuters.

Take your pick. #NFP pic.twitter.com/M2h4dUPFBU

— Josh Noble (@JoshTANoble) September 4, 2015

For all those believing the jobs data makes a rate rise this month less likely, there are others believing the opposite:

34% chance of Sep hike from 30% yesterday

— Ashraf Laidi (@alaidi) September 4, 2015

Markets selloff deepens after US jobs report

We warned earlier that a middling jobs report might not be good for markets.

And it turns out we were right. Europe’s stock markets are falling deeper into the red, knocking at least 2% off the main indices.

Wall Street is expected to fall back when it opens in 10 minutes.

Investors are still anxious, because there’s still no clarity on whether the Fed will push the button on rate hikes. Nor is it any clearer whether the US economy is strong enough to take it.

Marcus Bullus, trading director at MB Capital, says:

“It has been a turbulent fortnight and this latest jobs data will not assuage market fears.

The August figure is an unconvincing start to the Fall and will trigger even more concern in the markets about the state of the global economy.”

Here’s the damage in Europe right now:

Updated

Millennials are still struggling to break into the labor market:

The share of prime age Americans (25-54 years old) who have jobs still has not increased at all this year. pic.twitter.com/LeWdueD7io

— Binyamin Appelbaum (@BCAppelbaum) September 4, 2015

Updated

It may not feel like it, but the US economy has now achieved “full employment”.

So says Paul Ashworth of Capital Economics:

The decline in the unemployment rate leaves it in line with the Fed’s 5.0% to 5.2% estimate of the equilibrium long-run unemployment rate.

In short, the Fed just achieved the full employment part of its dual mandate.

Admittedly, the participation rate remained at a depressed 62.6% and that decline in the unemployment rate was partly due to a 41,000 decline in the labour force last month. But it was notable that the wider U6 measure of unemployment also fell again, to 10.3% from 10.4%.

Ashworth also believes a September rate hike is 50:50 toss-up, given today’s “fairly mixed” report.

Updated

ING: not strong enough for a rate hike

This is a particularly difficult Non-Farm Payroll to interpret, sighs Rob Carnell of ING.

It’s a “very mixed bag”. And for that reason, he doesn’t see the Fed raising rates this month:

The August US labour report delivered something for everyone. But in the end, we don’t think it is sufficiently strong enough for the Fed to proceed with a September rate hike without markets worrying that the data is not good enough to support it.

For that, we think we needed to see less ambiguity in these numbers – e.g. a clear surge in payrolls to back up falls in the unemployment rate and rising wages. And this didn’t happen.

Updated

The FT’s economics editor suggests Janet Yellen and colleagues shouldn’t give today’s Payroll much attention:

Mixed bag US labour market figs are a perfect example why it is ALWAYS nuts to base policy on monthly data

— Chris Giles (@ChrisGiles_) September 4, 2015

Analysts aren’t really sure what to make of this Non-Farm Payroll report.

One the one hand, fewer jobs were created than expected, suggesting the jobs market is weakening.

On the other, the unemployment rate continues to hit levels not seen since the financial crisis began, indicating ultra-loose monetary policy has done its job.

Who’d be a Fed policymaker, eh?

This is just about what a labour market report would like if *designed* to give few clues about the Fed.

— Duncan Weldon (@DuncanWeldon) September 4, 2015

Labor force participation rate still at 38-year low

At 62.6%, the US labor force participation rate is actually the joint-lowest rate since 1977.

That helps explain how the unemployment rate has dropped so much -- as it doesn’t include Americans who have dropped out the jobs market.

There are still 8.0 million unemployed in America, the BLS says. That includes 2.2 million who have been unemployed for at least 27 weeks.

And 6.5 million people were working part time for economic reasons in August.

America’s health care, social assistance and financial services firms all took on more staff last month, reports the Bureau for Labor Statistics.

Manufacturing and mining firms shed jobs, though.

The BLS also reports that the labor force participation rate was 62.6% in August for the third consecutive month. That means firms didn’t manage to lure more people into the labor market.

Updated

The ‘underemployment rate’, which measures whether people want to put in more hours, also dropped last month to 10.3% from 10.4%.

"Underemployment" is declining alongside official unemployment rate, although still above prerecession level. pic.twitter.com/tJMgCoJMl4

— Ben Casselman (@bencasselman) September 4, 2015

US workers’ hourly earnings beat expectations last month.

They rose by 0.3% in August, to $25.01, which is a 2.2% gain on last year. Wall Street expected 2.1%.

The Labor Department points out that August’s initial non-farm payroll reading tends to be revised up in future months (as mentioned earlier)

July’s payroll has been revised up from 215,000 to 245,000, making up for some of August’s shortfall.

June has been revised up by 14,000.

Updated

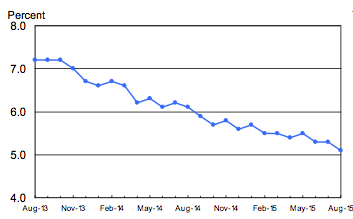

US unemployment rate hits seven-year low of 5.1%

Here we go!

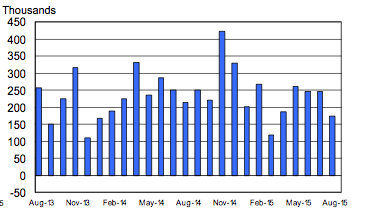

173,000 new jobs were created across the US economy last month, according to the Non-Farm Payroll.

That’s rather weaker than the 217,000 which economists expected. But June and July’s figures have been revised higher (details to follow).

And importantly -- the unemployment rate has fallen to its lowest level since March 2008, to just 5.1% from 5.3%.

That’s a bigger drop than Wall Street had pencilled in.

More to follow....

BREAKING: US created 173,000 jobs in Aug vs 220,000 expected; unemployment rate at 5.1% » http://t.co/tjCRv48D4Z

— CNBC Now (@CNBCnow) September 4, 2015

Updated

Just one minute to go.....

Could Jeffrey Lacker suspect that today’s report will miss forecasts, so he’s getting his rebuttal in early by arguing that it doesn’t matter too much?

Hint from Lacker? "Should the US jobs report for August turn out to be a weak one, it shouldn't deter the #Fed from raising rates this year"

— RANsquawk (@RANsquawk) September 4, 2015

Heads-up: Jeffrey Lacker, the president of the Richmond Fed, is arguing that today’s non-farm payroll shouldn’t derail the case for raising rates.

In a speech in Richmond, Lacker, a hawkish Fed policymaker, says that a poor August report would be a “one-month blip” that shouldn’t distract from the recent labour market recovery.

“I am not arguing that the economy is perfect, but nor is it on the ropes, requiring zero interest rates to get it back into the ring.”

Sounds like he’ll vote to raise rates this month.

Lacker says he has not made up his mind yet, will listen to debate at Sept FOMC.

— Carl Riccadonna (@Riccanomix) September 4, 2015

Updated

Non-Farm Payroll: What to watch for, and what we expect

The final, and most important, economic news of the week is going to be released in just 30 minutes time.

The US employment report is published at 1.30pm BST, or 8.30am EDT, giving important new insight into the state of America’s economy.

People have a habit of getting too excited about the Non-Farm Payroll. But this one does matter.

It will show how the world’s largest economy is faring, at a time of global unease. And it will be a crucial factor in deciding if the Federal Reserve raises interest rates this month.

The consensus is that around 217,00 new jobs were created last month. However, there’s massive uncertainty around that figure, which is why stock markets are all still in the red.

The unemployment rate is expected to drop again, from 5.3% to 5.2%. That would be fresh meat to the hawks on the Fed, who feel the economy doesn’t need ultra-low interest rates.

But other Fed policy makers will be watching the average hourly earnings figure. They are expected to show a rise of just 2.1% year-on-year; not a sign of a red-hot labour market that could drive inflation up.

If we get a strong payroll, the chances of an early rate rise will surely increase.

Ric Spooner, chief market analyst at CMC Markets in Sydney, says:

Given that the Fed is comfortable with the broad trend of job growth, a strong number would improve the atmosphere for a September rate hike.”

And that might drive shares up; after all, a strong labour market means a solid economy.

Shares could fall, though, if NFP is a bit weak. An increase of, say, 165,000 to 180,000 new jobs wouldn’t end the uncertainty gripping the markets.

As Chris Weston of IG put it:

This is a grey area and the scenario I feel would actually prove to be the worst case for market participants.

If you are an economist who has September or October pencilled in for Fed rate hikes then you probably wouldn’t amend that view, but the growth in job creation is lacklustre and would provide the least amount of clarity.

And we can’t rule out a really bad number -- which would probably spook traders:

BAML says the worst payrolls result for risk would be "a stinker" eg under 125K. #stinker

— Katie Martin (@katie_martin_fx) September 4, 2015

Unfortunately, August is a notoriously unpredictable month where Non-Farm Payroll is concerned. The initial number is usually revised by around 80,000 jobs!

Since 2010, no month has been upwardly revised more than August cc: @steveliesman pic.twitter.com/gDqXTkXkG7

— Squawk Box (@SquawkCNBC) September 4, 2015

More gloominess, this time from airline industry group IATA.

It reports that the amount of freight shipped by air aroug the world fell by 0.6% in July, having risen by 1.2% in June.

IATA Director General Tony Tyler warns that tough times are ahead, given the economic situation:

“The combination of China’s continued shift towards domestic markets, wider weakness in emerging markets, and slowing global trade indicates that it will continue to be a rough ride for air cargo in the months to come.”

The futures markets suggests US stocks will fall by around 1% when Wall Street opens in three hours time.

However, the US jobs report comes an hour earlier, and will have a major impact on the markets. Although as explained earlier, we could get a ‘middling’ reading that doesn’t give much clarity.

European shares keep dropping

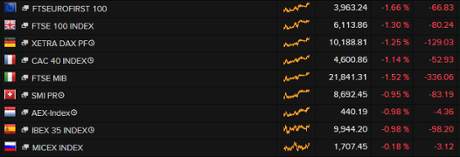

The selloff in Europe is accelerating, pushing the FTSE 100 down by 101 points or 1.6%.

Almost every share is down, led by retailers after it emerged August was the worst month for the sector since 2008:

Worries over the global economy, China, and the upcoming US employment report are all weighing on the markets and wiping out Thursday’s gains.

Yesterday’s rally, after the ECB suggested it could do more QE, looks rather overenthusiastic now.

As Conner Campbell of SpreadEX puts it:

It looks like the flip-flopping nature of markets is set to continue this Friday; after the Draghi-boosted highs on Thursday afternoon, the European indices seem to be in the midst of a harsh come-down this Friday morning, with all the major indices falling by over a percent.

Germany’s DAX is suffering even more, down 1.8%, as investors react to the worrying drop in German factory orders.

So its official then, we were over enthusiastic yesterday? #FTSE #DAX #CAC #INDU pic.twitter.com/KFHIp2lnMm

— Alastair McCaig (@AMcCaig_IG) September 4, 2015

Updated

The slump in German factory orders in July (see 8.03am) shows that the Chinese slowdown is hurting, say economists.

Ulrike Kastens, economist at German private bank Sal. Oppenheim, said the fall in factory orders in July was “disappointing,” though the “modest” upward trend in German industry continues thanks to growth in recent months.

While economic trends have improved within the eurozone, “developments in emerging markets, especially China, give cause for concern”.

“This will be a drag on German exports in coming months and will also dampen prospects for the world economy.”

Stefan Schilbe, economist at HSB Trinkaus, said domestic orders and from the rest of the eurozone had done well and falling oil prices should help.

“But the main problem is what happens to global trade. Orders from the rest of the world fell by nearly 10%. There aren’t enough growth drivers in the global economy. The USA looks solid, but many developing countries such as China, Brazil and Russia are under pressure. Countries that depend on raw materials like Canada and Australia are also struggling.”

(quotes via Reuters. Thanks to Julia Kollewe for the translations)

The European Central Bank has shaken off its anxiety over the eurozone economy, and pressed on with installing a large artwork shaped like a tree outside its headquarters.

No that’s not a joke.

See -->

@ecb The tree is currently installed and nice pic.twitter.com/5NCzUdtBPC

— Peter Ehrlich (@PeterEhrlich) September 4, 2015

Created by Italian artist Giuseppe Penone, it’s called “Gravity and Growth” -- (neatly encompassing the gravity of Europe’s growth problem). It’s made of bronze and granite, and a staggering 17 metres tall.

And how much has this little enterprise set us back? There’s no price tag on the tree, but the total competition to find three new artworks to brighten up the ECB HQ cost €1.25m!

Money better spent on a project to tackle eurozone unemployment, or the refugee crisis, perhaps.

The G20 will also resist blasting Beijing over the turbulence caused by its recent devaluation of the yuan, according to CNBC’s Steve Sedgwick.

#G20 Sources telling me (not unsurprisingly) NO criticism or even mention of #China specifically in draft Communique.

— Steve Sedgwick (@steve_sedgwick) September 4, 2015

G20 meeting: All about the Fed, eurozone QE, China and commodities

There are four challenges facing finance chiefs at their G20 meeting, Luxembourg finance minister Pierre Gramegna tells Bloomberg TV.

He’s hoping for a “frank and open” discussions on these points:

- The likely increase of US interest rates. “It’s not a secret, it’s going to happen.”

- Eurozone QE, with Mario Draghi pledging yesterday to do more if needed.

- The financial turmoil in China.

- The low commodity prices, especially oil, which is posing a lot of problems for emerging countries.

On China, Gramegna pointed out that China is still aiming for 7% growth this year, despite the slowdown in its manufacturing sector. That would be an “outstanding result”, compared to Europe.

But on the financial side, Gramegna warns that it’s “very difficult” to go against the market. As we may see on Monday, when the Shanghai index reopens....

G20 finance ministers fret about US rate hike

The prospect of a US interest rate hike is worrying top finance ministers and central bankers as they gather in Ankara for the G20 meeting.

A draft communique, seen by Bloomberg, warns that:

In line with the improving economic outlook, monetary policy tightening is more likely in some advanced economies, which may remain one of the main sources of uncertainty in financial markets.

However, the G20 meeting isn’t expected to lobby the Federal Reserve not to raise borrowing costs; it would, after all, be a sign of normalisation returning to the world economy.

Updated

Look who’s back!

Yanis Varoufakis, the former Greek finance minister, has just told CNBC that he won’t back Syriza’s Alexis Tsipras in the general election on September 20th.

BREAKING: Yanis Varoufakis tells CNBC: I'm not endorsing Tsipras in this election; he is still a friend but we have political disagreement

— CNBCWorld (@CNBCWorld) September 4, 2015

That disagreement is Tsipras’s decision to accept the tough conditions attached to Greece’s third bailout, rather than exiting the eurozone.

LIVE: Varoufakis: A 10 year old would know that (Greece's debt situation) would not end well http://t.co/bJppuJzX5m pic.twitter.com/auHdpiRG98

— CNBCWorld (@CNBCWorld) September 4, 2015

Varoufakis also declared that the political situation in Greece is toxic, with the country “on the foundations of an economy that’s imploding”.

Six months of brinksmanship and fruitless negotiations, leading to the introduction of capital controls, didn’t exactly help, of course....

Updated

European stocks fall around 1.4% in early trading

So much for the Draghi rally.

Europe’s stock markets are sliding back as trading gets underway.

In the City, the FTSE 100 quickly shed 80 points, led by retailers Next and Dixons Carphone (both down 3% after a broker downgrade) and then BP (down 2.7% as the oil price slides again)

This follows a late selloff on Wall Street, showing nervousness ahead of today’s US jobs report.

Tony Cross, market analyst at Trustnet Direct, says:

A fair chunk of yesterday’s gains have been wiped off London’s FTSE-100 index in the first few minutes of trade this morning with selling in the latter part of yesterday’s Wall Street session clearly taking a toll on sentiment.

Traders are now looking at screens awash with red numbers and even if today’s non-farm payrolls are seen as having no meaningful implications in driving a September rate hike, the Fed still has time to act before the year is out. Yesterday’s nascent rebound for commodity prices is also looking to be rather short lived – crude oil is slumping once again and as a result it’s little surprise that the natural resources stocks have been shunted towards the foot of the index.

John Lewis, that barometer of UK high street spending, has reported that sales at its department stores slid by 3.4% year-on-year in the last week of August. Not a great signal.

It admitted that “a tough trading period closed with another difficult week”, but is pinning its hopes on targeting “pent-up demand” in September.

Updated

We also have fresh signs of weakness in Europe’s powerhouse economy this morning.

German factory orders shrank by 1.4% in July, according to new data from the Economy Ministry. That’s a big reversal on June’s 1.8% rise in orders.

It’s a volatile measure, so caution is needed. But it reinforces Mario Draghi’s point yesterday - Europe’s economy isn’t too rosy.

Eurgh...some rather horrible factory orders from Germany -1.4% July vs June...much worse than expected

— Caroline Hyde (@CarolineHydeTV) September 4, 2015

Nikkei index hits seven-month low

A fresh bout of gloom swept Japan’s trading floor today, pushing the Nikkei index down by 2% to a fresh seven-month low.

Nikkei tumbles 2.2% to 17792.16 lowest since Feb on global de-risking. Falls 7% this week, worst week since Apr2014. pic.twitter.com/JZfgn3BoZ0

— Holger Zschaepitz (@Schuldensuehner) September 4, 2015

The selloff appears to have been triggered by renewed worries over the state of the global economy, after Mario Draghi warned yesterday that eurozone growth has slowed.

Tokyo traders also weren’t impressed by the latest Japanese wage data, which showed real earnings rose just 0.3%. That’s not enough to get Japan’s economy roaring.

Japanese wages: still stagnant http://t.co/Zgxe0rtST3 pic.twitter.com/qGRidw0qWs

— Patrick McGee (@PatrickMcGee_) September 4, 2015

Introduction: Nervous markets await US jobs report

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

Today is all about the US jobs report, and the possibility that the long run of record low interest rates is about to end.

Investors are hunkering down ahead of the Non-Farm Payroll, released at 1.30pm BST (8.30am EDT). It will show how many new jobs were created in August.

A strong reading could persuade the Federal Reserve to raise borrowing costs soon, perhaps this month, especially if it is accompanied by a decent rise in wages. A poor NFP could kick the first rate hike into 2016.

A middling report, though, will leave investors baffled about when the Fed will act, at a time when the global economy is looking weaker.

The Wall Street consensus is that the NFP will rise by 218,000, but as usual there’s wide variation, so it could be lively day.

Especially as Federal Reserve policy maker Jeffrey Lacker will give a speech just before the Non-Farm payroll is released, called “the case against further delay”......

Good Most-Important-NFP-ever-Day Morning

— Nicola Duke (@NicTrades) September 4, 2015

European stock markets are expected to slide by at least 1% this morning, having jumped yesterday after European Central Bank chief Mario Draghi hinted at more stimulus measures.

Our European opening calls: $FTSE 6106 down 88 $DAX 10155 down 163 $CAC 4576 down 77 $IBEX 9867 down 176 $MIB 21829 down 348

— IGSquawk (@IGSquawk) September 4, 2015

Asian markets have already dipped, even though the Chinese bourses are shut until Monday.

I guess #Draghi's speech never made it to Asia. #Nikkei turns sharply lower. pic.twitter.com/uSbxCOAzIo

— jeroen blokland (@jsblokland) September 4, 2015

We’ll also be tracking reaction to yesterday’s ECB press conference, and monitoring events in Turkey as G20 finance ministers and central bank chiefs meet.

Updated