And that’s all for today.

Our summary of Mario Draghi’s testimony to MEPs is here.

Back tomorrow.... Thanks all, and goodnight. GW

Draghi’s testimony even pushed shares a little higher in London, where the FTSE 100 just closed 17 points higher at 6671 points, a gain of 0.25%.

Jasper Lawler of CMC Markets says the ECB chief’s talk of possibly buying government bonds – and a takeover offer for botox-maker Allergan – took traders’ minds off the Japanese recession.

Markets in Europe traded between gains and losses for most of the session on Monday as investors weighed up slightly better growth at home, renewed M&A activity in the pharmaceutical sector against sharp growth contraction in Japan.

It was only after a speech from Mario Draghi that markets found their footing thanks to the prospects of sovereign bond purchases from the ECB.

The euro fell, and European stock markets rose, after Mario Draghi declared that:

“Other unconventional measures might entail the purchase of a variety of assets, one of which is government bonds.” .

The French CAC and the German DAX are both up around 0.7%, reversing the losses triggered by Japan’s return to recession.

The euro, though, has shed 0.6 of a cent against the US dollar, to $1.246.

Updated

Draghi is now taking further questions, in his role as chairman of the European Systemic Risk Board.

He’s told MEPs that future bank stress tests should include the risk of fines for misconduct.

Draghi Says Financial Sector Is Transferring Risk To Non-banks

— Steve Collins (@TradeDesk_Steve) November 17, 2014

Draghi testifies to the European Parliament - what we learned

OK, that’s the end of Mario Draghi’s testimony to the European Parliament in his role as president of the European Central Bank.

A reminder of the key points from the last couple of hours.

1) Draghi has urged European leaders and policymakers to deliver “concrete” short-term commitment for structural reforms in the member state, and to take steps towards long-term sharing of sovereignty to reinforce euro.

He said:

2015 needs to be the year when all actors in the euro area, governments and European institutions alike, will deploy a consistent common strategy to bring our economies back on track.

2) The ECB chief denied that Greece will require debt restructuring, insisting that its borrowing is sustainable if Athens sticks to its targets.

3) Draghi gave a clear signal that the ECB could begin buying eurozone government debt if its existing stimulus measures don’t bring inflation back to target.

The governing council is unanimous in its commitment to unconventional measures, he insisted, which:

“could include changes to the size and composition to the Eurosystem balance sheet, if warranted, to achieve price stability over the medium term.”

He then added:

“Other unconventional measures might entail the purchase of a variety of assets, one of which is government bonds,”.

4) Draghi defended the euro, saying it is “irreversible”. He denied that the single currency caused the structural problems and weak growth in the eurozone.

5) But he remains concerned about the state of the eurozone economy, saying current growth rates are dismal, and unemployment still too high.

6) And Draghi refused to accept that the ECB forced Ireland into applying for a bailout in 2010.....and also ruled out being a ‘formal’ part of Ireland’s bailout.

Updated

Draghi bursts into Italian, to answer a question about banking supervision. Then he apologises for yielding to his natural instincts.

Ever the pro, Draghi then translates his answer into English, (for the benefit of any ignorant Brits tuning in).

Eurozone banks have been tested robustly, and most passed our tests. But if problems arise in future, then the supervisory board will pick it up and deal with it, he says.

Draghi repeats that the ECB is committed to doing everything within its mandate, and wants people to understand that it is ready to act if more unconventional measures are needed.

Another Irish MEP asks whether Draghi will take part in Ireland’s inquiry into its bailout, will he make a senior official responsible to liaise with the inquiry, and will it release any necessary documents to help the inquiry?

Surely you agree, Mr Draghi, that the ECB should be accountable to the public. An Irish inquiry without the ECB would be like Hamlet without the prince.

Draghi agrees that the ECB must be accountable to the people, and indeed it already is, through this committee. So it won’t take a formal role in the inquiry – we might participate informally, but we haven’t decided yet.

And it won’t appoint a ‘point-person’ to help the inquiry.

Draghi: We will not formally participate in a national parliaments' inquiry; we have not decided on any informal participation

— ECB (@ecb) November 17, 2014

Not terribly helpful, frankly.

The euro area must grow more, Draghi insists.

Europe’s current economic performance is “dismal”, and the jobless levels - particularly for young people- is unacceptably high.

#Euro #ECB Draghi on Euro Area : current performance is dismal, unemployment is socially unacceptable..

— Shire Blogger (@Shireblogger) November 17, 2014

But he denies that the euro is the cause of this malaise -- look, most of the countries in the eurozone grew in the last quarter. Only two saw their economies shrink.

The eurozone must also “move from rules to institutions”, Draghi concludes, but he won’t say any more because it’s not in his remit.

Governments must deliver structural reforms even if they mean changing the way that countries have run for a long time, Draghi says.

And he claims that many eurozone members had lost monetary sovereignty long before the creation of the euro. Now they share sovereignty.

Will the ECB’s new asset-backed securities programme turn it into a bad bank?

NO, Draghi insists. He explains that the default rates between US ABS products (which often comprises sub-prime loans) is much, much higher than the ABS products which the ECB will buy.

Draghi: Default rates on ABS in US 18.5%, in Europe 1.5%. And we will only buy very specific ABS, which have even lower default rates

— FinSec Advisory Serv (@FinSec_com) November 17, 2014

And we will only buy the senior tranches of some ABS products -- to call the ECB a bad bank is not right, to say the least.

Furthermore, we will only buy mezzanine levels (the ‘riskier’ stuff), if there is a government guarantee.

Updated

Draghi says the ECB welcomes the new capital market union that was recently proposed by the EU’s president, Jean-Claude Juncker.

BREAKING: Mario Draghi says buying government bonds is an option if ECB decides to take additional easing steps.

— CNBC Now (@CNBCnow) November 17, 2014

Here’s the quote from Draghi, confirming that the ECB could potentially start buying government bonds:

Mario Draghi: "The other unconventional measures might entail the purchase of a variety of assets, one of which is govt bonds’’ BBG #EU

— Richard Bravo (@richbravo2) November 17, 2014

Draghi: ECB could purchase sovereign bonds

Draghi causes a little stir by saying that the ECB could potentially start buying sovereign debt, if necessary.

But he also defends the decisions taken so far - saying the ECB’s monetary policy has been “extraordinarily successful in reducing interest rates”. Some are even lower than in the United States, even without resorting to quantitative easing.

Draghi Says Expanded Purchase Program Could Include Govt Bonds

— Steve Collins (@TradeDesk_Steve) November 17, 2014

If #Draghi does not get this market up by these statements of buying sovereign govt bonds then he is out of ammo...

— Lex van Dam (@lexvandam) November 17, 2014

Reminder -- the bottom line is that the ECB will do everything possible within its mandate...

A German MEP queries the measures take by the ECB recently - is everything really ok?

Draghi replies that the measures taken since June (such as starting to buy asset-backed securities), should have a positive effect. But the governing council is committed to taking further unconventional measures if needed.

It’s all about hitting our mandate of inflation close to, but below 2%, he smiles.

First German query. #Draghi: Between June & Sept the ECB has undertaken its new programmes...we are confident...(regurgitates same answer)

— Dr Ausberto Torres (@aussietorres) November 17, 2014

German member asks #Draghi in German: " Are you sure everything is ok?" Terrific!!!! #EP

— Dr Ausberto Torres (@aussietorres) November 17, 2014

Drink!

Draghi: The euro is irreversible.

— ECB (@ecb) November 17, 2014

He was answering a question on whether member states may leave the euro - we don’t have the legal power to keep members in, but our position, as we’ve said before, is that the euro is irreversible.

Draghi ducks a question about the LuxLeaks scandal - saying the ECB does not, yet anyway, have authority over taxation in Europe.

Another MEP who asks under what authority the ECB had instructed Dublin to seek a bailout in 2010.

Draghi tries to slap him down -- don’t you think the ECB should act in the interest of all member states, including those who have been helping Ireland?

Draghi answers angrily "Don't you think the #ECB should act in situations like this?" hahahaaa

— Dr Ausberto Torres (@aussietorres) November 17, 2014

To get up to speed on the Irish letters, check out this piece in the Economist. It explains how Jean-Claude Trichet made an “imperious” demand that Ireland should seek a bailout, else the ECB would withdraw its support for the Irish banking sector.

What particularly sticks in the Irish craw is Mr Trichet’s imperious tone. His letter makes four demands: Ireland must request financial support from the Eurogroup (euro-zone finance ministers); the request must include a commitment to austerity, structural reforms and a clean-up of the banking sector; recapitalisation of banks; and a guarantee of the repayment of ELA funds.

Draghi: By early Nov 2010 situation in Ireland had rapidly deteriorated and Governing Council had a duty to address that issue

— ECB (@ecb) November 17, 2014

A series of questions about Ireland’s bailout in 2010, the decision to release letters between Draghi’s predecessor Jean-Claude Trichet, and the ECB’s advise that Ireland should not ‘burn’ senior bondholders.

Draghi replies that it wasn’t the ECB’s fault that Ireland took a bailout.

Instead, it was the government’s decision to guarantee bank losses, the sheer scale of the domestic crisis, aggravating external factors, and the loss of market confidence that made a bailout inevitable.

It’s not just about the letters, he insists.

Draghi doesn't really look like the letter writing type..

— Lorcan Roche Kelly (@LorcanRK) November 17, 2014

The eurosystem also provided huge support to Ireland’s banks in the run-up to the bailout. But there are limits...

And the governing council had a duty to consider the deteriorating situation in Ireland, which prompted the letter from Trichet.

Updated

Another question: Would an ECB quantitative easing programme deter countries from implementing structural reforms, or from using the fiscal headroom available to them? [a hint about Germany and its reluctance to borrow more to stimulate growth]

Draghi denies that eurozone countries have been deterred from taking action because they have been showered with money, or because interest rates are very low or very high.

Draghi: Countries have reformed, even when interest rates were already very low

— ECB (@ecb) November 17, 2014

A question about whether Greece needs debt restructuring.

If Greece stays on course and hits its commitments, its debt will remain sustainable, Mario Draghi replies.

We don’t think a debt restructuring is needed, and we don’t think it would be useful.

Greece must focus on the need for further reforms to deliver competitiveness - we can see that the work it has implemented is paying off.

And he insists that the ECB has not made a profit on the Greek bailout - those profits were returned.

Draghi: ECB profits have been returned to Greece

— ECB (@ecb) November 17, 2014

Asked about the need for structural reforms, Draghi says that they aren’t the only answer.

But, “we now see that the countries that are growing faster are the ones where some structural reforms have taken place”.

GDP data released on Friday showed Spain and Greece both growing, but Italy entering another recession.

Draghi: 2015 must be year of eurozone action

Mario Draghi concludes with a loud call to arms to the European parliament, and to politicians and central bankers across the eurozone.

He declares that:

2014 has been a year of profound change, but what has been achieved so far is not enough.

2015 needs to be the year when all actors in the euro area, governments and European institutions alike, will deploy a consistent common strategy to bring our economies back on track.

Monetary policy alone will not be able to achieve this.

This is why there is an urgent need to agree on a concrete short-term commitment for structural reforms in the member states, on a consequent application of the stability and growth pact....on the aggregate fiscal stance for the euro area, and on a strategy for investment....

....and to launch work on a long-term vision to further share sovereignty, ensuring the sustainable and smooth functioning of the European Monetary Union.

Draghi’s now taking questions; I’ll keep an eye for any fireworks.

Now Draghi is talking about how the ECB provides liquidity to banks by offering them credit in return for collateral (various financial assets).

He is trying to reassure MEPS that these activities have a good track record. The eurosystem has never made a loss through these collateral programme -- in the rare cases of a financial crisis, the ECB recovered its collateral by seizing the underlying assets that banks had placed with it.

So far the Euro system has not yet realised a loss from our credit operations...we recovered from Lehman by claiming back collateral- Draghi

— Dr Ausberto Torres (@aussietorres) November 17, 2014

Draghi: However, monetary policy alone cannot overcome financial fragmentation in the euro area @acardenasfx

— DAVID LOYO (@rasecfx) November 17, 2014

Draghi moves onto a reminder that monetary policy can’t do everything itself. National governments must act too, and implement structural reforms

Draghi: We have tasked relevant staff and committees with the timely preparation of further measures to be implemented, if needed

— ECB (@ecb) November 17, 2014

Mario Draghi repeats some key news lines from the ECB’s most recent governing council meeting -- the GC is unanimously committed to expanding its balance sheet towards 2012 levels, and has tasked staff to develop further measures if needed.

Draghi says the ECB can see early indications that its credit easing package is delivering tangible benefits, but a full recovery will take some time.

#Draghi looks pretty tired.

— stewart hampton (@stewhampton) November 17, 2014

Credit market fragmentation has made it harder for the ECB to fulfil its mandate, Draghi says.

Some markets have improved recently, but other credit markets are still impaired. So overall credit availability is still tight on a historical basis.

And some banks are failing to fully pass the improvements in credit availability onto customers, he warns.

Draghi tells the committee that the ECB still expects a moderate pick-up in growth next year. But, euro area growth momentum did weaken over the summer.

And the risks to the economic outlook continue to be to the downside.

This chimes with his statement at the ECB’s most recent monthly press conference, two weeks ago.

Updated

Mario Draghi begins by telling MEPs that 2014 has been a year of profound change. He cites the changes to the way eurozone banks are supervised and regulated.

He also says that 2014 was “a challenging year for monetary policy”, which saw the ECB takes a number of measures to address an increasingly sobering financial landscape.

Mario Draghi’s testimony at the European Parliament is just starting now.... (livefeed here)

Capital Economics reckons the Japanese yen will weaken sharply in 2015, from around ¥116 to the $1 today to ¥140 next year.

Capital Economics on Japan recession: "we now expect the yen to fall to 140 against the dollar next year"

— Sara Eisen (@SaraEisen) November 17, 2014

Photos: demonstrations in Greece

Over in Greece, demonstrators marking the 1973 Athens Polytechnic uprising – the event that triggered the fall of seven years of hated military dictatorship the following year – are amassing in the Greek capital.

From Athens, Helena Smith reports:

7000 police, many in riot gear, have been deployed around the centre of Athens following clashes last week in the run-up to the anniversary.

Protesters, who blame swingeing EU-IMF mandated austerity cuts for plummeting living standards and problems in the education system, will stage a march to the US embassy this afternoon. Washington is widely blamed for backing the military dictatorship which sent in tanks to crush the student revolt, killing dozens in the process.

The protests come three days after Greece officially returned to growth, and amid confusion over how it will exit its bailout package.

Tensions are running high as despondency grows with Greece’s governing coalition.

Panos Garganas, a veteran leftist mingling with the crowd gathered outside the Polytechnic, explains:

“It is quite clear that despite all the talk of success the economy has seized up and the government is in no position to leave the bailout program and go out to the markets,”

“We are essentially in a pre-election period. A new government will have to negotiate with creditors when elections are held early next year, which everyone believes.”

Heads-up: Mario Draghi, ECB chief, will begin testifying to the European Parliament Committee on Economic and Monetary Affairs. in 10 minutes.

.@EP_Economics discusses with Mario #Draghi at 15:00 the @ECB 's perspective on economic & monetary developments.LIVE http://t.co/JlQO1eIiwY

— EP PressService (@EuroParlPress) November 17, 2014

Lunchtime summary

Time for a recap.

Japan’s stock market has suffered its biggest fall in three months, as the unexpected news that the country is back in recession spooked the Tokyo stock market.

The yen also crashed into a new seven year low after Japanese GDP shrank at an annual rate of 1.6%.

Economists blamed the government’s decision to raise the sales tax this year, and its plan for a second hike in 2015. Reaction starts here

European markets have now recovered their earlier losses, as speculation grows that prime minister Shinzo Abe will tomorrow announce a snap general election and postpone the sales tax in increase until 2016.

The disappointing data came hours after David Cameron cautioned that risks in the global economy are growing. Chancellor George Osborne repeated that warning today.

"Europe remains very weak... not immune from that...that's why red lights are warning... " Mr Osborne says in Rochester in a neon jacket

— Faisal Islam (@faisalislam) November 17, 2014

Japan’s surprise slide into recession has shown the limits of monetary policy in fighting the country’s economic malaise, says Stephen Lewis of ADM Investor Services:

The truth that emerges clearly from Japan’s experience so far this year is that fiscal policy nowadays exerts a much more powerful effect than monetary policy.

The BoJ’s unprecedented efforts, injecting liquidity through its QQE policy, have left Japan’s economy still slumping while consumer price inflation, stripping out the effects of the sales tax increase, is beginning to slip, despite households’ expectation that it is on a solid rising trend.

The effects of monetary policy are hard to trace while the effects of April’s fiscal adjustment are plain to see.

In other news....

Its president, Jens Weidmann, has also hit out at calls for QE in the eurozone.

Europe’s trade surplus has grown again, as has Britain’s trade deficit with the eurozone.

Delaying the planned sales tax hike would help Japan achieve ‘escape velocity’ levels of growth, according to Jesper Koll of JP Morgan (speaking on Bloomberg TV a moment ago)

And this chart shows how Japan’s economy has struggled since the financial crisis began, with growth lagging behind the US, Germany, Britain and (even) France.

Japan GDP -1.3% v pre-crisis peak (US +7.7%, UK +3.4%, Ger +3.1%, Fra +1.4%, Spa -5.8%, Ita -9.4%, EZ -2.2%) pic.twitter.com/9k827qkPvN

— Chris Williamson (@WilliamsonChris) November 17, 2014

Japan’s slide into recession is worryingly reminiscent of 1997.

Then, the Hashimoto government decided to raise the sales tax in an attempt to rebuild the country’s fiscal position. But the move may have backfired -- a strong-looking recovery was snuffed out and Japan fell into an 18-month long recession.

It’s hard to pin all the blame on the sales tax hike -- 1997 was also the year of the Asian currency crisis. But it’s a reminder of the difficulty in turning Japan’s economy around over the last 20 years.

Will Japan ever raise their sales tax again, after what just happened w/ Q2+Q3 GDP, after 1997 crisis? Fiscal reform w/Abe = dead. $USDJPY

— Christopher Vecchio (@CVecchioFX) November 17, 2014

Over in Rochester, Kent, the UK chancellor George Osborne has repeated David Cameron’s warning that the eurozone is a threat to the UK:

"Europe remains very weak... not immune from that...that's why red lights are warning... " Mr Osborne says in Rochester in a neon jacket

— Faisal Islam (@faisalislam) November 17, 2014

Osborne is campaigning ahead of Thursday’s by-election, which could well be won by UKIP.

Our politics live-blogger Andy Sparrow has all the details:

Rochester byelection hustings: Politics Live blog

For an alternative take on Germany, check out Wolfgang Munchau in the Financial Times today.

Munchau argues that German economists and politicians are hamstrung by their devotion to the “ordoliberal” policies that emerged from the trauma of the 1920s and 1930s.

In short, the belief that governments must set and enforce rules, not just fix the damage when they are broken. That’s not easily compatible with monetary union with other countries.

Here’s a flavour:

The ordoliberal doctrine may even have worked well for Germany, though I suspect that the country’s economic success is due mostly to technology, high skills and the presence of some excellent companies, rather than to economic policy.

Through its dominance of the euro system, Germany is exporting ordoliberal ideology to the rest of the single currency bloc. It is hard to think of a doctrine that is more ill suited to a monetary union with such diverse legal traditions, political system and economic conditions than this one. And it is equally hard to see Germany ever giving up on this. As a result the economic costs of crisis resolution will be extremely large.

Full piece here (behind the FT paywall).

Great lede from Munchau's latest, "The wacky economics of Germany’s parallel universe" (http://t.co/Criaixs6wF)... pic.twitter.com/cxRW1qNSrz

— Cardiff Garcia (@CardiffGarcia) November 17, 2014

The Bundesbank’s chief, Jens Weidmann, has also attacked the idea that the European Central Bank should embark on a larger stimulus programme.

He told the Handelsblatt newspaper that the ECB should resist pressure for a full-blown quantitative easing programme (buying sovereign debt with new money).

He argued:

“Such purchases might create new incentives to run up debt, besides adding to the reform fatigue in a number of countries.”

Business Insider has a good take.

The Germans just don't seem to care that we're on the brink of a continent-wide recession http://t.co/wg01yU0LGS via @BI_Europe

— Jim Edwards (@Jim_Edwards) November 17, 2014

Bundesbank says German growth will be sluggish in Q4

Meanwhile in Germany, the Bundesbank has warned that economic growth in Europe’s largest economy will remain weak for the next few months.

In its latest monthly report, the German central bank says:

“The further deterioration in economic expectations and the stagnation of new orders point to a rather sluggish course of economic development in Germany until at least the end of 2014.”

And the rest of Europe is little better:

“No marked recovery in important euro-area partner countries has yet materialised.”

Some economists argue that Germany should respond to this stagnation by raising government spending, rather than insisting on achieving a balanced budget.

The Bundesbank knows better, though, arguing:

“An additional, debt-financed economic package...would not be constructive for the economic situation in Germany, or the comparatively meagre stimuli it is expected to give to the rest of the euro zone,” the Bundesbank said in its monthly report.

“In view of the considerable uncertainty surrounding the global and European economy, it seems appropriate for the moment to continue in the fiscal direction laid out in previous planning.”

Disagree? Check out the full report here (in German)

Updated

#Bank control needs to fall under criminal legislation, regulars need to carry badges, not business cards.

— Ralph Silva (@rsilvalondon) November 17, 2014

Banking analyst Ralph Silva has applauded Bank of England governor Mark Carney’s proposal that bankers’ fixed pay should be clawback-able (see 9.01am post for details).

Controlling #bankers is controlling compensation, not bonuses, Mark #Carney gets it! He also talked about criminal sanctions. #banks beware

— Ralph Silva (@rsilvalondon) November 17, 2014

The mood in the financial markets has also been dented by the events at the G20 summit in Brisbane last weekend, where Vladimir Putin faced the unhappiness of fellow world leaders over the Ukraine crisis.

As IG’s Alastair McCaig explains:

Rather than the plethora of sound bite-friendly empty promises that we have become accustomed to, the focus was disproportionately on sanctions against G20 member Russia.

Japan’s recession has added to those concerns:

Japan’s problems are far greater than markets had assumed and the likelihood of snap elections has taken a step closer.

Vladimir Putin’s presence and early departure from this weekend’s latest G20 summit ensured that sentiment was already frosty before this disappointment.

Starting to look like Japan might be facing a European-style lost decade.

— Sam Bowman (@s8mb) November 17, 2014

With Abenomics looking ropey, Japan’s prime minister may be tempted to unleash more fiscal firepower to drive the economy back to growth.

But Japan’s precarious financial position doesn’t give Shinzo Abe much freedom. Especially as the unpopular sales tax hike - now to be postponed - was designed to show that Tokyo was serious about tackling its huge debt pile.

Fung Siu, Japan analyst at The Economist Intelligence Unit, says the Bank of Japan will need to maintain its bold stimulus packages:

The government will be keen to draft a fiscal stimulus package, but given the precarious state of the public finances--there isn’t much room for maneouvre here and any package is unlikely to match the size of the previous supplementary budget (implemented in January 2014).

The weak data are a major setback for the BOJ and it now might take even longer for it to meet its inflation target of 2%, meaning that it is unlikely to end its ultra-loose monetary policy any time soon.

Updated

Japan in recession: latest reaction

Back to the news that Japan is in recession, after GDP shrank by another 0.4% in the third quarter of the year.

Nicholas Ebisch, currency analyst for Caxton FX, reckons that the yen is likely to weaken further.

With the Yen already in a weakened position after a surprise round of monetary stimulus announced very recently, this could cause the world’s third most traded currency to crumble further. This poor GDP reading is likely to have a detrimental effect on stock markets in Asia and have a ripple effect on equity markets abroad.

However, stock markets should be cushioned by the fact that Friday’s eurozone GDP data was better than feared (Germany avoided recession).

Although Japan officially now falls into the definition of a recessionary period (two consecutive quarters of economic contraction), it seems unlikely that this would cause a steep global equity downturn for more than a few days.

Updated

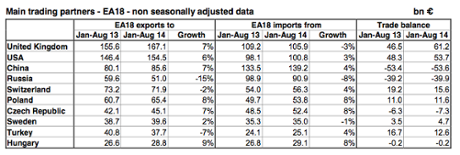

Eurozone trade surplus jumps

Just in...... the eurozone’s trade surplus has doubled month-on month.

Latest data from Eurostat show that the eurozone’s trade in goods with the rest of the world jumped to €18.5bn in September, up from €8.6bn in August and €10.8bn in September 2013.

Exports rose by 4.2% month-on-month, while imports rose by just 3.0%.

But Britain’s trade gap with the euro area has widened this year, suggesting the weak euro economy and stronger pound are hitting British companies.

In the first eight months of 2014, eurozone countries exported 7% more goods to the UK than a year ago, but imported 3% less.

Eurozone exports to China are also up by 7% between January and August, but exports to Russia are down 15% as sanctions take their toll.

This chart has more details:

Eurostat also reports that Germany has the biggest trade surplus of any European Union member, and Britain the biggest deficit.

The largest surplus was observed in Germany (+€138.8bn in January-August 2014), followed by the Netherlands (+€38.5bn), Italy (+€26.2bn), Ireland (+€23.2bn) and the Czech Republic (+€10.8bn).

The United Kingdom (-€89.8 bn) registered the largest deficit, followed by France (-€49.3 bn), Spain (-€16.6 bn) and Greece (-€13.6 bn).

Andy Haldane isn’t the only person feeling dovish about UK interest rates:

HSBC has shifted its BoE rate hike call by a YEAR. Q1 2015 -> Q1 2016.

— Peter Spence (@Pete_Spence) November 17, 2014

Haldane: I'm watching inflation expectations like a dove

When it comes to crisp wordplay and biting insights, it’s hard to beat a speech from Andy Haldane.

And Haldane fans will be pleased to hear that the Bank of England’s chief economist has spoken about central bank psychology, in London this morning.

He begins by reminding the audience that the BoE was holding a conference on the “Great Moderation” on 13 September 2007, the day when Northern Rock began to implode as the wheels came off the financial system.

As Haldane put it:

As Great Recession abruptly replaced Great Moderation, it was clear a grave analytical and policy error had been made. Economic and financial pride had come before a momentous fall.

Nemesis had duly followed hubris. It was the coldest of comforts that this cognitive lapse was shared by the whole economic and policy-making profession.

He goes on to warn that economists, like any collective, can be guilty of groupthink -- looking for evidence that confirms past beliefs.

This, rather than alcohol, is why drunks search for lost keys under the lamppost.

The broad sweep of Haldane’s speech is that he’s shaking up the Bank of England’s forecasting unit to help it understand its biases and learn from its mistakes.

But he also hints that he is far from ready to vote for an interest rate hike, as there are signs that UK households expect inflation to be lower in the months ahead.

Here’s the key section:

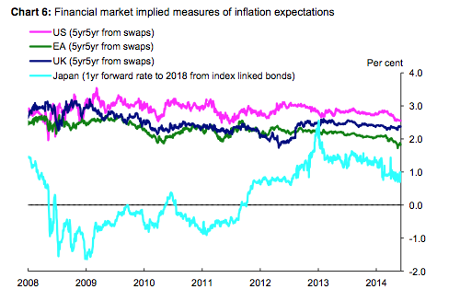

Friedrich Hayek likened the process of controlling the economy as akin to taking a tiger by the tail. As far as inflation control is concerned, Hayek was right. As some countries are finding today, the tiger is capable of biting back.

Chart 6 plots inflation expectations from financial markets in the UK, US, the euro-area and Japan over recent years. In Japan, inflation expectations have been anything but well-anchored, varying significantly around a trend close to zero. Most recently, they have been falling once again. The same is true in the euro-area and, to lesser extent, in the US.

So far, inflation expectations in the UK have held up and, on a central view, the Bank expects inflation to be on target at a 2-3 year horizon. But this tiger needs careful handling. Even in the UK, some measures of household inflation expectations have fallen slightly over the course of this year. The tiger has stirred.

Wearing my MPC hat, and with UK inflation already below target, this is something I am watching like a dove.

Here’s the full speech: Central bank psychology

Updated

Mark Carney: Can't just blame bad apples for financial crisis

Mark Carney, the Bank of England governor, has argued that bankers’ basic pay may need to be controlled if the financial sector is ever to put recent scandals behind it.

In a speech in Singapore, Carney argued that much progress has been made since 2007 to make banks safer and simpler. However, finance must now

The governor channelled Winston Churchill (during his time as chancellor of the exchequer) by saying:

It is not merely that we should want to follow Churchill’s wish to see “finance less proud and industry more content”.

We want to see industry content and finance taking justifiable pride in its contribution to society.

That is hard, when the public are bombarded with tales of rigging in the financial market. Just last week, for example, 6 banks were fined around £2.6bn for failing to prevent their traders from manipulating the foreign exchange markets.

Carney warned:

As Bill Dudley and my colleague Minouche Shafik have argued, the succession of scandals mean it is simply untenable now to argue that the problem is one of a few bad apples. The issue is with the barrels in which they are stored.

Leaders and senior managers must be personally responsible for setting the cultural norms of their institutions. But in some parts of the financial sector the link between seniority and accountability had become blurred and, in some cases, severed.

The solution may include closer control of bankers’ fixed pay, making it easier to claw it back:

Standards may need to be developed to put non-bonus or fixed pay at risk. That could potentially be achieved through payment in instruments other than cash. Bill Dudley’s recent proposal for certain staff to be paid partly in ‘performance bonds’ is worthy of investigation as a potentially elegant solution....

The full speech is here (pdf): The future of financial reform

Updated

Our latest news story on Japan's recesssion

From Tokyo, my colleague Justin McCurry reports that the Japanese government is widely expected to can the proposed sales tax hike tomorrow, and announce a snap general election:

Abe now faces a difficult balancing act: whether to address Japan’s huge public debt – now more than twice the size of its economy – by pushing ahead with what would be a deeply unpopular tax hike, or hold off and attempt to kickstart growth.

All the indications are that Abe will opt for a delay in the tax rise and call a snap election on Tuesday. Voters will probably to go to the polls in mid-December, just halfway through his current term.

“In light of the sharp fall in today’s preliminary estimate, it now looks likely that PM Abe will call off the hike and announce snap elections,” said Marcel Thieliant at Capital Economics.

Here’s Justin’s full story: Japanese recession figures prompt talk of snap election

Analysts at Daiwa reckon that PM Shinzo Abe’s LDP party would be returned to power, despite the recession:

Daiwa on Japan election: 'Given the opposition’s disarray, the main question then will be... the eventual size of the ruling LDP’s majority'

— Mike Bird (@Birdyword) November 17, 2014

Michael Hewson of CMC Markets agrees that Japan’s unexpected slump has hit the mood in Europe:

European trading this week looks set to continue the weaker theme this morning as we get set to open lower after economic data showed that Japan slipped back into recession as the economy contracted 0.4% in Q3, underlining the recent decision by the Bank of Japan to increase its stimulus program.

The main European stock indices have dropped at the start of trading, as Japan’s recession weighs on the markets.

The German DAX and Italian FTSE MIB both shed 1%, and the French CAC is down 0.8%.

And in London the FTSE 100 dropped 30 points, or 0.4%, at the open to 6626. Supermarket chains are leading the fallers:

#FTSE opens down 04% after Japan enters recession. Biggest fallers Sainsbury (-1.9%) then Tesco (-1.9%)

— Garry White (@GarryWhite) November 17, 2014

Mike van Dulken, head of research at Accendo Markets, says investors are cautious in the face of:

uneven growth, financial risks, geopolitics, waning demand and the threat of a European (and now Japanese) recession.

Updated

Japan’s recession shows that there simply isn’t enough demand to sustain global growth and inflation, argues Daniel Alpert, managing partner of investment bank Westwood Capital.

#Nikkei down 430 points. US 10 year down 4 bps. Countries tossing around "hot potato" of inadequate demand. Today Japan dropped it. #USNext

— Dan Alpert (@DanielAlpert) November 17, 2014

How seriously should we take David Cameron’s warning that “red lights are flashing” for the global economy?

Our economics editor Larry Elliott says that Cameron is absolutely right to be worrying about the eurozone (a clear red-flag risk). Geopolitics and slowing emerging markets are also a concern. Global trade talks? Not so much.

Larry writes:

The first problem he identifies is Europe, where he fears a third recession in the eurozone will lead to deflation. Given that the single currency area has never recovered from the financial and economic crisis of 2007-09, this is justified. There are already signs that the latest slowdown in Europe is having an impact on UK exports. Warning light rating: bright red.

A slowdown in emerging markets is the second risk highlighted by the prime minister. This is less problematical for the UK. Some emerging market economies – such as Brazil and Russia – have weakened, but China is still expanding at 7% a year while the worst of India’s problems seem to be behind it. What’s more, the UK exports more to the Netherlands than it does to the Bric (Brazil, Russia, India and China) countries combined. Warning light rating: amber.

Here’s his full analysis: David Cameron’s economic warning lights: dark days ahead?

By identifying these concerns so boldly, the PM is also putting the economy at the centre of next May’s general election. And also, perhaps, encouraging the voters to blame the situation overseas rather than domestic problems if things do turn sour over the next six months....

The Japanese recession a “big macro-economic shock’, says Ian Williams of Peel Hunt.

Williams is alarmed that domestic demand was so weak in the last quarter, with household consumption and business investment below forecast.

The data increase the likelihood of PM Abe postponing the next sales tax hike and calling a snap election.

Reuters reckons that the election could be announced as early as tomorrow....

UBS’s former chief economist, George Magnus, is confident that prime minister Abe will now postpone the plan to raise Japan’s sales tax, from 8% to 10%.

Japan’s plight also shows the limits of quantitative easing (QE), he adds.

So what did we lesson overnight from the East? Japan's back in recession. Abe's tax hike 2,0 will be postponed. QE and growth bad bedfellows

— George Magnus (@georgemagnus1) November 17, 2014

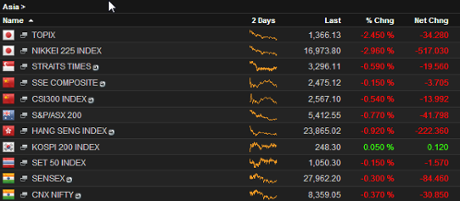

Nikkei tumbles 3%

Shares have tumbled in Tokyo after Japan fell back into recession, and there were losses across the region.

The Nikkei index of leading Japanese shares suffered its biggest one-day fall since August, shedding almost 3%.

Stan Shamu of IG says:

Japan’s GDP release has been a key turning point for the session as optimism swiftly waned and traders took profits on equities and USD/JPY [positions on the US dollar versus the yen].

This week has been pinned as key for Abenomics and so far it certainly has not been a good start.

The yen weakened sharply when the GDP data was released, hitting a seven year low of 117 yen to the $1. It then recovered a little, as traders tried to work out the implications of the recession.

Updated

Good morning, Europe. Here's a chart of Japan entering recession (again). pic.twitter.com/V2dFPjlHlZ

— Patrick McGee (@PatrickMcGee_) November 17, 2014

Japan back in recession

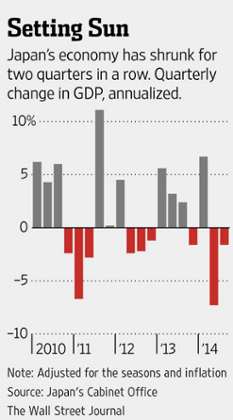

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

The storm clouds gathering over the global economy have darkened this morning, with the unexpected news that Japan has fallen back into recession.

Data released overnight shows that Japanese GDP shrank by 0.4% in the third quarter of 2014 (or 1.6% on an annualised basis), dashing hopes of a return to growth.

The news sent shares sliding in Japan, and pushed the yen down to a new seven-year low against the US dollar.

It’s a bruising blow to prime minister Shinzo Abe, who was rumoured to have been considering a snap general election.

And Abe’s plan to raise Japan’s sales tax next year is being blamed for causing the recession. Japanese firms cut back their inventories drastically during the quarter, in anticipation of falling demand.

As Junko Nishioka, an economist at RBS Japan Securities, explains:

“The impact of the sales tax was much more severe than expected.”

It now appears even more likely that Abe will postpone that sales tax hike now.

But Japanese household consumption and capital spending only rose a little during the quarter, highlighting the weakness of its economy.

As this chart from the Wall Street Journal shows, this is Japan’s third recession in the last four years (and the fourth since the collapse of Lehman Brothers).

The news came just a couple of hours after David Cameron warned that the global economy could be heading a new crisis.

“Red warning lights are flashing on the dashboard of the global economy”, the prime minister warned, as the G20 meeting of world leaders ended.

Writing in the Guardian (where else?), Cameron warned that the eurozone is on the brink of another recession, emerging markets are slowing down, and world trade talks have stalled. The ebola epidemic, and geopolitical crises in Ukraine and the Middle East, also threaten stability, he added.

And that’s even without Japan’s fall back in recession....

Full story: Red lights are flashing on the global economy

I’ll be tracking all the key events and reaction through the day.

There’s not much in the calendar, but European Central Bank chief Mario Draghi is testifying to the European Parliament at 2pm BST....

Updated