Closing summary: Greece in the spotlight as snap presidential election looms

Greece’s drive to exit its bailout programme has taken a dramatic twist tonight, putting the country’s political stability back in the spotlight.

The drama began this evening when Eurozone finance ministers decided to allow Athens a two-month extension to its current loans programme, which was due to run out at the end of December.

This is designed to give Greece time to meet the outstanding demands of the Troika, and means it will not exit part of its four-year bailout by the new year, as it hoped.

The extension will also allow the lenders more time to assess if a black hole is lurking in Greece’s 2015 budget.

And shortly afterwards, Greeks were stunned to learn that the upcoming presidential election will be brought forward. This ballot, involving members of parliament, is on a knife-edge, given the coalition’s thin majority in parliament.

The first ballot takes place on December 17. With barely a week to go, we don’t know who any of the candidates are, but PM Antonis Samaras is due to reveal his choice on Tuesday.

Meanwhile in #Greece, fact that Presidential Election date is set without a candidate name (!) shows hasty nature of govt's decision

— ThePressProject EN (@PressProject_EN) December 8, 2014

A spokesman said the move will:

“prevent the opposition from undermining Greece’s economy and directing messages of political uncertainty to financial markets”.

If Samaras cannot secure the support of three fifths of MPs by a third vote, on December 27th or 29th (reports vary), then he could be forced to call early elections. Given he has 155 seats in the 300-strong parliament, the vote could be close....

Economists and analysts say the next few weeks will be dramatic. It could result in the left-wing Syriza party taking power. Syriza, indeed, has already predicted that Samaras simply doesn’t have the votes to win the presidential ballot.

Syriza wants a debt restructuring to put Greece on a firmer footing, which could create another chapter in the ongoing eurozone crisis.

Hello 1Q Eurozone crisis MT “@graemewearden: Greece brings forward presidential poll. http://t.co/V67YnW0bgA”

— Charlie Robertson (@RencapMan) December 8, 2014

Do scroll back through the blog for more expert reaction and early analysis.

I’ll be back tomorrow morning to cover full reaction to the latest developments. Goodnight! GW

Updated

Here’s a photo from inside the eurogroup meeting of finance ministers today:

And here’s the press conference, where we learned Greece has been given two more months to tie up the outstanding measures demanded by its lenders:

A couple more names in the mix for the presidential race that dramatically opened up tonight.

EU Commissioner @Avramopoulos, former EU Commr Dimas, former EU Ombudsman Diamandouros r thought to b on the short list for Greek Presidency

— Yannis Koutsomitis (@YanniKouts) December 8, 2014

Another possible presidential candidate, apparently, is former prime minister Kostas Karamanlis.

My money is on ex-PM Kostas Karamanlis being named as presidential candidate https://t.co/hXWFT7OVnM #Greece

— Teacher Dude (@teacherdude) December 8, 2014

Karamanlis was Greek PM in a New Democracy (ND) government until autumn 2009, when he called an snap election after the full scale of Greece’s debt crisis began to emerge.

He lost to the left-wing Pasok party, which went on to agree two bailout packages and deep austerity, before being replaced by a technocratic leader in 2011. Samaras’s ND party then won power, in a coalition, the next June.

It’s not immediately clear who might take on the heady role of being Greece’s next president.

Which is remarkable, given the first poll is just nine days away!

Antonis Samaras’s spokeswoman Sofia Voultepsi has apparently told local media that no candidates have been named yet; the PM’s speech tomorrow should shed some light.

Greece is holding presidential elections in a week and there are no candidates yet http://t.co/pb0s1rNWv6

— BI: Markets (@themoneygame) December 8, 2014

Brussels insiders are suggesting commissioner Dimitris Avramopoulos, according to the FT’s ever-well-informed Peter Spiegel:

@mvanhulten Smart money in Brussels focusing on @Avramopoulos as likely New Democracy candidate. @YanniKouts

— Peter Spiegel (@SpiegelPeter) December 8, 2014

Megan Greene, chief economist at Manulife Asset Management, has just discussed the Greek developments on Al Jazeera (you can hear it here).

She explains that a bailout extension was “inevitable” (as Greece had not satisfied its lenders that it had hit the targets agreed under its bailout).

Greece still has work to do, she added:

I think a number of structural reforms still need to be implemented. A lot of have been legislated, but not implemented

Megan also predicted that Greece probably need a precautionary credit line even if it does exit its bailout in late February 2015. That would be a line of credit in case it couldn’t borrow in the money markets.

Reax to news in #Greece from @economistmeg on Al Jazeera Listen: http://t.co/RsYdl69aGk pic.twitter.com/CGGvCs9aqc

— Derek Gatopoulos (@dgatopoulos) December 8, 2014

Things are moving fast:

#Greece PM Samaras to give a televised speech tomorrow and announce the govt's pick for the President.

— Yannis Koutsomitis (@YanniKouts) December 8, 2014

Syriza: Samaras will lose

The opposition Syriza party, which is leading the Greek opinion polls, has reportedly predicted snap elections in Greece:

#Greece opposition party #Syriza says presidential vote on Dec 17 will trigger snap elections...about time we had another Eurozone crisis

— RANsquawk (@RANsquawk) December 8, 2014

For that to happen, the government would have to fail three times to get a presidential candidate endorsed by parliament, on votes on December 17, 22, and 27th (although some reports say 29th)....

They need the support of three-fifths of MPs, so 180 of the 300 members of parliament. Currently, the coalition government only holds 155 seats....

Updated

Financial analyst Jens Bastian predicts a dramatic run-up to Christmas.

A highly charged political Christmas forthcoming in #Greece. The outcome of presidential elections will then define the New Year's party.

— Jens Bastian (@Jens_Bastian) December 8, 2014

Greece has brought forward the Presidential vote to December 17th. Potentiality big news for the Eurozone if it leads to fresh elections.

— Duncan Weldon (@DuncanWeldon) December 8, 2014

The BBC’s Mark Lowen, who covered the 2012 Greek debt crisis from Athens, agrees that Greece is back in the spotlight:

First shot fired in what could be #Greece's leap into the political unknown. If you thought EU's problem child had gone quiet, think again

— Mark Lowen (@marklowen) December 8, 2014

Updated

AP: Greek government gambles with early presidential poll

Bringing forward the Greek presidential elections to the end of December (they were due in February) is a “gamble” by prime minister Samaras, says Associated Press.

Greece’s conservative-led government has called for a vote in parliament for the country’s new president late this month - in a surprise move that will determine its survival in the recession-weary country.

Government spokesman Sofia Voultepsi said late Monday the vote would be held Dec. 17, with possible later rounds held through Dec. 22. The vote had not been expected to be held until late February.

The government needs support from opposition lawmakers to avoid a stalemate and a snap general election, but is trailing in opinion polls to the anti-bailout Syriza party and facing widespread public discontent after a six-year recession.

Earlier Monday, Eurozone bailout lenders backed a Greek request to extend the rescue lending program for another two months.

Did eurozone finance ministers know that Greece was bringing forward its presidential elections, when they agreed to give Athens another two months to deliver the reforms demanded by its Troika of lenders?

Eurozone crisis expert Yannis Koutsomitis wonders what happened behind the scenes.....

Legit Q: Did #Greece's FinMin Hardouvelis inform the Eurogroup on govt's decision to hold early presidential election? /cc @pierremoscovici

— Yannis Koutsomitis (@YanniKouts) December 8, 2014

Updated

Greek developments: early reaction

Nick Malkoutzis of the Kathimerini newspaper explains that the December presidential vote will decide whether prime minister Antonis Samaras will conclude negotiations with the Troika, during the two-month bailout extension agreed tonight:

By moving president vote fwd to Dec 17, gov't turns it into ballot on whether MPs prefer coalition or SYRIZA to finish troika talks #Greece

— Nick Malkoutzis (@NickMalkoutzis) December 8, 2014

More reaction:

Presidential Election in #Greece to kick off on Dec 17. Whatever the outcome, process will be over before New Year's.

— ThePressProject EN (@PressProject_EN) December 8, 2014

#Greece to Start Presidential Election Process Dec. 17. pic.twitter.com/n3icrNBeER

— Holger Zschaepitz (@Schuldensuehner) December 8, 2014

Updated

Reuters reports that Greece will formally ask for a two-month bailout extension tomorrow -- which is a formality now that eurogroup officials have said they’d accept it.

Here’s Reuters’ take:

Euro zone finance ministers are in favour of granting Greece a two-month extension of its bailout program, which Athens will ask for on Tuesday, Eurogroup chief Jeroen Dijsselbloem said on Monday.

The EU had considered extending the current bailout by six months to mid-2015, a document obtained by Reuters showed last week. But Athens had said it was only willing to consider extending the unpopular programme by a few weeks.

“We need an extension,” Dijsselbloem said after euro zonefinance ministers discussed the bailout plan, pointing out that it would not be possible to conclude a review of the program before year-end.

“Let’s do this as quickly as we can, and in our mind that is two months,” he added. “Two months is long enough to complete review and not too long to leave questions open for the future.”

More here: Greece to get two-month bailout extension -Eurogroup’s Dijsselbloem

Greece brings forward presidential elections after two-month bailout extension agreed

Hello again. Some late news breaking involving Greece. Over in Brussels, eurogroup ministers have agreed to give the Greek government a two-month extension to its bailout.

That gives Greece until the end of February to reach agreement with its troika of lenders over the outstanding parts of its loan deal, which was due to expire at the end of December.

Eurogroup chief Jeroen Dijsselbloem explained (via the FT).

“Despite its progress, there’s not enough [done] at this point to conclude this review now or by the end of the year.”

A formal request from Athens will come on Tuesday morning, according to Reuters.

And a few minutes later, Athens announced that it is bringing forward elections to choose its next president. They will begin on December 17, with a second poll on December 22 and a third on December 27.

This is a key test for prime minister Antonis Samaras, given his small majority in parliament. If he can’t gather enough support to win the third ballot (a majority of three-fifths of MPs is needed), Greece would presumably head to the polls for an general election.

And currently, the radical left-wing Syriza party is leading in the opinion polls. It argues that Greece needs debt relief; a prospect that has alarmed some investors in recent days.

Government calls key presidential vote Dec. 17-27, after gaining 2 month extension on bailout review #Greece

— Derek Gatopoulos (@dgatopoulos) December 8, 2014

After some calm months, the Greek crisis is back on the agenda. Here’s some instant reaction from experts on twitter: GW

#Greece - If parliament fails to elect a new President, early elections will be called for January 25 or February 1.

— Yannis Koutsomitis (@YanniKouts) December 8, 2014

Forget Christmas in #Greece this year as the festive season. It will all be about presidential elections and possible early elections.

— Jens Bastian (@Jens_Bastian) December 8, 2014

#Samaras gambles: early presidential elex in #Greece Dec17. If no agreed candidate, new elex in Jan. "Tear up bailout" #Tsipras looks strong

— Mark Lowen (@marklowen) December 8, 2014

More reaction to follow.....

Updated

European markets fall on disappointing data

Weak Chinese trade data and news that Japan had fallen into a deeper recession than expected, not to mention continued weakness in the eurozone has sent shares sharply lower. Commodity companies in particular have come under pressure, with Brent crude falling around 4% to a new five year low of $66.35 a barrel on fears of falling demand and oversupply. The final scores showed:

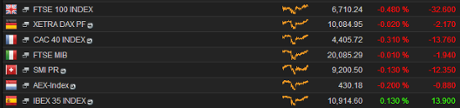

- The FTSE 100 finished down 70.69 points or 1.05% at 6672.15

- Germany’s Dax dropped 0.72% to 10014.99

- France’s Cac closed 1% lower at 4375.48

- Italy’s FTSE MIB fell 0.68% to 19,951.15

- Spain’s Ibex ended down 0.88% at 10,805.2

On Wall Street the Dow Jones Industrial Average is currently down around 60 points or 0.33%.

And on that note, it’s time to close up for the evening. Thanks for all your comments, and we’ll be back again tomorrow.

The US Federal Reserve should be on track to raise interest rates in the latter half of 2015, according to Atlanta Fed president Dennis Lockhart.

But in a speech to a symposium in Atlanta he said with the recent improvements in the economy, including the jobs market, it was a concern that inflation had not yet picked up. He said (courtesy Reuters):

Simultaneous readings of robust job creation...and weak inflation readings are somewhat puzzling. [But] the momentum I perceive in the economy gives me confidence that the Federal Open Market Committee can consider beginning to normalise interest rates in 2015.

More on the Greece deliberations:

Dijsselbloem: Despite the progress there is not enough basis to conclude th review before the end of the year #Greece

— Efthimia Efthimiou (@EfiEfthimiou) December 8, 2014

Dijsselbloem: taking into account time to finalise review, concluded Eurogroup would be favourably disposed to 2 month technical extension

— Open Europe (@OpenEurope) December 8, 2014

Dijsselbloem: asked Troika to prepare factual report on state of play in #Greece for tomorrow

— Open Europe (@OpenEurope) December 8, 2014

Dijsselbloem: Greek request will come in tomorrow, will allow EFSF directors to approve it before end of the year

— Open Europe (@OpenEurope) December 8, 2014

Dijsselbloem: we only briefly discussed future arrangements for Greece, we remain favourably disposed to precautionary credit line

— Open Europe (@OpenEurope) December 8, 2014

Dijsselbloem: any credit line remains dependent on completion of reforms & relevant national approval

— Open Europe (@OpenEurope) December 8, 2014

EFSF to confirm the two month technical extension to Greece by the end of the year, once formally agreed by eurogroup and Greek government

— Tony Connelly (@tconnellyRTE) December 8, 2014

Dijsselbloem: have also extended the use of buffer funds in Greek bank recapitalisation fund for further two months

— Open Europe (@OpenEurope) December 8, 2014

Updated

It appears Greece’s bailout may indeed get an extension:

GREEK BAILOUT TO BE EXTENDED BY TWO MONTHS: DPA

— MineForNothing (@minefornothing) December 8, 2014

To recap:eurogroup to say Greece has 2 mth technical extension to fulfil set tasks, if carried out will be poised for precautnry credit line

— Tony Connelly (@tconnellyRTE) December 8, 2014

In 2 months, *Greek Bailout* will be rebranded in2 *Greek post-Bailout* to be followed by *Greek pre-Bailout 2.0*.

— Constantin Gurdgiev (@GTCost) December 8, 2014

Updated

Financial stability is improving at European banks but the sector is still vulnerable, ratings agency Moody’s has said. In a new report it said:

In most European banking systems, financial stability is improving, but rising bail-in risks and weak profits pose challenges. New EU-wide regulation has enforced higher capital levels, which, through de-risking and better asset-liability matching will improve bank performance, longer term.

However, weak macroeconomic conditions weigh on Europe’s banking sector, and low overall bottom lines implies that the European banking industry remains structurally vulnerable.

“Weak macroeconomic conditions will continue to weigh on Europe’s banking sector in 2015 and banks’ low overall profitability implies that Europe’s banking sector remains structurally vulnerable, meaning that we may see banks making further adjustments to their costs and possibly changes to their business models. European banks’ bottom lines should benefit from declining provisioning costs in 2015, but conduct and litigation charges will remain high,” says Carola Schuler, a Managing Director in Moody’s EMEA Financial Institutions Group. Also, given the pending EU bail-in regime, benign funding costs are likely to rise. It remains to be seen whether banks will be able to pass on to their customers the higher cost of regulation and in particular, any bail-in costs.

The full statement is here:

Mostly negative European banking system outlooks in 2015 owing to new bail-in regimes, despite improving financial stability

Over in Greece officials are putting a positive spin on events today in Brussels. But government insiders are also saying that much will depend on discussions later this week in Berlin. Helena Smith reports from Athens:

Although hopes have been dashed that decisive decision-making will be the order of the day as euro area finance ministers hold their working session, the Greek government is expressing optimism that headway will be made.

“We expect some progress on the basis of what has been said already at the Eurogroup which has called for the speedy completion of the [economic] review which must be concluded in December,” the government spokesperson Sophia Voultepsi told Real radio station.

“Mr Moscovici, himself, said ‘we want to go in the direction of exiting the difficulties Greece is facing,’” she added, referring to statements made earlier by the EU commissioner for Economic and Financial Affairs.

Well-placed sources said auditors representing the country’s troika of creditors at the EU, ECB and IMF may ever return to Athens “as soon as tomorrow” in a bid to wrap up the review.

Despite all evidence to the contrary, Greek officials are also denying that euro area finance ministers are contemplating extending the country’s unpopular bailout programme by six months – a nightmare scenario for the ruling coalition. With the radical left main opposition Syriza party leading in the polls, the government has staked its survival on a hasty retreat from international surveillance.

Prior to his departure to Brussels, the finance minister Gikas Hardouvelis rejected suggestions that the program would be prolonged until mid-2015 – although he stopped short of denying that it could be extended through to March. “I am convinced that the process of the final review will end soon with a positive result,” he told the Greek parliament late Sunday hours before it voted through next year’s budget.

Acknowledging that relations with the troika are “very tense” officials conceded that passage of the budget would be likely to exacerbate negotiations further. Both sides are still at loggerheads over how to plug a fiscal gap in 2015 that the troika maintains is almost certain to be bigger than government forecasts.

Greece’s deputy premier Evangelos Venizelos will also attempt to smooth ruffled feathers when he holds talks with the German finance minister Wolfgang Schauble in Berlin on Wednesday. In blunt comments earlier today, Schauble said there was little chance Athens would receive its last tranche of EU aid by the end of the year.

“Germany, and Schauble in particular, has been very irritated by our desire to exit the bailout by the end of the year,” a senior insider conceded. “Venizelos will explain the environment in Greece to Schauble and underline the dangers of being pushed too far. There are dangers not just for Greece but all of the euro zone if there is a change [of government] and Syriza comes to power,” he said. “Schauble calls the shots and it is going to be a very important meeting.”

Oil continues to slide on worries about oversupply and falling demand, with Brent crude now down 4% to $66 a barrel, a new five year low.

The latest drop follows the weak economic data from China and Japan, raising fears about the state of the global economy.

Morgan Stanley reckons prices could fall as low as $35 briefly, lagging any intervention by Opec which would probably have been made by then. The bank said:

With Opec on the sidelines, oil prices face their greatest threat since 2009, but we expect a volatile 2015 rather than a one-way trade. Without intervention, physical markets and prices will face serious pressure, with the second quarter of 2015 likely marking the peak period of dislocation. But unlike 2009, this is a self-inflicted “crisis”, and the coming oversupply is grossly exaggerated. With only a modest fix required, the market is complacent about potential upside risk, particularly in light of lower prices. We see several factors that could contribute to recovery, potentially as early as 2H15, especially on a constant-currency basis.

Outage risks rise with low prices, effective spare capacity is near zero and Opec or non-Opec intervention (less supply) is still possible. Sustained low prices also risk a supply crunch by 2017 or 2018 related to insufficient investment.

Although near- term fundamentals are less concerning, the risk of material oversupply is high by the second quarter of 2015. Even though dislocations are unlikely to match prior crises, the market is primed to sell any sign of trouble.

The only true floor in an oversupplied market is cash cost (around $35-40 a barrel). We would expect Opec intervention or lost production to prevent this, but the lagged fundamental impact and sentiment could push prices to these levels for a brief period.

The bank cut its average Brent base-case forecast by $28 to $70 a barrel for 2015 and by $14 to $88 for 2016.

Meanwhile Opec member Kuwait said oil prices were likely to remain around $65 a barrel for the next few months.

Updated

Eurozone finance ministers, currently meeting in Brussels, will not make any decision on extending Greece’s bailout programme, Greek newspaper Kathimerini is reporting:

The European Union is considering extending the current bailout by six months to mid-2015, a document obtained by Reuters showed last week. But Athens says it is only willing to consider extending the unpopular program by a few weeks.

“What we really want is to reach good agreements that allow Greece to cut its deficit and carry out the right reforms that will allow it to have a solid economy,” EU Commissioner for Economics and Financial Affairs Pierre Moscovici told reporters on Monday before a meeting of eurozone finance ministers.

“There will be no decision today on an extension of the Greek (bailout) program but I hope a few steps forward will be registered,” Moscovici said, adding he was well aware of the efforts made by Greece.

Greece’s parliament approved next year’s budget in the early hours of Monday, the plan being closest to a balanced budget Greece has produced in more than three decades.

Prime Minister Antonis Samaras is struggling to push through an early exit from the bailout and ensure the survival of his government after a presidential vote next year.

A row with the EU and IMF over a disputed budget shortfall next year has held up the country’s final bailout inspection and plans to exit the aid program. Greece’s lenders are demanding €1.7bn (€1.08bn) in additional measures to hit budget targets next year, something Athens has rejected.

Over in the US and Wall Street has edged lower in common with other global markets, following the disappointing Chinese and Japanese data. The fall in crude oil prices amid continuing talk of oversupply has sent energy shares lower, while McDonald’s has lost around 3% in early trading after a bigger than expected decline in like for like sales.

Despite all that, the Dow Jones Industrial Average is bearing up reasonably well and is currently down 17 points or 0.09%.

Updated

The European Central Bank has released details of its latest covered bonds and asset backed securities programme:

Covered bonds and ABS cumulatively purchased and settled as at 05/12/2014: 20,927 mln and 601 mln respectively http://t.co/QdyMEbhrzR

— ECB (@ecb) December 8, 2014

ECB has bought a total of €21.5 Billion in ABS and Covered Bonds so far. Only €978.5 Billion to go

— zerohedge (@zerohedge) December 8, 2014

Oh, ECB, slow down. You dont want to buy all the avaible ABS at once, do you? ..... #ugh

— Captain EvilStomper (@Makro_Trader) December 8, 2014

Over in Brussels and the Eurogroup has said that none of the draft budget plans produced were in “serious non-compliance” with the stability and growth pact.

So no country was required to resubmit its budget. There were risks in some cases, however. Regarding Italy, for example, the Eurogroup said:

We agree with the European Commission’s assessment that the budget is at risk of non- compliance with the requirements of the stability and growth pact.

While we acknowledge that the unfavourable economic circumstances and the very low inflation rate have complicated the achievement of the debt reduction benchmark and full compliance with the debt rule appears very demanding at this point, the high debt level remains a matter of concern. We note that according to the latest Commission assessment, Italy’s structural fiscal effort in 2015 will be 0.1% of GDP, whereas 0.5% of GDP is required under the preventive arm. On that basis, effective measures would be needed to allow for an improvement of the structural effort.

EU said to tell Italy to make additional budget cuts in 2015 worth 0.4% of GDP Ht @cigolo

— MineForNothing (@minefornothing) December 8, 2014

And elsewhere:

EUROGROUP France's structural fiscal effort in 2015 will be 0.3% of GDP, whereas 0.8% of GDP required under excessive deficit procedure

— Agence Europe (@AgencEurope) December 8, 2014

EUROGROUP Spain: headline deficit will be 4.6% of GDP in 2015, whereas a deficit of 4.2% of GDP is recommended

— Agence Europe (@AgencEurope) December 8, 2014

EUROGROUP Portugal: headline deficit will be 3.3% of GDP in 2015 (measures would be needed to improve the headline deficit)

— Agence Europe (@AgencEurope) December 8, 2014

The full statement is here (PDF).

Updated

There are plenty of reasons behind McDonald’s disappointing sales figures in recent months.

One theory is that lower-income households have not seen their earnings pick up in line with economic growth.

Another is that its customer base is switching to alternative fast foot outlets, as Chelsey Dulaney of Marketwatch explains:

An increasingly complicated menu has slowed service in the U.S. as McDonald’s once-reliable base of younger customers have also defected to fast-casual chains boasting customized ordering and fresh ingredients, including Chipotle Mexican Grill Inc., and specialty-burger chains such as Five Guys.

Updated

November’s weak sales are part of a broader trend at McDonald’s, flags up Bloomberg’s Joe Weisenthal.

Abysmal chart of US McDOnald's comp sales pic.twitter.com/y8puNWUOx6

— Joseph Weisenthal (@TheStalwart) December 8, 2014

McDonald’s has also reminded investors of the problems it has suffered in China.

Back in the summer, a TV investigation showed that a major supplier had been repackaging meat that had passed its expiry date. Operations at the plant were halted, leaving many McDonald’s outlets in China unable to sell items such as burgers and chicken nuggets. Its Japanese restaurants also stopped importing chicken from China.

The “ongoing impact of the supplier issue in China” will knock $0.07 to $0.10 per share of its profits in the current quarter, it says.

McDonald's suffers from falling sales and stronger dollar

Oh dear. McDonald’s latest sales figures are out, and they’re not a pretty sight.

Global sales at the fast food giant fell by 2.2% on a comparable basis in November (ie, stripping out new stores).

- In America, like-for-like sales fell by 4.6%.

- In Europe, comparable sales are down 2.0%.

- And across Asia/Pacific, Middle East and Africa they fell 4.0%

McDonalds November sales disappointment goes large, -2.2% globally vs -1.7% est.

— Mike van Dulken (@Accendo_Mike) December 8, 2014

McDonald’s also warned that the strengthening of the US dollar against “nearly all foreign currencies” will have a negative impact on its profits (as takings at overseas outlets are worth less in dollar terms).

It’s the latest in a string of disappointing results from the company.

President and CEO Don Thompson insisted that McDonald’s is making changes, both in America:

To restore momentum, McDonald’s U.S. is diligently working to enhance its marketing, simplify the menu, and implement a more locally-driven organizational structure to increase relevance with consumers.

And in Europe:

Europe’s comparable sales decreased 2.0% in November as positive performance in the U.K. was more than offset by very weak results in Russia and negative results in France and Germany. While the operating environment remains challenging across most of the segment, McDonald’s Europe remains focused on providing customers with locally-relevant value and premium menu options, including differentiated beverage and breakfast offerings.

Investors are not, er, loving it -- shares have fallen 2.5% in pre-market trading.

Not a great sign - McDonald's is a key US consumer discretionary stock: Americans ditch McD's as sales tumble 4.6% http://t.co/exS1BUV1rm

— Alice Ross (@aliceemross) December 8, 2014

Updated

Lunchtime summary: Not much festive cheers

It’s been a generally downbeat morning, and that’s reflected in Europe’s stock markets.

Weak Asian data overnight, gloomy warnings from the ECB’s Ewald Nowotny and the OECD, and the latest fall in the oil price are all weighing on shares.

And there’s also jitteriness after the influential Bank for International Settlements warned that the strength of the US dollar could cause turmoil in emerging markets:

Strong dollar threatens global economy, warns BIS

The main indices all remain in the red as lunchtime approaches in the City.

So, a quick recap.

Austrian central bank chief Ewald Nowotny has warned of a ‘massive weakening’ in the eurozone economy, with growth and inflation both slowing.

He warned:

“We see a massive weakening in the euro zone economy.”

Nowotny also waded into the row over whether the ECB should launch a big government bond-buying programme, saying QE could be a “valuable” tool.

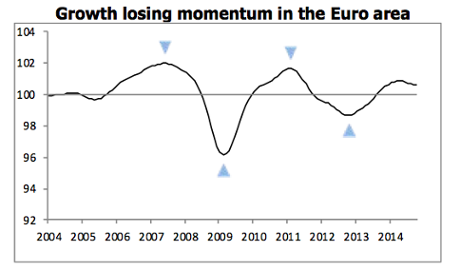

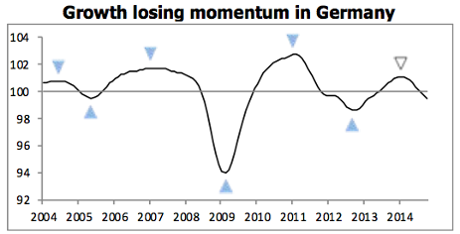

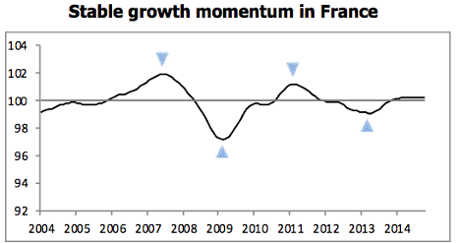

The OECD’s latest data has shown that growth is weakening in Europe, led by Germany and France.

Composite leading indicators (CLIs), designed to anticipate turning points in economic activity relative to trend, suggest that growth will continue to lose momentum in Europe while the outlook is for stable growth momentum in most other major economies and in the OECD area as a whole.

Japan is deeper in recession than first thought; updated GDP data showed it contracted at an annual rate of 1.9% between July and September.

And China has reported a drop in export growth, and a fall in imports.

This cocktail of bad news pushed the oil price steadily down - Brent crude fell below the $67/barrel mark a few minutes ago, a new five-year low.

Brent getting crushed again today. 42% drop since June. Stunning. pic.twitter.com/htrMGfZtuK

— Jonathan Ferro (@FerroTV) December 8, 2014

And the dollar has continued to rally today, making fresh gains against emerging currencies:

EM currencies slide to lowest since at least 2000 http://t.co/KAD4YCsbS9 pic.twitter.com/032qnOUw3Y

— Robin Wigglesworth (@RobinWigg) December 8, 2014

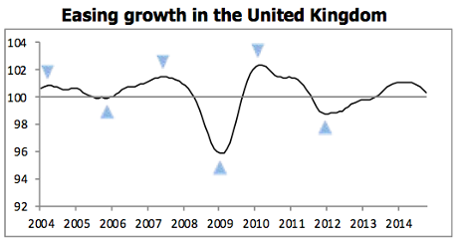

OECD: Growth is weakening in Europe

The OECD has piled fresh pressure on the ECB, and eurozone politicians, by warning that the euro economy is slowing.

Echoing Ewald Nowotny’s concerns today, the Paris-based organisation predicted that “growth will continue to lose momentum in Europe”, particularly in Germany and Italy.

France’s growth momentum will be “stable”, it suggested, while UK will also ease back after robust growth.

The broader outlook is for “stable growth momentum in most other major economies and in the OECD area as a whole”, it said in its latest Composite Leading Indicators (CLIs) (which are online here).

The OECD sees:

Stable growth momentum in the United States, Canada, China and Brazil while tentative signs of a positive change in momentum are emerging in Japan. The CLI for Russia points to growth tentatively losing momentum.

India is the only major economy where the CLI points to a clear pick-up in growth momentum.

Here’s the state of play:

- OECD Area: Stable growth momentum

- Euro Area: Growth losing momentum

- Canada: Stable growth momentum

- France: Stable growth momentum

- Japan: Tentative signs of a positive change in momentum

- Germany: Growth losing momentum

- Italy: Weakening momentum

-

United Kingdom: Easing growth

- United States: Stable growth momentum

- Brazil: Stable growth momentum

- China: Stable growth momentum

- India: Growth gaining momentum

- Russia: Growth tentatively losing momentum

Updated

Over in Brussels, eurozone finance ministers have convened for the monthly Eurogroup meeting.

They’ll be considering what to do about Greece. The Greek government passed its 2015 budget last night but has not yet reached agreement with its lenders to unlock its last aid payment from Europe.

Greece has admitted that ‘technical problems’ might mean the bailout lasts a few more weeks; some eurozone officials are reportedly considering a six-month extension.

#Eurogroup meeting today to assess eurozone member states' draft budget plans for 2015 and to discuss Greece's economic adjustment programme

— Pierre Moscovici (@pierremoscovici) December 8, 2014

#Germany finance minister #Schaeuble expects #EU governments to 'find a way' for #Greece #EUROGROUP #ecofin

— Karl Stagno-Navarra (@ksnavarra) December 8, 2014

EU's Moscovici: No decision on today on #Greece bailout extension - @reuters

— Piers Scholfield (@inglesi) December 8, 2014

The oil price is weakening this morning, hitting new five-year lows on speculation that a supply glut is building up.

Brent crude hit $67.35 per barrel, the lowest since October 2009.

It offers consumers around the globe the prospect of cheaper fuel and energy bills, and also poses more deflationary problems for central bankers.

Today’s weaker-than-expected Chinese import and export data is also pushing down the oil price, as it may indicate the global economy is slowing.

Alastair McCaig, market analyst at IG, comments:

Last night’s high jump in China’s trade balance figures has seen commodity and mining stocks in the FTSE lose some of their appeal.

Nowotny: QE could be valuable

Austria’s Ewald Nowotny has gone on to express support for a full-blown quantitative easing programme in the eurozone:

Reuters has the details:

Extending European Central Bank asset purchases to government bonds, or quantitative easing, can play a valuable role in addressing the economic weakness of the euro zone, a senior ECB policymaker and head of Austria’s central bank said on Monday.

Asked whether a programme of quantitative easing would be sensible in addressing the weakness of the euro zone’s economy, Ewald Nowotny said: “As a supportive measure in the context of a comprehensive plan, it can certainly be valuable.”

(scroll back to earlier post for Nowotny’s earlier comments)

Euro lower as #ECB's Nowotny changes language. Says ECB sees massive weakening of Eurozone economy. pic.twitter.com/pzzUc0tu1o

— Holger Zschaepitz (@Schuldensuehner) December 8, 2014

Updated

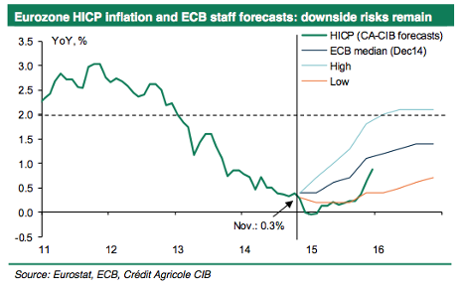

Ewald Nowotny also warned that there is a “high probability” that eurozone inflation would slow further in the coming months, from 0.3% in November.

That makes sense, given recent tumbles in energy prices. Credit Agricole suggested last week that eurozone inflation could dip briefly below zero in early 2015.

The latest ECB staff forecasts, though, reckon it won’t:

Updated

This chart shows how Ewald Nowotny’s dovish comments has pushed the euro down to its lowest point since August 2012:

Updated

ECB's Nowotny: Eurozone is suffering a massive weakening

A senior European Central Bank policymaker has warned that the eurozone economy is suffering a “massive weakening”, sending the euro down to a new two-year low.

Ewald Nowotny, a member of the European Central Bank’s governing council, threw his weight behind president Mario Draghi’s plan to drastically expand the ECB’s balance sheet, despite opposition.

Nowotny also indicated that a full-blown QE programme may be needed.

He told a conference in Frankfurt that:

“We see a massive weakening in the euro zone economy.”

adding:

“The balance sheet of the ECB should reach the levels at the start of 2012, a level which is around 1 trillion euros higher than it is now,”

Last week, the ECB was split down the middle over this issue. Half of the six-strong executive board opposed Draghi’s decision to make the €1trn balance sheet expansion an ‘expectation’, not a mere ‘intention’.

According to Reuters, Nowotny (who is Austria’s central bank chief) said that the main focus of discussion on any further ECB asset purchases would be on buying sovereign bonds.

The pros and cons of such a move into full-blown quantitative easing would be debated, he added. (debated fiercely, I’d suggest).

This has sent the euro down to $1.2253 against the US dollar, a new two-year low.

Very bearish comments from Nowotny. Did the dog eat the recovery again?

— MineForNothing (@minefornothing) December 8, 2014

EUR/USD moving lower this morning on dovish comments from #ECB Nowotny, though seemed largely in line with Draghi pic.twitter.com/qk2pCa7nXL

— Open Europe (@OpenEurope) December 8, 2014

Updated

Shares in Marks & Spencer have fallen over 3% this morning, after it made a stumbling start to the crucial Christmas period.

Problems at M&S’s Castle Donington distribution centre has forced it to delay online orders for several days, up to a fortnight in some cases.

As my colleague Sarah Butler reported last night:

Disappointed customers have been complaining on social media about delays to their orders which have been caused by problems at the retailer’s distribution centre in Castle Donington, Leicestershire, which opened in May last year.

While some orders have been delayed by up to two weeks, next-day deliveries to customers’ homes have been taking up to two or three days and M&S has withdrawn its next-day deliveries to stores.

The company admitted it had been forced to extend delivery times after its Black Friday weekend promotions as its distribution centre could not keep up with demand.

Full story: Marks and Spencer customers hit by delays to online shopping orders

One example:

@marksandspencer poor service from M&S who supposedly prides itself on delighting it's customers !!ordered Xmas tree 24th nov STILL WAITING!

— Gareth (@gazbroc) December 6, 2014

Updated

Weak Asian data hits European markets

Jasper Lawler of CMC Markets confirms that the gloomy news from Asia has dampened the mood in Europe’s markets:

An implosion in Chinese trade data and a bigger than expected Japanese contraction in the third quarter demonstrate the constraints that Asia’s two largest economies are putting on global growth.

Mike van Dulken of Accendo Markets agrees that the “host of disappointing macro-economic data overnight” has hit sentiment:

Japanese GDP confirmed that Q3’s recession is worse than previously estimated (annual and quarterly) along with a worsening October Trade deficit and decline in November business sentiment surveys.

This is coupled with a Chinese November Trade Surplus rising to an unexpected record high, but at the expense of growth in both exports and import, with the former slowing markedly and the latter actually dropping into contraction suggesting a worsening of the slowing growth trend in the world’s second largest economy.

Updated

China’s stock market spiked after its disappointing trade data hit the wires.

The main Shanghai index leapt by over 4%, driven by predictions that the Beijing government might launch more stimulus measures.

China’s stock market has been on an absolute tear in recent weeks, seemingly driven by a surge of retail investors, as these tweets show:

One scary chart as China stock mkt surges on. Up 50% since summer and highest for nearly 4 yrs. chart via @FT pic.twitter.com/MaPGhGq5or

— George Magnus (@georgemagnus1) December 8, 2014

Retail investors just opened the most new accounts in China in 3 years last week. http://t.co/Y5tHxC9gWl pic.twitter.com/EBB9SG6Iqc

— Joseph Weisenthal (@TheStalwart) December 7, 2014

Updated

The triple-whammy of bad news from Japan, China and Europe has hit Europe’s stock markets.

The main indices are all in the red:

- The FTSE 100 is down 28 points, or -0.4%, at 6715.

- The German DAX is down 25 points, or -025%, at 10061.

- The French CAC is down 16 points, or 0.4%, at 4402.

Europe opens in the red with DE Industrial Production miss adding to bigger JP Q3 recession and CN trade data adding to slowing growth fears

— Mike van Dulken (@Accendo_Mike) December 8, 2014

Weak Chinese trade data fuels slowdown fears

The third piece of gloomy news this morning comes from China.

The latest trade data was much weaker than expected, bolstering fears that the world economy is slowing.

Chinese exports rose by just 4.7% in November compared with a year ago, barely half as much as expected. And imports fell by 6.7% year-on-year.

That left it with a huge trade surplus of over $54bn, and left economists fretting that China, and the global economy, are both slowing:

Associated Press explains:

The decline in trade numbers probably was due in part to a crackdown aimed at ending misreporting by traders as a way to evade Chinese capital controls, but also indicates the underlying activity is weakening, said Julian Evans-Pritchard of Capital Economics in a report.

“The magnitude of the fall suggests that underlying export growth has weakened too,” said Evans-Pritchard. As for imports, “the sharp fall also hints at a further cooling of domestic demand.

Full story: Surprise fall in China imports as exports also slow

Carsten Brzeski, economist at ING, is hoping that Germany’s “soft spell” is coming to an end, despite October’s small rise in industrial production.

The German economy should soon benefit from the weak euro and falling oil prices, something he dubs “a very special stimulus package”:

As experienced in the past, the German economy is one of main beneficiaries from lower energy prices and a weaker exchange rate.

This positive effect should start to kick in in the coming months.

And that would presumably further dampen any enthusiasm for other stimulus packages, such as a QE programme from the ECB....

German industrial output misses forecasts

The early news from Europe isn’t too cheery either; German industrial production rose by less than expected in October.

New figures showed that industrial output rose by just 0.2% in October, missing forecasts of growth of up to 0.4%.

And September’s figure have been revised down, from a 1.4% increase to 1.1%.

It suggests Europe’s largest economy struggled to bounce back strongly from its summer slowdown, having narrowly avoided a recession.

Ulrike Kastens, economist at Sal Oppenheim, says:

“German industry had a weak start to the fourth quarter but given the better order levels, we expect a strong development in the coming months.”

German industrial frustration.

— Frederik Ducrozet (@fwred) December 8, 2014

The agenda: Japan falls deeper into recession

Good morning, and welcome to our rolling coverage of the world economy, the financial markets, the eurozone and business.

A new week begins with bad news from Japan, which is deeper in recession than first feared.

Revised data published overnight shows that the Japanese economy shrank at a annual rate of 1.9% in the third quarter of 2014. That dashes hopes that the first estimate, of a 1.6% contraction, would be revised higher.

Alarmingly, business spending contracted by 0.4%, compared to a first estimate of a 0.2% fall. Economists expected it to have recovered, by 0.9%.

And private consumption was also weak, growing by 0.4% after plunging 5.1% in the second quarter.

The figures come as Japan prepares to head to the polls for a snap election.

Prime minister Shinzo Abe is looking for a mandate to delay the sales tax hike due next year. But this economic weakness also shows that Abe’s three-pronged strategy of monetary easing, fiscal stimulus and structural reforms hasn’t paid off.

Also coming up today...

In the eurozone, finance ministers will be holding their monthly Eurogroup meeting in Brussels. They’ll be considering member states’ draft budgets for 2015 (details here), and also whether to extend Greece’s bailout.

Last night, the Greek parliament voted through its 2015 budget, with prime minister Antonis Samaras declaring that:

“We are exiting the era when bond markets were closed to us and we needed bailout loans to survive”.

But with Greece’s 10-year bond yields still in the “danger zone” over 7%, and a nail-biting vote over the next president looming, the country’s future still looks scary.

And in the UK parliament, PricewaterhouseCoopers and drugs giant Shire face tough questioning on tax avoidance from the Public Accounts committee, from 3.15pm (details).

Updated