/NVR%20Inc_%20building%20sign%20by-%20DCStockPhotography%20via%20Shutterstock.jpg)

Reston, Virginia-based NVR, Inc. (NVR) operates as a homebuilder in the U.S. Valued at $23.2 billion by market cap, the company builds single-family detached homes, town homes, and condominium buildings under the Ryan Homes, NVHomes, and other trade names. NVR provides a number of mortgage-related services to its homebuilding customers and to other customers through its mortgage banking operations.

Shares of this homebuilding giant have underperformed the broader market over the past year. NVR has declined 11.9% over this time frame, while the broader S&P 500 Index ($SPX) has rallied nearly 15.1%. In 2025, NVR stock is down 1.4%, compared to the SPX’s 9.9% rise on a YTD basis.

Narrowing the focus, NVR’s underperformance is also apparent compared to the iShares U.S. Home Construction ETF (ITB). The exchange-traded fund has declined about 8.9% over the past year. However, the ETF’s 7.2% returns on a YTD basis outshine the stock’s dip over the same time frame.

NVR's underperformance can be attributed to recent price weakness, particularly in the Washington D.C. market, which experienced a slowdown. Additionally, the company's asset-light model leaves it vulnerable to tariffs passed on by developers and potential labor cost increases due to new immigration restrictions, which may require higher wages for subcontractors.

On Jul. 23, NVR shares closed down marginally after reporting its Q2 results. Its revenue stood at $2.6 billion, down marginally from the same quarter last year. The company’s EPS declined 10.1% year-over-year to $108.54.

For the current fiscal year, ending in December, analysts expect NVR’s EPS to fall 17.5% to $418.15 on a diluted basis. The company’s earnings surprise history is mixed. It beat the consensus estimates in two of the last four quarters while missing the forecast on two other occasions.

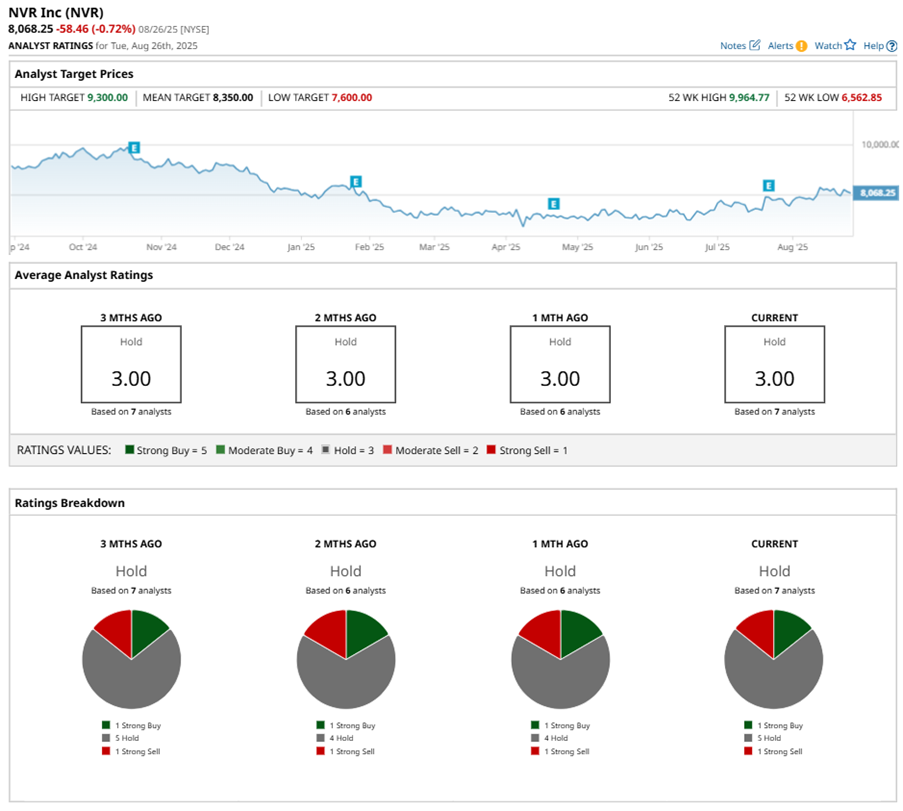

Among the seven analysts covering NVR stock, the consensus is a “Hold.” That’s based on one “Strong Buy” rating, five “Holds,” and one “Strong Sell.”

The configuration has been relatively stable over the past three months.

On Jul. 18, Bank of America Corporation (BAC) analyst Rafe Jadrosich reiterated a “Buy” rating on NVR and set a price target of $8,000.

The mean price target of $8,350 represents a 3.5% premium to NVR’s current price levels. The Street-high price target of $9,300 suggests an upside potential of 15.3%.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.