Oakland, California-based The Clorox Company (CLX) manufactures and markets consumer and professional products worldwide. The company has a market cap of $10.8 billion and operates through Health and Wellness, Household, Lifestyle, and International segments.

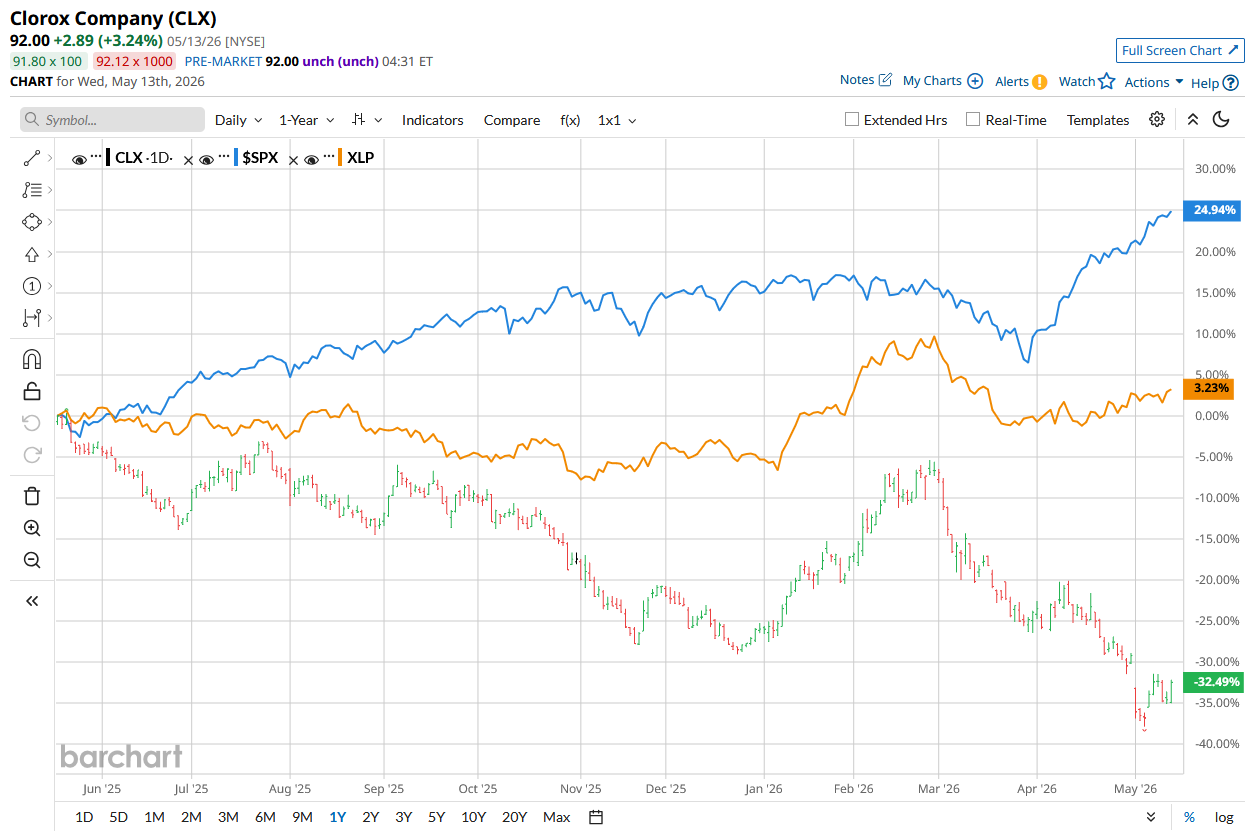

CLX shares have lagged behind the broader market over the past year, declined 32.5% compared to the S&P 500 Index ($SPX) 26.5% surge. Moreover, in 2026, the stock has fallen nearly 8.8%, underperforming the SPX’s 8.8% rise.

Focusing on its industry benchmark, the State Street Consumer Staples Select Sector SPDR ETF (XLP) has risen 6% over the past year, outperforming the stock. In 2026, as well, XLP surged 9.1% and has also outperformed the stock.

On May 1, CLX stock declined 9.7% following the release of its Q3 2026 earnings. The company’s revenue remained flat from the prior year’s quarter at $1.71 billion and surpassed the Street’s estimates. Moreover, its adjusted EPS amounted to $1.64 and also surpassed Wall Street’s forecasts. However, investor confidence was greatly hampered due to the company’s weaker outlook, as management lowered its full-year adjusted EPS guidance by 9.4% to a midpoint of $5.55.

For the current year, which ends in June, analysts expect CLX’s EPS to fall 27.1% to $5.63 on a diluted basis. The company surpassed the consensus estimate in three of the last four quarters, while missing the mark once.

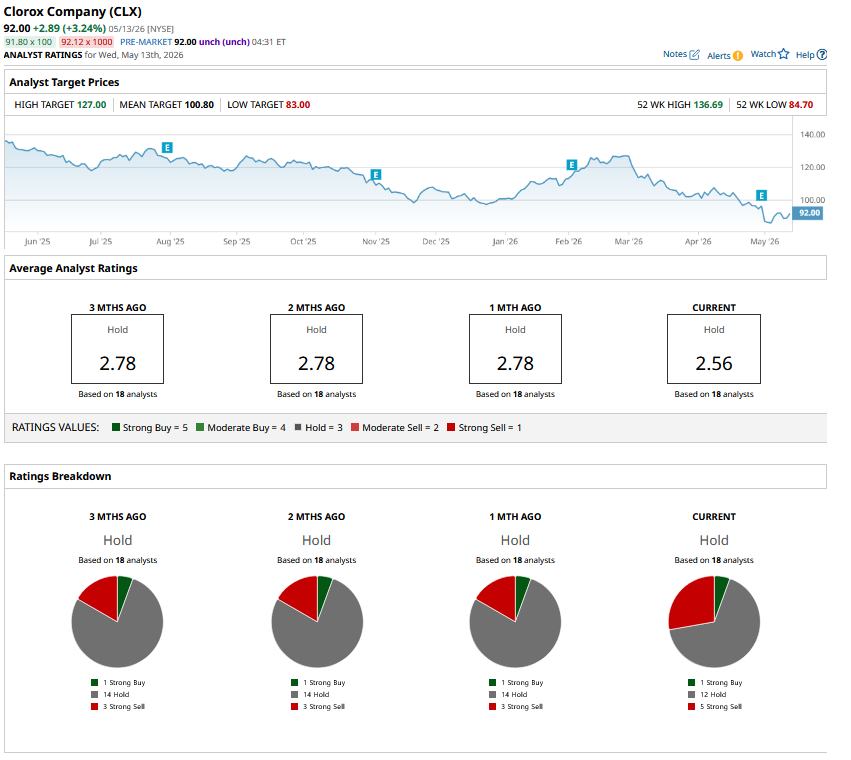

Among the 18 analysts covering CLX stock, the consensus is a “Hold.” That’s based on one “Strong Buy” rating, 12 “Holds,” and five “Strong Sells.”

The configuration has grown more bearish over the past month.

On May 2, Barclays analyst Lauren Lieberman maintained a “Sell” rating on Clorox and set a price target of $102.

CLX’s mean price target of $100.80 indicates a premium of 9.6% from the current market prices. Its Street-high target of $127 suggests a robust 38% upside potential from current price levels.