/Palo%20Alto%20Networks%20Inc%20HQ%20sign-by%20Sundry%20Photography%20via%20Shutterstock.jpg)

Palo Alto Networks (PANW) recently reported its fourth quarter and full year fiscal 2025 earnings. The company not only exceeded the $10 billion revenue run rate (an industry first), but it also laid out a bold vision for leading the next decade of cybersecurity innovation in an era dominated by artificial intelligence (AI).

Palo Alto is a cybersecurity firm that helps businesses, governments, and organizations protect their networks, applications, and data from cyber threats. It generates revenue through a combination of hardware sales and recurring subscriptions and support services, making its business predictable and profitable.

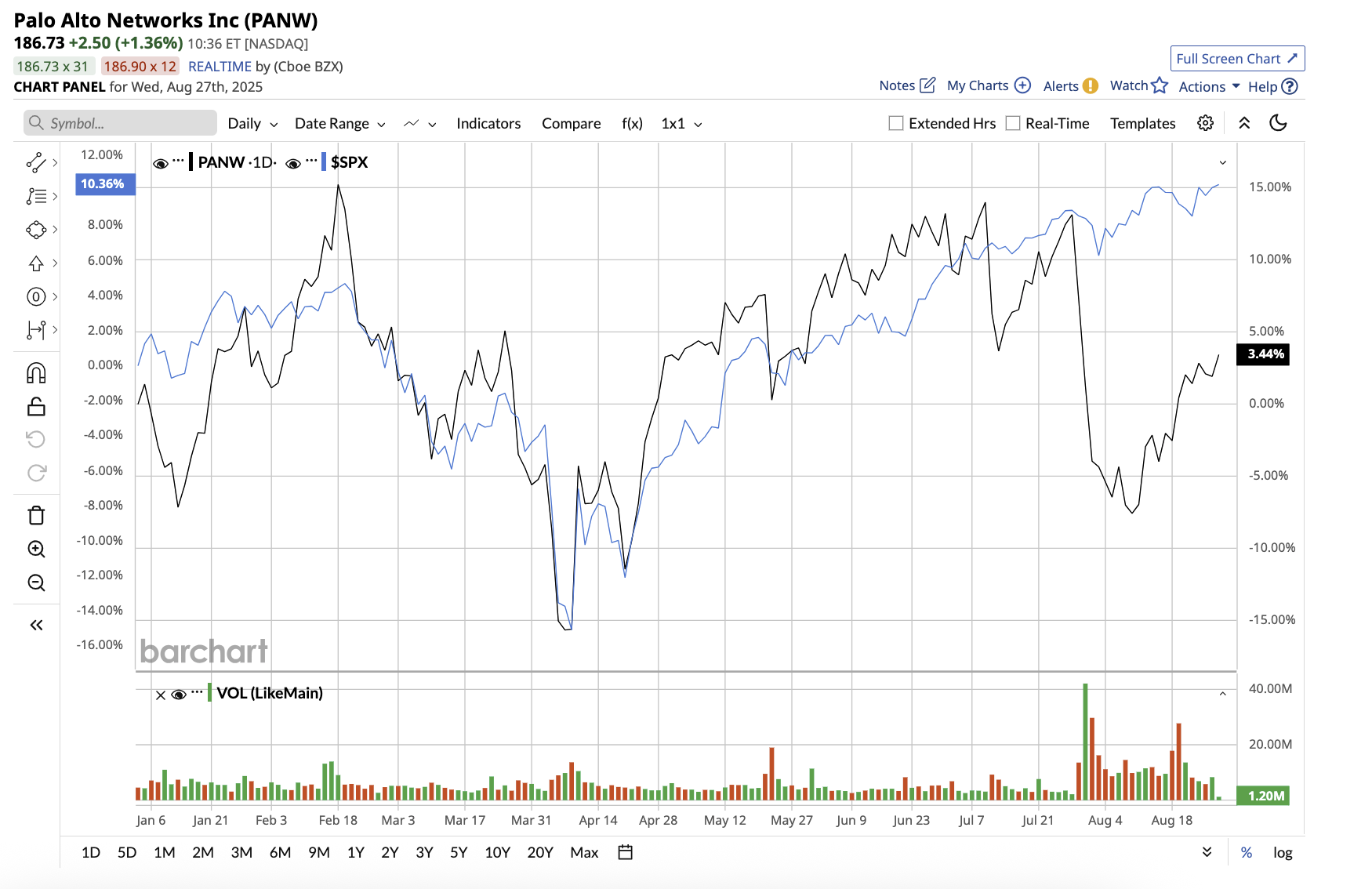

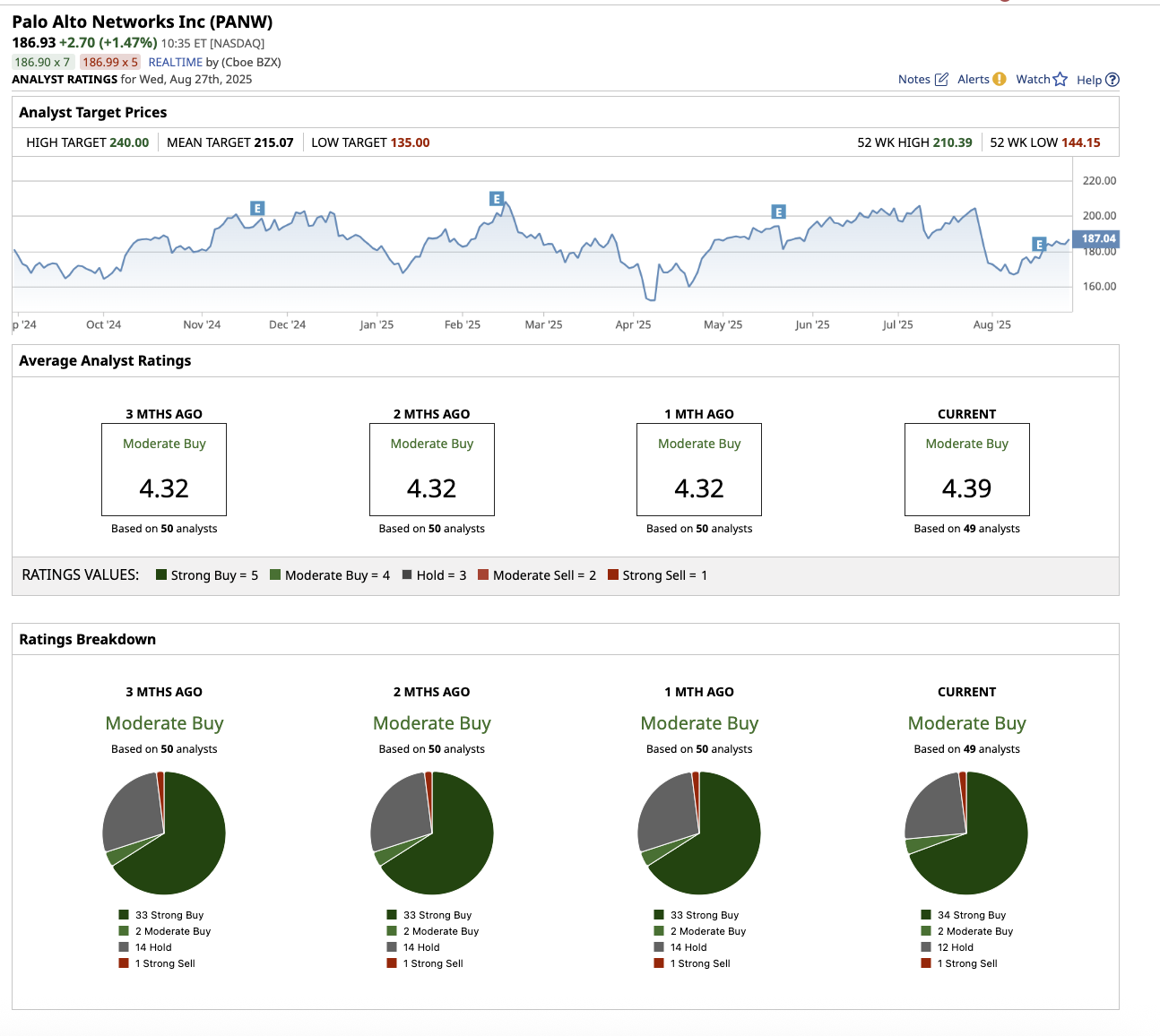

Valued at $122.8 billion, Palo Alto stock is up 3.1% year-to-date, trailing the overall market. Let us see if the stock can gain traction this year and reach Wall Street’s high price estimate of $240.

Palo Alto’s Platforms Are Driving Exceptional Growth

Palo Alto’s portfolio strength is supported by three critical growth drivers, including the Prisma SASE platform, XSIAM, and software firewalls. In the fourth quarter, the company posted its strongest bookings growth in 2.5 years, thanks to large strategic deals, strong renewals, and upsells across its portfolio. Total revenue in the quarter total revenue reached $2.54 billion, growing 16% year-over-year. Product revenue rose 19%, led by software firewalls and PAN-OS SD-WAN, with Services revenue up 15%, driven by 17% growth in subscriptions.

The company stated that 56% of product revenue now comes from software form factors, indicating the company’s shift to next-generation models. Remaining performance obligation (RPO), which measures revenue yet to be recognized, rose 24% to $15.8 billion. Gross margin stood at 75.8%. In fiscal 2025, the company generated $3.5 billion in free cash flow (FCF) and expects to generate 38% to 39% of revenue as FCF in fiscal 2026.

Importantly, the company’s next-generation network security business, which includes software-based solutions such as SASE and software firewalls, increased 35% year on year to $3.9 billion in annual recurring revenue (ARR). This places Palo Alto as the largest and fastest-growing player in next-generation network security at scale. Notably, SASE is the company’s most rapidly growing network security product. It signed a $60 million contract with a global professional services firm for 200,000 seats in the quarter.

Recently, Palo Alto announced a significant strategic shift by entering the identity security market in collaboration with CyberArk (CYBR), a recognized leader in privileged access management (PAM). The company intends to complete the acquisition in the second half of fiscal 2026. Management expects the combined company to generate more than 40% adjusted free cash flow margins by fiscal 2028, supported by integration synergies and expanded customer reach.

With bookings and RPO increasing, a strong deal pipeline, and widespread platform adoption, CEO Nikesh Arora expressed confidence in Palo Alto’s path to achieving its $15 billion next-generation security ARR target by fiscal 2030.

In fiscal 2026, the company anticipates a 14% increase in revenue to around $10.47 billion to $10.52 billion, with earnings growth of around 12% to 15%, in line with analysts’ expectations. In fiscal 2027, analysts expect revenue and earnings to rise by 13.4% and 13.3%, respectively. The stock is expensive, trading at 48 times forward earnings, implying that strong future performance has already been priced in.

What Does Wall Street Say About Palo Alto Stock?

Overall, Wall Street rates Palo Alto stock a “Moderate Buy.” Of the 49 analysts covering the stock, 34 rate it a “Strong Buy,” two rate it a “Moderate Buy,” 12 rate it a “Hold,” and one suggests a “Strong Sell.” The stock’s average target price of $215.07 suggests the stock can rally 15% from current levels. Plus, the Street-high estimate of $240 suggests the stock has upside potential of 28.4% over the next 12 months.

The Bottom Line

With cybersecurity demand on the rise, Palo Alto stands to benefit from long-term growth in the industry. The stock’s bull case is built around its leadership position, strong growth trajectory, and secular tailwind of cybersecurity spending. However, because the stock is currently trading at a premium, investors willing to take some risk should consider buying at $175 level. Others with a low risk tolerance can accumulate shares at around $130 to invest with a margin of safety.