/Lam%20Research%20Corp_%20HQ%20sign-by%20Michael%20Vi%20via%20Shutterstock.jpg)

Lam Research Corporation (LRCX), headquartered in Fremont, California, designs, manufactures, markets, refurbishes, and services semiconductor processing equipment used in the fabrication of integrated circuits. Valued at $122.8 billion by market cap, the company’s products are used to deposit special films on a silicon wafer and etch away portions of various films to create a circuit design.

Companies worth $10 billion or more are generally described as “large-cap stocks,” and LRCX perfectly fits that description, with its market cap exceeding this mark, underscoring its size, influence, and dominance within the semiconductor equipment & materials industry.

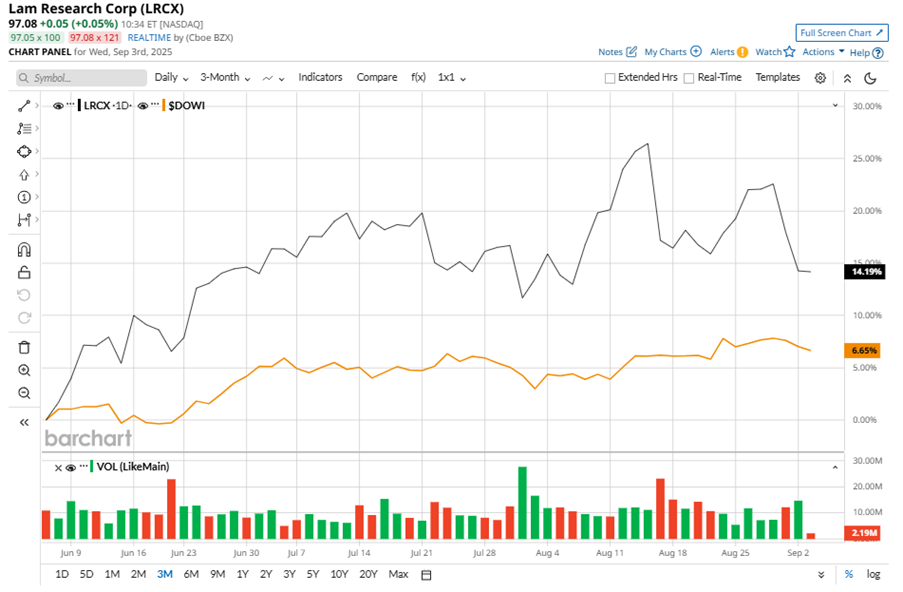

Despite its notable strength, LRCX slipped 10.3% from its 52-week high of $108.02, achieved on Aug. 14. Over the past three months, LRCX stock gained 15.9% outperforming the Dow Jones Industrials Average’s ($DOWI) 6.3% gains during the same time frame.

In the longer term, shares of LRCX rose 34.2% on a YTD basis and climbed 26.6% over the past 52 weeks, outperforming DOWI’s YTD gains of 6.2% and 10.4% returns over the last year.

To confirm the bullish trend, LRCX has been trading above its 200-day moving average since mid-May. However, the stock has been trading below its 50-day moving average recently.

Lam Research reported impressive Q4 results on Jul. 30, with $5.2 billion in revenue and $1.33 in adjusted EPS, both beating expectations. The company's top line surged 33.6% year-over-year, driven by robust demand for its deposition and etch technologies, which resulted in strong gross margins and a record EPS. Despite the stellar performance, Lam Research's shares fell 4.3% in the next trading session, likely due to investor concerns over the company's substantial exposure to China, which poses regulatory and market risks.

LRCX has considerably outpaced its rival, Applied Materials, Inc. (AMAT), which declined 20.1% over the past 52 weeks and 3.1% on a YTD basis.

Wall Street analysts are reasonably bullish on LRCX’s prospects. The stock has a consensus “Moderate Buy” rating from the 32 analysts covering it, and the mean price target of $112.50 suggests a potential upside of 16.1% from current price levels.

On the date of publication, Neha Panjwani did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.