The New York-based Consolidated Edison, Inc. (ED) is a regulated utility company that delivers electricity, natural gas, and steam. The company also invests in electric and gas transmission projects to support energy reliability and grid modernization.

With a market cap of approximately $38.4 billion, Consolidated Edison belongs in the “large cap” category, a group reserved for companies valued at more than $10 billion. The scale enables the company to serve millions of residential, commercial, and industrial customers while operating extensive power transmission, distribution, and natural gas infrastructure.

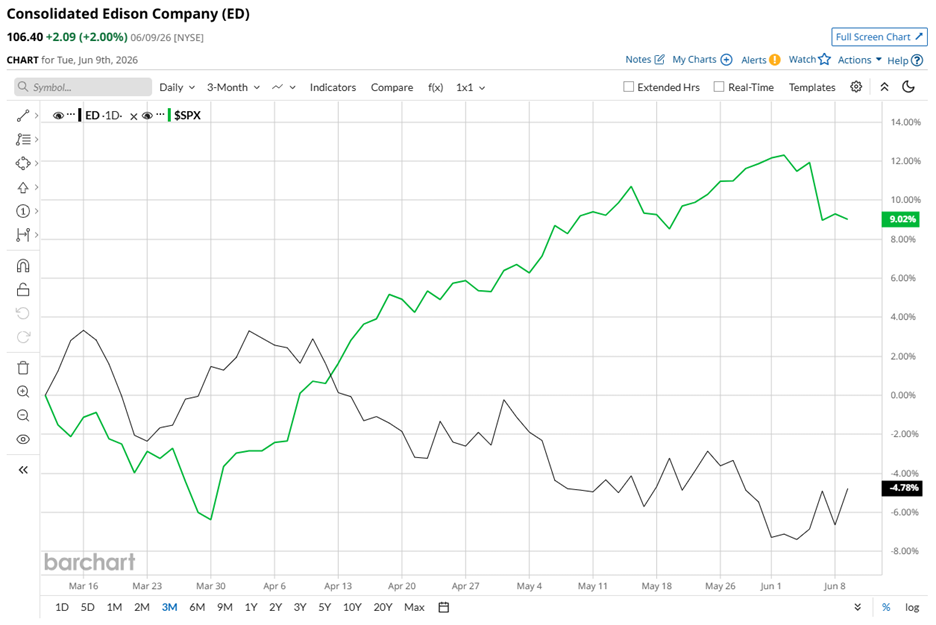

When it comes to price action, ED stock has been slipping behind the curtain. The stock is currently trading 8.5% below its 52-week high of $116.23 reached in March. It has also lost 4.8% over the past three months, while the S&P 500 Index ($SPX) moved the other way entirely with an 8.7% gain over the same stretch.

Zooming out makes the gap feel even more one sided. ED stock has managed a 5.2% gain over the past 52 weeks while the S&P 500 Index climbed 23% in the same period. The story has not improved in 2026 either, since Consolidated Edison shares are down 7.1% year-to-date (YTD) while the index has advanced 7.9%.

Technically, the stock has been stuck in a mild tug of war. It has stayed below its 50-day moving average of $108.86 since mid-April, which signals short term pressure hanging over it. However, it is still holding above its 200-day moving average of $104.11 since mid-January, which suggests longer term support has not given up the fight yet.

Fundamentals added another layer to the picture on May 7 when the company reported Q1 FY2026 earnings results and the stock edged lower again. Revenue climbed 6.2% year over year to $5.1 billion and came in ahead of Street expectations of $4.95 billion. Yet adjusted EPS fell 3.5% from the year ago figure to $2.18 and missed Wall Street expectations of $2.32.

These left investors balancing one beat against one miss without a clear winner. Yet, management leaned into the bigger structural story, pointing out that electrification of heating and transportation is accelerating at an unprecedented pace, powered by long standing state and local policy support, strong customer preference, and steady economic growth across its region.

In fact, the management also reaffirmed its FY2026 adjusted EPS guidance range of $6 to $6.20, signaling confidence despite the mixed quarterly print.

Against that backdrop, peer comparison sharpens the contrast even more. Consolidated Edison’s rival, Entergy Corporation (ETR), has taken a very different route with its shares rising 32.4% over the last 52 weeks and climbing 18.6% YTD. This makes ED’s slower climb look even more measured by comparison.

Even Wall Street has not picked a strong side here. Among 19 analysts covering Consolidated Edison, the consensus rating stays at “Hold” while the average price target of $110.29 implies potential upside of 3.7% from current levels.