Valued at a market cap of $23.1 billion, Church & Dwight Co., Inc. (CHD) manufactures and markets household, personal care, and specialty products. In addition to its dominant retail portfolio, this Ewing, New Jersey-based company is a leading global producer of sodium bicarbonate, supplying industrial, medical, and agricultural markets.

Companies valued at $10 billion or more are typically classified as “large-cap stocks,” and CHD fits the label perfectly, with its market cap exceeding this threshold, underscoring its size, influence, and dominance within the household & personal products industry. The company’s primary strength lies in its highly resilient "Evergreen" business model, which maintains a balanced mix of value and premium products that perform well across all economic cycles.

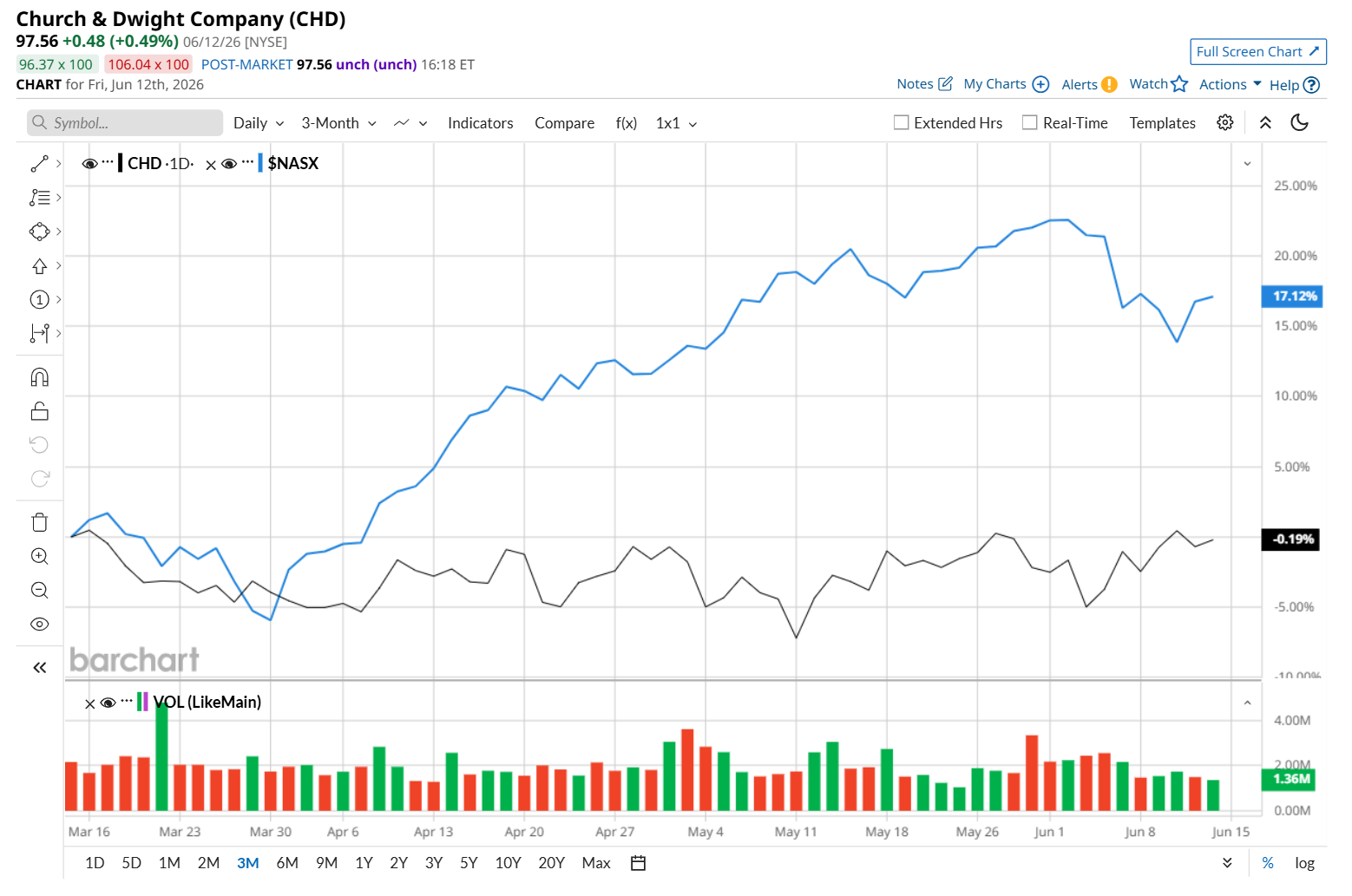

Despite its notable strength, this personal care products manufacturer has declined 8% from its 52-week high of $106.04, reached on Feb. 24. Shares of CHD have declined 1.6% over the past three months, considerably underperforming the Nasdaq Composite’s ($NASX) 16% uptick during the same time frame.

In the longer term, CHD has fallen 1.5% over the past 52 weeks, notably lagging NASX's 31.7% return over the same time period. However, on a YTD basis, shares of CHD are up 16.4%, outpacing NASX’s 11.4% rise.

To confirm its recent bullish trend, CHD has been trading above its 200-day moving average since late January and has remained above its 50-day moving average since mid-May, with slight fluctuations.

On May 1, CHD shares plunged 1.1% after reporting its Q1 results. The pullback occurred despite the top-line figure meeting consensus forecasts at $1.5 billion, representing a robust 5.1% year-over-year increase driven by volume growth and favorable product mix across its retail portfolio. Furthermore, the company reported an adjusted EPS of $0.95, which also surpassed Wall Street expectations of $0.93 and marked a 10.5% growth from the year-ago quarter.

CHD stock has outperformed its peer, The Clorox Company (CLX), which has declined 23.9% over the past 52 weeks and 4% on a YTD basis.

Despite CHD’s recent underperformance, analysts remain moderately optimistic about its prospects. The stock has a consensus rating of "Moderate Buy” from the 20 analysts covering it, and the mean price target of $104.61 suggests a 7.2% premium to its current price levels.