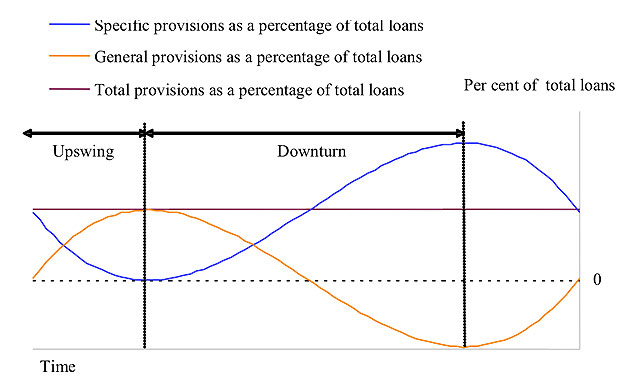

Liquidity

The credit crunch has been driven by the dramatic loss of liquidity in financial markets, sparked by the US sub-prime crisis. Gieve said the instability over the last year has been 'the most severe in living memory'Photograph: Bank of England

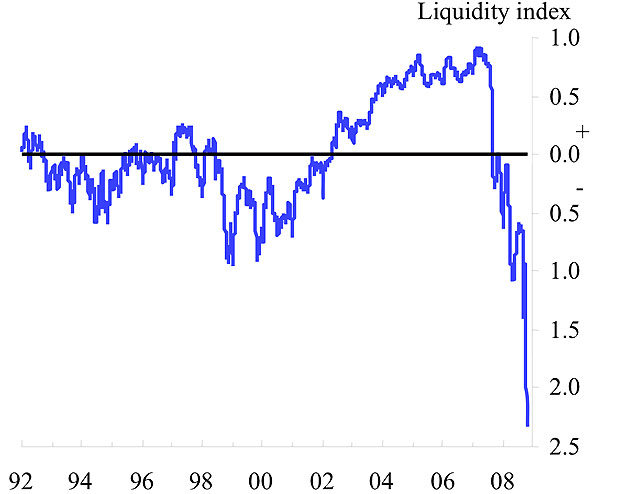

Household consumption

While the current crisis has some similarities to previous downswings there are some significant differences. The last three recessions in the UK in the 70s, 80s and early 90s were preceded by sharp rises in consumption. As this chart shows that was not true of the last few years when consumption was stablePhotograph: Bank of England

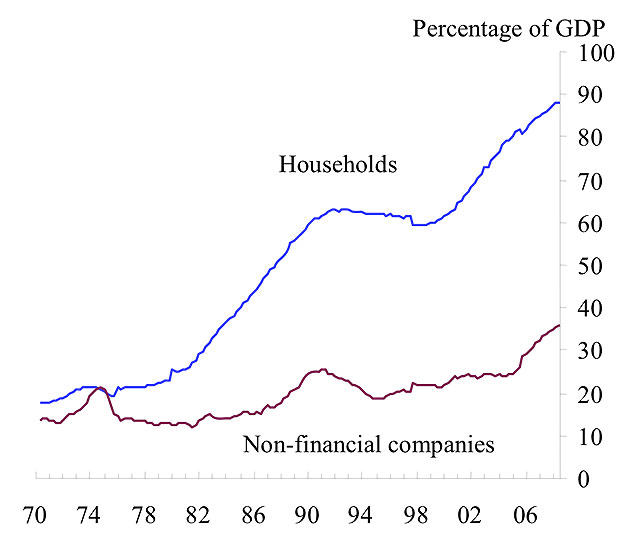

Bank lending to households exploded

Cheap credit fuelled a spectacular expansion of bank balance sheetsPhotograph: Bank of England

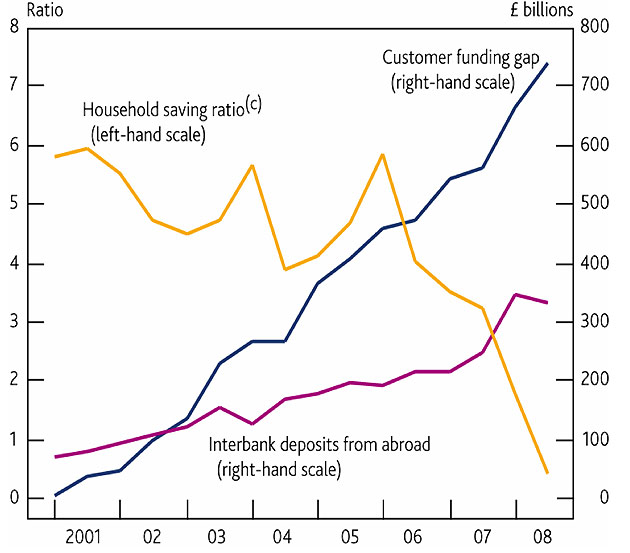

The bank funding gap

As British consumers saved less (yellow line), the gap between how much banks lent and their deposits grew sharply (blue line). To fill the gap, UK banks borrowed more from overseas (purple line)Photograph: Bank of England

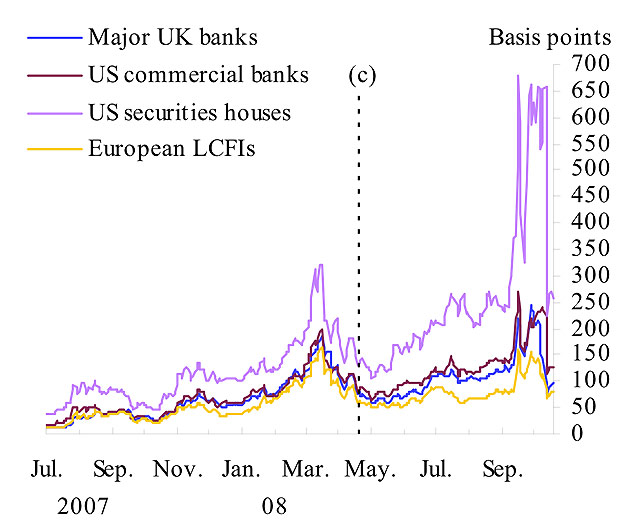

Cost of credit

As the crisis took hold, central banks flooded money markets with extra liquidity but conditions got worse over the summer as worries grew about the downturn in the broader economy and its consequences for bank losses. Credit default swap premiums rose to unprecedented levelsPhotograph: Bank of England

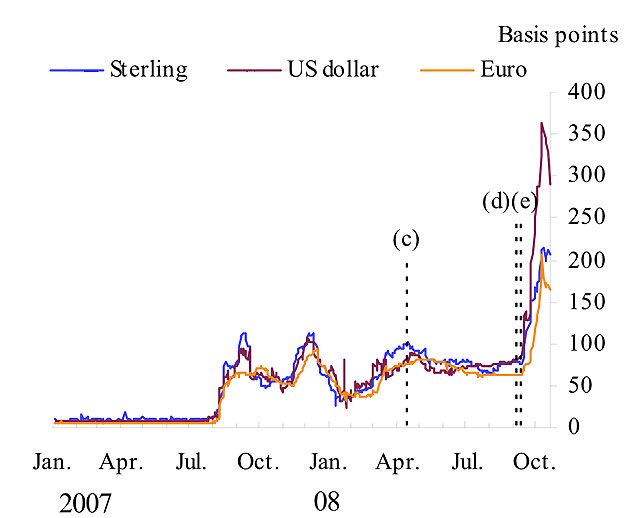

Three-month interbank rates relative to base rates

Interbank lending rates rose sharply and stayed well above central banks' base rates in Britain, the eurozone and the US, making credit increasingly expensive for firms and consumersPhotograph: Bank of England

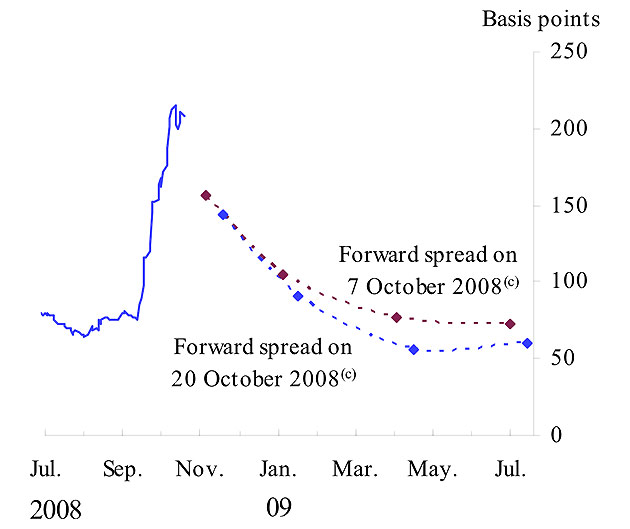

The gap between three-month UK libor and the base rate

In unprecedented coordinated action on October 8, the Fed, Bank of England and ECB announced a package to cut base rates, inject new capital and boost liquidity. Libor spreads have edged down and are now expected to fall a bit further and faster than before the package, Gieve said. This should make credit cheaperPhotograph: Bank of England